Overcapacity Weighs on Europe, China’s White Knight Rides to the Rescue

05/14 2026

05/14 2026

518

518

Introduction

Introduction

Chinese electric vehicle companies are poised to address Europe’s overcapacity challenges.

The European automotive industry stands at a pivotal juncture—a sentiment that has resonated for some time. Initially, Europe and its automakers faced the pivotal decision to transition toward electrification. Now, with electrification becoming an unstoppable force, history’s wheels are turning toward the factories of these established traditional automakers.

Recently, numerous foreign media outlets have reported that the once-thriving assembly lines of Europe’s automotive industry now lie dormant, with factories becoming “zombie assets.” The combination of sluggish demand following the 2019 pandemic, the substantial costs associated with electrification transformation, and fierce competition from Chinese automakers has collectively driven the continent’s automotive manufacturing sector into an unprecedented predicament.

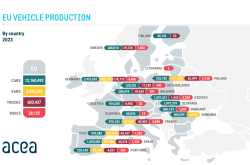

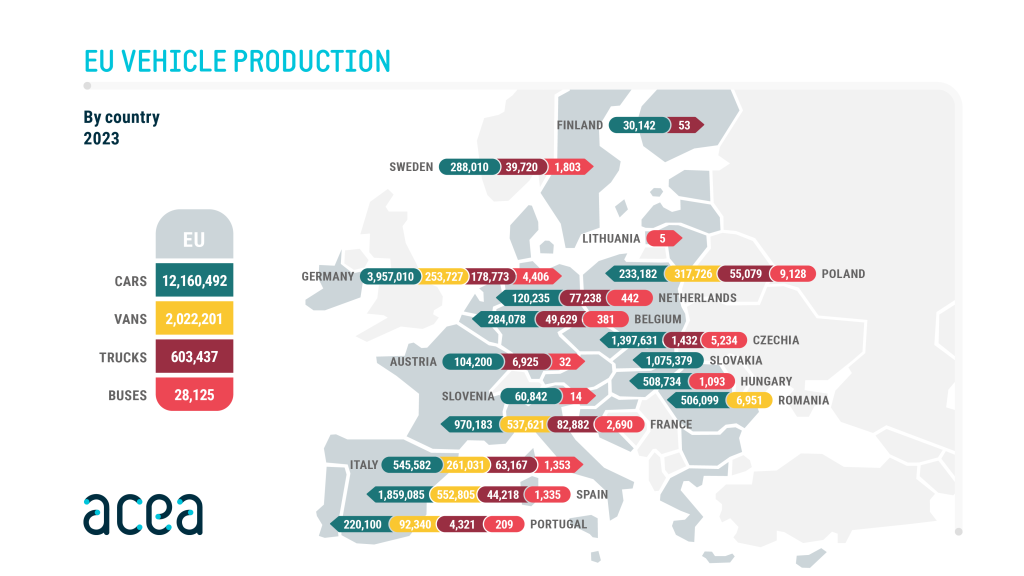

According to data from the trade union organization IndustriALL, Europe’s annual automotive production has plummeted from 16 million units in 2018 to 11.4 million units in 2024, marking a nearly 30% decline. This downturn has been accompanied by overcapacity and waves of layoffs, with the automotive components industry alone shedding 54,000 jobs in 2024 and an additional 22,000 in the first half of 2025.

As European manufacturers grapple with these challenges, Chinese electric vehicle companies, armed with technological prowess and cost advantages, view Europe as a “new frontier.” Three years ago, brands like BYD, MG, Chery, and Geely were virtually unknown in Europe. Today, according to Dataforce, they account for 9% of overall European sales and 14% of electric vehicle sales.

However, EU tariff barriers and localization regulations requiring European assembly to qualify for subsidies are compelling Chinese automakers to shift from exports to local production. Consequently, European factories desperate to shed excess capacity and Chinese automakers eager to establish a foothold are engaging in mutually beneficial negotiations.

01 The Familiar ‘Joint Venture’ Model

Faced with the stark reality of persistently high factory idle rates, European automakers are making a once-unthinkable decision: entrusting production lines to their former competitors—Chinese automakers. Rather than incurring exorbitant costs to shut down factories and risk social unrest, they are seeking Chinese partners to take over. This strategy is evolving from isolated cases into an industry-wide trend.

In 2023, Chery Automobile broke new ground by acquiring a former Nissan factory in Barcelona, Spain, with plans for an annual production capacity of 200,000 units. This move paved the way for subsequent deals. Last month, Chery further announced plans to open a research and development center in Paris, dedicated to developing a small electric vehicle for production and supply in Europe.

Meanwhile, Nissan is reportedly considering selling its factory in Sunderland, UK—its last remaining plant in Europe—to Chery or China’s Dongfeng Motor. Felicie Burelle, CEO of French automotive components maker OPmobility, commented that selling European factories to Chinese manufacturers “is a wise choice rather than exacerbating overcapacity.”

Most symbolically, Stellantis—a French-Italian-American automotive giant and the first European manufacturer to publicly embrace this decision—announced it is considering selling part of its Villaverde factory in Madrid to Leapmotor, in which Stellantis itself holds a 51% stake.

Moreover, Stellantis has plans to open a factory in Zaragoza, Spain, where Leapmotor will produce its own brand models. An electric SUV under the Opel brand may also be co-produced with Leapmotor in Zaragoza. According to disclosures, Stellantis’s ambitions extend further: it is considering selling three factories in France, Germany, and Italy to another long-term Chinese partner, Dongfeng Group. A union representative confirmed that a Dongfeng delegation recently visited the French factory.

In fact, Ford Motor has also joined this trend. Recently, Ford confirmed it is negotiating with China’s Geely Automobile to partially sell its factory in Valencia, Spain. Geely, already a co-owner of Renault’s factories in Brazil and South Korea, will produce a new model for the European market.

Germany’s Volkswagen has also shown strong interest. Its CEO, Oliver Blume, recently admitted that the company is studying “whether our Chinese cars have opportunities in Europe or whether we can cooperate with our Chinese partners.” He added that other options even include selling factories to defense manufacturers, but “the worst and most costly option is to close a factory.”

Meanwhile, some European models have already become deeply integrated into the Chinese supply chain. For example, Renault’s electric Twingo was designed in China and heavily relies on Chinese components. Additionally, Stellantis has openly co-produced complete vehicles with Chinese partners, rather than just sourcing components. According to Bernard Jullien, an automotive industry expert at Bordeaux University, this approach is a “shortcut” for manufacturers like Stellantis, which are struggling in Europe.

But where does this shortcut lead? Jullien stated: For manufacturers, suppliers, employees, and local officials, selling factories to Chinese companies is indeed more appealing than letting them disappear entirely. “But this is equivalent to providing a powerful competitor with an advantage in the heart of Europe, installing a strong accelerator for its penetration into our market.”

Given Chinese companies’ leading position in electric vehicle R&D, Jullien does not rule out the possibility of European companies outsourcing their entire electrification business to Chinese partners. He warned that this “every man for himself” strategy will ultimately boost Chinese manufacturers while “destroying Europe’s automotive manufacturing industry.”

However, with continuously shrinking demand and capacity utilization at only half, European automakers have few options left. For them, the arrival of Chinese white knights can at least preserve jobs in the short term, even if it means betting their future on a former adversary they once tried to resist.

02 Increasingly Proficient ‘Localization’

Undoubtedly, faced with such a severe overcapacity situation, Europe urgently needs external forces to inject vitality. Chinese electric vehicle companies are the most reliable partners in this context because they have also navigated the joint venture model when foreign brands entered China. Therefore, they bring not only capital but also commitments and actions for deep localization.

Georg Leutert, head of automotive and aerospace at IndustriALL, made it clear: “As long as decent employment opportunities can be protected or created through union representatives and collective bargaining agreements, no affiliated union in Europe will reject investment, including from Chinese companies.”

This indicates that Chinese capital is not perceived as a threat by European unions but as a positive force that can be negotiated and cooperated with. In fact, Chinese investors generally commit to long-term operations in Europe, hiring and training employees strictly in accordance with EU standards, thus effectively mitigating the social impact of large-scale layoffs.

Some early concerns suggested that Chinese investors might only engage in “screwdriver assembly”—importing completely knocked-down kits from China and completing final assembly in Europe—thus providing limited benefits to local employment and the supply chain. However, mainstream Chinese automakers are actually doing the opposite.

Justin Cox, global production director at LMC Automotive, pointed out that faced with rising trade protectionism, “many Chinese automakers are trying to overcome this barrier through localized production, using components sourced from domestic production.” Here, “domestic” refers to Europe.

Jeremy Carlock, a predictive analyst at GlobalData, also mentioned that low localization rates once “prompted European industry stakeholders to demand the introduction of a ‘Made in Europe’ content threshold.” Chinese automakers are actively responding to this demand by gradually increasing their procurement in Europe, covering key modules such as batteries, electric motors, electronic controls, chassis components, and interiors.

This deep localization not only brings new orders to European small and medium-sized suppliers but also promotes the alignment and mutual recognition of technical standards and certification systems between China and Europe, truly achieving “in Europe, for Europe.” For example, Geely’s ownership of Volvo demonstrates the positive value of Chinese ownership.

Under Geely’s control, Volvo Cars has not only preserved its Swedish management culture and union consultation traditions but also achieved double-digit growth in sales and profits, with sustained increases in R&D investment and steady progress in electrification transformation. This fully shows that Chinese investors are fully capable of respecting and integrating into Europe’s labor governance system while injecting new vitality and market vision into the enterprise.

Other Chinese automakers are actively learning from this successful experience, proactively communicating with local unions before entering the European market, and signing collective agreements covering wages, working hours, occupational health and safety, and other aspects. Some companies have even established Sino-European joint working committees at the factory level to regularly consult on production schedules, skills training, and other issues.

The EU previously imposed tariffs on Chinese electric vehicles due to anti-subsidy investigations, but it has been proven that trade barriers cannot revitalize European manufacturing. The true path forward lies in open cooperation. The EU’s newly proposed Industrial Accelerator Act explicitly emphasizes attracting foreign investment, creating local jobs, and promoting the implementation of green technologies. Chinese electric vehicle companies’ localized production in Europe is the best response to this policy direction.

Compared to transporting complete vehicles from Asia over long distances, local production significantly reduces carbon footprints, meeting the requirements of the European Green Deal. At the same time, these factories often repurpose existing idle facilities, avoiding additional consumption of land and resources from new construction. Therefore, the arrival of Chinese automakers is by no means a threat to European industry.

Currently, most discussions around Chinese outward investment focus on how to restrict it. However, for the European automotive industry, the interaction between struggling manufacturers, Chinese electric vehicle companies seeking market entry, and increasingly strict localization regulations may help prevent the decline of the continent’s industrial base—provided all parties can participate constructively.

Editor in Charge: Du Yuxin Editor: He Zhengrong

THE END

-

![]()

Four Major Independent Brands: Divergence Deepens | April New Energy Vehicle Market Report

-

![]()

Chinese-Style Reorganization: The Hierarchical Rivalry Between Foreign and Joint Ventures Amid the Auto Show Excitement | Cover Story: In China, for the Global – 2026 Beijing Auto Show Special Report

-

![]()

With Its New CEO at the Helm, Can Volvo Surpass Audi in the Coming Years?

-

![]()

Emulating Kazuo Inamori: The Overlooked Commercial Revolution Driving Dreame Technology’s Influencer Campaign

-

![]()

Who Deploys Products When AI Can Write Code? The 'Middle Layer' Battle Among Netlify, Vercel, and Cloudflare

-

![]()

Q1: AI Has Seamlessly Integrated into Every Aspect of Tencent's Operations

-

![]()

Overcapacity Weighs on Europe, China’s White Knight Rides to the Rescue

-

![]()

Is XPENG Merely a Stopgap Solution? Volkswagen’s Secret Weapon in China’s Autonomous Driving Race: CARIZON’s Advanced R&D Strategy