Hormuz: A Passive 'Catalyst' for the Global Automotive Industry's Transition

04/23 2026

04/23 2026

483

483

From the 'Black April' to negotiation windows, the aftershocks of the Hormuz crisis linger. When the control over a critical energy chokepoint shifts away from market forces, the ripple effects on costs, supply chain restructuring, electrification transitions, and consumer expectations are being profoundly rewritten. Who will seize this moment to accelerate? Who will be forced to reshape?

On April 22, the second round of U.S.-Iran talks mediated by Pakistan reached an impasse, with the prospects for an agreement remaining uncertain. Although a temporary ceasefire has been extended, the inherent high risks in the Strait of Hormuz have not been eliminated. Global market pessimism toward a 'Black April' has only seen a tentative, cautious easing.

For the global automotive industry, this presents a crucial 'observation window.' Short-term logistical disruptions and order reductions are now inevitable, with impacts gradually surfacing in production schedules across major automakers. However, deeper, lagging effects are only beginning to propagate: a cost storm in energy and industrial raw materials (primarily aluminum) is solidifying from futures markets onto factory floors, while sustained high oil and gas prices are reshaping end-consumer behavior—particularly accelerating electrification transitions—first breaking through in the used-car market.

March data from the German Automobile Industry Association (VDA) shows that the U.S.-Israel-Iran conflict has yet to have a measurable immediate impact on new electric vehicle registrations in Europe, primarily due to the typical several-month delay between ordering and registration. But beneath the surface, currents are shifting: inquiries for electric vehicles on major European automotive trading platforms have surged, while used electric vehicle sales in the U.S. rose 12% year-on-year and 17% quarter-on-quarter in the first quarter (Cox Automotive data). These signals indicate that the temporary lull in conflict is far from the end of the crisis but rather a pivotal turning point where the global automotive industry shifts from passively enduring a 'cost storm' to actively embracing supply chain restructuring and energy transitions.

How an Energy Chokepoint Reshapes Manufacturing Costs

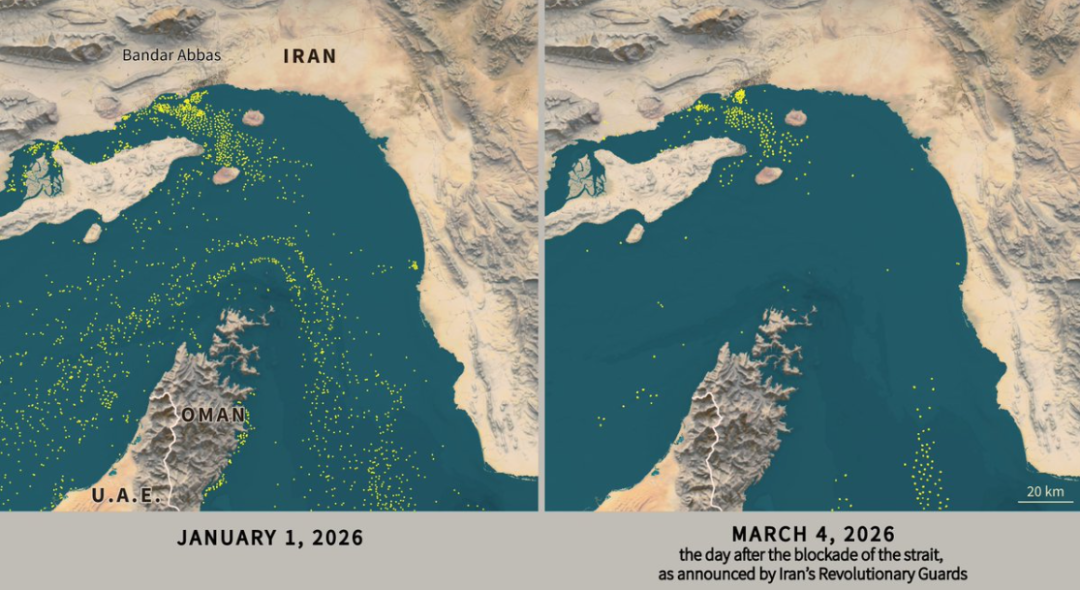

The Strait of Hormuz, responsible for transporting approximately 20% of global oil and liquefied natural gas, has effectively been blocked since the February 28 military conflict. This sudden disruption has severed the logistical and energy chains vital to the global industrial system. While cargo ships in March could still rely on pre-conflict inventory stocks, by April, the dilemma of 'no new cargo to load' has become unavoidable.

Fatih Birol, Executive Director of the International Energy Agency (IEA), issued a stark warning on April 7: 'The shortage of crude oil and refined products in April will be double that of March.' He characterized the current energy crisis as 'more severe than the combined totals of 1973, 1979, and 2022,' predicting a true 'Black April' for the globe. This macro assessment is reflected in micro-level prices: Brent crude futures surged above $126 per barrel, a 57% increase from pre-conflict levels, while European natural gas benchmark prices nearly doubled. The chain reactions followed swiftly: the European Central Bank was forced to delay planned interest rate cuts and significantly raised inflation forecasts, casting a shadow over economic recovery prospects.

The industrial fallout has been nearly simultaneous and far more concrete. The aluminum supply chain, critical to automotive manufacturing, fractured first: Bahrain Aluminum declared force majeure on March 15, shutting down 19% of its capacity (approximately 300,000 tons per year); Qatar Aluminum halted production due to upstream natural gas shortages; and Al Taweelah, owned by Emirates Global Aluminum, suffered severe damage in an attack, halting operations. These three Gulf aluminum giants, with a combined annual capacity exceeding 570,000 tons, account for roughly 9-10% of global automotive-grade aluminum supply.

From a materials economics perspective, aluminum acts as an amplifier in this crisis due to its energy-intensive production. Refining one ton of primary aluminum requires an average of 14-15 megawatt-hours of electricity, and Gulf aluminum plants rely heavily on cheap, abundant natural gas for power. Once gas supplies are cut off, smelting costs skyrocket non-linearly. This 'energy-aluminum-automotive' transmission chain, masked by low energy prices in normal times, exposes its inherent fragility with alarming speed during crises.

Meanwhile, the global automotive industry's reliance on aluminum has deepened continuously over the past two decades. Driven by demands for lightweighting and extended range, mainstream electric vehicles now use 200-300 kilograms of aluminum per vehicle, with some luxury electric models exceeding 340 kilograms. This means that any sharp rise in aluminum prices will hit electric vehicle manufacturers far harder than traditional internal combustion engine vehicle makers.

Aluminum prices have soared under the dual pressures of supply collapse and surging energy costs (European factory electricity prices have doubled). LME three-month aluminum futures surpassed $3,400 per ton by late March, up over 38% since the start of the year. Analysts at S&P Global Mobility express deep concern: 'If the conflict persists, inflationary pressures on production costs will become entrenched.' Once entrenched, these costs will not dissipate immediately with a ceasefire agreement, as restarting aluminum smelters involves time-consuming processes like preheating electrolytic cells and restoring process parameters. From shutdown to full capacity typically takes three to six months, meaning cost stickiness will persist deep into the second half of 2026, continuously testing the profit resilience of global automakers.

Facing this cost storm, major multinational automakers have adopted a blunt and ruthless strategy: prioritizing production of high-margin SUVs and pickup trucks while strategically compressing or canceling entry-level, low-margin product plans. This logic is not difficult to understand. Under acute cost inflation, thin-margin products hit break-even thresholds first.

However, this 'scalpel' cuts away not just short-term losses but potentially severs connections between automakers and young consumers or price-sensitive emerging market users. Once the crisis eases, whether disrupted entry-level product lines can restart quickly and whether consumer attention has shifted to competitors (particularly Chinese brands) will become strategic imperatives for traditional automakers in the post-crisis era.

Japanese automakers have reacted most swiftly. On April 6, Mazda officially announced a suspension of production for export models to the Middle East until May, citing logistical disruptions for parts and finished vehicles due to the Hormuz blockade. Toyota and Nissan had already begun cutting Middle East production in March. Toyota Vice Chairman Koji Sato publicly acknowledged that the Hormuz blockade represents 'the core challenge for vehicle transportation.' These production cuts are essentially defensive contractions amid inventory backlogs and export blockades. Alarmingly, even if a breakthrough occurs in the second round of talks, restoring shipping order in the strait will take weeks, while aluminum plant restarts will require months, with cost stickiness persisting through year-end—continuously testing the supply chain resilience of global automakers.

Europe and Japan Under Pressure, China's New Energy Sector Shows Resilience

The crisis acts as a mirror, clearly reflecting structural differences and risk-resistance capabilities among industrial players.

Japanese and European traditional automakers are undoubtedly the hardest-hit groups on the production front in this shock.

First, the direct freeze in Middle East exports. Gulf states like Saudi Arabia, the UAE, and Qatar have long been key markets for Japanese premium models and German luxury brands. Toyota, for example, sells approximately 250,000 vehicles annually in the Middle East, accounting for nearly 4% of its global sales, with SUVs and pickups making up over 70% of that volume—far higher in profit per unit than global averages. The sudden narrowing of export channels means high-value models are now stuck in ports.

Second, sustained energy price pressures in Europe. European automotive manufacturing is deeply integrated into European energy markets. Major vehicle and parts producers in Germany, Slovakia, and the Czech Republic face sharply rising factory operating costs amid doubled energy prices.

Third, the European Central Bank's monetary policy shift. Persistent inflationary pressures have forced the ECB to delay interest rate cuts, keeping automotive loan financing costs elevated. In a market environment with high consumer loan rates, monthly vehicle payment costs have risen significantly, creating a 'pincer attack' of supply-side cost pressures and demand-side constraints that further clouds prospects for European passenger vehicle market recovery.

Facing these pressures, response paths among European traditional automakers are diverging: luxury brands like BMW and Mercedes-Benz, with stronger brand premiums and thicker profit cushions, have greater capacity to absorb costs, and their core consumer bases are relatively less sensitive to fuel prices and financing costs. Stellantis and others face more daunting dilemmas, needing to absorb cost shocks while maintaining scale efficiencies in mass production—caught between a rock and a hard place.

In contrast, China's automotive sector has demonstrated remarkable resilience. Its core strength lies in a highly localized supply chain—the localization rates for battery systems and numerous core components have steadily increased. This shields Chinese automakers from short-term shocks caused by overseas aluminum and energy price fluctuations.

However, attributing Chinese automakers' resilience solely to 'supply chain isolation' would be an oversimplification. What truly distinguishes Chinese new energy vehicle makers in this crisis is the systemic advantage forged through a decade of strategic accumulation in electrification technologies.

First is absolute leadership in battery costs. Leading firms like CATL have driven costs for lithium iron phosphate batteries down to the $60-70 per kilowatt-hour range through mass production and vertical integration, roughly 20-30% below global averages. This cost advantage becomes even more pronounced in an era of high oil prices. As fuel costs for internal combustion vehicles surge, the lifetime cost advantages of electric vehicles become clearer, accelerating car purchase decisions (car-buying decisions) toward electrification in emerging markets.

Second is strategic depth in product portfolios. Chinese automotive groups now offer comprehensive coverage across high-, mid-, and low-end product lines, enabling them to capture multi-tier market opportunities in the electrification wave driven by high oil prices—without facing the tough trade-offs between high-margin and volume models that plague Japanese and European automakers.

More critically, soaring oil prices are accelerating shifts among consumers in emerging markets from traditional fuel vehicles to hybrid and pure electric models. Chinese brands, leveraging their first-mover advantages and cost control capabilities in new energy, are seizing this window to expand export shares in markets like Russia, alternative Middle East channels, Southeast Asia, Australia, and New Zealand. Some Chinese new energy automakers have seen inquiry volumes surge over 50% in Australia and New Zealand. In Southeast Asia, Thailand has become a key stronghold for Chinese automakers, with BYD, Changan, and SAIC either establishing or announcing localized production bases to circumvent tariff barriers and reduce logistics costs—steadily extending their strategic reach.

Meanwhile, the Middle East's intelligent driving landscape is following a script of 'short-term disruption, long-term optimism.' WeRide suspended its Robotaxi operations in Dubai in early March over safety concerns; testing by Pony.ai and affiliated firms in the UAE also halted temporarily. However, as of April 15, leading Chinese autonomous driving firms including Didi and Baidu are accelerating commercial layout (expansion plans) in the UAE. Gulf states' national strategies for smart city development remain unshaken by regional conflicts. Dubai's 2040 Urban Master Plan explicitly targets 25% of trips to be autonomous by 2030. This national strategic goal provides far more stable long-term demand support for Chinese autonomous driving firms than any single order.

The current negotiation window may instead act as an accelerator for these Chinese firms to deepen local partnerships and seize market opportunities. On one hand, regional tensions have slowed commercial footsteps of some Western competitors in the Middle East; on the other, the UAE government has maintained openness to Chinese firms during the crisis, with some regulatory approval processes even speeding up. With leading advantages in supply chain resilience and cost efficiency, Chinese intelligent driving firms are poised to swiftly fill market vacuums left by distracted Japanese and European traditional automakers once the crisis abates.

The 'Delayed Gift' of High Oil Prices

The VDA's March report explicitly states: 'The U.S.-Israel-Iran conflict has had no measurable impact on electric vehicle registration numbers.' Data shows a 66% year-on-year increase in pure electric vehicle registrations in Germany in March, reaching a 24% share—largely driven by release of pre-war backlogged orders, expanded model choices, and sustained price declines. The VDA maintains cautious optimism for the full year: 2.9 million total passenger vehicle sales (+2% YoY) and 1 million electric vehicles (+17% YoY).

However, truly forward-looking signals are already clear in consumer markets. Sustained high oil prices have directly increased total ownership costs for fuel vehicles, dramatically amplifying the relative economic advantages of electric vehicles. This effect first detonated in the more price-sensitive and decision-flexible used-car market. According to Cox Automotive, approximately 93,500 used electric vehicles were sold in the U.S. in the first quarter, achieving double-digit growth year-on-year and quarter-on-quarter. In Europe, electric vehicle search shares on Germany's largest automotive trading platform, Mobile.de, surged from 12% to 36%, with inquiry volumes up 66%; the UK, France, and Spain also saw electric vehicle inquiries generally rise 20-50%.

From the perspective of consumer behavior economics, the impact of the current high oil prices on the perception of electrification is far more profound than that of previous energy crises. This is because the current shock is compounded by multiple amplifying factors:

First, there is uncertainty regarding the duration. Unlike the market expectation of a 'short-term shock and rapid recovery' at the beginning of the Russia-Ukraine conflict in 2022, the geopolitical resolution path of the current conflict between the United States, Israel, and Iran is more complex. When formulating medium- to long-term travel budgets, consumers have to assign a higher weight to the possibility of 'oil prices remaining high for an extended period.' The anchoring of such expectations has a far more profound impact on car-buying decisions than a single peak in oil prices.

Second, the 'oil price memory effect' has been activated. Gasoline prices at gas stations in some European cities once exceeded €2.5 per liter, sparking widespread discussions and emotional resonance on social media. This 'price sensitivity' may continue to influence consumers' preference assessments of fuel vehicles even after the crisis eases.

" "

"

Third, there is the critical effect of charging infrastructure. The number of public charging piles in Europe has exceeded 600,000, marking a qualitative leap in charging experience and convenience compared to three years ago. When oil price pressures exceed psychological expectations, more consumers who previously hesitated to buy electric vehicles due to 'inconvenient charging' begin to reassess the actual severity of this obstacle and ultimately make the switch.

In multiple regional markets, used electric vehicles have become the 'entry-level choice' for consumers in the era of high oil prices due to their lower price threshold. This trend, like the 'duck knows first' of the warming spring river, indicates that the follow-up of new car sales will gradually become apparent in the second half of the year. Although analysts disagree on whether the new car market will be dragged down by factors such as tax incentive policy adjustments, there is a general consensus that hybrid (including PHEV) and entry-level pure electric models will be the first to benefit. The aforementioned IEA Executive Director Birol also stated, 'This crisis will accelerate the development of renewable energy, nuclear energy, and electric vehicles. The architecture of the global energy system is undergoing irreversible changes.'

This shift in consumer attention holds particularly profound significance for Chinese auto brands that are going global. Currently, the repurchase rates and word-of-mouth dissemination willingness of Chinese electric vehicle owners in major European markets are becoming important engines for brand penetration. Once the positive experiences of these early users are widely disseminated on social networks, the trust cost for subsequent potential car buyers will be significantly reduced, propelling market penetration from 'novelty' to 'mainstream.'

For Chinese new energy vehicle companies with advantages across the entire industrial chain, this is a highly promising favorable window. If international oil prices remain high above $100 per barrel for an extended period, it will force more consumers worldwide, especially European private car users highly sensitive to usage costs, to turn their attention to economical hybrid and pure electric products.

Supply Chain Restructuring Catalyzed Passively

The Hormuz crisis has, in a more straightforward and brutal manner, pushed 'supply chain resilience' from strategic memoranda to the top of the emergency agenda.

The modern supply chain system of the automotive industry is a precision machine built through decades of continuous optimization. Production models such as 'just-in-time' have achieved extremely high capital efficiency by maintaining extremely low inventory levels. Their operating premise is that the stability of the global supply chain is the norm, and interruptions are occasional short-term anomalies.

However, from the chip shortage in 2021 to the nickel price fluctuations in 2022, and then to the Red Sea shipping crisis in 2024, 'once-in-a-century' supply chain shocks have been striking at the foundations of this premise with increasing frequency. The Hormuz crisis is the most severe one to date. It has not only cut off logistics channels but also simultaneously struck at energy supply and the supply of some core raw materials, placing the transnational automotive industry under extreme stress testing.

Faced with this reality, the transformation of the global automotive supply chain has become unavoidable. The transition from 'efficiency first' to 'resilience first' has long been a consensus in theory, but it is often the painful real-world shocks that truly accelerate its implementation.

Geopolitical diversification is the core path for building supply chain resilience. Japanese automakers are already accelerating their strategic transformation of aluminum procurement from 'Gulf concentration' to 'global dispersion': Australia, Canada, and Southeast Asia are becoming important alternative sources.

Europe, on the other hand, is promoting a 'nearshoring' strategy: expanding aluminum processing capacity in North Africa and Eastern Europe to shorten logistics distances and reduce exposure to geopolitical risks. The EU's 'Critical Raw Materials Act' has also listed aluminum as one of the strategic raw materials, planning to increase Europe's domestic aluminum processing capacity by at least 30% by 2030 through subsidies and regulatory incentives.

For Chinese automakers, domestic bauxite resources and a complete aluminum processing industrial chain provide natural safeguards, but this does not mean they can rest easy. As more destination markets begin to emphasize the localization of links and raw materials, the global supply chain layout of Chinese automakers also faces the strategic necessity of 'decentralization.' Perhaps establishing localized production bases around destination markets is the long-term way to avoid tariff barriers and deepen market rootedness.

Of course, the more important strategic move at present is to transform the 'time window advantage' into a 'market rootedness advantage.' In the European market, the construction of localized service networks for charging, maintenance, and insurance should be accelerated to convert user word-of-mouth into a brand moat. In the Southeast Asian and Middle Eastern markets, an industrial ecosystem beyond 'trade exports' should be built based on the deepening of local factory construction and government relations. In the field of intelligent driving, the negotiation window period in the Middle East should be transformed into the rapid locking of localized cooperation to hedge against future geopolitical uncertainties that may intensify with the 'first-mover advantage' of commercial implementation.

For the global industry as a whole, this crisis should be seen as a rare 'catalyst' to accelerate the process of new energy transition and supply chain resilience building by leveraging the longer-term changes in consumer expectations brought about by high oil prices. More importantly, this crisis clearly reveals that the strategic significance of energy transition lies not only in climate goals but also in the energy security of countries and industries. This deepened understanding will provide more lasting political and social impetus for electrification transition than any single subsidy policy.

Crisis Catalyzes Transformation, Window Determines Success

A temporary ceasefire does not mark the end of the crisis but rather a critical window period for the global automotive industry to shift from responding to geopolitical cost shocks to embracing energy structure and supply chain reshaping. Soaring oil and gas prices are pushing electric vehicles from a 'policy-driven' option to an 'economically driven' inevitable choice, with the booming used car market being a clear harbinger of this historic transformation.

From a broader historical perspective, every major energy crisis has profoundly reshaped the competitive landscape of the automotive industry. The 1973 oil crisis spurred the rise of Japanese fuel-efficient compact cars in the North American market, making it difficult for the Big Three American automakers to recover their dominant positions. The 2008 oil price surge accelerated the popularization of hybrid technology, solidifying the cross-era significance of the Toyota Prius. Now, the Hormuz crisis is becoming a new chapter in this historical sequence—and this time, it is Chinese new energy vehicle companies with the most complete electrification industrial chains that are standing at the historical window of opportunity (fengkou, meaning 'at the forefront').

With their deep local roots and accumulating technological advantages across the entire new energy vehicle industrial chain, Chinese companies undoubtedly occupy a favorable position in this round of global industrial restructuring and are expected to win a larger market share and voice. Regardless of the final outcome of subsequent negotiations, the pace of industrial transformation is irreversible. In this future-oriented competition, whoever can most rapidly deploy a more resilient supply chain and most precisely seize the historic window of electrification transition will gain the upper hand in the global automotive landscape of the post-crisis era.

Image: From the Internet

Article: Auto Review

Layout: Auto Review

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’