Is the Chinese Market Still a 'Market' for the German Automotive Industry?

04/30 2026

04/30 2026

458

458

'China is both a partner and a competitor.' This assessment was made unhesitatingly by Hildegard Müller, President of the German Association of the Automotive Industry (VDA), during a conversation. However, this leads to a follow-up question: As competition reshapes the industry landscape, can the term 'market' still fully capture the essence of China's role?

Standing amidst the sprawling 380,000-square-meter exhibition halls of the 2026 Beijing Auto Show, surrounded by 1,451 vehicles on display and 181 global premieres, the sheer volume of information is overwhelming. To be frank, absorbing it all is an impossible task.

Amidst this chaos, a persistent question arises: What industry trends are we truly witnessing beneath the surface of continuous expansion? This is not just a conundrum for visitors but a shared narrative that companies and industry institutions are striving to decipher.

Starting with record-breaking figures, the 2026 Beijing Auto Show underscores a further shift in the competitive landscape. As domestic brands and new entrants secure more prominent positions, even showcasing in standalone halls, German automakers have significantly ramped up their participation. Volkswagen Group unveiled four global premieres, with Volkswagen Anhui's 'Zony 09' development cycle compressed to approximately 24 months. BMW showcased the iX3 and i3 long-wheelbase versions, powered by its new-generation cluster drive and explicitly tailored to Chinese user needs. Mercedes-Benz exhibited nearly 40 models, placing the important global debut of its core SUV—the electric GLC—in Beijing.

New-Generation BMW iX3 Long-Wheelbase Version

These moves signal German automakers' intensified commitment to the Chinese market. However, beyond the products on display, what deserves closer scrutiny is the nuanced attitude of VDA President Hildegard Müller during the auto show. She reaffirms the importance of cooperation while acknowledging the reality of competition. This delicate balance between 'partner' and 'rival' extends German automakers' strategic considerations beyond exhibition booths into deeper transformation narratives.

President of the German Association of the Automotive Industry (VDA)

Hildegard Müller

The Dual Narrative of the German Automotive Industry in China

From a financial standpoint, the relationship between the German automotive industry and the Chinese market is undeniably a 'partner narrative.' VDA data reveals that in 2025, German automakers sold approximately 3.7 million passenger vehicles in China, surpassing their domestic sales by over 1.7 million. In essence, one in every six new cars sold in China bears a German brand. For Volkswagen, BMW, and Mercedes-Benz, the Chinese market has long been a significant contributor to their global profit pools—a commercially successful story spanning over four decades.

However, viewed through a different lens, this relationship also embodies a 'rival narrative.' Over the past few years, competition in the Chinese market has been among the fiercest globally, characterized by frequent price wars. More critically, many companies transitioning to new energy vehicles have yet to achieve stable profitability, and the industry as a whole remains in a phase of trading scale for market share, as noted in earlier industry forum discussions. The high market share once enjoyed by German brands is challenging to replicate in the current environment.

Müller does not shy away from this narrative contradiction. Her statement at the auto show was clear: 'China is both a partner and a competitor.' This succinctly encapsulates the duality of their relationship. Her logic is equally straightforward: Precisely because competition is intense, cooperation becomes more valuable. 'The German side excels in system integration and vehicle safety, while the Chinese side is unparalleled in iteration speed and understanding of local needs. For instance, in core digital domains like advanced autonomous driving and intelligent connectivity, Chinese and German automakers are already on par, with highly complementary strengths,' Müller explained.

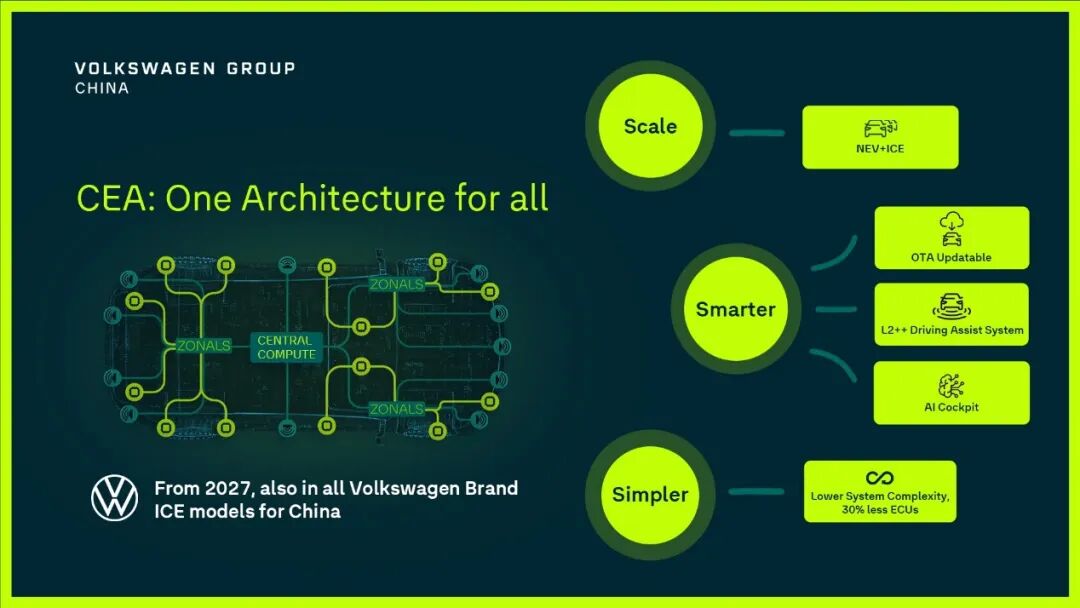

Volkswagen Group's CEA Architecture

The data she cited is impressive: In 2025, German automakers' sales in China significantly outpaced their domestic market. However, these figures also underscore the German automotive industry's deep reliance on the Chinese market. Yet, precisely when this reliance remains strong, the 'dual narrative' judgment becomes more pronounced: The pressure German companies feel does not stem from the current profitability of their Chinese counterparts but from the asymmetric game theory dynamics between two capital logics operating in the same market.

In the world's most competitive new energy vehicle market, this 'abnormal' pressure often arises from fundamental differences in the value assessment systems followed by both sides. For German automotive giants, profitability is a constraint. Earlier, Patrick Heinecke, CFO of Volkswagen China, stated that as publicly traded or family-controlled global enterprises, they must maintain certain profitability benchmarks to support stock prices, R&D investments, and employment commitments under union expectations. Every vehicle sold in China must align its pricing logic with global profit statements, with price reduction flexibility constrained by manufacturing costs, brand premium, and shareholder return expectations.

For many Chinese domestic automakers, however, profitability remains a 'long-term variable' in some cases. They are supported by capital willing to accept extended return cycles and cross-border capital viewing automobiles as ecological entry points. The patience of these forces allows companies to defer 'profitability' until market share and user scale reach critical points.

The clash of these two competitive logics has created a situation where German automakers face not just pressure on their pricing systems but systemic erosion of their entire value chain discourse power. When the market's value perception of a smart electric vehicle is re-anchored at a lower price point, the engineering advantages German brands once relied on for pricing—such as powertrain precision, vehicle safety, and chassis tuning expertise—still exist but are losing weight in consumers' willingness to pay. In other words, German companies fear not that they cannot build good cars but that the definition of 'good' is shifting under a new value coordinate system.

Thus, the structural root of the 'partner and rival' dual narrative lies here: German companies' profit dependence on the Chinese market remains real, but the value chain logic supporting this profit pool is being rewritten. This rewriting is a natural friction resulting from the parallel evolution of two industrial organizational models in the same testing ground.

For this reason, the posture displayed by German companies at this auto show is even more noteworthy. The series of product and rhythm adjustments mentioned earlier are not isolated moves but external manifestations of the same logic: On one hand, they are deepening local integration; on the other, they are reorganizing their engineering systems to respond to new competitive intensities.

These actions are both extensions of cooperation and direct responses to competition. They attempt to prove that systematic engineering capabilities can adapt to 'China Speed,' while localized R&D can participate in defining new values without entirely sacrificing brand premium.

When Speed Becomes a Proof of Competence

The 'all-in' posture of German automakers at the 2026 Beijing Auto Show is unmistakable. Whether through significantly compressed development cycles, structural product adjustments for the Chinese market, or placing global premieres of key models in Beijing, these signals collectively point to one conclusion: German brands are systematically rewriting their product and decision-making rhythms in China.

Against this backdrop, individual flagship projects become particularly critical. For example, Volkswagen Anhui compressing its vehicle development cycle to 24 months represents not just efficiency gains but an external manifestation of organizational mechanism reconstruction. BMW's panoramic iDrive in its new-generation models is equally noteworthy: This next-generation intelligent cockpit, built on the technical foundation of China's version of BMW's new-generation operating system X, has 70% of its source code developed and optimized in China. It aims to ensure driving focus while creating a more immersive intelligent experience tailored to Chinese users, fully reflecting BMW's deep local R&D in China.

VDA President Müller called these models 'examples of having the best of both worlds': retaining German engineering traditions and reliability while embedding digital and AI capabilities for Chinese users. She added a judgment that in providing tailored solutions, 'no one can do it better than us.'

These two statements form a text worth analyzing closely. 'Having the best of both worlds' acknowledges the necessity of learning and integration, while 'no one can do it better than us' attempts to reincorporate this capability into their own advantage narrative framework. In this tension between restraint and assertion, the dual proof proposition implicit in the German technological offensive at this auto show becomes clear: They must prove they can learn China Speed while ensuring their engineering soul is not diluted in the process.

Of course, the essence of 'keeping pace with the Chinese market' lies not in time itself but in the organizational mechanisms supporting these numbers. For example, a 24-month development cycle is not merely acceleration for traditional German engineering processes but implies reconstruction at the foundational level.

Traditionally, German vehicle development follows a 'waterfall' process: From conceptual design, technical verification, engineering prototyping to mass production release, each stage has strict quality checkpoints, with development rhythms radiating outward from European headquarters. The advantage of this system lies in risk control and consistency assurance, but the cost is long decision chains and slow local responsiveness.

To understand what 'Zony 09's 24 months represents, one must see the structural adjustments behind it. As Volkswagen's new joint venture entity in China, Volkswagen Anhui has enjoyed higher decision-making autonomy than traditional joint ventures since its inception. According to sources close to the project, it adopted a co-located, parallel development model with Chinese and German teams, front-loading some engineering verification steps previously done in Europe to China, and shortening procurement and testing cycles through deep integration with the Chinese supply chain. This means the Chinese team gained more voice in early stages of product definition, technical solutions, and supplier selection.

Thus, Müller's mention during the auto show of German strengths in 'vehicle technology, safety, and system integration' is no coincidence. It is both a commitment to the outside world and a reminder internally: Speed can be learned, but safety baselines cannot be compromised.

When the Soul Faces Redefinition

Beyond proving speed, German companies simultaneously face the proof of 'soul'—whether their engineering traditions remain an irreplaceable source of premium in the era of electrification and intelligence. However, the depth of the 'China-exclusive' label at this auto show provides a new observational window. For example, in digitalization, some features developed for the Chinese market have shifted from 'local adaptation' to 'local leadership.' Certain intelligent experiences are not extensions of European versions but are redefined based on Chinese user needs.

This raises a question worth exploring: If 'engineering tradition' is considered the core asset of German brands, then when product definition authority is partially ceded to local teams and digital functions are dominated by Chinese teams, in what sense do these vehicles still represent 'German engineering'? The answer may lie in a new division of labor: German strengths may be converging toward 'non-negotiable foundational capabilities,' such as body structure safety, chassis tuning, powertrain reliability, and system integration verification, while Chinese teams gain greater definition rights in 'experience layers' like interaction logic, content ecosystems, AI training data, and local scenario understanding.

What Müller calls 'having the best of both worlds' may be the prototype of this division of labor: It is no longer the traditional joint venture model where one side provides technology and the other provides markets but a more equitable, domain-specific leadership structure in respective areas of strength.

After this series of technological offensives, Müller's assessment of the situation is exceptionally sober. She summarizes the current predicament as follows: Downward pressure on the global economy directly suppresses consumer willingness in China's premium luxury car market; the aftershocks of price wars continue, with many companies' automotive businesses under profit pressure; and the high market share German automakers once enjoyed in China was formed under conditions when China's domestic automotive industry was still taking shape—'it is not a replicable benchmark but an era that has ended.'

The honesty of this assessment forms the premise for understanding all technological moves at this auto show. Precisely because 'the old era's market share benchmark' has been declared invalid, proving 'speed' becomes urgent. Precisely because the 'soul's' value needs re-argumentation in new competitive dimensions, defining its boundaries becomes a strategic issue.

Müller disclosed that, spanning from 2025 to 2029, German automakers intend to allocate €320 billion towards research and development, along with an additional €220 billion for capital expenditures, such as factory modernization initiatives. A substantial portion of the cash flow required for this colossal investment remains contingent upon the profit contributions generated from the Chinese market. This implies that the endeavors of German automakers to demonstrate their speed and essence in China are being financed by the very market whose returns are being put to the test by this intense competition.

This could potentially elucidate why Müller characterized everything showcased at the Beijing Auto Show as a 'mutual learning process' and concluded this unprecedented technological exhibition with a seemingly modest comment: 'We have not only embraced 'China Speed' but also rediscovered our true selves through this mutual learning journey.' Under the duress of dual proof, 'rediscovering ourselves' is not merely a rhetorical flourish but a factual depiction of the ongoing organizational transformation, the redrawing of capability boundaries, and the evolution of value standards.

Müller remarked, 'We approach all of this with utmost seriousness, yet we also strive for continuous growth while navigating through challenges, perceiving it as a mutual learning endeavor.' This could very well be the most candid statement emanating from the German industry at this Beijing Auto Show.

China: Beyond Just a 'Market'

The Chinese market serves as both a catalyst for the transformation of German automobiles and their most crucial funding source, as well as a technological mirror. This paradoxical situation is unlikely to dissipate in the near future. The Chinese market has transcended its role as merely a sales territory; it has now evolved into a 'training ground' and a 'technology source'.

For the German automotive industry, this transformation, on one hand, offers the most intensive environment for technological advancement: electrification, intelligence, price competition, user demands, and so forth, are all magnified to an extreme degree here. On the other hand, it also signifies that the existing advantage system must reaffirm its value in a faster-paced and more volatile scenario.

It is in this context that the 'mutual learning' emphasized by Müller (Note: corrected from "Muschia" assuming it's a typo) transcends mere cooperative rhetoric and approaches a more realistic portrayal: no single party can accomplish the transformation independently along the existing path.

Image: Sourced from the Internet

Article: Auto Review

Layout: Auto Review

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

-

![]()

Doubao Goes 'Professional', Volcano Rolls the Snowball

-

AI: No Sign of a Bubble!

-

![]()

NVIDIA-Backed AI Unicorn Secures $1.5 Billion Funding: Revenue Soars 2000%

-

![]()

Doubao Pro is Here: How Can Seed 2.1 Be Integrated into Real Processes?

-

"PCB Juice" Sees Four Consecutive Declines: Even Computing Power Material Suppliers Can't Lift This "Old Stock"

-

![]()

Potential 'Seismic Shift' in the U.S. TV Industry: Competition Shifts from Hardware Sales to Traffic Entry Points

-

![]()

Audi A6L's Defense in the Luxury C-Class Market: Following Huawei's Smart Driving Integration, Is Large-Battery HEV the Next Move?