No New Stories Left in the Auto Circle After Exhausting All Tricks

04/21 2026

04/21 2026

543

543

Introduction

Introduction

Quality is sacrificed for quantity.

What is the auto circle competing over this year? The answer is blunt: quantity. In 2026, the Chinese auto market is suffocating from an overwhelming number of new car launches. A leading automotive media company reports that its team of over 100 people has been fully dispatched to attend these events.

According to incomplete statistics, nearly 80 new car-related events were held domestically in March alone, surpassing a daily update pace. On many days, four automakers squeezed their launch events into the same day. As April approaches, this launch frenzy not only fails to cool down but intensifies with the Beijing Auto Show on April 24th, making three to four daily launches the norm.

According to incomplete statistics, at least 40 new car models were launched, pre-sold, or unveiled in the domestic auto market in April. Automakers are rushing to release new models before the auto show to avoid the information deluge during the event and secure media attention in advance. April 22nd is even more remarkable, with over 10 new car launches or releases initially counted for that day alone.

Notably, these new cars are highly similar in positioning and pricing. Take April 16th as an example: Xpeng GX and Volvo XC70 were launched earlier, while on the same day, the ZhiJi LS8, Leapmotor D19, and Volkswagen ID.08 were pre-sold or launched. Later, the Zeekr 8X and WEY V9X were launched and pre-sold. All these models are large SUVs, with prices densely clustered in the RMB 200,000 to 400,000 range, indicating severe product homogenization.

Even more alarming is the number of launch events for a single new car model, from technical teasers to final delivery, often involving five to six or even more events. These include technology brand days, product debuts, static photo shoots, dynamic test drives, pre-sales, official launches, vehicle teardowns, or long-term test live streams, layer upon layer of additional requirements (adding layer upon layer, like a drama series).

In the era of traditional fuel vehicles, a new car model typically required only two to three launch events. Nowadays, it often starts with five or six. Automakers are almost monthly creating new topic nodes. Some brands can shorten the period from pre-sale to delivery to just one month, while others begin preheat (teasing) a year in advance.

In the past, people advised against intense competition, but now it has escalated to a more absurd direction. It is labor-intensive, time-consuming, and results in information overload, much like scrolling through short videos, with only a few truly remembered by consumers. The craziness during the Beijing Auto Show week barely describes the surge in the Chinese auto industry. There are more and more cars, but they all seem to taste the same.

01 What Has Been the Focus of Competition All These Years?

In the current Chinese auto market, automakers may verbally deny intense competition, but their actions say otherwise—it's inevitable.

The starting point of intense competition is chip computing power, or more precisely, intelligent cockpit chips. With the rapid penetration of automotive intelligence, whether a new energy vehicle's cockpit is smarter, qualified, or high-end is judged by whether it is equipped with chips like Qualcomm 8155, 8295, or 6nm/4nm processes.

Meanwhile, in the field of intelligent driving, competition has shifted to computing power, followed by the number of LiDAR sensors and their line counts. Initially, NVIDIA's Orin-X chip dominated the industry, becoming almost synonymous with automakers' pursuit of high-level intelligent driving. Later, Chinese automakers began developing their own chips, with NIO, Xpeng, and Li Auto giving it a try. Then came Huawei's significant lead and Horizon Robotics' rapid rise.

When the computing power race hit a bottleneck, the focus of intense competition shifted to another dimension: refrigerators, TVs, and large sofas. Li Auto stood out with this product definition, but its once-winning selling point quickly became an industry standard. Nowadays, even RMB 100,000-class family cars can be equipped with car refrigerator (vehicle-mounted refrigerators), RMB 150,000 SUVs with massage seats are basic, and cars priced at RMB 200,000 without three large screens would be embarrassed to hold a launch event.

These selling points have become standard, trapping innovation in homogenization. Automakers can only Crazy addition (go all out in adding features) in this track (track). For example, Ford created a "1-bedroom, 1-living room, 1-kitchen" concept, ZhiJi added a tailgate shower system to its flagship model, and Leapmotor D19 even introduced a vehicle-mounted oxygen generation system, creating a forest wilderness oxygen cabin.

What if consumers are indifferent to these configurations? Then the competition shifts to promotions. Direct price cuts risk damaging brand image and upsetting existing owners, so automakers repackage price wars into low-interest financial battles. In early 2026, Tesla took the lead by offering seven-year ultra-low-interest financing with monthly payments of just over RMB 1,000.

Subsequently, over 20 automakers, including BYD, Xiaomi, Li Auto, and Xpeng, followed suit, with Dongfeng Nissan extending the period to eight years. ZhiJi Automobile launched a combo of seven-year zero-down payment plus a RMB 23,000 cash Red envelope (red packet). This is less about financial service innovation and more a price war in financial disguise.

Here, we need to mention a new track—not intense competition but industry-driving: the installation volume of intelligent driving assistance solutions. For example, Huawei ADS, Momenta, AutoX, Horizon Robotics, and ZhiYu Technology now constitute the first tier of Chinese intelligent driving suppliers.

What if these also fail? The fire of intense competition spreads to the supply chain. Automakers began competing to showcase lists of big-name suppliers to prove their superiority. On March 26th, Yijing held a supplier ecosystem cooperation conference, gathering 75 global key industrial chain (supply chain) suppliers, including Shenzhen Yinwang and CATL, covering core vehicle sectors such as chassis, intelligent driving, cockpits, braking, and body lighting—a top-tier matrix in the core areas of the entire vehicle manufacturing link.

The Leapmotor D19, launched on April 16th, adopted a similar strategy, releasing a series of big-name supplier posters during the preheat (teasing) phase, focusing on stacking materials. At the launch event, it showcased a string of top suppliers at once, including Konghui air suspension, Michelin low-noise tires, Fuyao double-layer soundproof glass, semi-aniline leather interiors, and 9,200-ton integrated aluminum die-cast floors.

In fact, if you recall, last year's Shanghai Auto Show saw the quietly rise (quiet rise) of supplier booth scales. The number of supply chain exhibition spaces at the 2025 Shanghai Auto Show jumped to 23 from 12 in 2023, with exhibition areas surging from 30,000 square meters to 100,000 square meters. This illustrates the importance of suppliers in the new energy era.

Now, as everyone can see, intense competition has entered its most blunt phase: competing over the number of launch events. Information shows that 193 press conferences were held over the two media days of last year's Shanghai Auto Show, a record high. What about this year's upcoming Beijing Auto Show, held at a new venue for the first time? Will the number of launch events surpass that of the 2025 Shanghai Auto Show?

02 What Are the Costs of Intense Competition?

When intense competition is unavoidable, another unavoidable question arises: who is footing the bill for this frenzy?

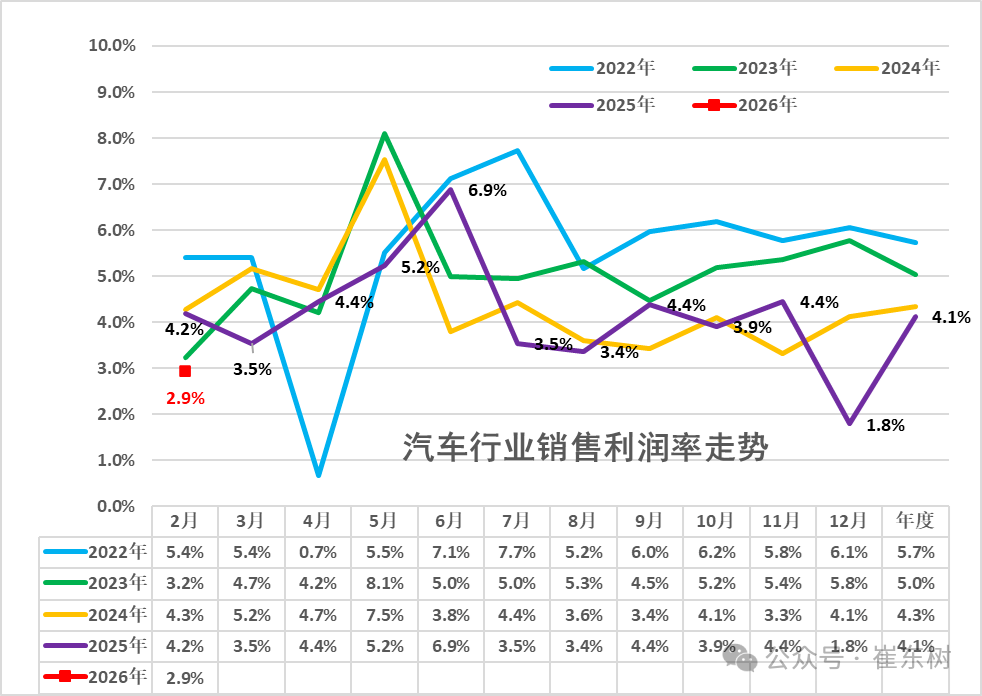

The most direct cost is the continuous collapse of industry profit margins. National Bureau of Statistics data shows that in 2025, the profit margin of China's auto industry was 4.1%, down 0.2 percentage points year-on-year, hitting a record low. In December 2025 alone, the profit margin was just 1.8%, down 2.3 percentage points year-on-year.

In 2026, the situation did not improve, with the industry profit margin further declining to 2.9% from January to February, far below the national average of 4.92% for industrial enterprises above a certain scale. During the same period, the total profit of the auto industry was just RMB 43.5 billion, down 30% year-on-year.

Financial reports from some mainstream automakers also look grim. In 2025, Li Auto reported revenue of RMB 112.313 billion, down 22.25% year-on-year; net profit attributable to the parent company was RMB 1.124 billion, down 86%. Xpeng Motors reported a full-year net loss attributable to the parent company of RMB 1.139 billion, despite achieving its first quarterly profit in Q4, still ending the year in the red. NIO reported a full-year net loss attributable to the parent company of RMB 15.571 billion, though narrower than the previous year.

NIO founder William Li once calculated: "It's common for a model to waste several hundred million yuan, with no one—the manufacturer, the supply chain, or the user—benefiting. Several hundred million yuan just goes to waste." He estimated that standardizing battery cells and unifying chips alone could reduce industry waste and release over RMB 100 billion in potential annual benefits for the entire industry.

The vast majority of auto dealers are the invisible victims dragged into the abyss by intense competition. According to estimates by Cui Dongshu, Secretary-General of the China Passenger Car Association, from January to September 2025, the gross profit per vehicle for automakers was only about RMB 14,000, compared to RMB 23,000 in 2017—a nearly 40% decline in per-vehicle profitability over eight years.

In 2024, the average gross profit margin of auto dealers nationwide was less than 3%, with over 4,400 4S stores closing down. In the first half of 2025, over 52.6% of dealers incurred losses, and 74.4% experienced price inversions, with some slow-selling models incurring losses exceeding RMB 10,000 per unit. A dealer for a joint-venture brand lamented, "Selling one car means losing several thousand yuan, relying entirely on after-sales and manufacturer rebates to fill the gap."

The biggest victims of intense competition are perhaps consumers. In the past, car facelifts typically occurred every three years, with full model changes every five years. Now, the iteration cycle for new cars has been compressed to just a few months or even shorter, frequently leaving existing owners feeling betrayed. Some owners who just bought a car in March found it officially discounted by RMB 30,000-50,000 just half a year later—a depreciation speed that makes many consumers feel like they're stock trading when buying a car.

The decline in new car prices most easily leads to a collapse in residual value. The 2025 China Automotive Residual Value Report shows that the three-year residual value for plug-in hybrid models is just 43.7%, and for pure electric models, it has slipped to 42.0%. In contrast, traditional fuel vehicles generally have three-year residual values above 50%, with Japanese joint-venture brands stable above 54% and luxury brand Porsche's three-year residual value as high as 66.2%.

Consumer complaints have also surged. At a local "3·15 Problem Car Expo" this year, complaints about new energy vehicles accounted for over 40% for the first time, becoming the primary source of complaints. According to the National 12315 Platform, there were 32,000 automotive consumer complaints in Q1 2026, up 18.6% year-on-year. Key pain points include exaggerated range claims, overhyped intelligent driving features, and three-electric system failures.

From declining automaker profits to dealer crises and compromised consumer interests, intense competition is a game with no winners. Especially when consumers lose their judgment and interest in understanding new cars amidst overwhelming marketing information, truly consumer-adapted vehicles are overshadowed.

Editor-in-Chief: Yang Jing Editor: He Zengrong

THE END

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’