Salesforce: Will AI Substitution Theory Wipe Out the SaaS Leader?

02/27 2026

02/27 2026

572

572

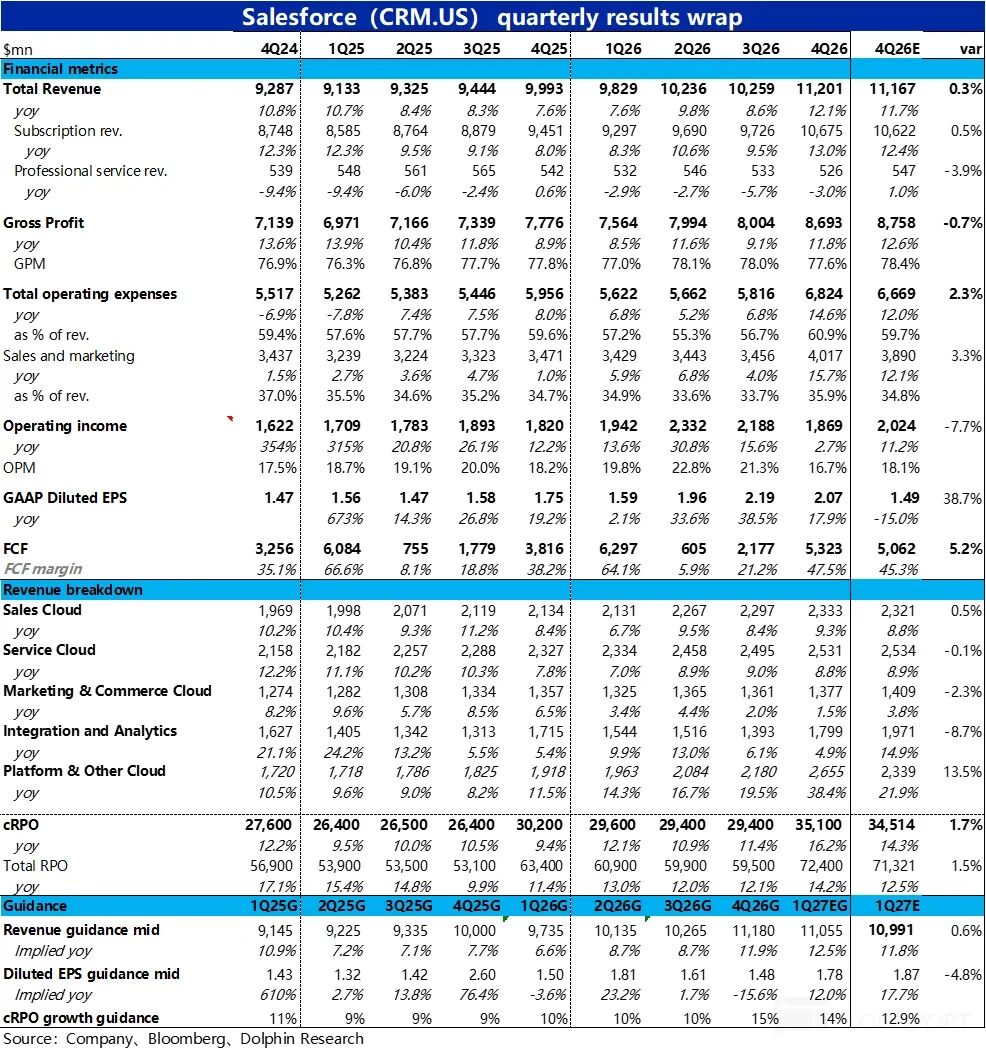

Recently, amid the narrative of 'AI Killing SaaS,' CRM—one of the hardest-hit sectors—released its Q4 FY2026 financial results (as of January 31) after U.S. market close on February 25 (ET). Overall, performance was mediocre.

Revenue growth did accelerate slightly as expected, but this was primarily due to acquisition consolidation. The original business growth remained weak. Gross margin continued to decline under pressure, while expenses increased significantly across the board, causing GAAP operating profit to fall short of expectations. Another core metric—cRPO (current remaining performance obligations) growth—also undershot buyer expectations, leading to negative market feedback.

Detailed analysis:

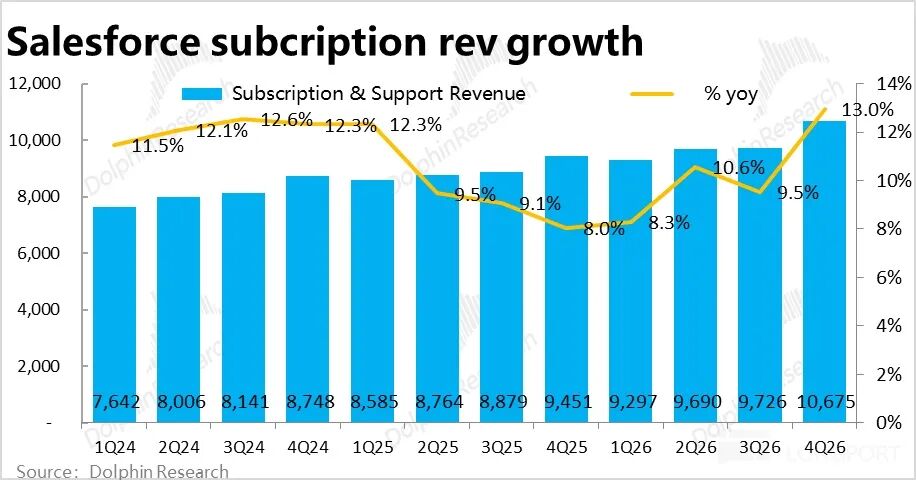

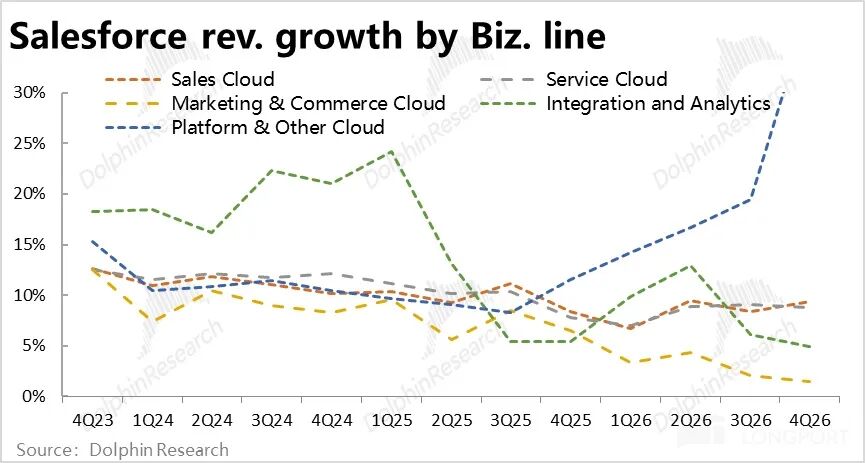

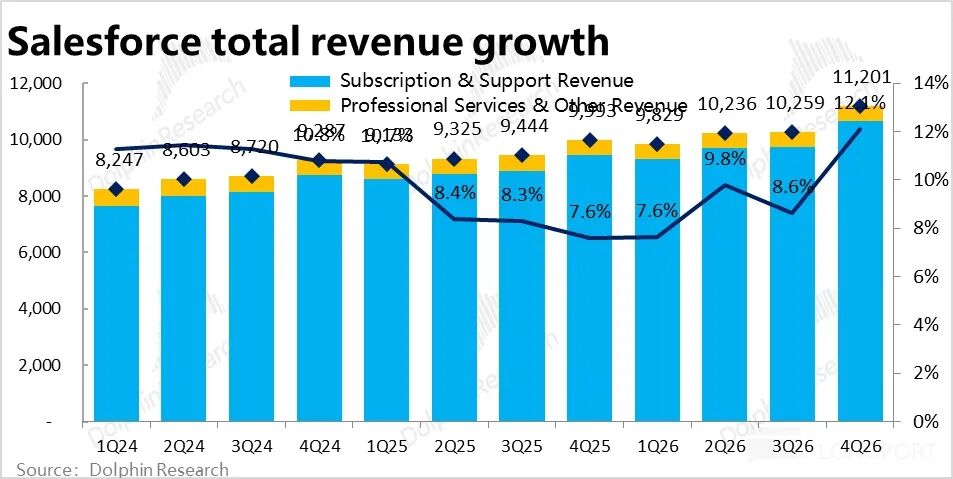

1. Growth appears to accelerate but is actually slowing: This quarter, core subscription revenue grew 13% YoY (11% excluding FX benefits), accelerating by 2 ppts QoQ. However, 4 ppts of this growth came from the consolidation of Informatica. Excluding this impact, the original business growth actually slowed.

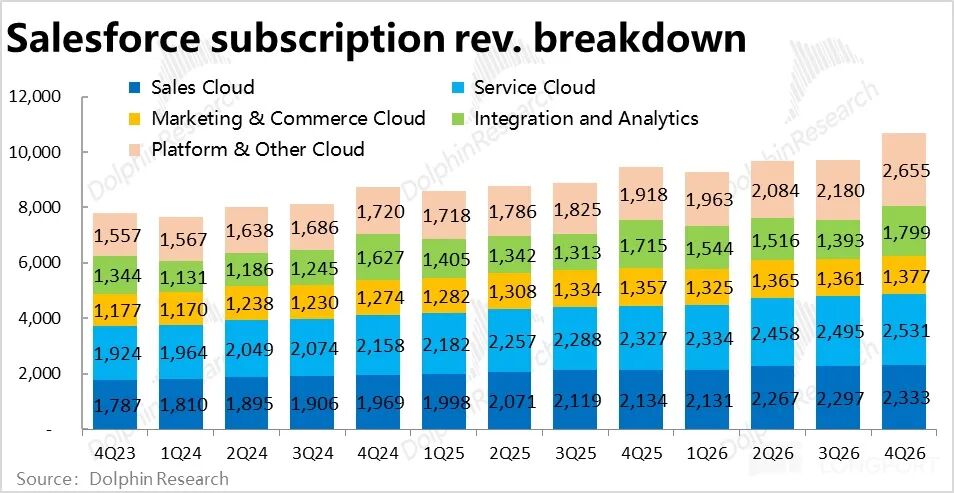

By business line, except for the Platform Cloud (which absorbed Informatica and saw significant acceleration), growth in other segments (at constant currency) generally declined or remained flat QoQ. Despite previous company guidance suggesting revenue growth would bottom out, this quarter showed little improvement.

2. AI revenue accelerated slightly but remains nascent: This quarter, Data & Agentforce annualized revenue reached $2.9 billion, with about $1.1 billion from consolidation. Excluding this, AI-related revenue grew 29% QoQ—the fastest growth since disclosure.

Agentforce annualized revenue hit $800 million, up nearly 170% YoY. The company’s AI business did accelerate slightly. However, in absolute terms, AI-related revenue accounted for less than 7% of total revenue (and under 2% for Agentforce alone). Customer adoption remains in early/trial stages, so 'acceleration' is relative to a small base.

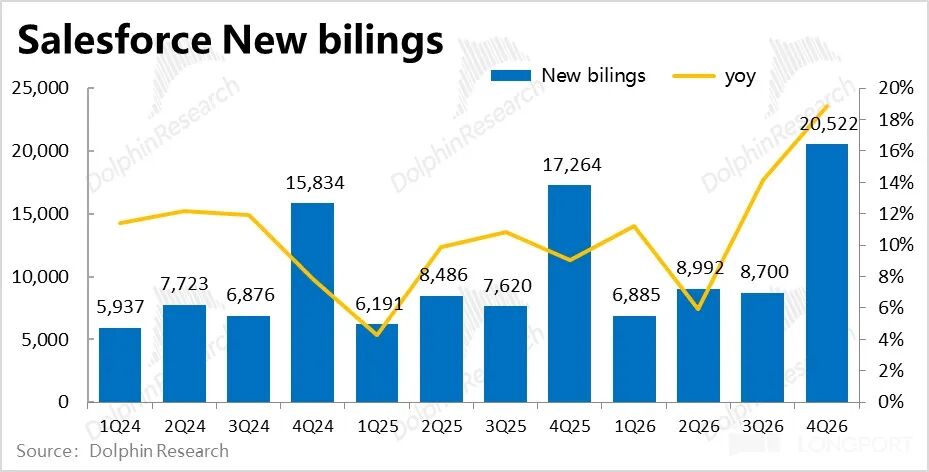

3. Leading indicators also underperformed: Core metric cRPO (current RPO) nominal growth surged to 16% YoY, appearing strong at first glance. But excluding FX benefits, actual growth was 13% YoY, with 4 ppts from consolidation. Excluding this, original business cRPO growth actually slowed QoQ.

Dolphin Research notes that pre-results, optimistic buyers expected 14–15% growth. Actual performance disappointed bullish investors and showed no signs of acceleration.

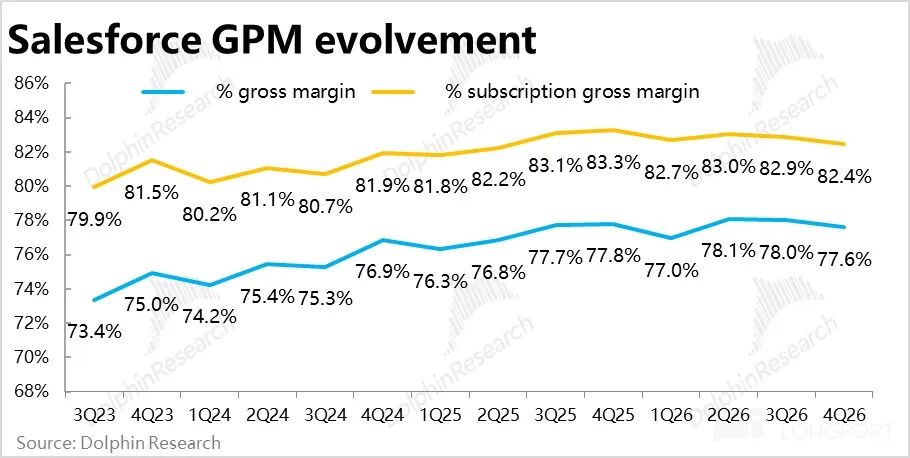

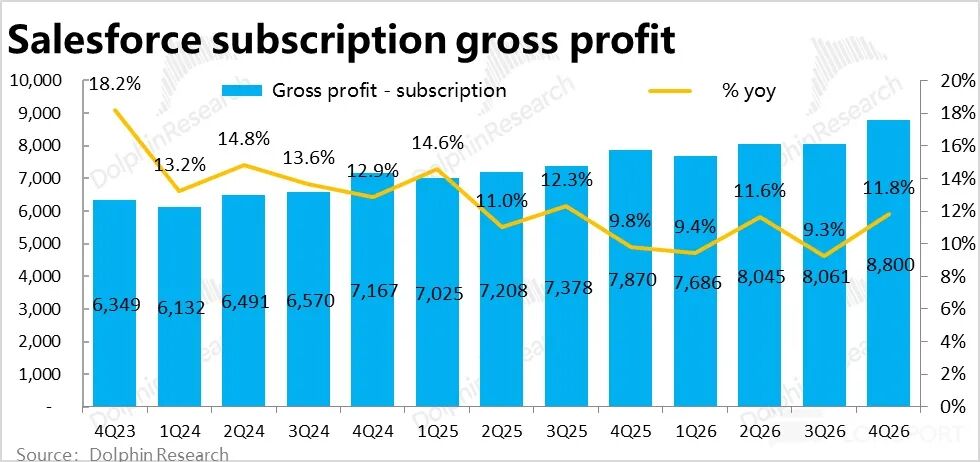

4. Gross margin declined further amid AI investments: Gross margin pressure continued this quarter, falling slightly YoY/QoQ to 77.6% (below Bloomberg’s 78.4% estimate).

Core subscription gross margin was 82.4%, down ~0.5 ppts QoQ and nearly 1 ppt YoY. Dolphin Research attributes this to lower-margin AI businesses like Agentforce, which require heavy backend computing.

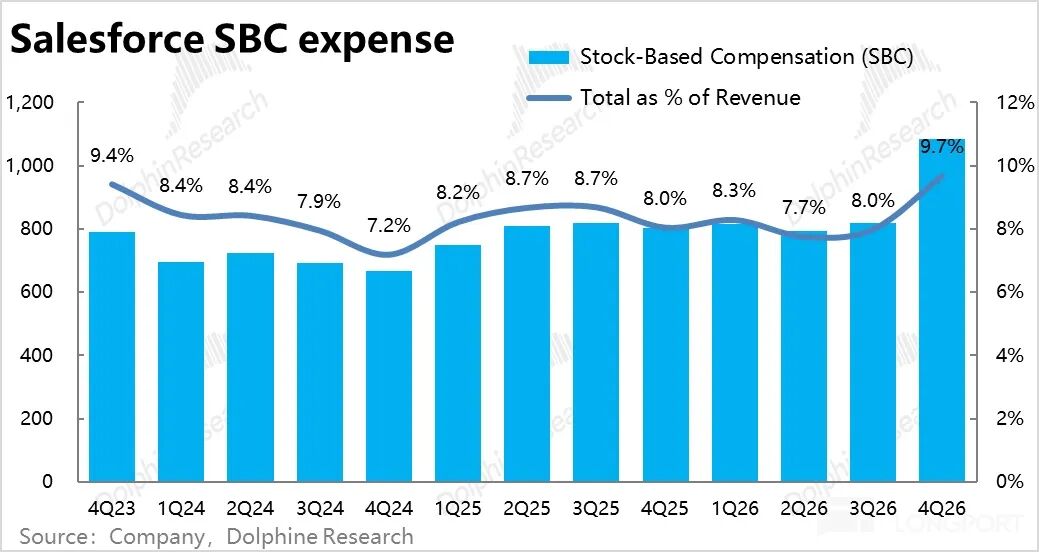

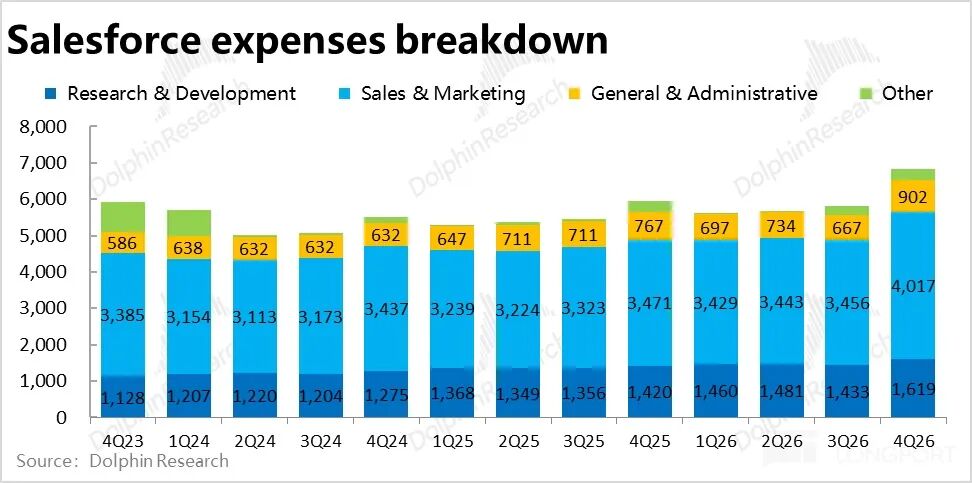

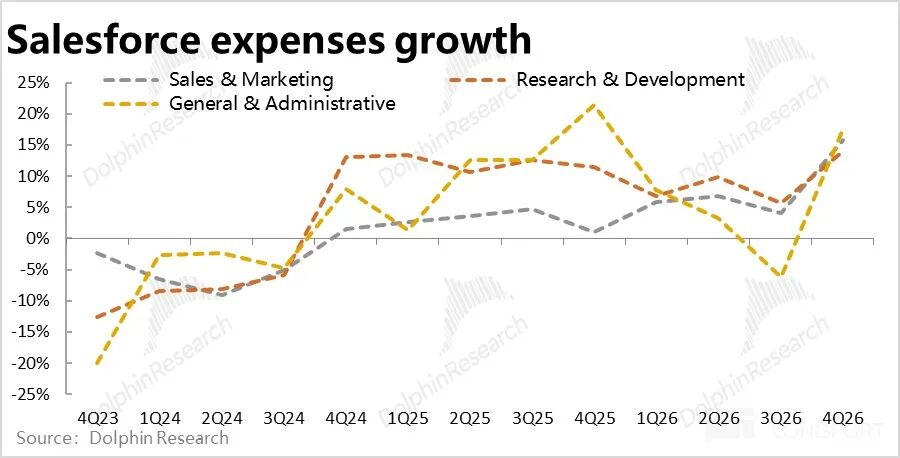

5. Expense growth accelerated sharply: While revenue growth remained flat, total operating expenses surged nearly 15% YoY (vs. single-digit growth in prior years), exceeding both market expectations and revenue growth.

R&D, marketing, and G&A expenses all grew ~15% YoY, indicating all-around spending increases. After strict cost controls last quarter, the sharp pivot suggests management’s strong intent to reignite growth.

6. Margin pressure and expense surge weigh on profits: Flat growth, margin contraction, and rising expenses resulted in a GAAP operating margin of 16.7%, down 1.5 ppts YoY—the first YoY decline since FY2023 (i.e., the 2022 trough post-pandemic).

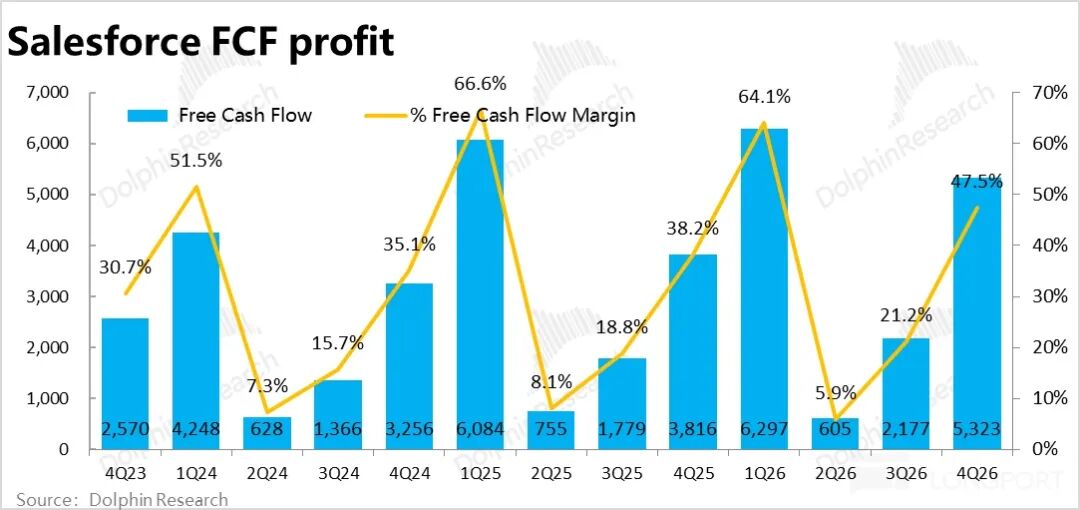

Operating profit reached $1.87 billion, up less than 3% YoY and nearly 8% below Bloomberg’s estimate. Free cash flow (excluding non-cash items like stock-based compensation and operating asset changes), which the company prioritizes, was $5.32 billion—better than expected and prior guidance. The divergence stems from higher deferred revenue recognized on the balance sheet.

7. Shareholder returns remain generous: As promised at the Dreamforce conference, after limited growth, shareholder returns became a key tool to maintain investor appeal. In FY2026, the company spent $14.3 billion on shareholder returns, mostly via buybacks. At current market cap, this equates to an 8% return rate—substantial.

The company also announced a new $50 billion buyback authorization (replacing the previous one), demonstrating strong shareholder commitment.

Dolphin Research’s View:

1. As analyzed, Salesforce’s Q4 performance was underwhelming. Excluding consolidation and FX benefits, original business growth did not accelerate but continued to slow. Management’s pre-year-end guidance of a revenue rebound was not reflected this quarter. (Including FX and consolidation benefits, total revenue growth did recover above 10%, but this lacks meaningful impact.)

Despite over a year of promotion and iteration, AI-related revenue (e.g., Agentforce)—while accelerating—remains a small base and fails to meaningfully drive overall revenue growth.

Meanwhile, higher costs for AI businesses and sharply increased investments (to reignite growth or defend against AI substitution threats) weighed on profits.

The overall impression is mediocre growth and weak profitability.

For next quarter’s guidance:

- Revenue is expected to grow 10–11% YoY at constant currency—similar to this quarter, with a slight uptick. Consolidation will still contribute 4 ppts, roughly in line with Bloomberg’s expectations (i.e., slightly better but no significant acceleration in original business).

- cRPO is guided to grow 13% YoY (constant currency), identical to this quarter. While consolidation’s contribution is undisclosed, there is no acceleration.

- EPS guidance is ~5% below Bloomberg’s estimate (though slightly higher on a Non-GAAP basis). Dolphin Research generally disagrees with excluding stock-based compensation from expenses, so GAAP-based performance remains unimpressive.

Overall, next quarter’s growth will remain steady without clear acceleration, while profits stay under pressure.

2. However, with Openclaw showcasing faster-than-expected AI Agent evolution and rapid iteration of top models like Claude/Gemini, the narrative of 'How AI Will Transform/Revolutionize Software and All Industries' now outweighs earnings performance in impacting stock prices.

Honestly, Dolphin Research believes: a) Existing software giants possess sufficient industry 'know-how' and exclusive data to maintain leadership in the AI era, making AI an enabler rather than a competitor; b) AI could drastically reduce costs for enterprises to develop in-house tools and achieve office automation, rendering 'expensive' SaaS services uncompetitive. Alternatively, as Agents replace employees, the number of billable SaaS seats could collapse. These scenarios could severely damage SaaS profitability.

Which outcome is more likely remains unanswered. What’s certain is high uncertainty—and uncertainty means risk, likely to amplify as AI evolves.

Thus, similar to our view on Uber, while Salesforce’s current performance remains stable with no clear AI disruption yet, the risk of total disruption ('going to zero') warrants a cautious stance in the medium-short term. As the saying goes, 'a wise man does not stand under a precarious wall.'

3. Unlike other SaaS stocks, which could see sharp valuation corrections even if AI doesn’t disrupt them, mature Salesforce has modest valuations with limited downside from pure multiple compression, especially with strong buyback support.

Existing investors need not fear a steep decline, but upside catalysts also remain unclear.

For detailed valuation analysis, see the same name article in the 'Dynamic - Deep Dive (Research)' section of the Changqiao App.

Below are key financial charts and business overviews.

I. Salesforce Business & Revenue Overview

Salesforce pioneered SaaS (Software-as-a-Service) in the global CRM (Client Relationship Management) industry. Its model features cloud-based services (vs. on-premise deployment) and subscription-based pricing (vs. upfront purchases).

Salesforce’s revenue consists of: ① Over 95% from various SaaS subscription services; ② ~5% from expert services (e.g., consulting, training).

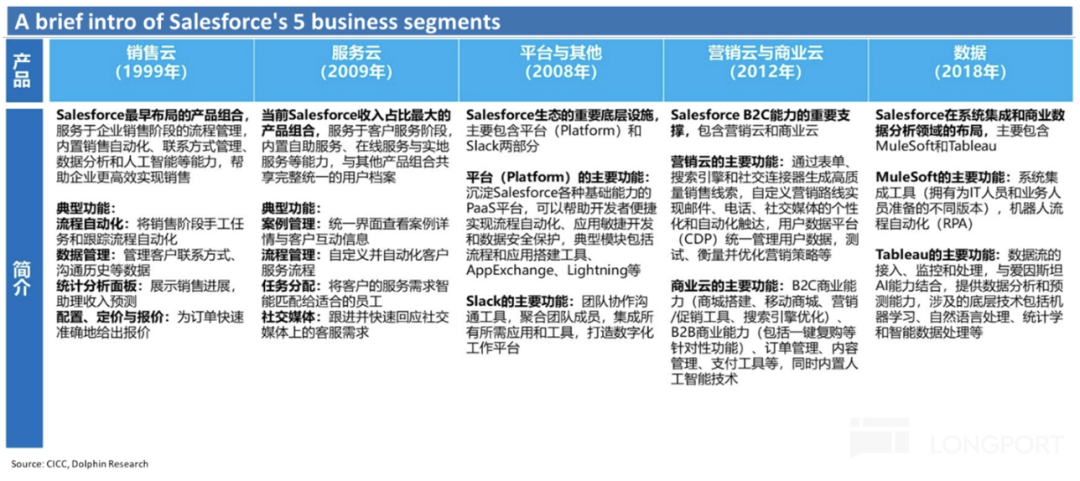

Subscription revenue is further divided into five major SaaS segments with roughly equal revenue contributions:

① Sales Cloud: The core CRM business and company’s oldest offering, providing sales process management tools (e.g., customer outreach, quoting, order management).

② Service Cloud: Another core business, offering customer service tools (e.g., customer information management, online support).

③ Marketing & Commerce Cloud: Marketing Cloud systematizes campaigns via search, social, email, etc.; Commerce Cloud provides e-commerce solutions (e.g., virtual storefronts, order management, payments).

④ Integration & Analytics: Internal database services and business analytics tools, primarily from MuleSoft and Tableau.

⑤ Platform & Others: Infrastructure and services underlying other SaaS offerings (similar to PaaS, or Platform-as-a-Service), including Slack, a team collaboration tool akin to Microsoft Teams.

II. Revenue Growth Appears Accelerated but Remains Mediocre

III. Leading Indicators Appear Strong but Underperform Expectations

IV. Gross Margin Declines Under Pressure

5. Significant Increase in Cost Investment

6. Nearly No Growth in Profit

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Authorization is required for reprinting.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with an independent professional advisor before making any investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available materials and are for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the views expressed in this report shall not, in any jurisdiction, be regarded or construed as an offer to sell or an invitation to buy securities, nor shall they constitute advice, solicitation, or recommendation regarding securities or related financial instruments. The information, tools, and materials contained in this report are not intended for, nor are they to be distributed to, jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials would contravene applicable laws or regulations or result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in such jurisdictions, nor to citizens or residents of such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) produce, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once