Shenzhen-Based Company, Once Dependent on BYD and Geely, Now Thrives with Roborock and Ninebot

06/03 2026

06/03 2026

410

410

Source | Yuan Media Hub

After years of intense competition among domestic LiDAR companies, the market has transitioned from a "hundred-team scramble" to a stable top three. These leading firms are fiercely vying for design wins, vehicle mass production, and cost reductions, leaving no stone unturned. However, the most captivating new narrative has emerged not in the new energy vehicle sector but on overseas lawns.

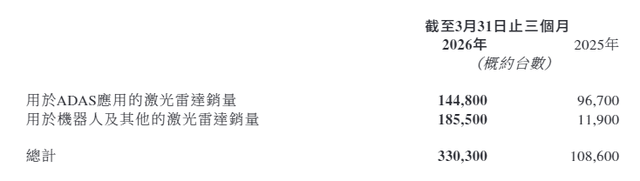

In late May, RoboSense's Q1 2026 earnings report garnered significant market attention: quarterly revenue soared to RMB 460 million, up nearly 40% year-on-year; total LiDAR shipments reached 330,000 units. The most remarkable growth came from the robotics business, with 185,500 units shipped, marking a staggering 1,458% year-on-year increase. Its revenue share also surged from 11% in the same period last year to 56.2%.

Image source: RoboSense Q1 2026 report

This Shenzhen-based LiDAR company witnessed its robotics business sales surpass its mainstay automotive ADAS business for the first time.

A long-time supplier to domestic smart electric vehicle makers, specializing in automotive LiDAR for years, this company has now reached new performance heights, thanks to a smart lawn mowing robot. This story alone merits discussion.

01. The Second-Place Automotive LiDAR Player Gets a Boost from Lawn Mowers

RoboSense has long been recognized as the "second-place automotive LiDAR player." Its clientele includes renowned automakers such as BYD, Geely, GAC, and XPeng. With ADAS LiDAR sales reaching hundreds of thousands of units annually, it has been the absolute revenue mainstay.

However, while the automotive sector is promising, it has long been a fiercely competitive market.

Currently, Hesai Technology is fiercely defending its market share, Huawei's self-developed LiDAR directly secures core clients like Seres, and Innovusion steadily captures a share with NIO. According to data released by Gasgoo, in Q1 2026, RoboSense ranked only fourth in LiDAR installations in China's passenger vehicle market, with an 11.0% market share.

Image source: Gasgoo

Even more detrimental than peer competition is the relentless price war, with automotive LiDAR unit prices plummeting from thousands of US dollars in early years to the hundreds of dollars range. By 2025, RoboSense's average automotive product price had fallen below $500, with gross margins continuously compressed and profitability almost elusive.

Simply put, automotive LiDAR is not a highly profitable business. With automakers themselves engaged in price wars, the bargaining power of upstream suppliers is evident.

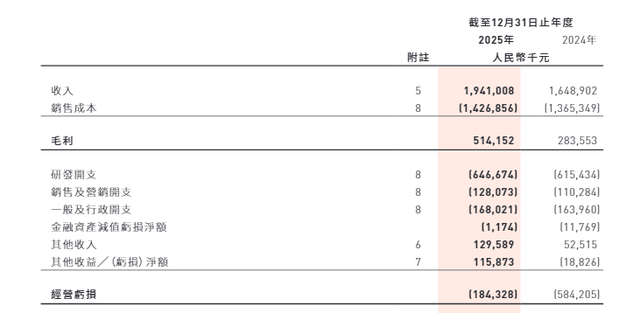

A review of RoboSense's 2025 financials reveals decent full-year revenue growth, but persistent losses due to the profitability of its automotive business being suppressed by price wars.

Image source: RoboSense 2025 financials

Therefore, when RoboSense's robotics business volume suddenly hit 185,500 units in Q1 2026, accounting for over half of the total, the market realized the company had finally broken free from the constraints of a single automotive business and quietly established a second growth curve.

The core of RoboSense's robotics boom lies in the seemingly niche smart lawn mowing robot, commonly known as a lawn mower.

Yun Junchun, Deputy CFO of RoboSense, revealed at the Q1 earnings call that the company expects to ship over 600,000 lawn mowing robots in 2026. For comparison: the company shipped only 200,000 lawn mowing robots in all of 2025, and virtually none before Q1 2025.

From zero to 200,000 to 600,000 in just over a year. What does this signify? Consider that RoboSense has dedicated itself to the automotive sector for nearly a decade, with ADAS LiDAR shipments reaching just over 300,000 units annually. The growth rate of the lawn mower sector in one year has directly surpassed a decade's accumulation in the automotive sector.

So, who is buying all this LiDAR? A look at RoboSense's client list reveals that besides traditional overseas lawn mower giants, the real drivers are a group of veteran players from China's robotic vacuum cleaner industry, such as Roborock, Ninebot's Weilan Continental, and Kuma Technology.

Over the past decade, these Chinese players have transformed robotic vacuum cleaners from "toys that bump around the living room" into household staples capable of mapping, obstacle avoidance, and self-cleaning mop pads. However, with the domestic market reaching saturation, leading players have turned overseas to explore new scenarios. The expansive lawns in American and European backyards present the next big opportunity for robotic vacuum giants.

The crossover logic is straightforward: the navigation, obstacle avoidance, and path planning technologies of indoor robotic vacuums are highly transferable to lawn mowing robots, with the only difference being a sensor solution capable of withstanding outdoor environments. And this is precisely what RoboSense can provide.

One side seeks markets, the other seeks clients—a perfect match. Robotic vacuum giants bring their channels and brands to European and American lawns, with RoboSense's LiDAR installed in their export containers.

Many may wonder: Why must lawn mowers use LiDAR? Can't mature pure vision solutions suffice?

This relates directly to the uniqueness of outdoor scenarios. Overseas household lawns may seem simple but place extremely high demands on sensors. With uniform lawn textures, extreme light contrasts between morning and evening, and blurred boundaries between grass and flowers, pure vision solutions are prone to misidentification, treating flower beds and greenery as passable areas, leading to miscuts and erratic movements.

LiDAR, unaffected by light, offers precise ranging and stable mapping. With proper dust, water, and grass clip protection designs, it perfectly adapts to complex outdoor conditions, far outperforming vision solutions in stability.

Compared to automakers, lawn mower manufacturers have much shorter decision chains. While they also negotiate prices, they are not as "ruthless" as automakers. More importantly, lawn mowing robots are still in the early penetration stage, with single-digit penetration rates. The priority is to grow the market first, rather than immediately engaging in price wars.

It can be said that the biggest driving force behind RoboSense's robotics boom is the group of Chinese companies that turned robotic vacuums into a fiercely competitive market domestically and are now seeking growth overseas. Their overseas lawn mower sales have inadvertently carried RoboSense to new heights.

02. Comprehensive Entry into Robotics Application Scenarios

Of course, if RoboSense's robotics story were limited to lawn mowers, a ceiling would be visible.

According to IDC data, global shipments of lawn mowing robots reached 1.992 million units in 2025, up 63.8% year-on-year, making it the fastest-growing segment in the smart robotics market. However, even with this impressive growth, the global market is still only around 2 million units annually. Even if all were equipped with LiDAR, the overall market capacity remains limited.

But the interesting part is that lawn mowers serve as an entry point.

RoboSense's robotics portfolio is already quite extensive: humanoid robots, robotic dogs, mining trucks, last-mile delivery vehicles... These scenarios share a common trend—moving from "LiDAR not required" to "LiDAR preferred."

Take humanoid robots: starting in the second half of 2025, domestic humanoid robot startups entered a new phase of financing and mass production, with companies like Unitree, Fourier, and Zhiyuan expanding production. Humanoid robots demand far higher spatial awareness than wheeled robots, requiring real-time 3D mapping for bipedal locomotion, making LiDAR almost essential. RoboSense has already secured numerous design wins in this area.

The same logic applies to robotic dogs, especially in outdoor scenarios like power grid inspections and security patrols, where LiDAR's robustness offers clear advantages.

Mining trucks need no introduction—open-pit mines are dusty with extreme lighting conditions, making cameras and millimeter-wave radar inadequate, with LiDAR being essential.

In this light, RoboSense's robotics business is not a single-point explosion but a simultaneous rise across multiple scenarios, with lawn mowing robots simply leading the charge.

In other words, RoboSense's identity is changing.

Previously, the market valued RoboSense as an automotive LiDAR company, benchmarking it against Hesai and focusing on design win counts, shipment volumes, ASP trends, and gross margin improvement curves. Under this framework, the company was perpetually shadowed by price wars, with valuation hard to break through.

But with robotics accounting for over half of its business, the story has changed.

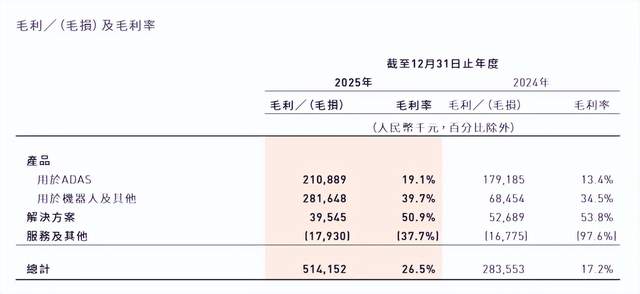

Image source: RoboSense 2025 financials

The robotics industry is still in its early stages, with low LiDAR penetration, rapid growth, and a relatively friendly competitive landscape. Moreover, robotics clients are diversified—lawn mower makers, humanoid robot companies, and mining truck manufacturers operate in different industries, giving RoboSense stronger bargaining power compared to the automotive era.

Of course, this doesn't mean the automotive business is unimportant. ADAS remains RoboSense's foundation, with over 300,000 automotive LiDAR shipments and long-term partnerships with automakers. However, with automotive mired in low-margin internal competition and sluggish growth, robotics offers a pathway to higher profits and valuations.

Another point worth noting: RoboSense is not just selling hardware in robotics. With rising shipment volumes, it has begun bundling perception algorithms and software services, whose margins far exceed pure hardware. This differs fundamentally from the "selling boxes" logic of the automotive era.

This also underscores a core logic in the hard tech industry: for platform technology companies, the extensibility of technology across scenarios matters far more than niche market dominance. While LiDAR's growth ceiling is visible when tied to the automotive sector, the robotics world has only just begun unlocking application scenarios, with limitless future potential.

Of course, risks remain in the new sector. Will the 2026 target of 600,000 lawn mower LiDAR shipments be met? Will humanoid robot mass production schedules fall short and face delays? Will the automotive sector's internal competition spill over into robotics? These questions require time to answer.

But at least starting from this quarter's earnings, RoboSense has completely broken free from the single-minded dependence on automakers. For its investors, there's no longer a need to guess performance based on monthly automotive sales and order fluctuations.

The once-underappreciated lawn care business has ultimately grown into a sexier, more promising story than the automotive sector.

Note: Some images in the text are AI-generated/sourced from the internet. Please notify us for removal if any infringement is found.

-

![]()

BYD’s Monthly Overseas Sales Soar Past 160,000 Units: Elevated Gross Margins Drive Profitability!

-

![]()

Tencent's Trump Card Has Never Been Large Models

-

![]()

Trunk Technology Joins Forces with Two National Teams: Can Autonomous Driving Tackle the 'North-South Grain Transport' Challenge?

-

![]()

Smartphone Makers Clash in 618 Sales Battle: Genuine Deals vs. Superficial Cuts

-

![]()

From HW1.0 to AI5: Has Tesla's Chip Seen a Radical Transformation?

-

![]()

Just Now! ChatGPT Incorporates Codex, What’s OpenAI’s Next Move?

-

![]()

Smartphone Manufacturers Clash in 618 Sales Battle: Genuine Discounts vs. Superficial Cuts

-

![]()

Just Now! Microsoft Sounds the AI Rallying Call: Unveils Powerful AI PC, Develops Proprietary Models to Diversify from OpenAI