Is XPENG Lagging Behind the Industry Leaders?

06/05 2026

06/05 2026

484

484

Recently, a widely circulated viewpoint has emerged: following the so-called industrial upgrading championed by certain 'visionary strategists,' BYD has not substantially increased its employees' salaries, while CATL distributed a staggering RMB 8.1 billion in dividends to its CEO.

In reality, this reflects a misunderstanding of the 'visionary strategy.'

BYD employs nearly a million workers. Although it hasn't raised wages, the employees it hires and the workers it supports along the supply chain—who previously could only earn RMB 3,000 per month screwing bolts in electronics factories—can now earn RMB 6,000-8,000 per month in automotive production, which, in essence, is a pay raise.

CATL recruited 40,000 junior college graduates in 2025 alone, offering an average annual salary of RMB 180,000. Even after accounting for substantial deductions, this still amounts to RMB 100,000.

Some argue that despite China's automotive industry advancing towards global leadership, salaries remain significantly lower than those of Western automakers.

Let me dispel the myth of Western 'high salaries': it's essentially economic colonization.

Take Volkswagen, for instance, with 700,000 global employees—400,000 in Germany and 70,000 in China. At its peak, China generated over half of Volkswagen's global profits.

In other words, China's 70,000 employees were effectively subsidizing the majority of Germany's 400,000-strong workforce.

A closer examination reveals that nearly every high-paying Western industry operates on this principle—essentially a sophisticated form of colonial economics.

China rejects colonial economics. We demand only fair compensation. The trade-off is that Chinese industrial workers won't earn the exorbitant profits seen in the West.

China ensures living standards through price stabilization and low living costs, pursuing a sustainable model of common prosperity that is distinct from Western colonial economics. This fundamentally reflects the difference between agrarian and piratical civilizations.

While we may envy Volkswagen employees' high salaries, the company just announced 50,000 local layoffs.

This is just the beginning.

1. The Volkswagen-XPENG Dynamic

After acquiring Gotion High-Tech and JAC Motors, Volkswagen has fully committed to China. The 50,000 layoffs reflect that R&D no longer needs to remain local.

In 2023, Volkswagen invested USD 700 million in XPENG, establishing a technical partnership. Two years later, this collaboration has entered a new phase. On March 13, the first model jointly developed by Volkswagen and XPENG—the Aimeo 08—commenced production in Hefei.

This marks Volkswagen's first full-time connected, full-size, pure electric SUV and its first strategic model developed and manufactured in Hefei.

More dramatically, XPENG is in negotiations to acquire or utilize Volkswagen's idle European factories. Cheng Xiaoguang, XPENG's Northeast Europe head, confirmed this development.

The role reversal is striking. Two years ago, Volkswagen was XPENG's financial backer and technical partner; now XPENG may absorb Volkswagen's idle capacity.

However, risks persist. Some Volkswagen factories are outdated and may not meet XPENG's latest product requirements. Acquiring European facilities also entails massive capital expenditures and operational challenges.

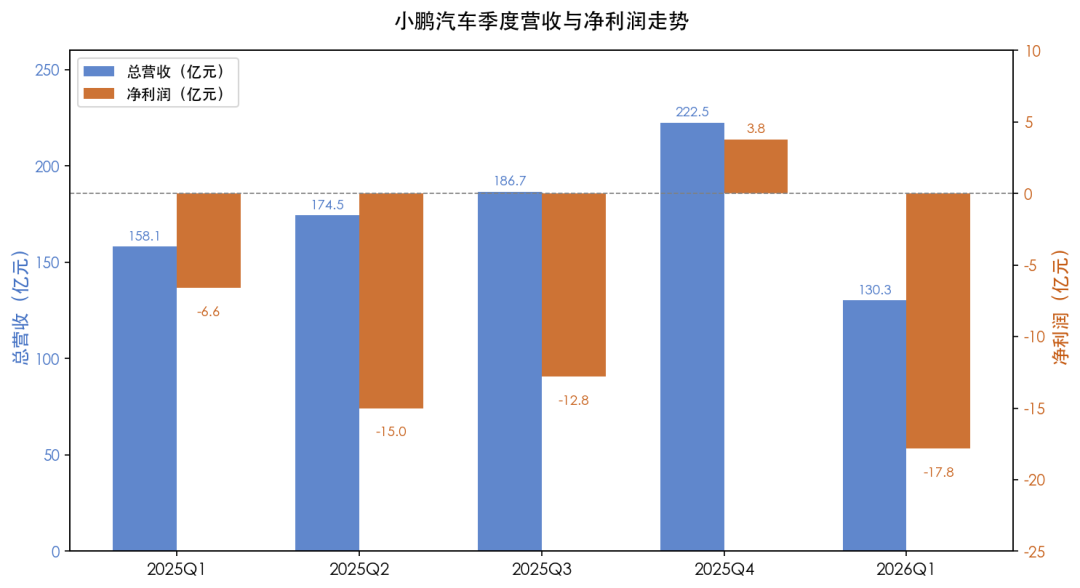

In Q4 2025, XPENG Group achieved a profit of RMB 380 million.

This marked the company's first quarterly profit since inception, leaving CEO He Xiaopeng visibly elated during the earnings call. However, the Q1 2026 report released on May 28, 2026, shattered that euphoria.

A loss of RMB 1.78 billion.

To put this in perspective: the Q1 2025 loss was RMB 660 million, a 169.7% year-over-year increase. The RMB 380 million profit from Q4 2025 now appears fleeting.

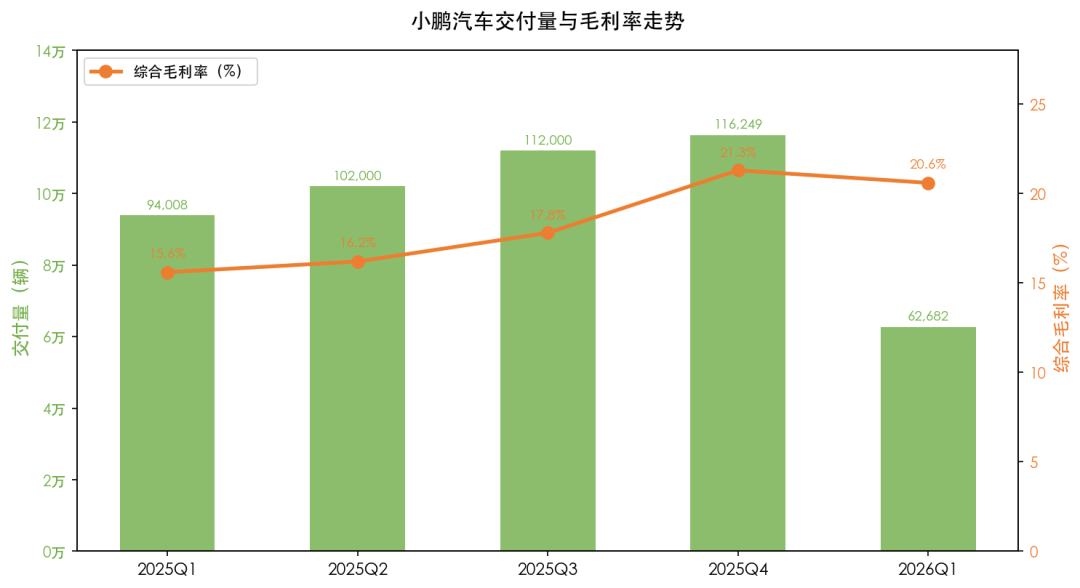

Total deliveries reached 62,682 units, down 33.3% year-over-year and 46% quarter-over-quarter. This plunge returned XPENG to levels last seen two years ago, erasing gains from Q4 2025.

Revenue collapsed accordingly. Total revenue hit RMB 13.03 billion, down 17.6% year-over-year and 41.4% quarter-over-quarter. Automotive sales revenue fell to RMB 11 billion, a 42.3% quarter-over-quarter contraction—the worst quarterly decline in recent memory.

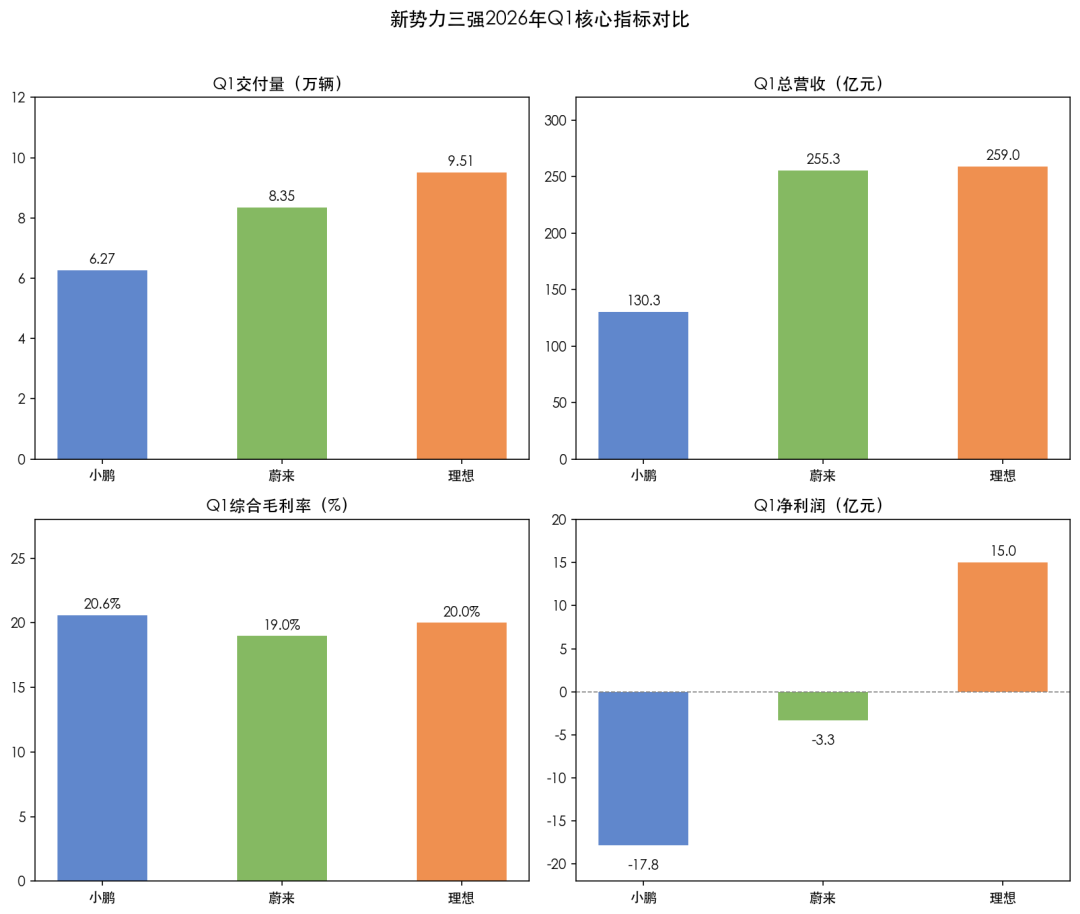

"Q1 is traditionally a slow season," the company claimed, but this excuse rang hollow against competitors. NIO delivered 83,465 units (+98.3% year-over-year), while Li Auto delivered 95,142 units (+2.5% year-over-year). When rivals grow, XPENG's decline signals deeper issues than seasonality.

2. The Secret Behind the Rising Gross Margin

Amid this gloom, one figure stood out: a consolidated gross margin of 20.6%.

This exceeded market expectations of 20% and improved by 5 percentage points year-over-year. Automotive gross margin reached 12.1%, up 1.6 points year-over-year.

Revenue fell, deliveries dropped, yet margins rose. This wasn't magic but structural optimization.

The secret lies in two areas:

First, service and other revenues hit RMB 2.03 billion, up 41.2% year-over-year. This primarily came from the Volkswagen partnership—technology licensing, platform sharing, and joint development.

Second, international revenues surged. He Xiaopeng revealed that April overseas sales topped 6,000 units for the first time, with international business contributing over 20% of revenue from Q2 onward.

"Self-developed technological innovation and rapidly growing international revenues maintained robust margins during the industry downturn," noted Gu Hongdi, highlighting XPENG's strategic shift from pure vehicle sales to technology exports and global expansion.

The question remains: Can service revenue growth sustain? Is Volkswagen partnership income recurring or one-off? With automotive sales revenue down 42.3% quarter-over-quarter, margin improvements resemble accounting maneuvers rather than genuine operational improvements.

3. R&D Spending Surges 46.8%

Q1 R&D investment reached RMB 2.91 billion, up 46.8% year-over-year.

Funds flowed to five areas: autonomous driving, AI chips, Robotaxi, humanoid robots, and physical AI.

On May 18, XPENG's first full-stack, self-developed, mass-produced Robotaxi rolled off the line in Guangzhou. This model uses a pure vision approach, powered by the second-generation VLA physical world model and four self-developed Turring AI chips delivering 3,000 TOPS—the highest computing power in the automotive industry.

In February, construction began on a humanoid robot mass-production base in Guangzhou's Guangtang Tech Innovation City, spanning 110,000 square meters. Target: mass production by late 2026.

He Xiaopeng's ambitions are clear: flying cars, Turring AI chips, VLA autonomous driving models, humanoid robots, IRON, Robotaxi... The company that once dominated with the G3 now races across multiple capital-intensive fronts simultaneously.

But cash reserves evaporated by RMB 5.6 billion in Q1, dropping from RMB 47.7 billion to RMB 42.09 billion. At this burn rate, how long can the cash last?

4. Overseas Surge: European Sales Boom Brings Joy and Concern

XPENG delivered 6,968 units in Europe during Q1, a 179% year-over-year surge. April sales hit a record 3,500-4,000 units, nearly tripling year-over-year.

In Denmark, the G6 surpassed the Tesla Model Y to rank among the top 10 new vehicle sales. Across Nordic markets, XPENG outperformed BYD and MG to become China's best-selling automaker abroad.

He Xiaopeng aims for sustained monthly overseas sales exceeding 10,000 units by Q4, with overseas sales accounting for half of total volume within five years.

But production bottlenecks loom. All European XPENG models are currently contract-manufactured by Magna Steyr in Graz, Austria. When sales explode, contract manufacturing exposes cost and quality control risks.

Acquiring Volkswagen's European factories would address both capacity constraints and manufacturing autonomy. However, this requires massive funding—which XPENG currently lacks due to losses.

5. Five Major Risks

1. Capital Chain Risk.

Persistent losses erode cash reserves, while tightening financing conditions create liquidity pressures. The 58% surge in short-term borrowing serves as a warning.

2. Multi-Front Operational Risk.

Simultaneously advancing Robotaxi, humanoid robots, flying cars, overseas factories, and new models scatters resources, with each front demanding enormous investment.

3. Volkswagen Partnership Dependency Risk.

Is technology licensing revenue recurring or one-off? If Volkswagen struggles, can partnership income sustain?

4. Overseas Expansion Underperformance Risk.

Potential escalation of European trade barriers, quality/cost risks from contract manufacturing, and capital expenditure pressures from self-built factories.

5. Sales Target Failure Risk.

The 550,000-unit annual target appears increasingly unattainable. Missing full-year delivery goals would deal a double blow to valuation and financing capabilities.

-END- Disclaimer: This article is based on the public company attributes of listed companies and core information disclosed according to their legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms). Shiyu Xingkong strives for fairness in content and viewpoints but does not guarantee accuracy, completeness, or timeliness. The information and opinions expressed herein do not constitute investment advice, and Shiyu Xingkong assumes no responsibility for any actions taken based on this article. Copyright Notice: This article is original content by Shiyu Xingkong and may not be reproduced without authorization.

-

![]()

MiniMax Faces an Uphill Battle to Reclaim Its Initial Vision

-

![]()

Is XPENG Lagging Behind the Industry Leaders?

-

![]()

The Various Aspects of Life in the Era of Involution: Six New Forces Strive to Find Profit Points

-

![]()

AI Reshapes Globalization: New Opportunities for Chinese Enterprises Going Global

-

![]()

Across-the-Board Decline: Joint Venture Brands Feel the 'Boomerang' Effect

-

![]()

The More the US Attempts to 'Suppress' China, the More Innovative Chinese Automakers Grow?

-

![]()

CCTV, People’s Daily, and Other Media Outlets Weigh In: Is a Weight-Based Tax for Electric Vehicles on the Cards?

-

Lenovo Aims to Continue Spinning Its AI Narrative