Ideal's Q1 2026: From Pioneering Profitability Among New Forces to a Net Loss of 2.3 Billion as Gross Margin Plummets

06/01 2026

06/01 2026

509

509

Li Auto, which once stood as the first new automotive force to achieve profitability and set a benchmark for others, has now reported a loss in its Q1 2026 financial results. It appears that in China's fiercely competitive automotive market, even seemingly invincible players can face setbacks swiftly.

The gross margin has been slashed in half, resulting in a net loss of 2.3 billion, and the operating cash flow has taken a sharp turn for the worse. The figures for this quarter are so grim that many are left wondering, "What's gone wrong with Li Auto?"

So, is Li Auto truly being overwhelmed by the competition? Or is there a grand strategy at play behind this quarter's performance?

This article will delve deep into Li Auto's Q1 2026 financial performance, product refresh rhythm (a specialized term referring to the pace of product updates), and self-developed technology layout (strategic placement or arrangement of technological advancements), to explore whether this 'King of Family Cars' is proactively biding its time or facing other challenges.

H1 Financial Performance

Let's dissect Li Auto's latest official financial report for Q1 2026:

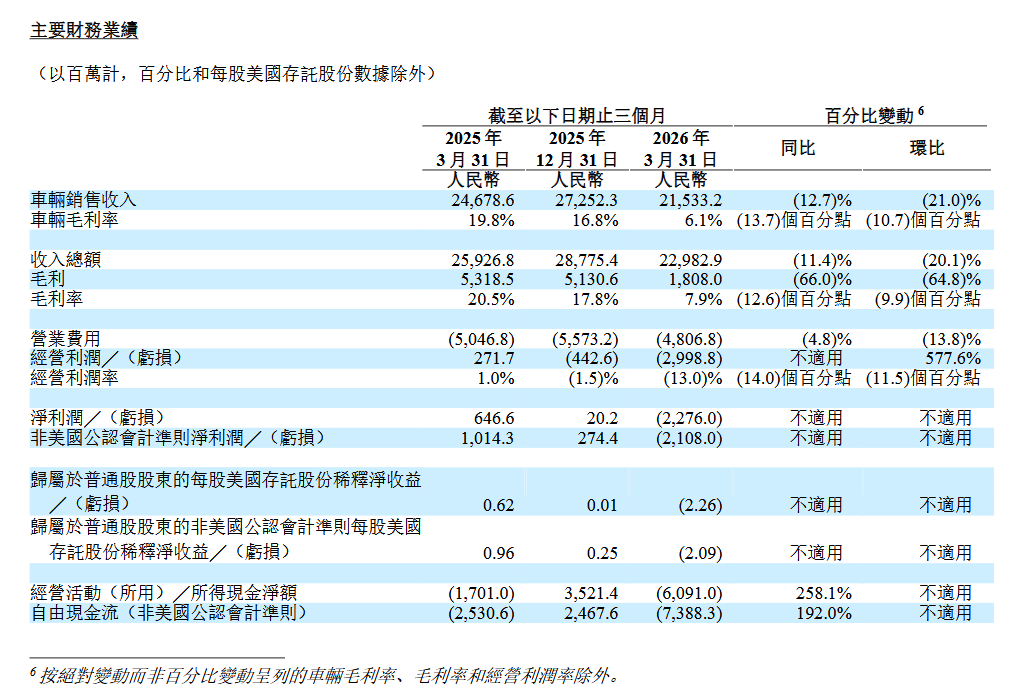

Deliveries: First, let's correct a common misconception—Li Auto delivered 95,142 vehicles in Q1, marking a year-on-year increase of 2.5%, not a decline. However, this figure is lower than the 109,000 vehicles delivered in Q4 last year, primarily due to seasonal factors during the Spring Festival lull.

Li Xiang stated during the earnings call that from January to April, Li Auto has reclaimed its position as the top-selling Chinese brand in the new energy vehicle market for vehicles priced above 200,000 yuan. Thus, in terms of sales volume, Li Auto's core market remains robust.

Total Revenue: 23 billion yuan, down 11.4% year-on-year and 20.1% quarter-on-quarter. Vehicle sales revenue was 21.5 billion yuan, a 12.7% year-on-year decrease. Here's an interesting twist—sales volume actually increased by 2.5% year-on-year, yet revenue fell by 11.4%. The discrepancy lies in the average selling price: the product mix has shifted, with a higher proportion of lower-priced vehicles dragging down the average price per unit. This reflects the broader challenges in the Chinese automotive environment, as discussed in our previous article, 'April 2026 Chinese Auto Market Realities: Sales Dip 2.5%, Exports Surge 74%, Profit Margins Fall Below 3.5%'—everyone is grappling with difficulties, not just Li Auto.

Gross Margin &

Gross Margin: This is the most alarming aspect of the financial report. Gross profit was only 1.8 billion yuan, a staggering 66% year-on-year plunge. The gross margin for vehicle sales dropped to 6.1%, compared to 19.8% in the same period last year and 16.8% in the previous quarter. The overall gross margin was 7.9%, down from 20.5% year-on-year, effectively being halved.

What caused the gross margin to collapse like this?

CFO Li Tie explained candidly during the earnings call: the proportion of pure electric i6 deliveries has surged (i6 monthly sales are steady at 20,000 units, ranking among the top three pure electric SUVs, but its gross margin is low), old L series models are being cleared from inventory, coupled with raw material price fluctuations and product refresh cycles. Essentially, high-margin older models are being phased out while low-margin new models are ramping up sales. It's as if automakers are adhering to the instant noodle adage of 'more quantity, same price.'

R&D and Expenses: R&D expenditure was 2.7 billion yuan, up 8.3% year-on-year. The key takeaway is that in a quarter when gross margins collapsed, Li Auto not only didn't cut R&D but increased it. After all, in the era of AI explosion, failing to invest in cloud computing power spells no future. Operating expenses totaled 4.8 billion yuan, down 4.8% year-on-year, with savings coming from personnel costs.

Losses: Operating loss was 3 billion yuan (compared to an operating profit of 270 million yuan in the same period last year), with an operating profit margin of -13%. Net loss was 2.3 billion yuan. This is a new force that was once the first to turn profitable, yet it's now reporting a net loss.

Cash Flow and Financial Strength: Operating cash flow was -6.1 billion yuan, and free cash flow was -7.4 billion yuan, both turning sharply negative. However, Li Auto's financial strength is truly remarkable—cash reserves at the end of the quarter were 90.43 billion yuan. With over 90 billion yuan in hand, Li Auto is still repurchasing shares. The 1 billion USD share repurchase plan announced in March had seen the purchase of approximately 16.4 million Class A shares for about 140 million USD as of May 26. Repurchasing shares while incurring losses can be seen as a positive signal of management's confidence in their position, or conversely, as neglecting investor returns.

Li Auto's Big Bet

All of Li Auto's difficulties this quarter seem to be paving the way for one thing—the launch of the new generation L series and the debut of its self-developed chip.

Li Auto aims to exchange one quarter's poor performance for a ticket to a new era.

New L9: Launched on May 15 and started deliveries on May 17, with a tight schedule. Two versions are available: the top-spec Livis version priced at 509,800 yuan and the Ultra version at 459,800 yuan. Orders exceeded 10,000 units within two weeks of launch, with an average transaction price exceeding 500,000 yuan.

Li Auto's goal for the L9 is straightforward: to capture over 20% of the market share in the new energy SUV segment priced above 500,000 yuan; starting from June, the Ultra version will be pushed to compete in the 400,000-500,000 yuan segment.

The order structure is intriguing—Li Xiang mentioned during the earnings call that the Livis version accounts for over 90% of orders, while the Ultra version accounts for less than 10%. This indicates that buyers of 500,000 yuan-plus vehicles are truly willing to pay a premium for the most advanced technology and performance. It also suggests that there is still significant room in the luxury car market above 500,000 yuan, and as long as a company's product and brand strength are sufficient, it's the best area to break free from the competitive red ocean.

Following closely, the new L8 will be launched at the end of June, positioned as a flagship five-seater SUV. Li Xiang confidently stated that the new L8 is not just a 'downsized' version of the L9 but a complete redesign, potentially 'the best-handling large SUV globally.' The L8 and L9 share the same technology platform and the same 72.7-degree 5C large battery, both produced at the Chengdu base, with flexible allocation between the two production lines.

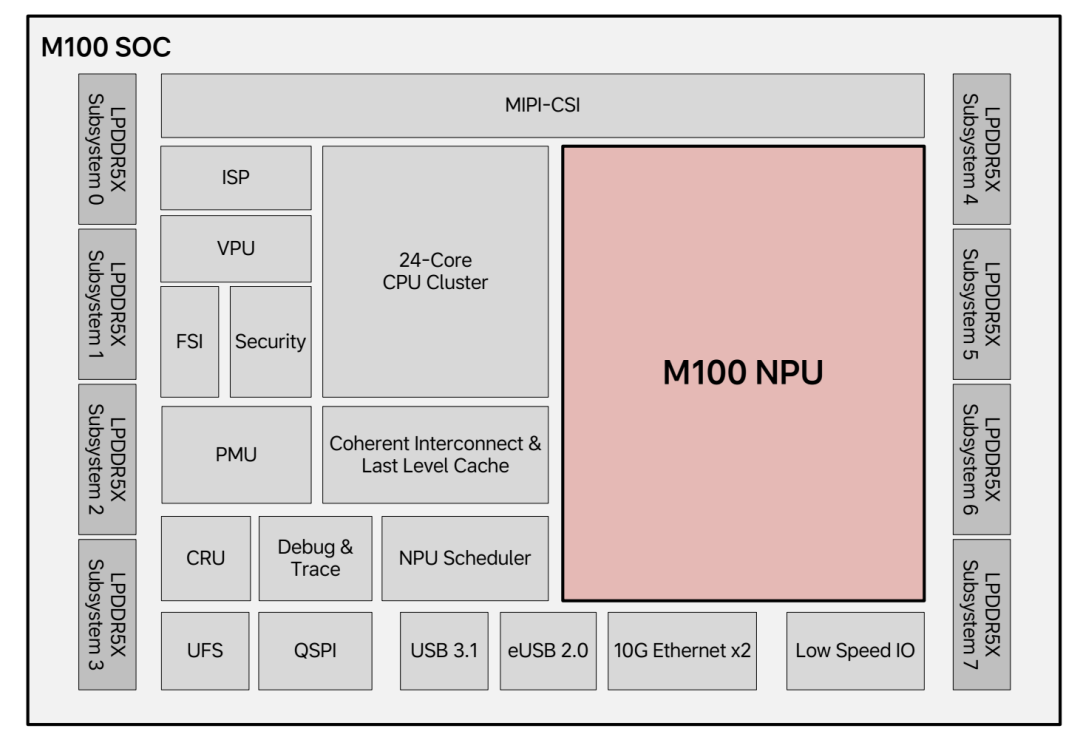

Self-Developed Mach M100 Chip: Li Auto's intended game-changer. The new L9 is the debut model for the M100 chip. Li Auto claims to be the first company in China to achieve full functionality on a brand-new chip from its first installation, a statement that might make executives at Xpeng and NIO raise an eyebrow and wonder, 'Who are they referring to?'

The M100 is an automotive-grade AI inference chip using a 5nm process and an AI-native dynamic dataflow architecture. Li Auto states that through integrated hardware and software design, the M100 achieves three times the effective computing power per unit cost compared to the previous generation. More crucially, the M100 enables Li Auto to run the new MindVLA large model—whose parameters are ten times those of the previous generation.

CTO Xie Yan made a bold statement during the earnings call: Li Auto aims to match Tesla's FSD V14 level in the U.S. with its autonomous driving system by the second half of this year. This statement echoes last year's bet by Xpeng's autonomous driving head Liu Xianming, who vowed to 'strip naked in Zhongguancun' if they failed. Is Li Xiang now betting on Zhan Kun doing the same?

Li Xiang also shared an insightful observation: in the past, information flowed too freely in the industry because everyone used NVIDIA chips, and hiring a few people could bring performance close to parity. But now, with Li Auto's full-stack self-development and vertical integration from chips to large models, 'hiring to catch up' no longer works. He calls this Li Auto's future 'systematic moat.' He particularly emphasized the variable of time—it took Li Auto four years from project inception to chip mass production, and this time difference itself is a barrier.

You have to admit, that's a well-articulated point.

Horizontal Comparison: Where Does Li Auto Stand?

Let's compare Li Auto's current quarter with NIO, a former peer.

NIO's Q1 vehicle gross margin was 18.8%, and its non-GAAP operating profit turned positive for the first time.

Li Auto's gross margin for this quarter dropped to 6.1%, with an operating loss of 3 billion yuan.

One company relies on launching flagship models like the ES9/ET9, using battery swapping as a covert strategy to lower prices, and building a moat with community services and clubs.

The other, Li Auto, with its L series extended-range brand being challenged by various competitors, took a risky move by developing the I series pure electric models to break free from the red ocean and is now returning to the L series to build its moat. The two companies are taking completely different paths.

Now, let's look at traditional giants—Volkswagen's operating profit margin for Q1 2026 was 3.3%, Toyota's for FY2026 was 7.4% (a three-year consecutive decline), while BYD maintains a stable gross margin of 17%-18%.

Li Auto's 6.1% vehicle gross margin for this quarter indeed falls short compared to both its peers and outsiders.

Li Auto attributes this to 'one-time growing pains during a transition period,' not a 'problem with the business model.'

CFO Li Tie provided crucial guidance—as the new L9's market launch and deliveries bring about economies of scale, coupled with product mix optimization, profitability will gradually recover. In other words, 6.1% is the bottom at this special juncture, not the new norm. The Q2 guidance is for deliveries of 95,000-100,000 units and revenue of 24.1-25.4 billion yuan, aiming to reassure the market.

In Closing

Li Auto's Q1 2026 results present unsightly numbers on the surface: gross margin halved, net loss of 2.3 billion, and sharply negative cash flow.

However, the earnings call conveyed Li Auto's unflappable confidence: 90 billion yuan in cash reserves, over 10,000 orders for the new L9 within two weeks, the debut of its self-developed chip, and a year-on-year increase in sales volume, with the annual growth target of 20% firmly held.

One can only say that Li Auto is making a significant gamble this time. Whether the new L8 can carry on the momentum of the L9, whether the I series pure electric models can increase sales volume while improving gross margins, and whether the M100 chip can truly bring autonomous driving to parity with FSD—every question mark remains hanging.

Li Xiang revealed during the earnings call that Li Auto plans to host a separate event in June focusing on software and AI, providing an in-depth explanation of the in-cabin interaction, foundational models, autonomous driving systems, intelligent agents (Agent), and the real-world experience of the Mach 100 chip.

This is worth anticipating. After all, from both sales volume and product strategy perspectives, Li Auto doesn't appear to have a significant moat at present. Follow Vehicle, and we'll analyze whether Li Auto still has a moat when the time comes.

Primary sources: Li Auto's Q1 2026 earnings call and financial report information.

*Unauthorized reproduction or excerpting is strictly prohibited-

-

![]()

Why Did the Former Chairman of Ferrari Get 'Angry' About Its First All-Electric Model, Luce?

-

Exclusive! Gas Leak at SK Hynix’s Cheongju Facility in South Korea Leaves 6 Injured—Could DDR5 Prices Surge Once More?

-

![]()

Leading the Charge in Ensuring Intelligent Driving Safety: Can BYD Outshine Huawei?

-

![]()

Li Auto (1Q26 Highlights): Maintains 20%+ Sales Growth Target for 2026

-

![]()

Ideal: Wanting Too Much Leaves Only 'Daydreams'?

-

![]()

Entering the Japanese Market Requires Learning 'Magic'

-

FTTH installation and maintenance engineer, how many instruments do you carry when you go out?

-

![]()

Is Waymo's Self-Driving Car 'Made in China'? When U.S. Robotaxi Leader Teams Up with Zeekr's 'Baby Bus', a Multi-Billion-Dollar Cross-Border Alliance Emerges