Leapmotor: Aiming for One Million Sales, but Gross Margin Slips First?

05/18 2026

05/18 2026

438

438

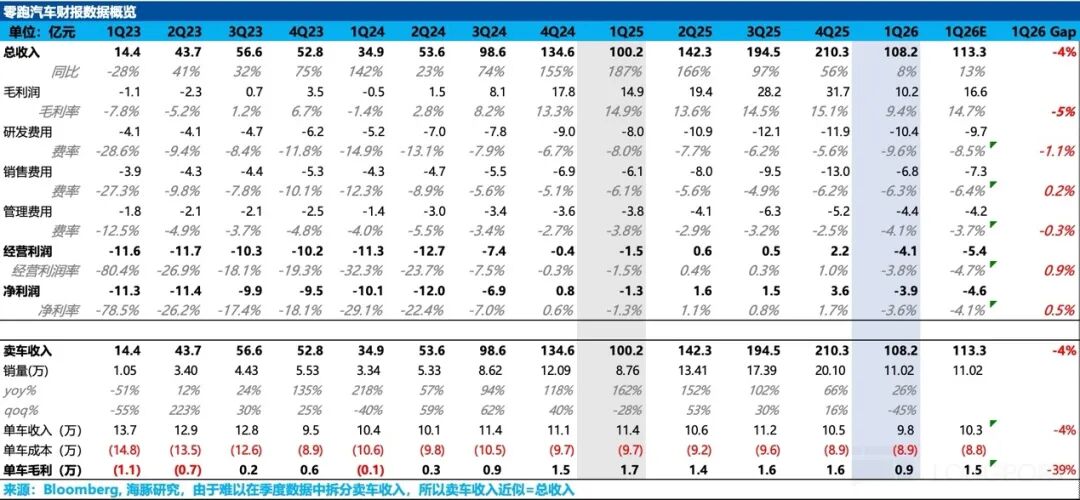

Leapmotor (09863.HK) released its Q1 2026 financial report after the Hong Kong stock market closed on May 15. The performance marked a departure from Leapmotor's historically stable operations. Despite respectable sales volume during the industry's off-season and reasonable cost control, both revenue and gross margin fell short of expectations, particularly vehicle gross margin, which significantly missed market forecasts. Details are as follows:

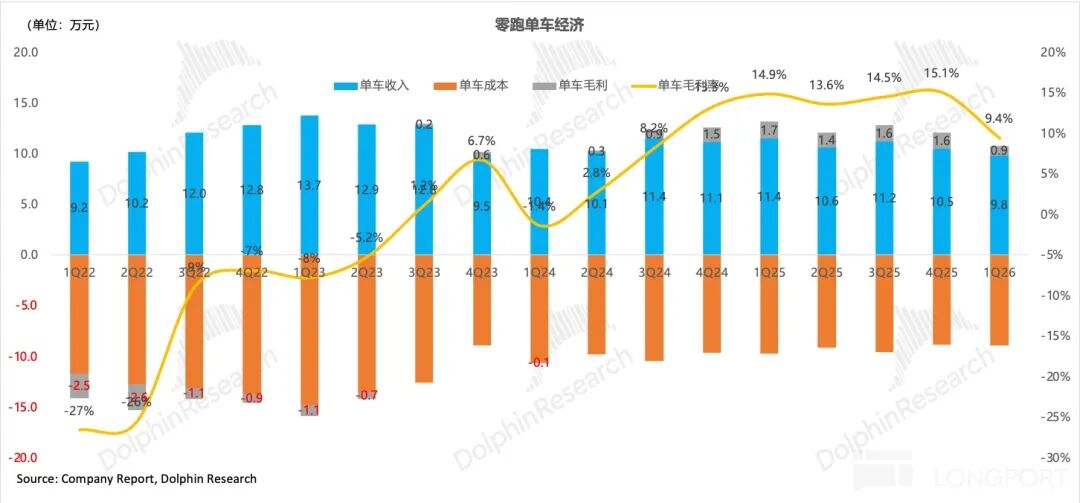

1. Revenue Misses Expectations, ASP Declines Further Due to Model Mix Shift: Quarterly revenue reached RMB 10.82 billion, up 8% YoY, but below market expectations. The increasing sales proportion of lower-priced models (B Series + T Series + A Series) significantly dragged down average selling price (ASP), which was the primary reason for the substantial miss in vehicle gross margin by 40 percentage points.

2. Gross Margin Declines 5.5 pct YoY; Even Excluding One-Time Gains, It Still Falls 3.9 pct YoY. The market has largely priced in the following factors:

1) Management provided guidance in the Q4 earnings call for a QoQ decline due to the Q1 off-season; 2) The proportion of T03 in the model mix increased by 11 pct QoQ to 22% in Q1, coupled with the launch of the new lower-priced A10 model in March, further shifting the model mix downward and reducing ASP.

Regarding vehicle costs, they were largely in line with consensus expectations. The company noted that the decline in production volume led to an increase in unit manufacturing costs, primarily due to:

a) Smaller sales scale and lower utilization rates of production capacity and component reserves in Q1; b) Rising raw material prices in Q1 2026, though the impact was limited due to advance procurement in Q4 2025. However, Dolphin Research reasonably speculates that the impact of rising battery material costs remains unavoidable.

3. Optimistic Q2 Guidance: Leapmotor guides for 240,000-250,000 units in Q2 sales. Combined with April's 71,000 units, this implies an average monthly sales volume of 87,000 units for May-June, which is a strong outlook. Export sales have been revised upward to over 150,000 units, with annual export sales targets largely as expected. Most importantly, gross margin guidance has been restored to 12-13%, providing a significant boost for Leapmotor, which is focusing on higher-volume, lower-priced models.

Dolphin Research's View

Overall, Leapmotor's vehicle gross margin in Q1 is concerning. From an expectations gap perspective, the miss was on the revenue side rather than the cost side. Once seasonal factors subside, Dolphin Research expects cost-side rebound to be rapid (given Leapmotor's strong cost control capabilities, as detailed in the Q4 2025 earnings analysis).

On the revenue side, the shift toward lower-priced models needs to be offset by the two models on the D platform. However, will pricing pressure remain seasonal as new models enter highly competitive markets? Fortunately, the company provided clear sales and gross margin guidance during the earnings call, which aligns with our long-term expectations for the company.

In Q1, Leapmotor entered a new product cycle with the sequential launches of A10 and D19. Market reactions have been mixed: A10, as a pillar for the one-million sales target, shows clear volume growth prospects, with a noticeable stock price boost post-launch. D19, as a brand-uplifting product, has seen a continuous stock price decline post-launch due to its lack of differentiation. The core concern is the potential erosion of ASP from a further shift toward lower-priced models.

In terms of the product lineup, among the four new models in this year's pipeline, A10 (March) and D19 (April) have already been launched. Management has further raised the full-year sales guidance to 1.05 million units based on better-than-expected order data for the new models. However, combined with the cumulative deliveries of only 180,000 units from January to April 2026, the average monthly deliveries from May to December need to reach nearly 110,000 units, posing significant pressure.

A10: Positioned as a high-volume small SUV, the A10 received over 40,000 orders in its first month on the market, with 14,372 units delivered in April, accounting for 20% of April's deliveries. Despite competing in the highly competitive sub-RMB 100,000 segment, the A10 demonstrates strong product competitiveness, particularly with its top variant being the first to bring LiDAR below the RMB 100,000 price point. Details are as follows:

- Base Variant: Features solid materials, offering a lower price point and autonomous driving performance as core selling points compared to similar models.

- Top Variant: Leveraging vertical integration capabilities, Leapmotor and BYD are currently the only two automakers in the industry to bring LiDAR down to the RMB 80,000-90,000 price range. Compared to the corresponding version of the Seagull, the A10's top variant is only slightly more expensive (less than RMB 1,000) but offers a larger body size and stronger three-electric system performance, making it a potential high-volume hit. We expect monthly deliveries of the A10 to exceed 30,000 units once production ramps up.

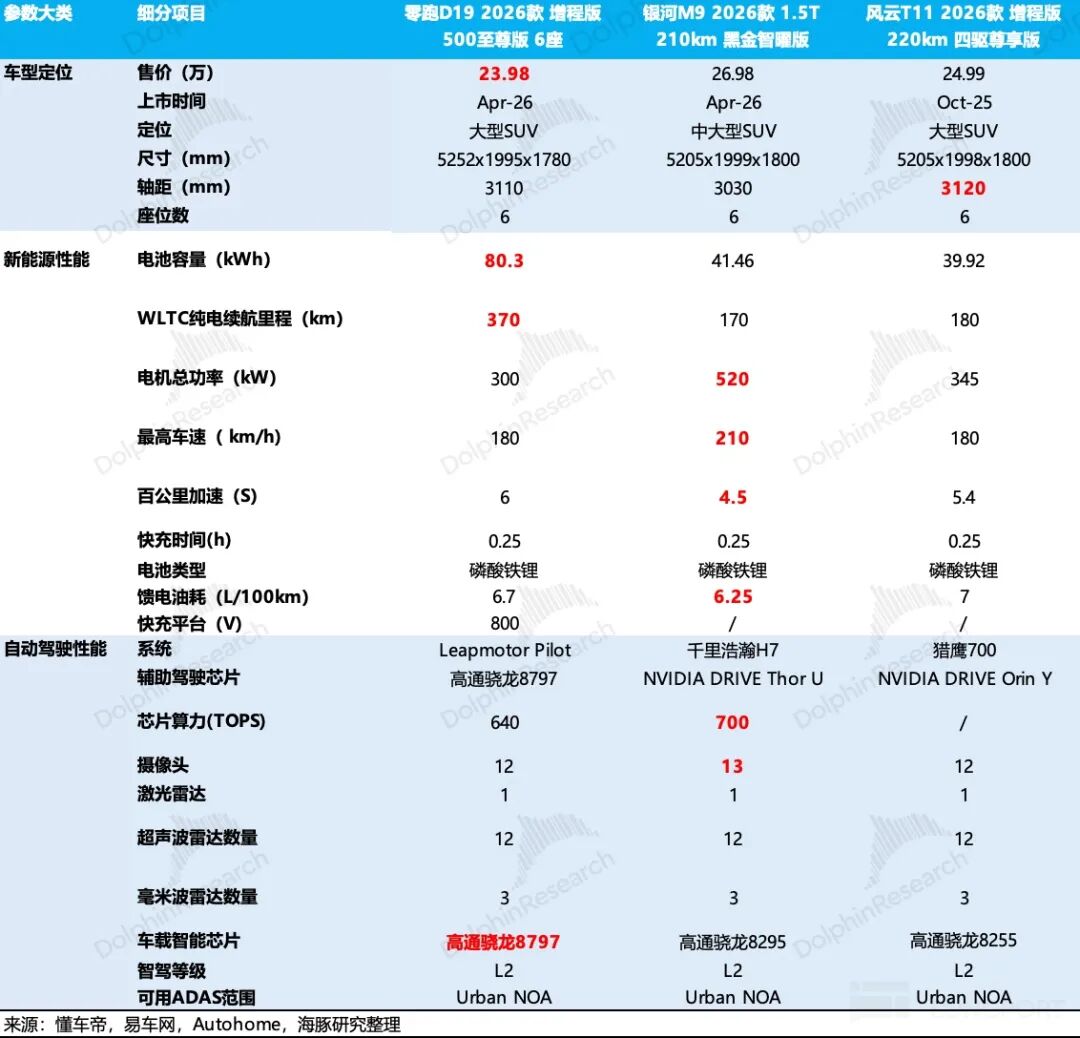

D19: As the first model from Leapmotor's flagship D platform, the highest-tech platform, the D19 is key to upgrading the model mix. Market performance has been largely in line with expectations, with over 10,000 orders received in the first seven days. The core high-volume variant is the 6-seat extended-range "Intelligent Supreme Edition" priced at RMB 240,000, accounting for 50% of orders.

While the high-volume variant offers a lower price, larger battery capacity, and longer range compared to its direct competitors (all-wheel-drive extended-range models in the same price range, such as the Galaxy M9 and Fengyun T11), it also suffers from slower acceleration, higher energy consumption, and weaker chip computing power, resulting in less distinct product advantages.

Priced between RMB 220,000-270,000, the D19's pricing is more than double the current overall ASP. However, the model mix continues to shift downward (the sales proportion of the relatively higher-positioned C Series has declined for six consecutive quarters, down 32% YoY). Brand uplifting may prove more challenging for Leapmotor, which does not operate separate sub-brands.

We conservatively estimate that the D19 will contribute 80,000 units in annual sales (10,000 units per month, consistent with management guidance), providing limited support for Leapmotor's overall ASP.

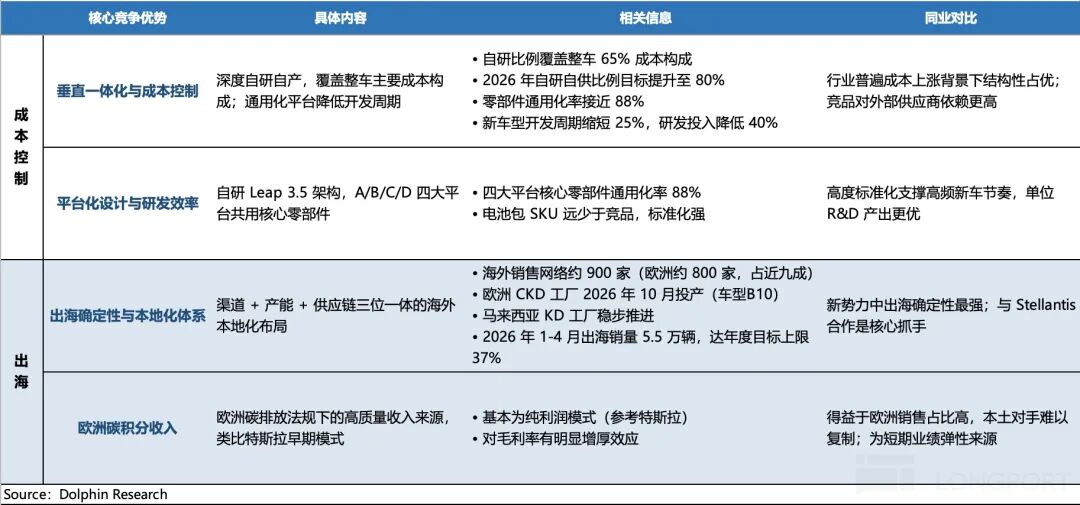

In the long term, we continue to emphasize Leapmotor's strong cost-reduction capabilities and scaling overseas expansion (high certainty, with overseas delivery proportion increasing 22.5 pct QoQ to 37%) as core factors for stabilizing vehicle gross margin, helping to offset margin erosion from model mix shifts and competitive/seasonal promotions.

For a more detailed value analysis, Dolphin Research has published a Same name article in the "Dynamic-Depth" section of the Changqiao App.

Related Charts:

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of the data in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or opinions expressed in this report shall not, under any jurisdiction, be construed as or deemed to be an offer to sell or an invitation to buy securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and data in this report are not intended for or proposed for distribution to jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations or would require Dolphin Research and/or its affiliates or associated companies to comply with any registration or licensing requirements in such jurisdictions, nor to citizens or residents of such jurisdictions.

This report reflects only the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright solely owned by Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research, (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Ali's Global Expansion: AliExpress Steps Out of the Shadows

-

![]()

Honda Corrects Course, Restructures Its 'New Four-Wheeled' Strategy

-

![]()

Don't Be Fooled by Your Home AI Again! D Lab Community's Latest Method, TraceLift, Exposes 'Fake Reasoning' and Ensures Model Thinking Processes Are Truly Reliable

-

![]()

Is Detroit Being Sidelined Amid Trump's China Focus?

-

![]()

19% Layoff Rate: Detroit's Big Three Bet on Future with Drastic Measures

-

![]()

Why These 17 Companies?

-

![]()

China’s Answer to Range Rover Has Arrived: A Review of Upcoming New Car Launches in the Second Half of the Year

-

![]()

BMW Didn't Bet on the Wrong Path, But Lacks a Toyota-Style Solution