In-Depth Analysis of the EU's Industrial Accelerator Act: Rewriting the 'Game Rules' for China's Auto Industry Going Global

05/25 2026

05/25 2026

360

360

On March 4, 2026, the European Commission unveiled a groundbreaking document—the Industrial Accelerator Act—that reshapes the relationship between China and Europe in the automotive industry. This is not just another round of tariff negotiations but a systematic combination of measures to rewrite the game rules: 70% EU local content, 2/3 of electric vehicles (EVs) must use EU-made batteries, foreign ownership capped at 49%, mandatory technology transfer, and 1% of revenue invested in local R&D...

The underlying message of these clauses is clear and stark: The EU is copying China's former 'market-for-technology' playbook and turning it against Chinese automakers.

The window for the traditional approach of 'export first, localize later' may close in less than 18 months.

Whether you are an executive responsible for overseas expansion at an OEM, a strategic department at a battery company, a parts supplier, or an investor following industry trends—every clause in this act will directly determine how you survive in the European market over the next five years.

Therefore, Vehicle has interpreted and dissected the 20,000-word EU Industrial Accelerator Act document, hoping to provide insights into its impact on China's auto industry going global and possible response strategies for Chinese automakers.

I. Basic Background of the Act

On March 4, 2026, the European Commission officially released the Industrial Accelerator Act (IAA) proposal, document number COM(2026)100. This is the core legislative tool of the EU's 'Clean Industrial Deal,' following the Critical Raw Materials Act and the Net-Zero Industry Act. It is expected to complete the legislative process and take effect between mid-2027 and the end of 2027.

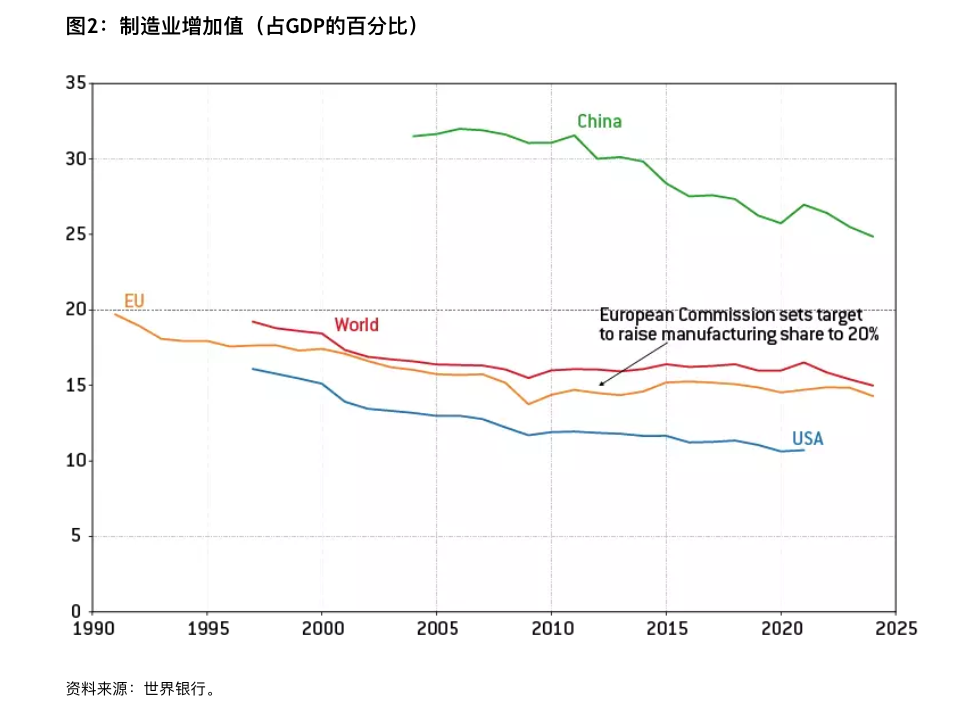

The core strategic goal of the EU in formulating this act is to increase the share of manufacturing in GDP from 14.3% in 2024 to 20% by 2035 and to retain and create about 150,000 jobs in key industrial sectors.

On the surface, this act sets rules to address the following 'three major issues':

Insufficient demand for low-carbon industrial products in Europe

Vulnerable supply chains in strategic industries and net-zero technologies

Failure to deploy industrial decarbonization technologies at scale

To put it bluntly, the underlying message of this act is that the EU realizes it is falling behind China in clean technologies such as EVs, batteries, and photovoltaics and has decided to fight back with a combination of 'industrial policy + market access.'

II. Five Pillars of the Act (with relevance to the automotive industry annotated)

The act may impose the following five pillars and constraints on raw materials and components in the automotive industry.

Pillar 1: Low-Carbon Product Differentiation (Carbon Intensity Labels)

Mandatory carbon intensity labels for energy-intensive materials like steel, potentially extendable to cement, aluminum, and other materials in the future.

Implications for the automotive industry: Future automakers will have to disclose carbon footprints when sourcing steel and aluminum in the EU and may be required to use low-carbon versions.

Pillar 2: Creating 'Leading Markets' Through Public Procurement and Subsidies (Core clause, most impactful on the automotive industry)

This is the most damaging part of the act for the automotive industry, with procurement and subsidy requirements for publicly procured goods, including:

(a) Mandatory low-carbon material requirements

Steel, cement, and aluminum used in automotive manufacturing must meet low-carbon standards in public procurement and public support programs.

Low-carbon thresholds for steel and aluminum industries: Approximately 25%.

(b) Mandatory 'Made in EU' requirements

EVs: At least 70% EU local content (excluding batteries calculated separately) required in public procurement and public support programs.

EV batteries: Phased implementation—battery energy storage systems (BESS) must use EU-made cells within three years; starting in 2027, about two-thirds of EVs must use EU-made batteries.

Vehicle components: Key components such as motors, electric controls, and battery management systems will also be subject to 'Made in EU' requirements.

Subsidies for corporate fleets: 100% must go to 'Made in EU' products.

Government support budget for clean technology industries: At least 40% must be allocated to 'Made in EU' products.

Pillar 3: New Approval Mechanism for Foreign Direct Investment (FDI) (Most pointed at Chinese companies)

This is the part that Chinese automakers and battery companies need to be most vigilant about. The new FDI review mechanism will run parallel to the existing FDI screening regulations:

Trigger conditions (all three must be met simultaneously):

The investment is in manufacturing.

The investment amount exceeds €100 million.

The industry invested in has more than 40% of global capacity controlled by the investing country.

The third condition is almost tailored for China—in batteries, photovoltaics, EVs, and critical raw materials, China accounts for over 40% of global capacity. Law firms Dechert and think tank Bruegel have pointed out that in practice, this mechanism mainly targets Chinese investors.

Covered 'emerging strategic industries':

Battery technology and energy storage system value chains.

Solar photovoltaics.

Electric vehicles.

Extraction, processing, and recycling of critical raw materials.

This seems to target China's future top three exports.

Mandatory compliance conditions (must meet 'worker localization' + at least 3 of the remaining 6 items = total of 4 items):

To put it bluntly: These conditions are highly similar to the structure of China's 'market-for-technology' policy for foreign investment in the 1980s-90s. Multiple international law firms and media outlets (Crowell & Moring, Reuters) have directly pointed out this historical parallel.

Pillar 4: Simplified Permitting Processes

'One project, one procedure' principle.

Establishment of a single access point through the 'European Business Wallet.'

Digital e-permitting.

Benefits for Chinese companies: Approval cycles for factory construction in Europe will be significantly shortened, good news for companies already committed to localization.

Pillar 5: Industrial Acceleration Zones

Member states must designate 'industrial manufacturing acceleration zones,' somewhat similar to our concept of industrial parks.

Benefits within these zones:

Rapid permitting and tacit approval mechanisms.

Priority access to funding support.

III. Key Timeline

So, what is the implementation timeline for this act? It is phased:

The FDI review will take effect immediately, with three possible final outcomes: unconditional approval, conditional approval (with mitigation measures), and rejection/prohibition of investment.

IV. Impact on China's Auto Industry: Scenario-Based Analysis

What are the impacts on China's auto industry going global? We analyze based on different current models of Chinese auto exports:

Scenario 1: Pure Export Model (CKD/Complete Vehicle Exports)—Window Closing Rapidly

CKD is currently the quickest way to respond to trade challenges, but this group faces the greatest impact. The act's 'leading market' clauses mean:

Any vehicles supported by EU public funds (procurement, subsidies, corporate fleet incentives) must meet the '70% EU local content (excluding batteries)' requirement.

Corporate fleets account for about 60% of the EU new vehicle market and are the main beneficiaries of subsidies.

Chinese-exported complete vehicles will largely fail to meet this requirement and will be excluded from the public support system.

Combined with the EU's anti-subsidy tariffs on Chinese EVs (up to 45.3%), which took effect in 2024, the traditional approach of 'export first, localize later' is no longer sustainable.

Scenario 2: Chinese Automakers and Battery Companies with Factories in Europe—A Mirror Image of 'Market-for-Technology'

Companies like CATL (Spain, 50GWh factory to start production in 2028), CALB, EVE Energy, BYD (Hungary factory), and Chery (Spain) that have already established a presence in Europe face not 'whether to enter' but 'on what terms to enter':

Actual costs:

The 49% equity cap means losing operational control.

Must license IP and know-how to EU joint venture partners.

1% of revenue must be invested in EU local R&D.

50% of employees must be EU locals (labor costs for automakers will rise significantly—T&E reports show 125 workers per GWh of battery capacity in Europe vs. 35 in China).

At least 30% of inputs must come from the EU (forcing local supply chain construction).

Potential buffer: If the EU internally exempts 'already approved existing projects,' CATL and other already-started projects may enjoy a grace period, but new projects will almost certainly fall under the new rules.

Scenario 3: EU Public Procurement Bids—Potential Direct Exclusion

An analysis by ARC Group highlights an overlooked but critically important detail: The act explicitly states that bidders owned or controlled by companies from third countries that have not signed relevant international agreements with the EU will be excluded from EU public procurement. This means Chinese state-owned automakers and some companies deemed 'Chinese-controlled' may be barred from public tenders.

Scenario 4: Secondary Impact on Costs and Prices

According to the EU's own impact assessment:

EV complete vehicle prices will rise by 0.225% (about €69) due to low-carbon steel/aluminum requirements.

Prices will rise by an additional 2.2% (about €630) due to 'Made in EU battery' requirements.

Energy storage systems/EVs will increase consumer costs by about €2.338 billion in total.

The automotive OEM industry will lose €291 million in gross value added (GVA).

This means that even if Chinese companies achieve localization, the price competitiveness of the entire European EV market will be weakened—the EU is essentially trading consumer welfare for industrial autonomy.

V. Strategic Recommendations for China's Auto Industry Going Global

So, how should China's auto industry go global?

1. Reassess 'Export vs. Localization' Paths

The validity period for the pure export model is less than 18 months (before mid-2027). Companies already in the export phase must immediately initiate localization decisions; otherwise, once they lose access to public procurement and subsidy markets, they will only be able to compete in the private consumer market with high-priced, tariff-imposed products.

Alternatively, focus on building brand strongholds in luxury, technology, and quality segments to achieve true dimensional superiority, akin to how Mercedes-Benz, BMW, and Audi once dominated.

2. 'Joint Ventures First' Instead of 'Sole Ownership First'

The 49% equity cap is already written into the proposal. Forming substantive joint ventures with EU local automakers or battery companies is the only viable path. Notable structures to consider:

Battery/platform joint ventures with OEMs like Stellantis, Renault, and Volkswagen.

Technology joint ventures with European battery newcomers (e.g., successors to ACC, Verkor, Northvolt).

Joint production ventures with European Tier 1 suppliers (Bosch, ZF, Valeo, etc.).

The next wave of reverse joint ventures to Europe should begin, but how to handle this reverse joint venture, having enjoyed the benefits of joint ventures in the past, is an interesting topic.

3. 'Tiered Firewall' for Technology Transfer

The act requires IP and know-how licensing, but reasonably designing the scope of licensing is crucial. Consider:

Mature last-generation technologies can serve as an 'entry fee' for joint ventures.

Next-generation core technologies (e.g., solid-state batteries, new material systems) should be retained in China.

Utilize 'independently developed' exemption clauses to protect both EU partners' existing IP and China's core IP.

4. Early Localization of Supply Chains

The 30% local input requirement means bringing Chinese upstream supply chain partners along:

Cathode material, anode material, electrolyte, and separator suppliers need to establish a presence in Europe simultaneously.

Prioritize member states with designated industrial acceleration zones (Hungary, Spain, Poland, Czech Republic, etc.).

Leverage these zones to access 'package deals' for land, permits, and subsidies.

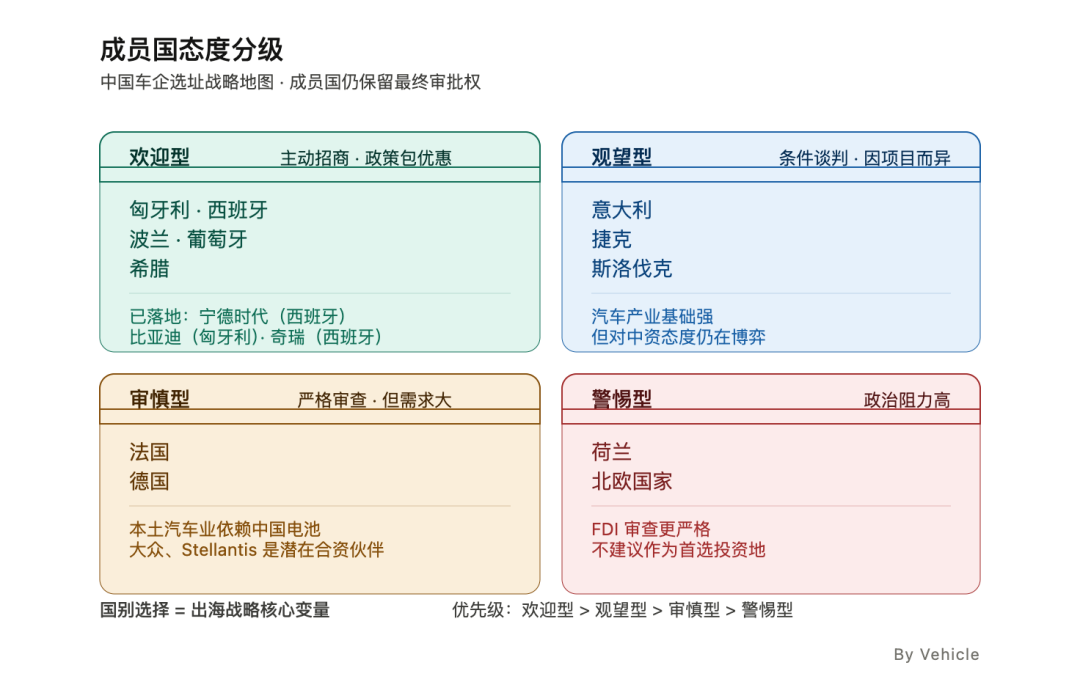

5. Explore Differentiated Opportunities Among Member States

Although the EU is unified, attitudes toward Chinese investment vary significantly among member states:

Welcoming: Hungary, Spain, Poland, Portugal, Greece.

Cautious: Italy, Czech Republic, Slovakia.

Prudent: France, Germany (despite Germany's automotive industry relying on China).

Wary: Netherlands, Nordic countries.

Meanwhile, member states still retain the final approval authority and the power to designate industrial acceleration zones. Therefore, we believe that country selection will become a core variable in the overseas expansion strategy.

6. Leveraging Reverse Game Theory Space

Our relevant institutions formally submitted consultations to the EU in April 2026, accusing it of violating WTO principles. The final provisions of the bill may still be softened during legislative negotiations:

Internal Divisions: Member states have differing views on the definition and intensity of 'Made in the EU.'

Industry Opposition: The European Automobile Manufacturers Association (ACEA) is concerned that battery localization will render entire vehicles uncompetitive.

Think Tank Criticism: The Bruegel think tank has explicitly pointed out that the bill 'lacks adjustment incentives' and 'may undermine competitiveness.'

Chinese companies can respond by: making investment commitments in exchange for transitional arrangements, forming a united front with EU domestic clients (such as Volkswagen and Stellantis), and participating in legislative consultations through European industrial alliances and industry associations.

VI. Conclusion: From 'Price Dividends' to 'Rule-Based Game Theory'

The Industrial Acceleration Act marks a new stage in Sino-European automotive industry relations. Over the past decade, Chinese automakers have relied on the triangular advantage of 'cost + technology + scale' to secure entry into the European market. However, the IAA clearly conveys three signals:

The EU is no longer exchanging market access for prices but for industrial capabilities; localization is no longer an option but an obligation; and the conditions for localization are set unilaterally by the EU.

A Historical Mirror Image Reversal: The conditions China once imposed on foreign investors—'exchanging market access for technology'—are now being copied by the EU in legal form.

For the Chinese automotive industry, success or failure in the next three to five years will not depend on how quickly or cheaply vehicles are produced but on whether it can reconstruct its overseas expansion model within the framework of EU rules and whether it can transform the 'costs' of localization into 'assets' for long-term market access.

If any companies still fantasy (fantasy/hold fantasy of) 'policy Warm up (warming)' or pin their hopes on 'high tariffs being unsustainable,' they may miss the final window of opportunity in this round of global automotive industry chain restructuring.

Primary Sources: Official proposal documents from the European Commission (COM(2026)100, SWD(2026)71, SWD(2026)72), Factsheet, analysis reports from Dechert LLP, Gleiss Lutz, Crowell & Moring LLP, Skadden LLP, policy briefs from the Bruegel think tank, S&P Global Mobility, Reuters, German Marshall Fund, etc.

*Reproduction or excerpting without permission is strictly prohibited-

-

![]()

Inside Look at 'RedSkill': Is Xiaohongshu Emerging as the Premier AI App Store?

-

![]()

The Ultimate Showdown in Handheld Smart Imaging: DJI's Ecosystem Moat and Insta360's Risk of Falling Behind

-

![]()

Organizational Groundwork in the AI Age: Time for Enterprises to Reassess DingTalk, Feishu, and WeCom

-

![]()

Ningde Is Being ‘Urged’ by Automakers to Invest in DeepSeek

-

![]()

In-Depth Analysis of the EU's Industrial Accelerator Act: Rewriting the 'Game Rules' for China's Auto Industry Going Global

-

![]()

The Pivotal Gamble of Li Auto L9: Is It Merely a Car or a Futuristic Robot?

-

![]()

What are the ways AI Coding is reshaping the software industry?

-

![]()

What Are the Technical Differences Between XPENG and Tesla in Pure Vision Intelligent Driving?