60%! Electric Vehicles Surge, Gasoline Vehicles Face Countdown

05/13 2026

05/13 2026

410

410

Joint Ventures Wane, All Else Flourish

Author|Wang Lei

Editor|Qin Zhangyong

How popular are new energy vehicles currently?

Among every 10 car buyers, 6 opt for electric vehicles.

This statistic comes from the latest data released by the China Passenger Car Association (CPCA). In April, retail sales of new energy vehicles soared to 849,000 units, with a penetration rate reaching 61.4%. This marks the first time the domestic penetration rate for new energy vehicles has exceeded 60%.

Moreover, this achievement was made despite an overall 21.5% decline in the automotive market. This indicates that new energy vehicles have shifted from being a market "supplement" to a "leading force." They are no longer just a novelty but have become mainstream.

At the same time, exports have also witnessed explosive growth, particularly for new energy models, which accounted for 52.7%—another historic milestone, surpassing the 50% mark.

As new energy vehicles surge ahead, other segments are struggling. Take Honda, for instance, which recently made headlines for its poor performance—only 22,600 units sold in April, less than Xiaomi SU7's sales alone.

It's truly disheartening.

01

Growing Adoption of New Energy Vehicles

Let's delve into the specific data first.

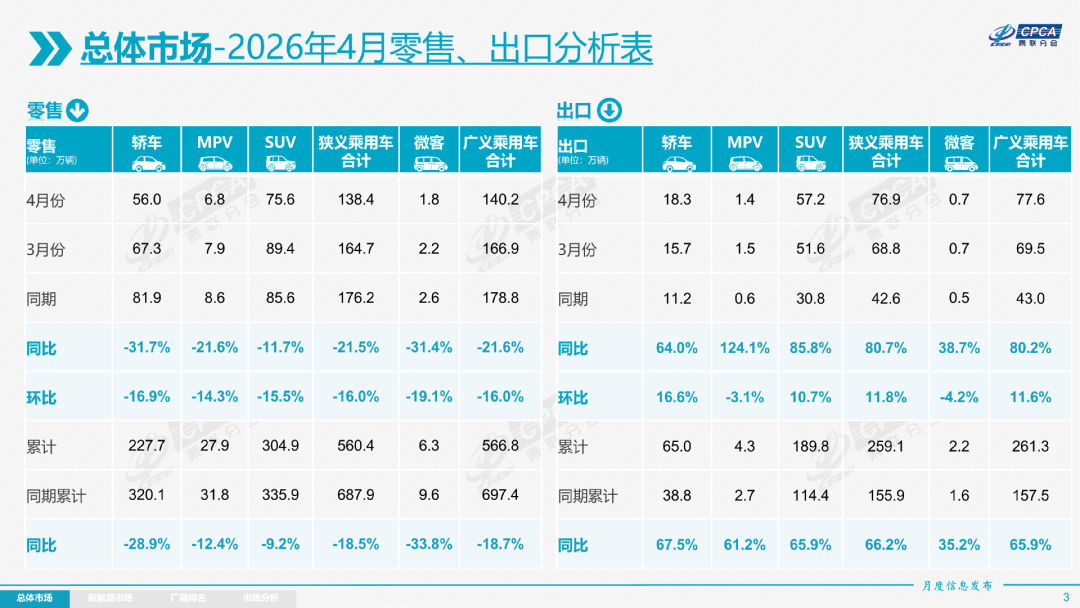

In April, the retail penetration rate of new energy vehicles in the overall domestic passenger vehicle market reached 61.4%. Both year-on-year and month-on-month increases were close to 10%, with a year-on-year rise of 9.7 percentage points and a month-on-month increase of 9.6 percentage points.

However, throughout April, the national passenger vehicle market exhibited characteristics of "overall pressure and structural differentiation."

From a broader perspective, the total retail volume of narrowly defined passenger vehicles in China in April was 1.384 million units. Compared to March and the same period last year, sales declined significantly, with a year-on-year decrease of 21.5% and a month-on-month decline of 16.0%.

While the total volume is declining, the share of new energy vehicles is rising, clearly indicating a trend: fewer people are buying fuel vehicles.

The impact of rising fuel prices on fuel vehicles is already evident. According to CPCA data, fuel vehicle sales decreased by 365,000 units year-on-year in April, with only 530,000 units sold at retail, a sharp decline of 37% year-on-year and 33% month-on-month. This decrease accounted for a staggering 84% of the overall sales decline, becoming the primary reason for the poor performance of the automotive market.

Moreover, it has become the sole major factor dragging down the entire passenger vehicle market. "This is mainly due to the decline in retail sales of fuel vehicles. Retail sales of fuel vehicles fell short of expectations, directly leading to a decline in April’s retail sales and also contributing to the year-on-year decline in cumulative retail sales of passenger vehicles nationwide for the first four months of the year," explained Cui Dongshu, Secretary-General of the CPCA.

Breaking it down by numbers: from January to February, retail sales of fuel vehicles decreased by 740,000 units year-on-year, accounting for 40% of the total decline in the passenger vehicle market. In March, fuel vehicle sales dropped by 345,000 units year-on-year, with their impact on the market decline rising to 52%. From January to April, retail sales of fuel vehicles fell by over 1.45 million units year-on-year, accounting for 84% of the decline in passenger vehicle retail sales.

If we extend the timeline further, this transformation becomes even more striking. In 2020, fuel vehicles still held over 90% of the market share in China, but now it has plummeted to less than 40%. In less than six years, China’s automotive industry has undergone an extremely dramatic structural transformation.

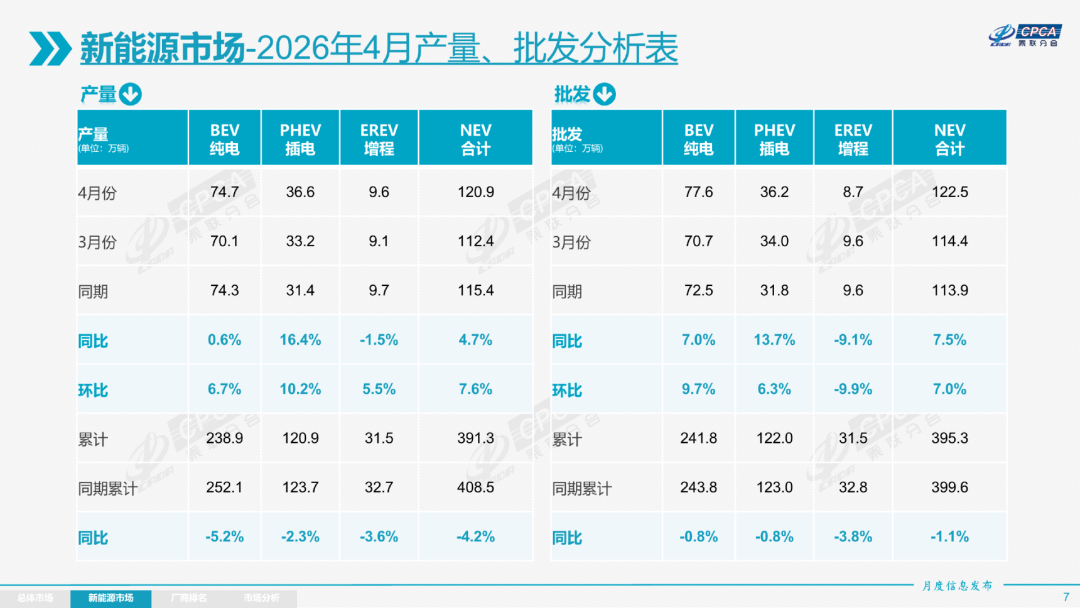

In stark contrast to the cooldown of fuel vehicles, new energy vehicles are "soaring." In April, production of new energy passenger vehicles reached 1.209 million units, a year-on-year increase of 4.7% and a month-on-month rise of 7.6%. Wholesale sales reached 1.225 million units, a year-on-year increase of 7.5% and a month-on-month rise of 7.0%.

However, amid the overall sluggishness of the domestic automotive market, retail sales of new energy passenger vehicles in April were 849,000 units, a year-on-year decrease of 6.8% and a slight month-on-month decline of 0.3%. Yet, against the backdrop of the sharp decline in fuel vehicle sales, the retail penetration rate of new energy vehicles surpassed the 60% mark.

From a powertrain perspective, battery electric vehicles (BEVs) accounted for 579,000 units in retail sales, making up 68.2% of total new energy retail sales and remaining the absolute dominant force. Plug-in hybrid electric vehicles (PHEVs) accounted for 192,000 units in retail sales, a year-on-year decrease of 25.4%. Extended-range electric vehicles (EREVs) accounted for 79,000 units in retail sales, a year-on-year decrease of 11.1%.

This also means that the long-discussed notion in the industry of "long-term coexistence of fuel vehicles and new energy vehicles" is gradually being shattered by reality. With the new energy penetration rate surpassing the 60% threshold, China’s automotive market has entered a new phase of "electric vehicle dominance," with fuel vehicles beginning to transition from market leaders to marginal players.

If we only talk about penetration rates, some might still think it’s driven by micro and small cars. However, among the data released by the CPCA, there’s a subtle detail: Class B electric vehicles are surging, with a significant increase in the proportion of models priced above 300,000 yuan.

In April, wholesale sales of Class B electric vehicles reached 243,000 units, a year-on-year increase of 27% and a month-on-month rise of 7%, accounting for 31% of the BEV market share, up 4.8 percentage points year-on-year. In contrast, the market share of economic electric vehicles in the A00+A0 segments declined. The former accounted for 9% of the BEV market share, down 12.3 percentage points year-on-year, while the latter accounted for only 27% of the BEV market share.

This also means that more people are buying expensive new energy vehicles, indicating a shift in perception that fuel vehicles are losing their default status.

However, the rapid rise in new energy penetration does not mean automakers are entering an era of high profits. According to CPCA data, the sales profit margin of the automotive industry further declined to 3.2% from January to March 2026. While this is better than the 2.9% seen in January-February, it remains at a historical low, far below the average profit margin of 6% for downstream industrial enterprises.

02

Overseas Expansion Becomes a Key Growth Driver

The divergence in the automotive market is also reflected in the varying fortunes of different brands.

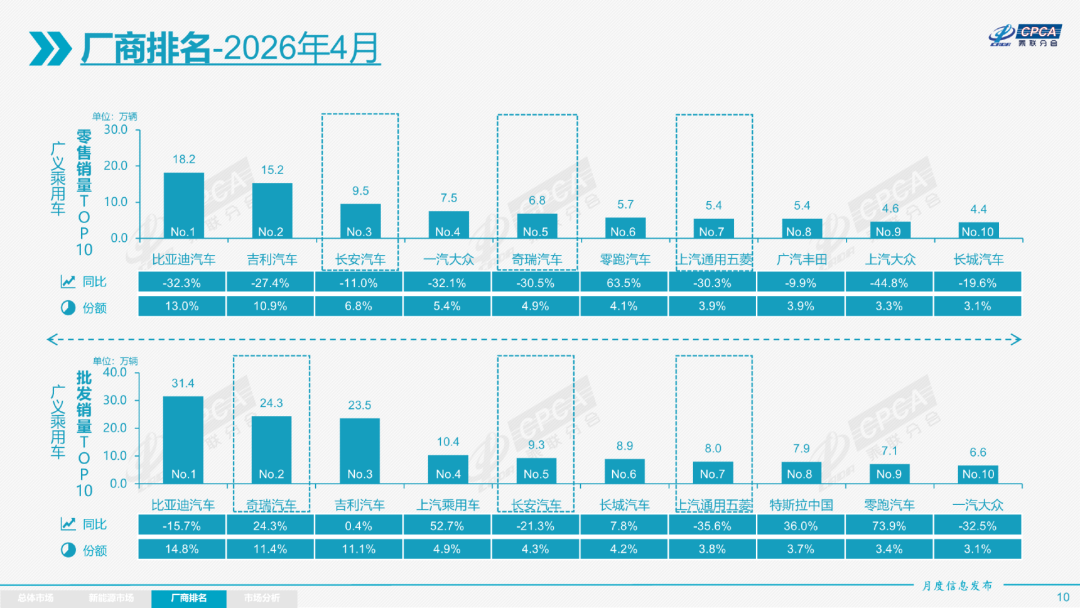

According to CPCA data, nearly all of the top ten automakers in retail sales experienced declines, with an average drop of around 30%. The only exception was Leapmotor, which saw a positive growth of 63.5% with 57,000 units sold.

Nevertheless, when we zoom out to the entire domestic market, independent brands are poised to reclaim dominance over the industry. In April, independent brands sold 970,000 units at retail. Although affected by the overall market downturn, with a year-on-year decrease of 16% and a month-on-month decline of 5%, their domestic retail market share reached a staggering 69.6%, up 4 percentage points year-on-year, accounting for 70% of the market.

In contrast, joint venture brands, which once relied on fuel vehicles to dominate half of the Chinese market, sold only 280,000 units at retail in April, a year-on-year decrease of 37% and a month-on-month decline of 33%.

The gap is even more pronounced when looking at new energy vehicle penetration rates.

According to CPCA data, the penetration rate of new energy vehicles among independent brands has reached 80.1%, while mainstream joint venture brands, despite some growth, only achieved a penetration rate of 14.1%. Among them, German brands stood at 13.3%, down 2.2 percentage points year-on-year; Japanese brands at 10.9%, down 1.2 percentage points year-on-year; and U.S. brands had the lowest at just 4.5%, down 0.3 percentage points year-on-year.

The luxury car market also struggled to remain unscathed, with retail sales of 140,000 units in April, a year-on-year decrease of 16% and a month-on-month decline of 33%.

Notably, while the domestic retail market faced pressure, automotive exports shouldered the burden of sales growth. In April, domestic passenger vehicle exports reached 769,000 units, an year-on-year increase of over 80%, accounting for 36% of total manufacturer sales—up from just 19% during the same period last year.

New energy vehicles played a crucial role—exports reached 406,000 units, doubling year-on-year with a growth of 111.8% and a month-on-month increase of 18.3%, accounting for 52.7% of passenger vehicle exports, up 8 percentage points year-on-year. Among them, BEVs accounted for 57.2% of new energy exports, marking the first time in history that the export share surpassed 50%.

Looking at the top three exporters, BYD exported 134,500 units in April, a year-on-year increase of 70.9%, setting a new record for the brand’s monthly exports, with overseas sales accounting for over 40% of total sales. Chery Group exported 177,600 units in April, more than doubling year-on-year and setting a new record for monthly exports by a Chinese automotive brand, with exports accounting for over 70% of total sales. Geely Automobile also achieved strong overseas export sales in April, reaching 83,200 units, a year-on-year increase of about 120%, marking the fourth consecutive month of doubling year-on-year growth.

Of course, judging that the entire automotive industry has entered the electric vehicle era based solely on the temporary penetration rate of new vehicles would be overly one-sided. After all, we cannot only look at new sales but also consider the existing stock and the total number of vehicles in use.

From the perspective of existing stock, fuel vehicles remain the absolute protagonists. As of the end of 2025, the domestic stock of fuel vehicles stood at a staggering 320 million units, accounting for 88% of the total. Moreover, the majority of these 320 million fuel vehicles are less than 5 to 8 years old.

This means that these vehicles will remain the dominant models on the roads for the next three to five years. However, it is undeniable that with the gradual rise in new energy penetration, new energy vehicles are set to take center stage in the industry, and nothing can stop that.

-

![]()

Pity Stirs as OpenAI and Anthropic Dive into Financial Maneuvers

-

![]()

Small Pre-Order Numbers Are Just a Sneak Peek: Seres V9 Faces Three Major Challenges to Overtake GL8

-

![]()

AI Enters the Era of 'Self-Evolution', Li Yanhong First Proposes 'DAA' as the Measurement for the AI Era

-

![]()

Mercedes-Benz China Executive Steps In to Steer Volvo Through Turbulent Waters

-

![]()

She Once Steered OpenAI's Technology, Now Aims to Redefine Its Rules

-

![]()

Porsche Bids Farewell to Bugatti Amid Tears as Mysterious Buyer Stealthily Takes the Helm

-

![]()

60%! Electric Vehicles Surge, Gasoline Vehicles Face Countdown

-

![]()

Decade’s First Leadership Shift: Can Duan Jianjun Revitalize Volvo?