Linghui: Not Expansion, But Strategic Liberation—The Pivotal First Move in BYD's Premium Brand Offensive

04/20 2026

04/20 2026

529

529

In June 2025, Wang Chuanfu declared at BYD's shareholder meeting: "Premiumization represents our next decisive battle, with the coming three years as the focal period."

Eight months later, Linghui Automobile made its formal debut. Nine months onward, the Linghui e7 entered the market with a starting price of 95,800 RMB.

This article offers a tripartite industry analysis of BYD's Linghui brand launch:

- What is the true strategic intent behind Linghui?

- How does it differentiate from other BYD sub-brands?

- Behind the synchronized rollout of flash charging technology across all brands lies a grander strategic vision.

By the conclusion, readers will acquire an analytical framework to assess multi-brand strategies among Chinese automakers.

I. Clarifying What Linghui Is Not

Three prevalent misconceptions about Linghui have led to flawed strategic assessments.

Misconception 1: "BYD is launching another new brand—a sign of overexpansion."

Reality: The Linghui trademark was registered in 2010. This is a 16-year-old strategic seed, not a hasty decision. BYD deliberately waited until 2026 to unveil it, timing the market entry with precision.

Misconception 2: "Linghui is BYD's new weapon for the cost-effective market."

Reality: The Wangchao Network's Qin PLUS starts at 79,800 RMB, while the Ocean Network's Dolphin starts at 88,800 RMB. BYD's main brand already dominates as the world's most formidable "cost-effectiveness machine." The Linghui e7, priced at 95,800 RMB, does not undercut the main brand. If price competitiveness were the sole objective, BYD would not require a new brand.

Misconception 3: "Linghui is exclusively designed for ride-hailing drivers."

On the surface, this appears plausible—all four initial models are rebadged versions of platforms from the Wangchao/Ocean networks, with configurations optimized for operational use. However, this describes Linghui's "product form," not its "strategic intent."

The core issue it addresses is branding, not product development.

II. The Current Challenge: BYD's 'Ride-Hailing King' Label Becomes a Liability

To comprehend why Linghui is essential now, consider three often-overlooked data points.

Data Set 1: Sales Growth Has Plateaued.

In 2025, BYD sold 4.6024 million vehicles, with year-on-year growth slowing to 7.73% from previous years' 40%+. In January 2026, monthly sales dropped 30.11% YoY, with pure EV sales falling 33.6%.

Data Set 2: Domestic Premiumization Efforts Have Stalled.

The Wangchao and Ocean networks contributed 88.5% of sales, while high-end brands (Tengshi, Fangchengbao, Yangwang) accounted for just 8.7%. In January 2026: Tengshi sold 6,002 units, Fangchengbao 21,581, and Yangwang 413.

Data Set 3: The Ride-Hailing Stigma Drags Down the Brand.

The Qin PLUS is humorously dubbed "a car that comes with a job"—new owners are immediately added to Didi driver groups. Industry data reveals 191,000 BYD ride-hailing vehicles sold in 2023 (second only to Aion's 219,000). Sales feedback indicates personal buyers often leave showrooms after learning "this car is popular with ride-hailing drivers."

This creates a vicious cycle: The main brand loses C-end pricing power due to its ride-hailing image → struggles to move upmarket → Tengshi/Fangchengbao/Yangwang are perceived as "fancy BYDs" → high-end brands also stagnate.

Aion serves as a cautionary tale. In 2023, 45.4% of its sales were ride-hailing vehicles, cementing its "Ride-Hailing King" label. Its high-end sub-brand Hyper launched in 2022 but has barely made waves. Wang Yunlong admitted in August 2024: "We separated B-end operations in early 2024." But it was too late—the label had stuck. BYD aims to avoid this path.

III. Surprise: Linghui's True Customers Aren't Ride-Hailing Drivers—They're Potential Main Brand Buyers

This is the article's most counterintuitive claim. Pause for 30 seconds to absorb it:

Linghui represents BYD's "brand subtraction surgery" to enable premiumization.

It appears downward but actually aims upward.

Here's how it works:

Step 1: Strip 'ride-hailing' from the main brand. Linghui integrates BYD's original corporate e-series resources, with independent branding, channels, and sales systems. From 2026 onward, new BYD vehicles added to Didi, Gaode, and T3 fleets will primarily be Linghui e5/e7/e9 models, not Qin PLUS EVs or Dolphins. The main brand will no longer be tied to "ride-hailing."

Step 2: Let Wangchao/Ocean ascend unburdened. Freed from the ride-hailing stigma, these networks can confidently target the 150,000–250,000 RMB mainstream family market—the stronghold of joint-venture brands (Volkswagen, Toyota, Nissan) and the most critical price band for Chinese brands to move upmarket.

Step 3: Create space for Tengshi/Fangchengbao/Yangwang. Only when the main brand pushes upward can high-end brands break through. Tengshi Z9 GT (269,800–369,800 RMB), Fangchengbao Titan 7 EV (179,800–219,800 RMB), and Yangwang U8 (million-RMB class) need the main brand's 200,000 RMB base to stabilize.

Step 4: Seize the Robotaxi opportunity. L3 autonomous driving is landing in China, and Robotaxi commercialization is imminent. Isolating B-end operations enables direct collaboration with Didi and T3 while laying groundwork for future self-operated Robotaxi services—a dual win.

Key Takeaway: To assess Linghui's success, don't measure Linghui's sales—track whether Wangchao and Ocean's average selling prices rise.

IV. The Truth About Technical Differences: Shared Foundations, Reconfigured Setup

This is the second critical insight. Many peers ask, "Is Linghui using BYD's old technology?"—a misleading question.

The reality: Core "three electric" technologies (battery, motor, electronics) are fully shared, but configurations are highly scenario-specific.

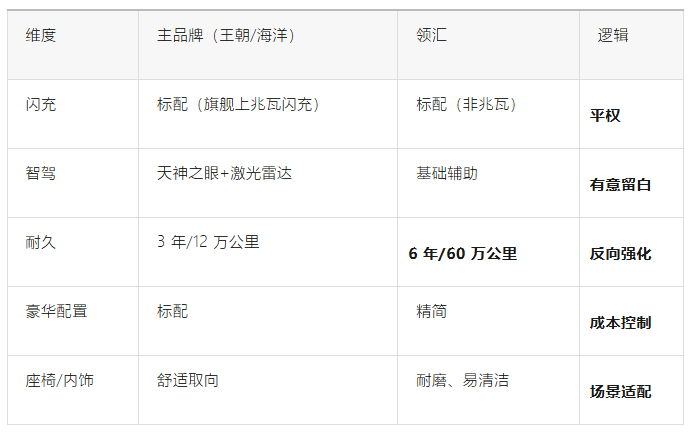

4.1 Flash Charging: Full Brand Synchronization—Linghui Isn't Second-Class

On March 5, 2026, BYD announced its second-generation Blade Battery and flash charging technology, stating: "All models under Wangchao, Ocean, Fangchengbao, Tengshi, and Yangwang will adopt it." On April 15, the Linghui e7 launched with flash charging: 5 minutes to 70%, 9 minutes to 97%, and just 3 extra minutes at -30°C—matching the Seal 07 EV's specs and representing standard second-gen Blade flash charging (not megawatt-class).

A notable detail: Megawatt flash charging (1,500kW peak) was reserved for flagships like the Han L and Tang L, not Linghui. This isn't "inferior technology" but reflects battery pack capacity and vehicle voltage architecture differences—megawatt charging requires a 1,000V platform, which is costly and demands larger battery packs. The e7's 400V + standard flash charging combo is optimal for operational scenarios.

4.2 Intelligent Driving: Deliberate 'Technical Blank Space'

The main brand's 2026 models fully adopt the "Divine Eye" ADAS system, with the Seal 07 EV and Song Ultra EV featuring standard LiDAR + urban NOA. The Linghui e7 skips LiDAR, offering only ACC, LKA, and HNOA.

This isn't a technical limitation but a strategic choice—operational drivers have minimal willingness to pay for ADAS. LiDAR + domain controllers cost ~15,000–20,000 RMB, which would break the 100,000 RMB price point. Maintaining this "ADAS gap" reinforces differentiation between the main brand and Linghui—a sophisticated "technology shelf reuse" strategy: not a lack of technology, but a commercial blank space.

4.3 Durability Standards: Linghui-Exclusive, Reverse Differentiation

The Linghui e7 introduces a standard absent in main brand family cars: 6-year/600,000 km operational durability, 9,600 cycles of enhanced rough-road testing (double that of family cars), and a 6-year/150,000 km vehicle warranty. This reflects targeted engineering for high-frequency use—not "repurposing family cars for operations" but enhancing them for operational demands.

4.4 The Logic Behind Configuration Differences

Combined, these points reveal Linghui's clear value realignment:

In summary: Linghui isn't a "downsized BYD" but a "scenario-based configuration reorganize"—cutting ADAS and luxury, adding durability and operational convenience, while retaining flash charging as the core weapon.

V. Analytical Frameworks for Three Reader Groups

For Decision-Makers: Evaluate Linghui's Success Beyond Linghui

If you're in corporate strategy at an OEM or cover automotive at an investment firm, Linghui's real lesson is this: To assess an operational sub-brand's success, don't focus on its sales—track changes in the parent brand's average selling price and C-end share.

Three Trackable Metrics:

- Whether Wangchao + Ocean's average selling price rises after Q3 2026

- Whether personal users account for over 70% of Tengshi N-series and Fangchengbao Titan 7 sales

- BYD main brand 4S store average transaction price and test-drive conversion rates—the most sensitive indicators of "ride-hailing stigma" erosion

Beware: Linghui isn't a panacea. In 2026, new energy subsidies will phase out, and trade-in incentives will shrink, while ride-hailing companies are extending vehicle lifecycles. Linghui's B-end order volume hinges on taxi electrification policies and Robotaxi pilot expansion—not just product quality.

For Practitioners: Four Pillars of Operational Market Configuration

If you're in product planning or channel management, Linghui offers a replicable scenario-based methodology:

- Cut ADAS: Operational drivers don't need L2+—save 15,000–20,000 RMB. (Future Robotaxi compatibility may require L4, though.)

- Boost Durability: 6-year/600,000 km warranty—B-end users will pay 20,000–30,000 RMB more for this.

- Preserve Flash Charging: This is the core time-value driver for operations—two extra trips daily yield 30,000 RMB in annual revenue.

- Control Costs: Reuse existing platforms and molds to lock in margins from the first vehicle.

This playbook's essence: B-end users have a different payment curve than C-end users—they don't pay for luxury or ADAS but for "earning efficiency." Whoever redefines configurations around "cost per kilometer" can replicate Linghui's path.

For Researchers: Three Structural Shifts to Track

- The new equilibrium between "technological equity" and "brand tiering": Linghui shares second-gen Blade Batteries and flash charging with the main brand but differentiates via configuration. This challenges the industry intuition that "premium brands = better technology"—worth tracking for 3+ years.

- The diminishing returns of multi-brand matrices: BYD now has six brands (BYD, Tengshi, Fangchengbao, Yangwang, Linghui, and a rumored ultra-premium sub-brand). Each new brand increases group management costs and fragments channel resources. When will marginal benefits turn negative?

- The survival space for joint-venture fuel-powered operational vehicles: Linghui's true competitors aren't Aion Hyptec (Guangzhou's similar plan) but Corolla and Lavida joint-venture fuel-powered operational models. If Linghui breaks through on TCO (total cost of ownership), the last bastion of joint ventures in the operational market will collapse.

Final Question: What Are the Risks in Linghui's Move?

Three concerning variables:

- The true investment in channel and brand-building. Linghui integrates resources from the original corporate e-series but must build independent 4S + urban showroom networks and brand recognition from scratch—estimated annual investment: 2–3 billion RMB. If B-end orders fall short, it could drag down overall scale effects.

- The main brand's 'de-ride-hailing' time window. Consumer perception shifts take 3–5 years, while competitors (especially HiPhi, XPeng, Xiaomi) are rapidly capturing the 150,000–250,000 RMB price band. BYD must raise the main brand's average price within this window, or the liberation's value will dilute.

- Robotaxi commercialization pace. If L3 deployment lags, Linghui's second growth curve will delay, forcing reliance on traditional ride-hailing orders—weakening its brand narrative.

Regardless, Linghui had to act. Once a brand's label hardens (as with Aion), it's impossible to shed.

BYD's 16-year-old seed wasn't planted to sell more ride-hailing vehicles—it was to remove "ride-hailing" from BYD's identity.

This is the first layer. In the next Vehicle article, we'll discuss the deeper implications

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’