Ideal: Wanting Too Much Leaves Only 'Daydreams'?

06/01 2026

06/01 2026

521

521

Li Auto released its Q1 2026 financial report after market close in Hong Kong and before market open in the U.S. on May 28 (Beijing Time). While Li Auto had relatively adequately communicated the downward trend in Q1 vehicle sales gross margin, the Q1 results themselves were still mediocre even under the most pessimistic expectations. Moreover, the Q2 guidance reflects that Li Auto has not yet reached the stage of 'turning the corner.' Here's a detailed look:

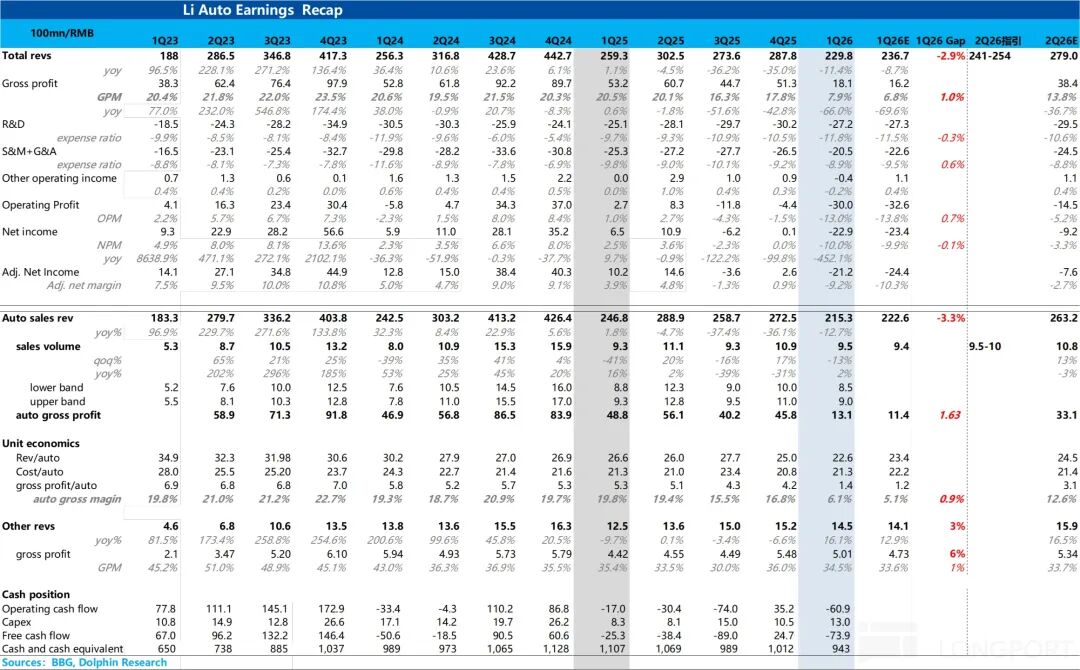

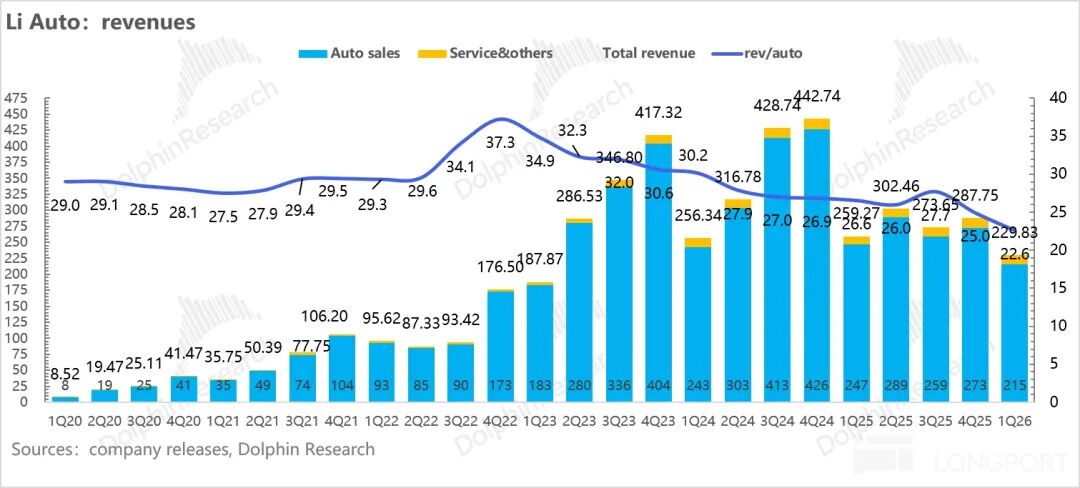

① Revenue fell slightly short of expectations, primarily due to a significant decline in ASP: In Q1, Li Auto's automotive sales revenue was RMB 21.5 billion (total revenue of approximately RMB 23 billion, down 11.4% YoY), falling short of market expectations. This was mainly because the ASP continued to decline sharply by approximately RMB 24,000 QoQ to RMB 226,000 (below market expectations of RMB 234,000).

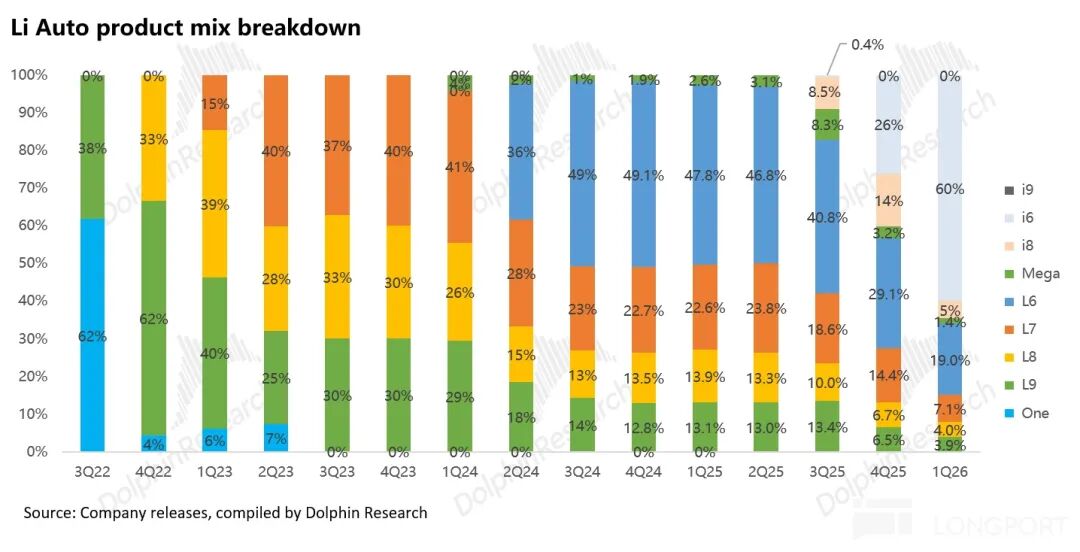

The core reasons for the significant decline in ASP are as follows: First, the model mix continued to shift significantly downward, with the lower-priced all-electric model i6 remaining a hot seller, accounting for approximately 60% of sales (a significant increase QoQ), while the higher-priced Mega's share declined to about 1.4%. Second, in the face of intense competition, Li Auto continued to increase discounts on its L-series mainstay models in Q1 (e.g., approximately RMB 36,000 off on L6, RMB 45,000 off on L7/L8, and RMB 50,000 off on L9). The combination of these two factors pulled down the overall ASP.

② Vehicle sales gross margin plummeted, but largely in line with market 'low expectations' and Li Auto's prior guidance:

The actual automotive gross margin in Q1 was 6.1%, a sharp decline of 10.7 percentage points QoQ from 16.8% in the previous quarter. Since management had already provided clear guidance of around 5% in the previous quarter's earnings call (mainly affected by purchase tax subsidy support, the rising share of the lower-priced i6, and inventory clearance of the old L-series models), the market had already anticipated this (consensus expectation was only around 5%). The actual result was only about 1 percentage point higher than the market's 'low expectations.'

The plunge in vehicle sales gross margin was primarily due to the dual pressures of declining ASP and rising costs: In Q1, the cost per vehicle increased by RMB 5,000 QoQ to RMB 213,000. Although the share of the lower-priced i6 increased, the 13% QoQ decline in sales volume weakened economies of scale, upstream storage chip and commodity raw material price increases (negatively impacting the i6's gross margin by about 3 percentage points), and the provision of approximately RMB 15,000 in purchase tax subsidy support for the i6. The combination of these three factors eroded gross profit margins, resulting in a gross profit of only RMB 14,000 per vehicle in Q1, indicating significant pressure on vehicle sales.

③ Operating profit turned from profit to loss, with sales volume leverage failure (failure to materialize) and gross margin collapse being the biggest drags:

Li Auto's operating profit in Q1 plummeted by nearly RMB 2.55 billion QoQ to -RMB 3 billion, plunging into a loss and becoming the biggest reason for the significant depletion of free cash flow in the quarter.

The core factors behind the collapse in operating profit are as follows: On the one hand, Q1 sales volume declined by 13% QoQ, preventing the effective release of sales volume leverage. On the other hand, the vehicle sales gross margin plummeted to 6.1%, severely eroding overall profitability.

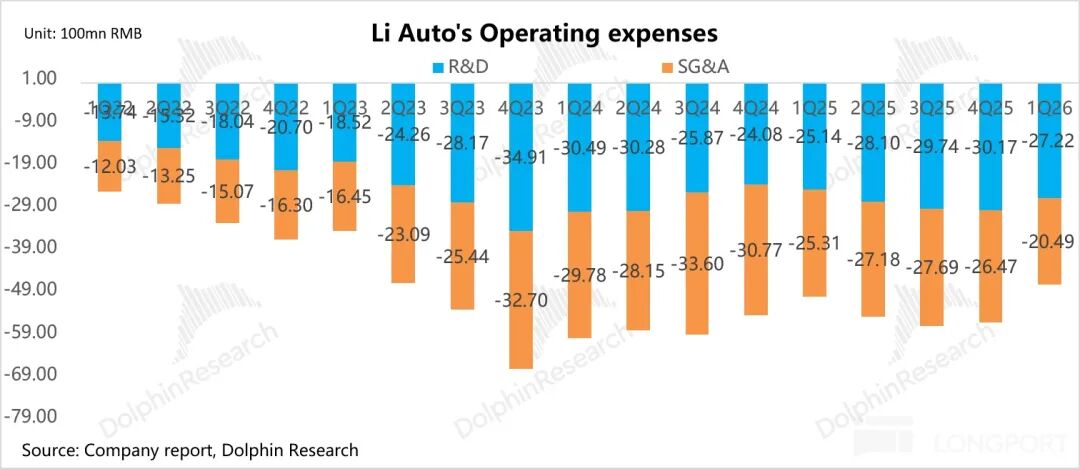

Although the company exercised restraint in operating expenses, with R&D expenses (down about RMB 300 million QoQ to RMB 2.72 billion) and selling, general, and administrative expenses (down about RMB 600 million QoQ to RMB 2.05 billion) both declining QoQ due to seasonal factors, staff reductions, and a shift in channel strategy from 'expansion to refinement,' these reductions were unable to offset the impact of revenue contraction and gross profit 'bleeding,' ultimately leading to a significant negative turn in operating profit.

Overall, although Li Auto had proactively communicated with the market about its performance, providing a 'preventive dose,' the actual data showed that the repeated collapses in ASP and vehicle sales gross margin directly led to significant 'bleeding' in operating profit and free cash flow, revealing the enormous operational pressures Li Auto faces amid 'internal and external challenges.'

As for market expectations, which are of greatest concern:

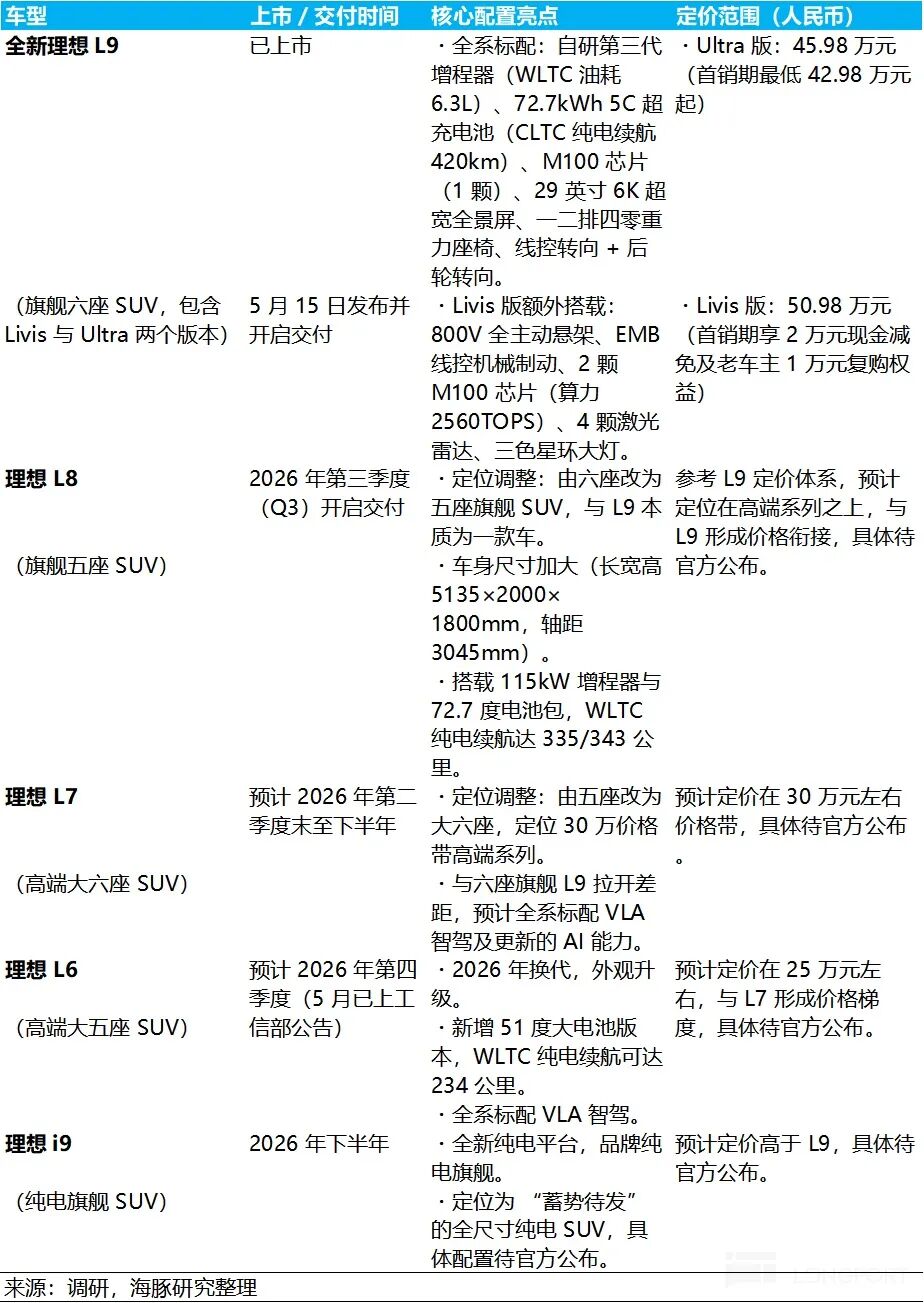

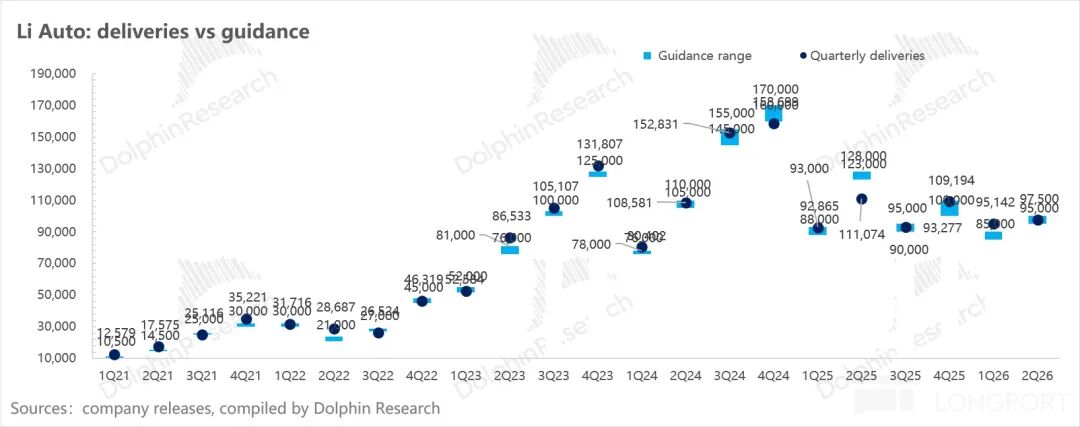

① Sales volume guidance falls short of expectations, with lackluster orders for the refreshed L9

Li Auto's Q2 sales volume guidance is 95,000-100,000 units, not only below market expectations of 108,000 units but also representing a YoY decline of 10%-14.4%. Given that 34,000 units were delivered in April, the guidance implies an average monthly sales volume of only 30,500-33,000 units in May/June—a QoQ decline compared to April.

The biggest new product catalyst in Q2—the all-new refreshed L9—officially launched and began deliveries on May 15. The signal behind this lower-than-expected and declining MoM sales volume guidance for May/June is that orders for the refreshed L9 are currently lackluster, failing to provide strong incremental momentum. Additionally, the backlog of orders for the previously hot-selling i6 is expected to be gradually depleted. Overall, the boost to sales volume from the new model cycle has not yet been effectively released.

② Revenue guidance is similarly 'underwhelming'

Q2 automotive revenue guidance is only RMB 24.1-25.4 billion, also below market expectations of RMB 26.3 billion, representing a YoY decline of about 16%-20%. This guidance implies a Q2 ASP of around RMB 238,000—an increase of about RMB 12,000 QoQ from the already low Q1 ASP of RMB 226,000 but still below market expectations of RMB 245,000.

This similarly reflects that order volumes for the refreshed higher-priced L9 may be relatively modest, failing to effectively drive the overall ASP back to a higher level.

However, on a positive note, Li Auto explicitly stated that with the launch and delivery of the all-new L9, it expects the automotive gross margin to recover from 6% in Q1 to around 10% in Q2. Nevertheless, this is still significantly lower than Li Auto's previously maintained 'healthy gross margin level of 20%,' indicating limited recovery and continued significant pressure on profitability.

However, looking beyond Q1's operational trough and considering the full-year 2026 performance:

① Li Auto is set to intensively launch a comprehensive refresh of the L-series models + an all-electric flagship i9

In Q2 2026, Li Auto took the lead in launching a major refresh of the L-series models—the all-new L9 (launched and delivered on May 15). Next, the refreshed L8, L7, and L6 will be sequentially released and deliveries will begin from late Q2 to the second half of the year. Among them:

- L8 (five-seat flagship): Deliveries expected to begin in Q3, with increased body dimensions, equipped with a 115kW range extender and a 72.7 kWh battery pack;

- L7 (large six-seat premium): Positioned in the RMB 300,000 price band, following closely after the L8;

- L6 (large five-seat premium): Expected to launch in Q4, with a new 51 kWh large battery version;

- i9 (all-electric flagship SUV): To be launched in the second half of the year as Li Auto's first full-size all-electric flagship.

Based on the already released L9 series, Li Auto has achieved upgrades in specifications and product competitiveness:

a. Significant battery and range upgrades: Standard 72.7 kWh 5C ultra-fast charging battery across all variants, with a CLTC all-electric range of 420 km (+50% vs. the previous model);

b. Range extender system refresh: Equipped with a third-generation in-house-developed range extender, achieving a WLTC feed-in fuel consumption as low as 6.3L/100km (previous model: 7.6L);

c. In-house-developed AI driving chip adoption: The M100 'Mach' chip (5nm process) makes its debut, with a dual-chip total computing power of 2560 TOPS;

d. Comprehensive chassis technology leap: Debut of a fully integrated drive-by-wire active chassis, covering drive-by-wire steering, rear-wheel steering, 800V active suspension, and EMB drive-by-wire mechanical braking;

e. Optimized body proportions: Shortened front overhang, extended rear overhang, visually shifting the center of gravity rearward, while replacing 12 ultrasonic radars with UWB sensors for a flawless vehicle surface.

It is evident that Li Auto has implemented a clear strategy of 'upgrading specifications while stabilizing prices + streamlining focus' for its 2026 model lineup:

a) Pursuing 'upgraded specifications but more pragmatic pricing': Taking the new L9 as an example, the Ultra version is priced at RMB 459,800 (a RMB 20,000 increase over the previous model but with greater specification upgrades), while the Livis version is priced at RMB 509,800 (a RMB 50,000 reduction from the pre-sale price). By stratifying the product lineup (standard version for volume sales, Livis version to define brand height) as its core competitiveness, it achieves 'full specifications from entry-level';

b) Streamlining SKUs for a more focused product line: Reducing from four previous product lines (9876) to two main lines—a flagship series (L9 six-seat + L8 five-seat) and a premium series (L7 large six-seat + L6 large five-seat)—to address past issues of excessive SKUs, minimal model differentiation, and difficulty in offering high specifications in lower price bands.

This combination of 'trading specifications for sales volume and streamlining for efficiency' aims to counter the impact of the market's full-scale shift to extended-range/plug-in hybrid segments in 2026, reverse the decline of the L-series mainstay models, and rebuild product moats rely on (relying on) AI capabilities (in-house-developed chips + VLA large models).

② Li Auto's strategy of continued investment in AI is expected to remain unchanged:

a. In-house computing power base Coming soon to land (about to land): The in-house-developed 'Mach 100 (M100)' chip, manufactured on a 5nm process, is about to enter mass production, with an effective computing power of up to 2560 TOPS in a dual-chip configuration per vehicle. This chip will debut on the new flagship L9 Livis model and plans to make VLA large models standard across the lineup in 2026.

b. Cross-border embodied AI: R&D efforts are officially extending to 'spatial robots,' integrating foundational models, in-house-developed chips, and robot operating systems. It is rumored that Li Auto's first embodied AI two-wheeled robot is expected to officially debut in the first half of this year.

From the current stock price position of Li Auto:

The company still maintains its target of achieving over 20% YoY sales volume growth in 2026, translating to approximately 480,000 units. The increment is expected to come from three major segments: ① a comprehensive refresh of the L-series models; ② i6 achieving a full-year delivery cycle (launched in H2 2025); and ③ incremental contributions from the new all-electric flagship i9 (launched in H2).

However, considering:

a) Intensifying market competition: Competitors are launching large-sized extended-range SUVs targeting Li Auto's L-series, creating Intensive encirclement and suppression (intense encirclement) in the RMB 250,000-350,000 price band;

b) i6's hot sales but ASP-lowering effect: As a mainstream volume model, its pricing is lower than the L-series, structurally depressing the overall ASP;

c) i9's non-volume nature: The all-electric flagship serves as a brand-uplifting and technology-verification model, with a limited sales ceiling;

Therefore, under neutral assumptions, Haitunjun expects Li Auto's full-year 2026 sales volume to be approximately 447,000-467,000 units, representing a YoY increase of about 10%-15%, falling short of the company's official guidance of 20%+.

On the revenue side, with the Gradually recovering (gradual recovery) of the share of high-priced models (refreshed L9, L8) and steady volume contributions from the i6, the full-year ASP is expected to be in the RMB 230,000-245,000 range. Adding other business revenue (charging networks, accessories, and services) of approximately RMB 6.5 billion, the corresponding total full-year revenue is expected to be approximately RMB 113.7-118.5 billion.

Considering Li Auto's currently abundant cash on hand (approximately RMB 91.7 billion) and its simultaneous progress in embodied AI (in-house-developed M100 chip, VLA AI driving model, humanoid robots, etc.), along with the automotive main business's cash flow generation capabilities, our neutral-assumption reasonable market capitalization is largely in line with the current U.S.-listed market capitalization. Even considering the potential option value of the AI business, there is limited room for further upside. Li Auto's 'turnaround' has not yet arrived.

Thus far, all three of the 'Wei, Xiao, Li' new energy vehicle startups have experienced their own 'life-and-death crises.' However, the differences are that Xpeng and NIO, facing severe cash flow shortages, have undergone painful organizational introspection, supply chain reforms, and strategic adjustments regardless of their financing capabilities.

What sets Li Auto apart is that it has accumulated a certain amount of cash capital through the L-series product cycle, but this has also dulled its internal sense of 'survival crisis.' With a weak automotive mainstay, it has further expanded its battlefront into areas such as robots and AI. Haitunjun still hopes to see organizational introspection and reforms in Li Auto's automotive operations.

Below is a detailed analysis:

Since Li Auto's sales volume has already been announced, the most critical marginal information lies in: 1) Q1 vehicle sales gross margin; and 2) Q2 2026 business outlook.

I. Vehicle Sales Gross Margin Plummets 'Off a Cliff'

Let's start with the vehicle sales business, which is of greatest concern to the market. Since Li Auto provided clear guidance in the previous quarter's earnings call—Q1 vehicle sales gross margin of around 5%, mainly affected by purchase tax subsidy support, the rising share of the lower-priced i6 model, and inventory clearance of the old L-series models—the market had already anticipated this quarter's vehicle sales gross margin, with consensus expectations also around 5%.

Ultimately, the actual automotive gross margin for the quarter was 6.1%, a sharp decline of 10.7 percentage points QoQ from 16.8% in the previous quarter, only about 1 percentage point higher than the market's 'low expectations.'

The combination of declining ASP and rising costs directly 'dragged' the gross margin 'into the mud,' directly reflecting the enormous pressure Li Auto faces in vehicle sales.",

① Significant increase in the proportion of low-priced i6 models, decline in the proportion of high-priced Mega models:

The model mix for Li Auto continued to shift significantly towards lower-priced segments this quarter. Due to the strong sales of the lower-priced battery electric vehicle (BEV) model i6, its share in the model mix surged to approximately 60% quarter-over-quarter, while the proportion of the higher-priced Mega model continued to decline (down by about 2 percentage points quarter-over-quarter to roughly 1.4%). This dual effect pulled down the overall average selling price (ASP) of vehicles.

② Li Auto continues to increase discounts for core L-series models:

In the first quarter, sales of Li Auto's core L-series models faced both internal and external pressures: internally, the lower-priced BEV models created internal competition, while externally, competitors launched large-sized extended-range SUVs targeting the L-series, intensifying market competition.

In response, Li Auto further increased discounts for its core L-series models—offering larger discounts in the first quarter compared to the fourth quarter of last year (e.g., approximately RMB 36,000 off for the L6, RMB 45,000 off for the L7/L8, RMB 50,000 off for the L9, and RMB 17,000 off for the Mega), along with continuing insurance subsidies and 0%/low-interest financing policies.

Despite these efforts, the decline in sales of the core L-series models was not fully arrested. In the first quarter, L-series sales continued to decline by about 64% year-over-year to approximately 32,000 units. Ultimately, with the strong sales of the i6 model filling the gap, overall sales managed a slight 2% year-over-year increase to 95,000 units.

2. Vehicle cost per unit rises by RMB 5,000 quarter-over-quarter, as upstream raw material cost increases erode gross margin

The cost per vehicle in this quarter was approximately RMB 213,000, up by about RMB 5,000 from the previous quarter. Despite the significant increase in the proportion of the lower-priced i6 model in the model mix, vehicle costs continued to rise, primarily due to the combined effects of the following three factors:

① Weakened scale effect: Li Auto sold 95,000 vehicles in the first quarter, down by about 13% quarter-over-quarter. The weakened scale effect led to an increase in depreciation and amortization costs per vehicle.

② Continued rise in raw material costs: In the first quarter, Li Auto also faced upward pressure on the prices of upstream storage chips, bulk raw materials, and batteries. The gross margin target for the i6 model was initially set at 15%, but due to cost increases in key components such as storage, management estimated the impact on gross margin to be around 3 percentage points.

③ Increased costs from i6 purchase tax subsidies: To address consumer hesitancy due to adjustments in the purchase tax reduction policy, Li Auto provided certain purchase tax subsidies for the i6 model (e.g., approximately RMB 15,000 in subsidies for customers who locked in non-cancellable orders before October 31, 2025, and took delivery in 2026), further increasing subsidy costs.

3. Gross profit per vehicle drops to RMB 14,000, a significant decline of RMB 28,000 quarter-over-quarter

From the perspective of profitability per vehicle, Li Auto earned only about RMB 14,000 in gross profit per vehicle sold in the first quarter, a sharp decline of about RMB 28,000 from approximately RMB 42,000 in the previous quarter. The gross margin per vehicle has reached a historical low, with the actual automotive gross margin also declining by 10.7 percentage points quarter-over-quarter to 6.1% in this quarter. This reflects the immense pressure Li Auto is facing in vehicle sales.

II. Q2 revenue and sales guidance both underperform

a) Sales guidance falls short of expectations, with lackluster orders for the new-generation L9

Li Auto's sales guidance for the second quarter is 95,000–100,000 units, not only below market expectations of 108,000 units but also representing a year-over-year decline of 10%–14.4%. Given that 34,000 units were delivered in April, the implied average monthly sales for May/June under this guidance is only 30,500–33,000 units—showing a sequential decline compared to April.

The largest new product catalyst in the second quarter—the all-new generation L9—officially launched and began deliveries on May 15. The signal behind this lower-than-expected and sequentially declining monthly sales guidance is that orders for the new-generation L9 are currently lackluster, failing to provide strong incremental momentum. Additionally, the backlog of orders for the previously strong-selling i6 model is expected to be gradually depleted. Overall, the boost to sales from the new product cycle has not yet been effectively realized.

b) Revenue guidance also underperforms

The automotive revenue guidance for the second quarter is only RMB 24.1–25.4 billion, also below market expectations of RMB 26.3 billion, representing a year-over-year decline of about 16%–20%. The implied ASP for vehicle sales in the second quarter under this guidance is approximately RMB 238,000—up by about RMB 12,000 from the already low level of RMB 226,000 in the first quarter but still below market expectations of RMB 245,000. This also reflects that order volumes for the revised high-priced L9 model may be relatively modest, failing to effectively pull the overall ASP back to a higher level.

However, on a positive note, Li Auto explicitly stated that with the launch and delivery of the all-new L9, the automotive gross margin is expected to recover from the low of 6% in the first quarter to about 10% in the second quarter. Nevertheless, this is still significantly lower than Li Auto's previously maintained "healthy gross margin level of 20%," indicating limited recovery and continued significant pressure on profitability.

III. Controlled growth in operating expenses

1) R&D expenses: Decline quarter-over-quarter, but full-year guidance still up

R&D expenses in this quarter were RMB 2.72 billion, down by about RMB 300 million from the previous quarter (approximately RMB 3.02 billion), broadly in line with market expectations. The sequential decline in R&D investment was likely primarily due to seasonal factors in investment timing rather than strategic contraction. Company management explicitly guided that full-year R&D expenses for 2026 are expected to remain at approximately RMB 12 billion, still representing a year-over-year increase of about 6% from RMB 11.3 billion in 2025. The main investment directions are as follows:

a. Upfront R&D investment for the dense (intensive) new product cycle: To prepare for the product-heavy year of 2026, Li Auto is accelerating R&D reserves for new models. This includes not only a complete overhaul of the L-series family (L6, L7, L9, etc.) but also covers an all-new full-size BEV SUV model, the i9.

b. Ongoing investment in the "All in AI" strategy: AI has become Li Auto's largest R&D expenditure item. In 2025, Li Auto invested over RMB 6 billion in AI, accounting for more than half of the total annual R&D expenses of RMB 11.3 billion. AI investment is mainly divided into two parts:

- Approximately 60% invested in AI infrastructure: Focusing on breakthroughs in foundational large models, self-developed inference chips, self-developed operating systems, and cloud/vehicle-side computing clusters.

- Approximately 40% invested in AI product commercialization: Covering Li Auto Assistant, multimodal intelligent agents (Agents), intelligent cockpits, intelligent manufacturing, and business analysis systems, as well as supporting the OTA rollout of the self-developed intelligent driving model across all AD Max models.

For 2026, Li Auto's strategy of continued investment in AI is expected to remain unchanged, with full-year AI investment still projected to be around RMB 6 billion. Centered around this core AI strategy, the company is deploying resources in the following three directions:

① Landing of self-developed computing power infrastructure: The self-developed "Mach 100 (M100)" chip, manufactured using a 5nm process, is about to enter mass production, with its dual-chip configuration delivering effective computing power of up to 2,560 TOPS per vehicle. This chip will debut in the new flagship L9 Livis model and is planned to be standard across all models with the VLA large model in 2026. Compared to ADAS 8.0, the ADAS 9.0 version equipped with the M100 chip features more human-like decision-making in complex scenarios and smoother longitudinal and lateral control.

The next steps will involve further expanding the scale and precision of input data and enhancing the model's cognitive ability for short-term causal relationships. The company aims to match the performance of Tesla FSD v14 in the U.S. by the second half of this year.

② Cross-border embodied AI: R&D efforts are extending toward "spatial robots," integrating foundational models, self-developed chips, and robot operating systems. However, Li Auto stated that for humanoid robots to achieve full-scale commercial deployment similar to that of new energy vehicles between 2010 and 2015, it will still take more than three years. Currently, technical paths in multiple specific directions have not converged, and many challenging problems remain to be solved.

③ Intelligent driving sprint for L4: Li Auto has set a goal of achieving L4-level autonomous driving by 2028 at the latest.

2) Sales and administrative expenses decline quarter-over-quarter, well-controlled

Sales and administrative expenses in this quarter were RMB 2.05 billion, down by about RMB 600 million from approximately RMB 2.65 billion in the previous quarter, also below market expectations (around RMB 2.26 billion). The effectiveness of cost control primarily came from adjustments in the following three areas:

a. Organizational optimization and staff reduction: In the fourth quarter, Li Auto made certain staff adjustments and structural optimizations in its marketing department, with a turnover rate of about 15% for frontline sales in directly operated stores, effectively reducing salary expenses.

b. Seasonal factors: No new models were launched in the first quarter, leading to a corresponding reduction in marketing and promotional expenses related to model launches.

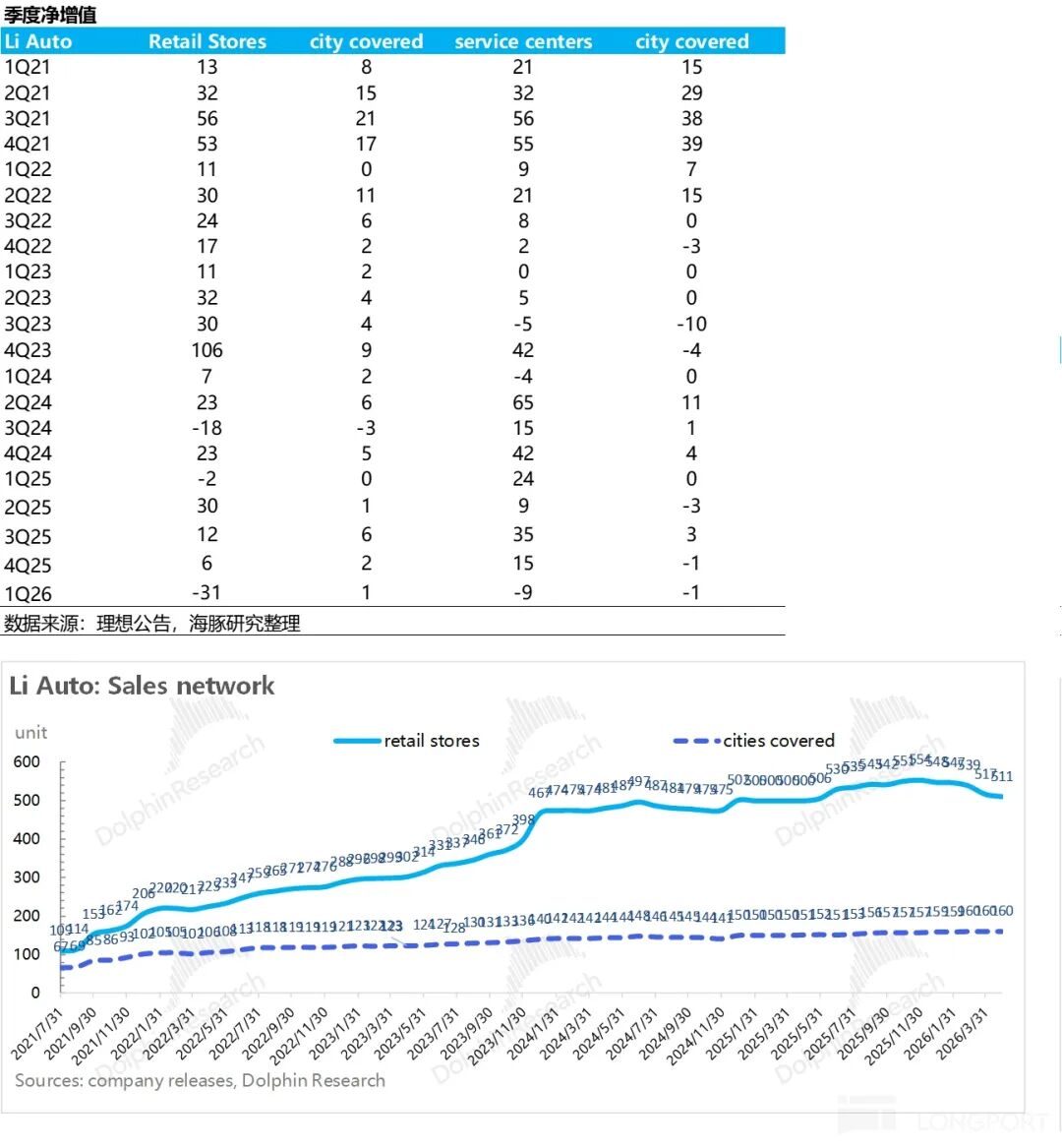

c. Channel strategy shift from "expansion" to "intensive cultivation": Li Auto has transitioned from aggressive early-stage expansion to cautious operation, proactively closing and optimizing some low-performing stores to reduce costs. In the first quarter, Li Auto's retail centers nationwide decreased by a net of 31, while service centers decreased by a net of 9.

IV. Revenue declines year-over-year again

Given the announced sales volume, Li Auto's total revenue in the first quarter was approximately RMB 23 billion, slightly below market expectations, representing a year-over-year decline of 11.4%.

Among this, automotive sales revenue was RMB 21.5 billion, performing below market expectations, primarily due to the strong sales of the lower-priced i6 model, which continued to pull down the ASP, coupled with Li Auto's increased promotional efforts for the older L-series models, further dragging down the ASP.

Other business revenue was RMB 1.45 billion, down by about RMB 70 million quarter-over-quarter but still up by 16% year-over-year. The year-over-year increase was mainly driven by the continuous growth in the vehicle ownership base, leading to an increase in the provision of products and services complementary to automotive sales.

In terms of gross margin, the overall gross margin in this quarter was 7.9%, down by about 10 percentage points from 17.8% in the previous quarter. This cliff-like decline was primarily dragged down by the automotive business gross margin, which declined by 10.7 percentage points quarter-over-quarter to 6.1%.

The gross margin for other businesses was approximately 34.5%, down by about 1.5 percentage points quarter-over-quarter. The sequential decline may be mainly because Li Auto also increased its provision of complimentary accessories, leading to a compression in the profit margin of its service business.

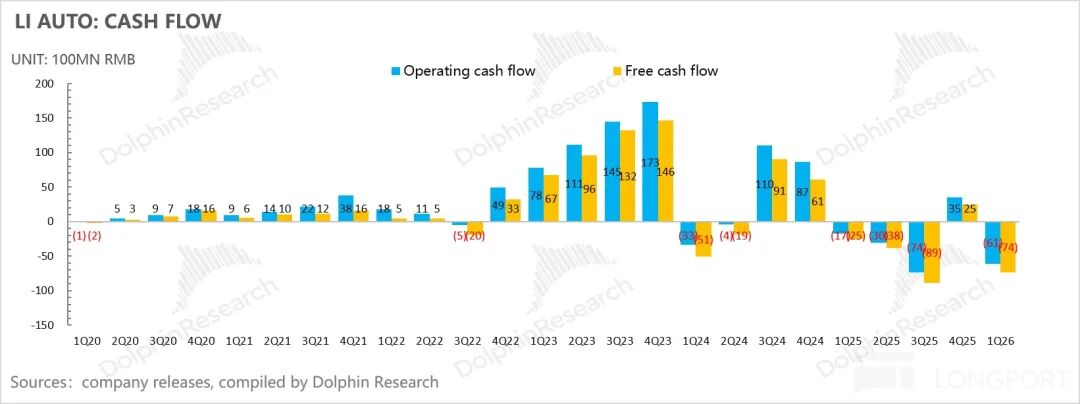

V. Significant depletion of free cash flow, but cash reserves remain sufficient

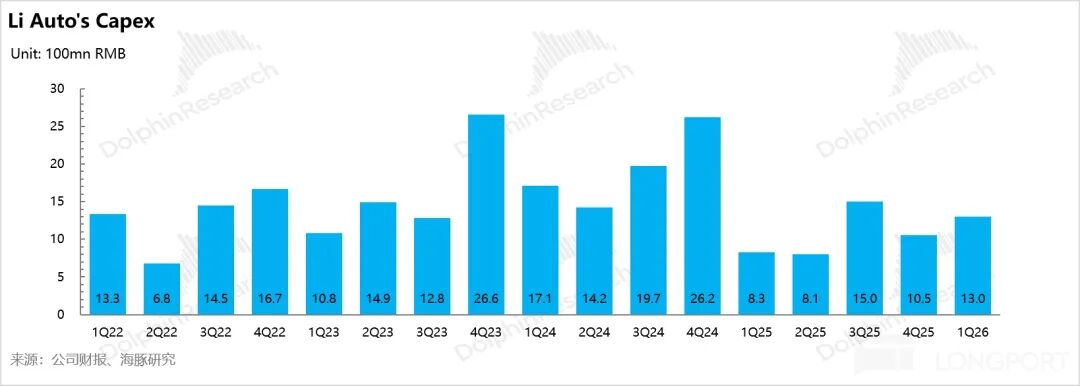

Operating cash flow in this quarter was RMB 6.1 billion, down sharply by about RMB 9.6 billion quarter-over-quarter. Meanwhile, capital expenditures increased by RMB 250 million quarter-over-quarter to RMB 1.3 billion. The combination of these two factors resulted in a free cash flow of RMB -7.4 billion, down by about RMB 9.9 billion quarter-over-quarter.

The core reasons for the significant depletion of operating cash flow are twofold:

a. Sharp decline in operating profit: The leverage effect of sales volume was not realized in the first quarter, coupled with the cliff-like decline in gross margin. Despite controlled operating expenses, operating profit still declined by nearly RMB 2.55 billion quarter-over-quarter to RMB 3 billion, becoming the largest drag on cash outflows.

b. Decrease in accounts payable: In the first quarter, the company proactively repaid some supplier payments, leading to a contraction in the scale of accounts payable and further intensifying the pressure on operating cash outflows.

Nevertheless, Li Auto still has ample cash on hand. As of the end of the first quarter, the company held RMB 91.7 billion in cash and cash equivalents (net cash of RMB 84.3 billion), with controllable short-term liquidity risks, providing relatively solid financial support for subsequent new product cycles and AI investments.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial condition, or special needs of any person receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information mentioned or the opinions expressed in this report shall not be considered or deemed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction, nor shall they constitute advice, inquiry, recommendation, etc. regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for or proposed to be distributed to citizens or residents of jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials would conflict with applicable laws or regulations, or would result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Why Did the Former Chairman of Ferrari Get 'Angry' About Its First All-Electric Model, Luce?

-

Exclusive! Gas Leak at SK Hynix’s Cheongju Facility in South Korea Leaves 6 Injured—Could DDR5 Prices Surge Once More?

-

![]()

Leading the Charge in Ensuring Intelligent Driving Safety: Can BYD Outshine Huawei?

-

![]()

Li Auto (1Q26 Highlights): Maintains 20%+ Sales Growth Target for 2026

-

![]()

Ideal: Wanting Too Much Leaves Only 'Daydreams'?

-

![]()

Entering the Japanese Market Requires Learning 'Magic'

-

FTTH installation and maintenance engineer, how many instruments do you carry when you go out?

-

![]()

Is Waymo's Self-Driving Car 'Made in China'? When U.S. Robotaxi Leader Teams Up with Zeekr's 'Baby Bus', a Multi-Billion-Dollar Cross-Border Alliance Emerges