Merz's China Visit: German Automakers' Growing Dependence on China

02/27 2026

02/27 2026

496

496

Introduction

German Automobiles: A Bow to Reality

When discussing German automobiles, one cannot ignore the changing tides.

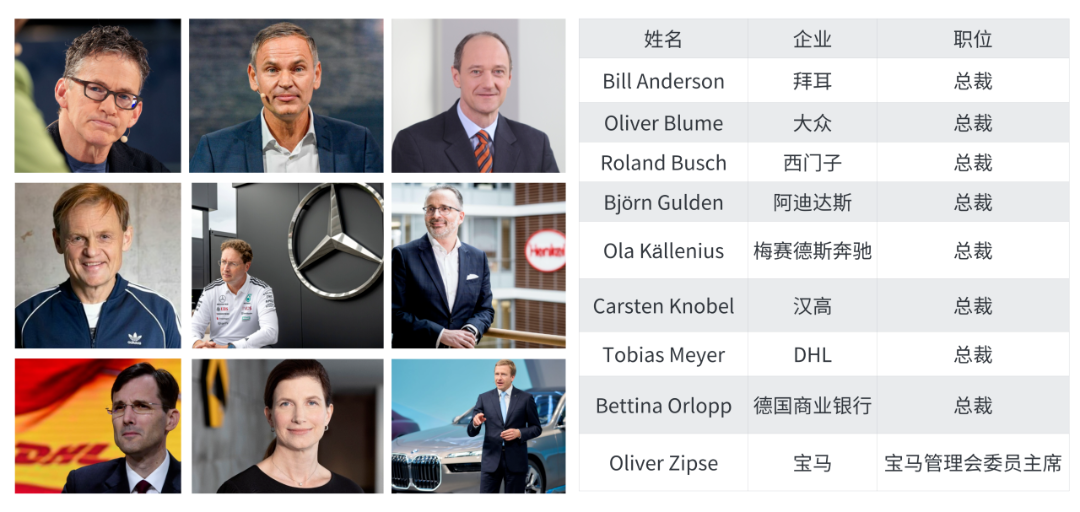

In early 2026, German Chancellor Merz, accompanied by the global leaders of Volkswagen, Mercedes-Benz, BMW, and over 30 core German corporate executives, embarked on a significant visit to China. This high-profile Sino-European diplomatic engagement transcended mere bilateral economic and trade considerations.

As the world's second and third-largest economies, deep dialogue between China and Germany carries significant weight in shaping the international political and economic landscape. For the automotive industry, the full participation of the three German automotive giants, the intensive signing of agreements between Chinese and German automakers, and in-depth discussions between government and corporate leaders clearly indicate that while Sino-German cooperation is mutually beneficial, Germany's automotive sector—and, by extension, its economy—has developed a deeper reliance on China, as evidenced by industrial realities and economic data.

In other words, this visit to China is less about Germany seeking economic and trade "balance" and more about a reversal of fortunes. Amid the wave of electrification and global restructuring, Germany and its automotive industry find themselves compelled to acknowledge China's market and technological prowess.

Merz's visit to China unequivocally placed the automotive industry at the heart of Sino-German cooperation. From the substantive agreements reached to the core content of government-enterprise discussions, it marks a formal transition in Sino-German automotive collaboration from the past "market-for-technology" model to a new phase of "bidirectional technological co-creation." Behind every cooperation initiative lies the urgent demand from German automakers for Chinese technology and supply chains.

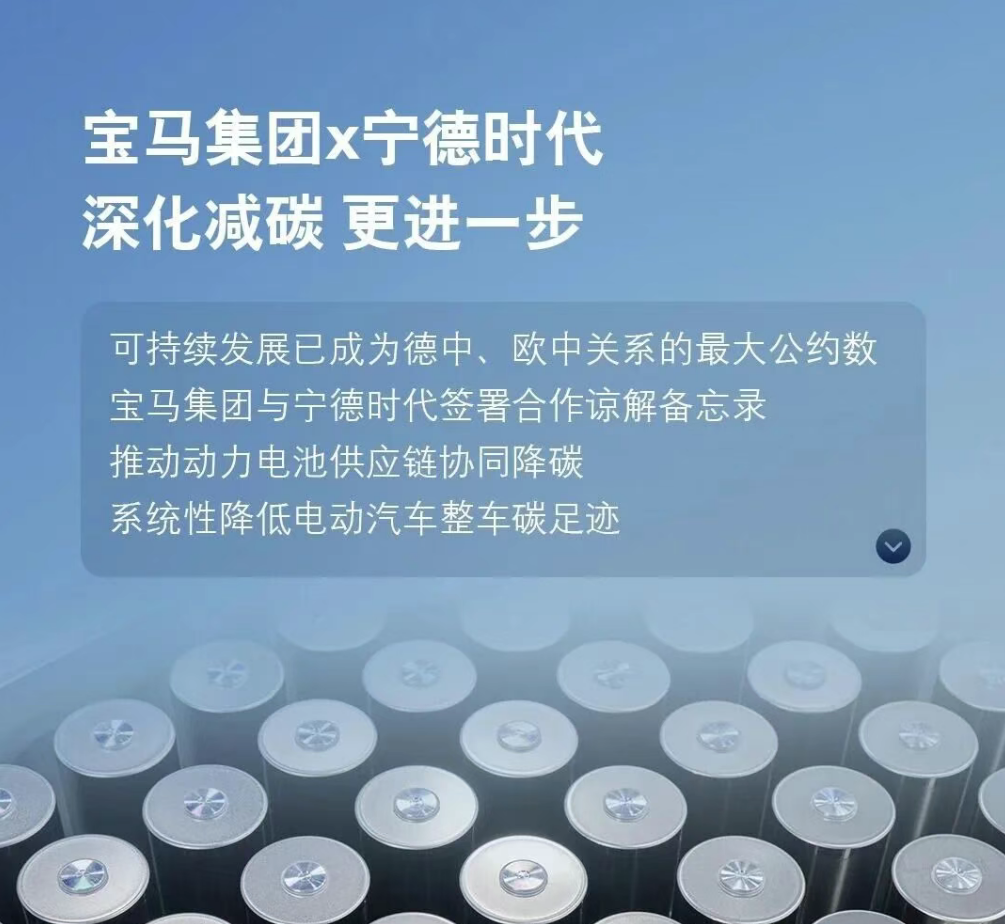

BMW signed a memorandum of understanding with CATL regarding the use of cross-border industrial data. While seemingly focused on data governance, it represents a crucial step for BMW in securing its electrification supply chain.

In the battery sector, CATL commands over 35% of the global market share and leads in core technologies such as solid-state batteries. BMW's Shenyang Power Battery Center and battery supply for its next-generation models heavily depend on CATL.

This consensus not only addresses BMW's core pain points in localizing operations but also underscores China's regulatory influence in data governance, elevating Sino-German cooperation from simple "product supply" to in-depth "rule co-creation."

Mercedes-Benz, on the other hand, signed an upgraded strategic cooperation memorandum with Momenta. Merz personally visited the Beijing Mercedes-Benz plant and test-drove the new-generation Mercedes-Benz S-Class, experiencing China's intelligent driving technologies and capabilities firsthand. This marks a practical advancement in technological cooperation between China and Germany.

At the Sino-German Economic Advisory Committee symposium on the 25th, over 60 Chinese and German entrepreneurs engaged in in-depth discussions on electrification, green manufacturing, localized supply chains, and R&D cooperation. Chinese automakers such as Geely, Xiaomi, and NIO directly engaged with German giants, with relevant consensus ultimately incorporated into a comprehensive cooperation document following the Sino-German Prime Ministerial Talks, elevating Sino-German automotive cooperation from the corporate level to the national strategic level.

The delegation's visit to Hangzhou, where they not only toured the highly sought-after Unitree Technology but also engaged with Hangzhou entrepreneurs from Geely and Leapmotor, can be seen as Germany's recognition and acknowledgment of the strength of China's domestic new energy vehicle (NEV) companies, highlighting the hard power of China's NEV industry.

Behind these series of actions lies a fundamental shift in the underlying logic of Sino-German automotive cooperation. In the past, German automakers entered China with core technologies, exchanging technology for market access and dominating the industry. Today, China has developed an unshakable structural advantage in electrification, intelligence, and batteries. German automakers not only require Chinese technology and complete supply chains to reduce transition costs but also need China, the world's largest automotive market, to sustain their profits and development foundations.

Admittedly, Sino-German automotive cooperation is bidirectional, as China also seeks to further penetrate the European market through cooperation with Germany, achieving global output of technology and brands. However, this need fundamentally differs from Germany's deep reliance on China.

When Merz called for "establishing a balanced partnership" before his visit to China and the German government attempted to project a tough stance of "not relying on China," the actual actions of German companies and cold economic data have already punctured this illusion of "balance." Germany's unilateral dependence on China is deeply ingrained in its industrial and economic fabric.

From trade data alone, China has long become Germany's irreplaceable largest trading partner. In 2025, Sino-German trade volume reached €251.8 billion, with China once again surpassing the United States to top the list. Germany's imports from China amounted to €170.6 billion, while its exports to China were only €81.8 billion, resulting in imports more than double exports and a trade deficit with China nearing €90 billion. This indicates that the German market's demand for Chinese goods far exceeds China's demand for German goods.

In the automotive sector, which accounts for 13% of German industrial employment and 17% of export volume and is known as the "lifeblood of German industry," this deficit is even more pronounced. Chinese electric vehicles, batteries, and intelligent components continue to flood the German market, while sales of German automakers in China decline and exports to China stagnate. The tilting trade landscape has predetermined Germany's passive position in Sino-German economic and trade relations.

Objective data further intuitively corroborate this reversal in industrial landscape. From 2022 to 2025, German automakers' market share in China declined by an average of 33%, with BMW dropping by 42% and Mercedes-Benz by 35%. The traditional advantages of German brands in China continue to erode.

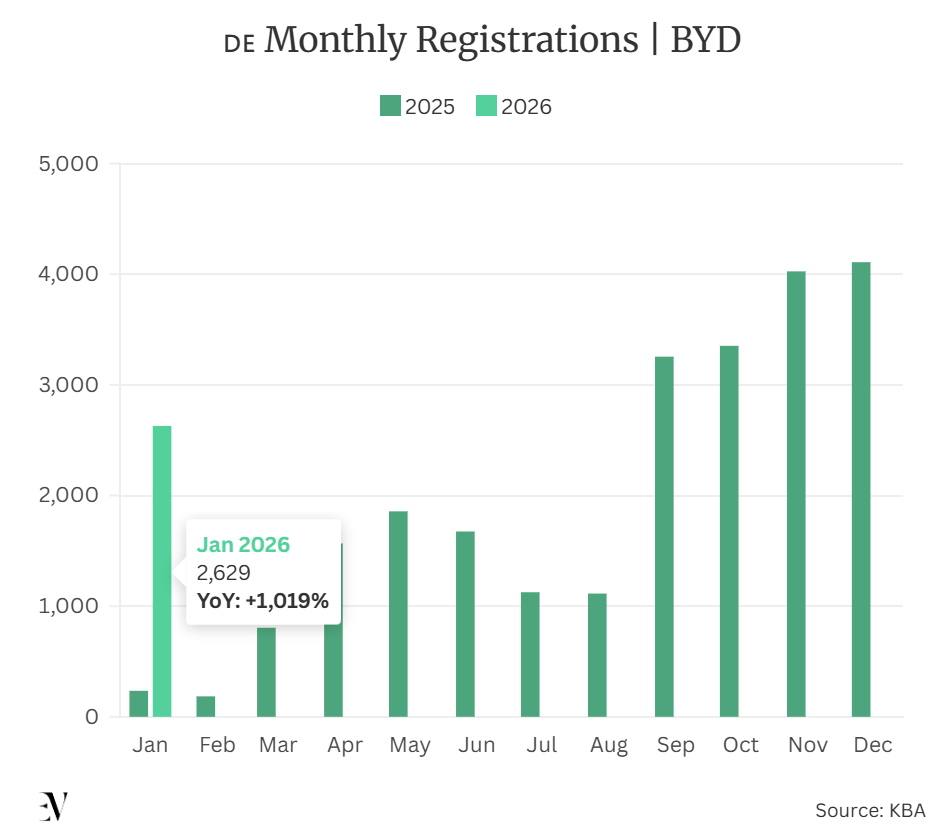

In contrast, Chinese brands not only squeeze German cars in the Chinese market but also make significant strides in the German domestic market. BYD delivered 23,306 electric vehicles in Germany in 2025, a year-on-year increase of 706.2%. In January 2026, sales surged by over 1000%, with plans to deploy over 350 dealers in Germany by the end of the year, aiming for annual sales of 50,000 units. The contrast between the decline of German brands and the rise of Chinese brands clearly illustrates the competitive landscape of the Sino-German automotive industry.

The global layout choices of German automakers further confirm their deep reliance on the Chinese market. While closing factories and reducing production capacity in Germany, they are investing heavily in localizing operations in China.

Volkswagen has invested over €20 billion in its Hefei base and acquired a stake in XPeng. BMW has invested over €10 billion in Shenyang to build a power battery center. Mercedes-Benz continues to ramp up its localized electrification R&D in China. The actions of the three German automotive giants are highly consistent, as they understand that "success in China is prerequisite for success in other markets." As BMW Chairman Oliver Zipse stated, ignoring the Chinese market means missing out on significant opportunities for global growth and economic success.

Undoubtedly, corporate choices are always more genuine than government statements. Although the German government seeks to maintain a certain "political dignity," direct investment from Germany to China increased by €7.5 billion in 2025, a 70% year-on-year expansion and a five-year high. German companies are voting with their wallets, demonstrating their unwavering confidence in the Chinese market.

This disconnect—where "the government wants to be tough, but companies dare not"—is the Merz government's greatest vulnerability. It also confirms a fact: Germany's China strategy ultimately cannot defy market choices or the deep reliance of German companies on China's market and technology.

Now, let's examine China's needs from Germany, which can be seen as "leveraging" rather than "dependence," and certainly not passive reliance for industrial development. Ongoing tensions in Sino-U.S. relations have made Europe a crucial blue ocean for China's automotive exports. Germany, as Europe's largest economy, serves as a "bridgehead" for Chinese brands to enter the European high-end market. In 2023, China surpassed Japan to become the world's largest automotive exporter. By 2025, monthly sales of Chinese electric vehicles in Europe exceeded 100,000 units, capturing a 9.5% market share with a year-on-year growth rate of 127%. Europe has become a core market for China's automotive globalization.

Clearly, cooperation between China and Germany can clear many obstacles for Chinese brands entering Europe. For example, the advancement of Sino-German automotive standards recognition enables brands like BYD, Geely, and NIO to better comply with European technical and environmental regulations. Germany's strengths in green manufacturing, carbon footprint management, and automotive-grade chips can also address some of China's automotive industry shortcomings, achieving mutual complementarity.

Meanwhile, intense competition in China's domestic NEV market compels Chinese brands to seek growth overseas. Europe, as a global high-end automotive market, not only drives sales growth but also enhances the international premium and influence of Chinese brands. However, all of this is based on China's structural advantages in the automotive industry, seeking global advancement.

Merz's visit to China, as seen through major official media outlets, has essentially set the tone for "bidirectional co-creation and deep integration" in Sino-German automotive industry cooperation, pushing bilateral collaboration to a deeper level. In the future, German automakers will accelerate their localization in China. In 2026, nine new Mercedes-Benz models will feature Chinese intelligent driving technology, and BMW's next-generation models will debut in China. The electrification transformation of German automakers will increasingly rely on China's technology and market. Meanwhile, Chinese brands will leverage Sino-German cooperation to further penetrate the European market and accelerate their globalization pace.

However, it cannot be denied that behind this cooperation, the dominance in the Sino-German automotive industry has quietly shifted toward China. China's structural advantages in electrification, intelligence, and batteries, along with its complete supply chain, scale effects, and technological barriers, compel German automakers to proactively align. China's vast market size serves as the core foundation for German automakers' electrification transformation. In contrast, Germany can offer China more access to the European market, some high-end manufacturing experience, and automotive-grade chips and other components. The balance of cooperation has already tilted toward China.

Germany's automotive industry and even its economy's deep reliance on China's market and technology is not accidental but an inevitable result of the electrification wave, global industrial restructuring, and the best proof of China's automotive industry rise. China's equal voice, and even dominance, in Sino-German cooperation stems from its tangible industrial strength.

Perhaps, as stated in the title of a German media article, "Bundeskanzler Merz darf in China alles machen, nur keinen Kotau" ("Chancellor Merz can do anything in China, but he must not kowtow"), the implication being: "Prime Minister, you can do whatever you want in China, but we must not bow." However, when it comes to German automobiles, they have already bowed their heads.

Editor-in-Chief: Shi Jie Editor: He Zengrong

THE END

-

![]()

Can the Brand-New Hongqi H7 Forge Its Own Identity in the Hybrid Vehicle Market?

-

![]()

Challenges in Redeeming Certificates for New Cars: Mercedes-Benz Dealership Group Grapples with Operational Hurdles Once Again

-

![]()

Porsche Returns to Volkswagen, Ending the 'Electric Ferrari' Story

-

![]()

"Chinese Version of Mythos": Can It Rise to the Challenge and Keep Pace?

-

![]()

Equity Changes Hands Three Times in Seven Years: JMCG Leans on Contract Manufacturing for Survival Amid Brand Deficits

-

![]()

Automotive Market News: Nine Departments Jointly Roll Out Aftermarket Consumption Initiatives

-

How Electronic Fabric Became the Critical Chokepoint for AI’s Trillion-Dollar Computing Infrastructure

-

![]()

Depreciation Rate on Par with Mobile Phones: Just 40% Value Retention After Three Years—Why Do Battery Electric Vehicles Lose Their Worth?