Across-the-Board Decline: Joint Venture Brands Feel the 'Boomerang' Effect

06/05 2026

06/05 2026

475

475

Stock Competition

Joint venture brands, which had been building momentum for a considerable time before their anticipated surge, failed to deliver the expected 'turnaround.'

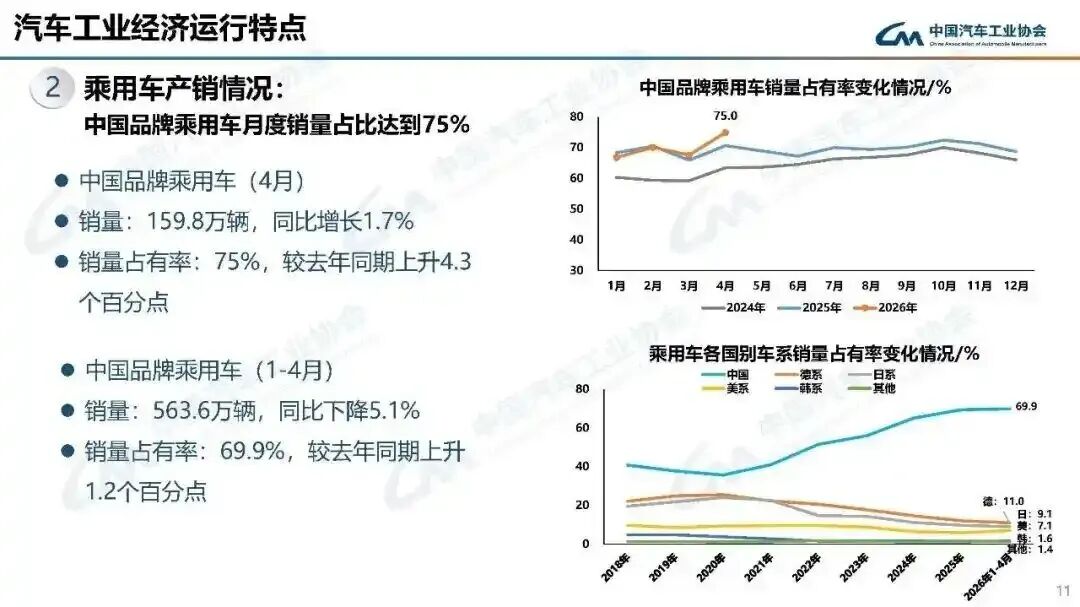

According to data from the China Association of Automobile Manufacturers, overall passenger vehicle sales in April experienced a 4.2% year-on-year decline. Among these, Chinese brand passenger vehicles sold 1.598 million units, marking a 1.7% year-on-year increase, and capturing a 75% market share, up 4.3% from the previous year.

Amidst overall market pressure, the market share of Chinese brand passenger vehicles reached a new peak, representing one of the most notable shifts in the April auto market. This development has posed significant challenges for joint venture brands, which have long enjoyed market prominence, as the dynamics of market offense and defense have undergone a complete reversal.

From followers to trendsetters, Chinese auto brands have not only achieved a record 75% market share for the first time but have also witnessed a simultaneous rise in the domestic penetration rate of new energy vehicles, surpassing 60% for the first time. Meanwhile, Chinese brands' export figures have continued to soar, with 901,000 vehicles exported in April alone, reflecting a 3% month-on-month increase and a staggering 74.4% year-on-year surge. Major Chinese brands are also swiftly expanding their overseas market presence.

These record-breaking numbers signify that the entire Chinese auto industry has officially entered a new era of profound transformation. From the domestic to the global market, Chinese brands are on the offensive, completely reshaping the market landscape.

Now, the survival challenges for joint venture brands are laid bare. Can they cling to their remaining market share of around a quarter?

Stock Competition

Cumulative data reveals that domestic passenger vehicle sales from January to April declined by 6.7% year-on-year, with Chinese brand passenger vehicles selling 5.636 million units, a 5.1% year-on-year decrease. This suggests that the increase in market share for Chinese brands stems more from displacing joint venture brands rather than a significant expansion in overall market demand.

Image Source: China Association of Automobile Manufacturers

Image Source: China Association of Automobile Manufacturers

Data from the China Passenger Car Association indicates that total retail sales of domestic narrowly defined passenger vehicles declined year-on-year in April, with fuel vehicles accounting for 84% of the decrease, while new energy vehicles maintained steady growth, becoming the market's core driver. This is also a key factor behind the expanding market share of Chinese brands, which are primarily focused on new energy vehicles. Specifically, new energy vehicle sales reached 1.344 million units in April, up 9.7% year-on-year, representing 53.2% of total vehicle sales.

Geely Auto led non-comprehensive vehicle manufacturers with a 57.65% new energy penetration rate, followed by GAC, SAIC, Chery, and Changan, all maintaining high penetration rates, indicating a deepening substitution effect for fuel vehicles. The growing proportion of high-end and intelligent models has become a core driver for automakers' profitability and brand elevation.

In contrast, joint venture brands have seen limited breakthroughs in the new energy sector, as most of their new energy models have failed to gain traction with the market and consumers. The brief resurgence of fuel vehicles came to an abrupt halt amid the strong growth of new energy vehicles and rising fuel prices.

In April, joint venture brands collectively held only a 25% market share, with German, Japanese, American, and Korean brands all experiencing declines. German brands, while still leading the joint venture camp with an 11% share, saw a 2.2% year-on-year decrease. Japanese brands fell below a 10% share, while American brands held a 7.1% share, up slightly by 1.3% year-on-year, mainly due to Tesla, which has no joint venture partners. Korean and French brands are becoming increasingly marginalized.

Meanwhile, exports have emerged as a new growth engine for Chinese brands. Not only have overall export figures reached new heights, but new energy vehicle exports have also continued to rise. According to Chinese customs data, 278,000 electric vehicles were exported in April, up 40% year-on-year. Geely Auto and Chery Group achieved doubled growth, while BYD, Changan Automobile, SAIC Group, and Great Wall Motor saw overseas sales increase by over 50% year-on-year.

Chen Shihua, Deputy Secretary-General of the China Association of Automobile Manufacturers, stated that exports maintained strong growth in April, continuing the rapid growth trend observed since the beginning of the year.

From primarily competing in the world's largest domestic auto market to now thriving across multiple fronts, Chinese auto brands have shifted their competition from a single dimension to a multifaceted battle focusing on total sales volume, new energy vehicles, and exports. As Chinese brands rise, joint venture brands are increasingly struggling.

Collective Dilemma

Faced with the fierce offensive from Chinese auto brands, joint venture brands have continuously adjusted their attitudes toward the electrification trend, frequently revising their strategies to stabilize their existing market share while seeking breakthroughs.

Since the beginning of the year, several major new energy models from joint venture brands have made their debut, including SAIC Volkswagen's ID.ERA 9X, FAW-Volkswagen's ID.AURA T6, Volkswagen Anhui's Zony 08, Dongfeng Nissan's NX8, GAC Toyota's bZ4X 7, and Buick's Ultium E7. These launches signal a collective push by joint venture brands into the new energy sector.

These new models share common characteristics: they are localized pure electric vehicles tailored to Chinese road conditions, user habits, and consumer preferences.

Take Buick's Ultium E7 as an example. It abandoned the past approach of relying on 'brand premium + overseas platform transplantation' and instead adopted a localized 'configuration-focused' strategy. The model comes standard with 42 configurations, featuring a 'five-constant' healthy cabin, an Eames zero-gravity front passenger seat, a 15.6-inch rear-seat cinema screen, an intelligent cockpit powered by the Doubao large model + Qualcomm Snapdragon 8775 chip, intelligent driving assisted by Momenta R6 reinforcement learning model with lidar, and a 1.5T 'True Dragon' plug-in hybrid system offering a CLTC combined range of 1,630 kilometers.

Wang Chendong, Deputy General Manager of SAIC General Motors, said, 'At the company level, we have implemented a series of deep reforms, comprehensively optimizing our intelligent R&D system and decision-making processes, truly embodying the philosophy of 'in China, for China.'

With relatively rich configurations and high cost-effectiveness, coupled with Buick's ability to deliver vehicles immediately upon launch, the model quickly achieved 10,000 deliveries in its first month, setting a record for the fastest sales milestone among joint venture new energy vehicles. Previously, GAC Toyota's bZ4X 3X also achieved over 10,000 orders.

Wang Qian, Deputy General Manager of Dongfeng Nissan Automobile Sales Co., Ltd., stated on his personal Weibo account that Nissan's N series, Buick's Ultium series, and Volkswagen's ID series have completed deep localization in terms of technology and product strength. However, they all face the industry dilemma of user perceptions lagging behind product innovations.

The brand perception dilemma that Chinese auto brands struggled to overcome for years has now, like a 'boomerang,' returned to joint venture brands amid the rising penetration rate of new energy vehicles. The high-end breakthrough dilemma that once plagued Chinese auto brands has now transformed into an intelligent breakthrough dilemma for joint venture brands in the era of electrification.

With the market balance now completely tilted, do joint venture brands still have a chance?

This article is original to China-NNC Auto. Feel free to share it with your peers. Media outlets wishing to reprint it should credit the author and source at the beginning of the article. Any media or self-media outlets creating video or audio scripts based on this article's content will face legal consequences.

-

![]()

MiniMax Faces an Uphill Battle to Reclaim Its Initial Vision

-

![]()

Is XPENG Lagging Behind the Industry Leaders?

-

![]()

The Various Aspects of Life in the Era of Involution: Six New Forces Strive to Find Profit Points

-

![]()

AI Reshapes Globalization: New Opportunities for Chinese Enterprises Going Global

-

![]()

Across-the-Board Decline: Joint Venture Brands Feel the 'Boomerang' Effect

-

![]()

The More the US Attempts to 'Suppress' China, the More Innovative Chinese Automakers Grow?

-

![]()

CCTV, People’s Daily, and Other Media Outlets Weigh In: Is a Weight-Based Tax for Electric Vehicles on the Cards?

-

Lenovo Aims to Continue Spinning Its AI Narrative