Li Auto (1Q26 Highlights): Maintains 20%+ Sales Growth Target for 2026

06/01 2026

06/01 2026

449

449

Below is a summary of Li Auto's 1Q26 earnings call, compiled by Dolphin Research. For the earnings report analysis, please refer to "Li Auto: Wanting Too Much Leaves Only 'Daydreams'?"

I. Review of Key Financial Information

1. Shareholder Returns: The company announced a USD 1 billion share repurchase program in March. To date, it has repurchased a cumulative total of 17.5 million Class A ordinary shares (including 7.3 million ADSs) at a total consideration of USD 148.1 million.

2. Business Guidance: Deliveries for 2Q26 are expected to range from 95,000 to 100,000 units, with quarterly total revenue projected between RMB 24.1 billion and RMB 25.4 billion. The company maintains its full-year sales growth target of 20%.

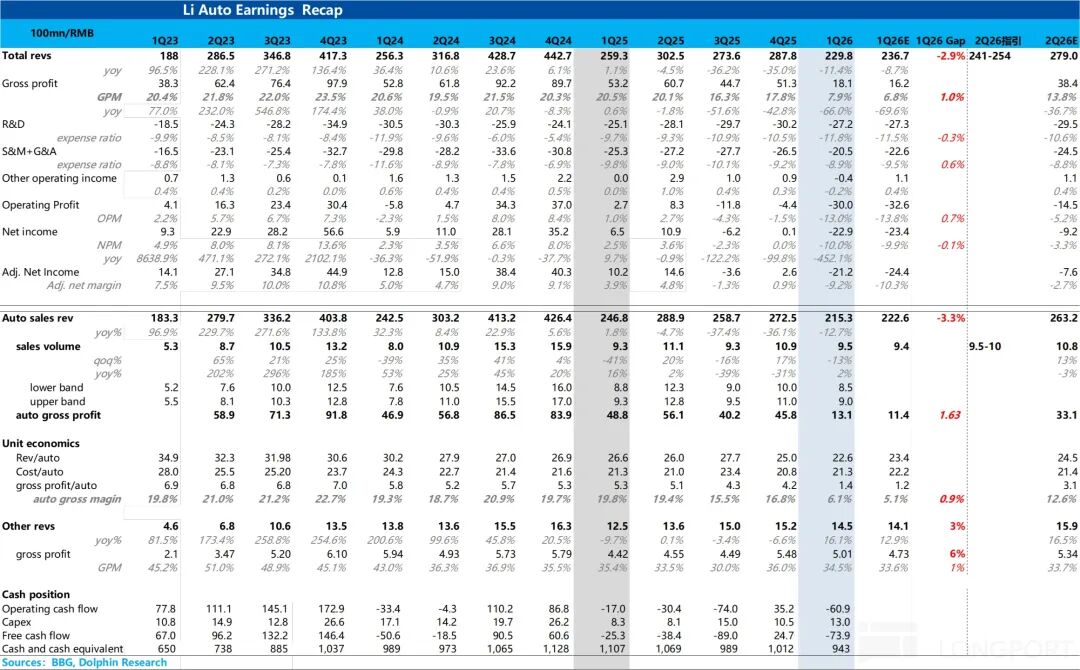

3. Changes in Key Financial Metrics: 1Q26 total revenue was RMB 23 billion, down 11.4% YoY and 20.1% QoQ. Gross margin was 7.9%, significantly lower than 20.5% YoY and 17.8% QoQ. Vehicle gross margin was only 6.1% (19.8% YoY, 16.8% QoQ). Operating loss was RMB 3 billion (operating profit of RMB 270 million YoY), net loss was RMB 2.3 billion (net profit of RMB 650 million YoY), and free cash flow was -RMB 7.4 billion. The ending cash balance was RMB 94.3 billion, with a robust balance sheet.

4. Path to Profitability Recovery: The CFO explicitly stated that with the delivery of the new L9, gross margin is expected to recover to approximately 10% in 2Q26. For the full year, as the L series refresh is completed and product mix optimizes, gross margin will continue to improve.

II. Detailed Content of the Earnings Call

2.1 Core Information from Executive Statements

1. Sales and Product Line Progress

a. 1Q26 deliveries entered a growth trajectory. From January to April 2026, Li Auto regained the top sales position among Chinese brands in China's new energy vehicle market for vehicles priced above RMB 200,000. Monthly sales of the pure electric Li i6 stabilized at 20,000 units, ranking among the top three in all pure electric SUVs.

b. The all-new Li Auto L9 was officially launched on May 15, with deliveries commencing on May 17. The new L9 is available in two configurations: Livis and Ultra, priced at RMB 509,800 and RMB 459,800, respectively. Within just two weeks of launch, the L9 Livis secured over 10,000 orders, all at transaction prices above RMB 500,000. The company expects to maintain over 20% market share in the NEV SUV market for vehicles priced above RMB 500,000.

c. Starting in June, the focus will shift to promoting the Ultra version, aiming to capture 20% market share in the RMB 400,000 to RMB 500,000 NEV SUV segment. The new L9 marks the beginning of the L series refresh sequence—a new L8 will also be launched in late June, positioned as a 5-seater flagship SUV, forming a product matrix with the L9 as a 6-seater flagship and the L8 as a 5-seater flagship, rather than a downgraded version of the L9.

d. The new L8 shares the same technology platform as the L9, featuring the same 1.5L turbo range-extender system and a 72.7 kWh 5C high-capacity battery. Overall vehicle dimensions and wheelbase have increased compared to the previous generation, significantly improving interior space. Dual-tone body colors and electric side steps are available as options.

e. The new L8 completed its declaration with the MIIT in April 2026, with a launch event planned for June.

2. Breakthroughs in Self-Developed Chips and Intelligent Technologies (MAHE M100 & MindVLA)

a. The new L9 achieves full-stack mass production deployment of the self-developed MAHE M100 chip and MindVLA large model, making Li Auto the first domestic company to implement full functionality upon initial chip integration—a significant milestone for the company.

b. The MAHE M100 is a 5nm automotive-grade AI inference chip featuring an AI-native dynamic dataflow architecture and integrated hardware-software design. Its effective computing power per unit cost is three times that of the previous platform. At the same cost, it delivers six times the effective computing power improvement, with input frame rates increased by threefold and inference frame rates seeing even greater enhancements.

c. The MindVLA model's parameter count has increased tenfold compared to the previous version. Its integration with the MAHE M100 will bring a leap forward in autonomous driving performance.

d. Compared to ADAS 8.0, the M100-equipped ADAS 9.0 version exhibits more human-like decision-making in complex scenarios, with smoother and more comfortable longitudinal and lateral control. Next steps include further expanding input data scale and precision (higher frame rates), enhancing the model's ability to understand short-term causal relationships, optimizing execution layer latency through a self-developed operating system, and achieving more precise motion control with a full-wire control chassis.

e. The company aims to match Tesla FSD v14's performance in the U.S. market by the second half of this year.

f. The company plans to host a dedicated launch event in June to comprehensively showcase its software and AI capabilities, including cabin interaction, foundational large models, autonomous driving, system agents, and the complete MAHE chip experience—requiring a dedicated 2- to 3-hour session to fully present.

3. Channel Reform: Store Partner Program

a. The Store Partner Program grants store managers true decision-making authority and profit-sharing rights, transforming store management from mere "executors" into genuine "operators" capable of independently evaluating ROI for various business activities and focusing on operational efficiency.

b. The stability and long-term commitment of the core management team have significantly improved. Store management has shifted from pursuing short-term sales targets to cultivating local user communities, building reputation, and enhancing long-term competitiveness.

c. 1Q26, a traditional off-season for the automotive industry and an early stage of the partner program's rollout, saw all stores meet monthly sales targets while successfully clearing inventory of the previous L series and significantly boosting customer satisfaction.

4. Overseas Market Expansion

a. The company adopts a phased internationalization strategy, flexibly choosing modes such as establishing local subsidiaries, partnering with local distributors, or using exclusive local agents based on local market size, industry landscape, and competition. Priority is given to collaborating with leading local enterprises to rapidly establish an integrated service system for sales, delivery, and after-sales.

b. During the Beijing Auto Show, overseas media, users, and partners showed significantly increased interest in the Li Auto brand. The company has officially signed agreements with dealers in Saudi Arabia and the UAE, planning to enter the Middle East and Central Asian markets in 3Q26 with the L series range-extender product line. The first product will be a customized overseas version of the new Li L9, optimized for local conditions (charging infrastructure, UI, software ecosystem, thermal management, etc.).

c. Starting from May 2026, the company will gradually enter markets including Macau, Cambodia, Laos, and Myanmar, continuing to cultivate Southeast Asia.

d. In the second half of this year, the fully electric Li i6 will be introduced to the European market. Additionally, a right-hand-drive version of the Li MEGA is planned for launch in right-hand-drive Asia-Pacific markets such as Hong Kong and Singapore by the end of this year.

e. All new models incorporate overseas regulatory compliance design from early development stages to support the ongoing globalization strategy.

5. Humanoid Robot Strategy

a. In the long term, humanoid robots will be needed in factories, stores, and user households, serving as standardized labor. Robots will not be limited to specific types of enterprises—any company requiring human labor will eventually use robots, with the only difference being whether they are purchased externally or self-developed.

b. It will take more than three years for humanoid robots to achieve comprehensive large-scale commercial deployment similar to that of new energy vehicles between 2010 and 2015. Currently, technical pathways in multiple specific directions have not yet converged, and numerous challenging problems remain to be solved.

2.2 Q&A Session

Q (Tim Hsiao, Morgan Stanley): What is the current order status for the Li L9? The waiting period for the Livis version has extended to 9-11 weeks. What is the company's production capacity arrangement? What is the expected sales proportion of the L9 in the second quarter's delivery guidance?

A: The order structure is very clear, with the Livis version accounting for over 90% of all orders and the Ultra version less than 10%. This fully reflects consumers' recognition of our latest advanced technologies and their willingness to pay for functionality and performance. It also demonstrates our solid position in the RMB 500,000+ segment, serving as a very positive signal for the brand. Subsequently, we will strengthen promotion of the Ultra version to continuously optimize the order structure.

In terms of production capacity, both the new L9 and L8 will be manufactured at the Changzhou base, with flexible allocation between production lines. May and June represent the production ramp-up period, with monthly capacity ranging from 4,000 to 5,000 units. Currently, the Livis dual-tone body color has certain limitations, and there are slight supply constraints for some exclusive components. We are working day and night with core suppliers to expand supply and ensure deliveries as soon as possible. Meanwhile, the Ultra version has ample production capacity, allowing flexible adjustments based on market demand.

For L9 deliveries in the second quarter, considering the production ramp-up pace, we expect to deliver approximately 8,000 units from mid-May to late June. After fully ramping up production in the third quarter, we are confident that the delivery scale of the new L9 will surpass that of the previous generation L9.

Q (Tim Hsiao, Morgan Stanley): What is the profit outlook for the second quarter? When will a significant profit inflection point occur throughout the year? Can profitability be achieved this year amid rising raw material costs? With the Li i6 accounting for approximately 60% of total sales, what is the lower limit for overall gross margin? What are the gross margin targets for new models like the L9?

A (CFO Tie Li): First-quarter gross margin was suppressed by multiple factors: first, the L series refresh cycle required gradual product iteration starting with the L9; second, the i6 accounted for a relatively high proportion of total sales; third, the purchase tax subsidy policy for the i6 had an impact. However, with the launch and delivery of the new L9, we expect gross margin to recover to approximately 10% in the second quarter. Looking ahead to the full year, as the L series refresh is completed and the product mix optimizes, gross margin will continue to improve.

Our top priority this year is to successfully complete the comprehensive refresh of the Li L series. We are delighted to see that the L9 Livis has gained strong market recognition for its flagship technological prowess, solidifying its share in the RMB 500,000+ price segment. The L9 Livis's successful establishment in this price range represents a further breakthrough beyond the previous generation L9. This year, the new L series and the BEV product line, including upcoming models, will extensively incorporate self-developed technologies, laying a solid foundation for our development over the next two years.

Q (Feixiang Gao, CITIC Securities): What are the specific achievements of the MAHE M100 chip and MindVLA large model in terms of vehicle performance, user feedback, intelligent differentiation highlights, and actual cost reductions? What is the next development direction for the company's autonomous driving system?

A (CTO Yan Xie): Compared to our ADAS 8.0 version, the 9.0 version based on the self-developed MAHE M100 chip shows significant improvements, primarily in more human-like decision-making in complex scenarios and smoother longitudinal and lateral control, resulting in a more comfortable overall driving experience. 9.0 represents our first autonomous driving version running on a self-developed chip, already achieving top-tier performance in a highly competitive market—but this is merely the starting point.

The new platform enables sensors to collect data with higher precision and frame rates, while the M100's powerful computing power allows us to run larger and better algorithms, enabling synchronous improvements across data, computing power, and algorithms. This will drive even more rapid advancements in autonomous driving capabilities.

The next steps for autonomous driving involve three directions: first, further expanding input data scale and precision models to allow neural networks to receive more driving semantic information from sensors, enabling the model to "see" more signals; second, enhancing the model's cognitive abilities, particularly its ability to learn short-term causal relationships, allowing it to make human-like judgments in more complex urban traffic scenarios beyond simple behavioral fitting; third, significantly improving execution layer precision and response speed through computing power latency optimization via a self-developed operating system and a full-wire control chassis, making the autonomous driving system feel safer.

In terms of costs, due to the integrated hardware-software design, the self-developed M100 chip delivers six times the effective computing power of the previous platform at the same cost, with input frame rates increased threefold and even greater improvements in inference frame rates. Our goal is to match Tesla FSD v14's performance in the U.S. market by the second half of this year. The high-performance AI inference system built around the M100 provides a solid foundation for achieving this target.

Q (Feixiang Gao, CITIC Securities): Since the implementation of the Store Partner Program, what specific changes have occurred in key metrics such as sales per square meter, average monthly store sales, salesperson efficiency, and expense ratios at pilot stores compared to before the reform? Has the program's impact on sales met expectations so far? How does the company quantitatively assess the program's effect on boosting sales in the third quarter and beyond?

A (CEO Xiang Li): Since implementing the Store Partner Program, granting store managers true decision-making authority and profit-sharing rights has fully unlocked the potential of our frontline sales teams. First, a fundamental mindset shift has occurred at the store manager level—they have transformed from mere "executors" into genuine "operators" capable of independently evaluating the ROI of various business activities and focusing on operational efficiency.

Simultaneously, the stability and long-term commitment of the core management team have significantly improved. Store management has shifted its focus from chasing short-term sales targets to cultivating local user communities, building reputation, and enhancing the store's long-term competitiveness.

From a timing perspective, 1Q26 represented both a traditional off-season for the automotive industry and an early stage of the partner program's rollout. On average, our stores met monthly sales targets while successfully clearing inventory of the previous L series and significantly boosting customer satisfaction. Looking ahead, as store managers accumulate more operational experience and leverage our training and support systems, we believe store operational efficiency and capabilities will continue to rise.

Q (Tina Hou, Goldman Sachs): What information can be disclosed about the all-new Li Auto L8 at present?

A (CEO Xiang Li): As the product lineup of the L series gradually improves, the L9 will be positioned as the flagship 6-seater version, while the all-new L8 will be positioned as the flagship 5-seater version. The two models complement each other and jointly consolidate our market share in the high-end flagship segment.

The all-new L8 has completed its declaration with the Ministry of Industry and Information Technology in April 2026 and is planned for an official launch in June. Compared to the previous generation, the overall dimensions and wheelbase of the new vehicle have increased, significantly improving the rear passenger space and overall riding experience in the 5-seater layout. In terms of the powertrain, the all-new L8 is also equipped with our self-developed 1.5L turbo range-extender system and a 72.7 kWh 5C high-capacity battery, identical to the L9. Both models share the same technology platform, delivering excellent energy efficiency and range performance. Additionally, the L8 will offer optional features such as a two-tone body and electric side steps. For more details, please stay tuned for the launch event in June.

Q (Tina Hou, Goldman Sachs): How does management view the current competitive landscape and investment trends in the AI industry? What is your judgment on the industry competition?

A (CEO Xiang Li): We believe that the competition for mid-to-high-end smart vehicles over the next 3 to 5 years will essentially be a competition of embodied AI. The deep integration of self-developed chips and large foundational models will be the highest technical barrier and core determinant of the company's long-term success and competitiveness.

Taking our experience with self-developed chips as an example: In the past, since everyone used NVIDIA chips, technology and information flowed freely within the industry. Competitors could easily poach and train talent, quickly catching up to us in performance despite our continuous innovation. However, with self-developed chips, larger-scale computing power, and larger-scale models, we adopted a completely different architecture, achieving vertical integration of hardware and software. This rendered the past approach of "poaching to catch up" entirely ineffective, as it cannot be replicated without deep hardware-software synergy.

Therefore, we will transform our systemic capabilities into a core competitive moat, ensuring that our capabilities and outputs can no longer be easily replicated by others. Another key factor is time—it took us 4 years from project initiation to the mass production and integration of self-developed chips. Over the next decade, while maintaining our technological innovation advantage, we will also ensure that our technical barriers remain sufficiently advanced, forming a long-term competitive edge in terms of time.

Q (Jing Chang, CICC): Li Xiang mentioned that a more detailed smart technology launch event will be held in June. What are the latest strategic developments in the company's humanoid robot plans?

A (CEO Xiang Li): In the long term, we clearly recognize that humanoid robots are needed in our factories, stores, and by our users. We believe robots should not be limited to startups, mid-sized companies, or large corporations—they will become standardized labor, adopted by any company willing to excel in its field, regardless of enterprise type. As long as a company needs people, it will need robots; the only difference is whether they are outsourced or self-developed.

From a timeline perspective, it will still take more than 3 years for humanoid robots to achieve full-scale development, deployment, and commercialization—similar to the stage electric vehicles went through between 2010 and 2015. This is because, in each specific field, technological paths have not yet converged, and many issues remain unresolved. During this period, we still need to continuously tackle numerous hard problems.

Q (Jing Chang, CICC): Please share the latest progress in the company's overseas market strategy, including plans for 2026 and beyond, the pace of international expansion and contributions, key regions, overseas sales targets, and product pipelines.

A (CEO Xiang Li): We are firmly advancing our internationalization strategy in a phased approach, flexibly choosing between establishing local subsidiaries, partnering with local distributors, or using exclusive local agents based on local market size, industry landscape, and competitiveness. Regardless of the model, we aim to collaborate with leading local enterprises or partners to rapidly establish an integrated service system covering sales, delivery, and after-sales.

Our products and brand continue to gain global recognition. During the Beijing Auto Show, we received significant attention from overseas media, users, and partners, and formally signed contracts with distributors in Saudi Arabia and the UAE. The Middle East and Central Asian markets will primarily feature the L series range-extender product line, starting with the overseas version of the all-new Li L9, customized for local conditions. A series of hardware and software optimizations have been made for local charging infrastructure, UI, software ecosystem, and thermal management. It is planned to officially enter the Middle East and Central Asian markets in 3Q26.

Meanwhile, starting from May 2026, we will gradually enter markets such as Macau, Cambodia, Laos, and Myanmar, further deepening our presence in Southeast Asia.

In the second half of this year, we will launch the fully electric Li i6 in Europe. Additionally, for right-hand-drive markets, we will introduce the right-hand-drive version of the Li MEGA in key Asia-Pacific markets such as Hong Kong and Singapore by the end of this year. At the product level, we are implementing a precise regional customization strategy. All upcoming models have incorporated overseas regulatory compliance design at the early stages of R&D to better support our ongoing globalization strategy.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reprinting is only allowed with authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general viewing and data reference by users of Dolphin Research and its affiliated entities. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the relevant information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, solicitations, or endorsements of relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for distribution to, or use by, any person or resident in any jurisdiction where such distribution, publication, provision, or use would contradict applicable laws or regulations or result in Dolphin Research and/or its subsidiaries or affiliates being subject to any registration or licensing requirements in that jurisdiction.

This report only reflects the personal views, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated entities.

This report is produced by Dolphin Research, and all copyrights are owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to any other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Why Did the Former Chairman of Ferrari Get 'Angry' About Its First All-Electric Model, Luce?

-

Exclusive! Gas Leak at SK Hynix’s Cheongju Facility in South Korea Leaves 6 Injured—Could DDR5 Prices Surge Once More?

-

![]()

Leading the Charge in Ensuring Intelligent Driving Safety: Can BYD Outshine Huawei?

-

![]()

Li Auto (1Q26 Highlights): Maintains 20%+ Sales Growth Target for 2026

-

![]()

Ideal: Wanting Too Much Leaves Only 'Daydreams'?

-

![]()

Entering the Japanese Market Requires Learning 'Magic'

-

FTTH installation and maintenance engineer, how many instruments do you carry when you go out?

-

![]()

Is Waymo's Self-Driving Car 'Made in China'? When U.S. Robotaxi Leader Teams Up with Zeekr's 'Baby Bus', a Multi-Billion-Dollar Cross-Border Alliance Emerges