The Ripple Effect of the AI 'Chip Grab': How Skyrocketing Automotive-Grade Storage Chip Prices Are Fueling New Energy Vehicle Price Increases

06/11 2026

06/11 2026

514

514

As the traditional fuel vehicle market rolls out massive sales promotions with discounts surpassing 20%, the automotive industry had widely anticipated a fresh wave of price cuts for new energy vehicles (NEVs) in 2026. However, the current market dynamics are defying those expectations. Despite a decrease in battery costs, consumer car prices are stealthily climbing. This time, the primary driver behind the price hikes isn't batteries or steel, but automotive-grade storage chips—components that most consumers can't even name.

According to UBS's latest research report, the surge in storage chip prices has emerged as the most significant cost pressure for the automotive industry in 2026, even outpacing the previous spike in battery raw material costs. As of early June, the chip price escalation, which began in March, has already permeated the consumer market. Over a dozen domestic NEV manufacturers have sequentially raised their prices or tightened purchase incentives, signaling that a capacity crunch sparked by the AI sector is now reverberating through the automotive industry.

▍Cost Pressure Transmission: From Chip Surge to Consumer Market

Since March 2026, global automotive-grade storage chip prices have witnessed a rare upward trajectory, with the magnitude and speed of the increases far exceeding industry forecasts. Reports from CCTV Finance and Huanqiu reveal that within just three months, from March to June 2026, the overall price of domestic automotive-grade storage chips has soared by 180%, with some high-end models experiencing even more staggering hikes.

This price surge directly translates into higher vehicle manufacturing costs. In the era of intelligent connectivity, NEVs have transformed from mere transportation tools into "data centers on wheels," with storage chip usage and cost proportions skyrocketing. High-level autonomous driving demands processing massive data streams from radars and cameras, while intelligent cockpits for navigation and entertainment also heavily rely on storage. UBS's research report highlights that a high-level intelligent driving vehicle now utilizes over 5,000 chips, with storage chips accounting for 8% to 20% of the vehicle's selling price.

Without automotive-grade storage, many intelligent functions simply cannot operate. Traditional fuel vehicles require only a minimal amount of basic storage to support vehicle operation. In contrast, high-end NEV models equipped with LiDAR, high-computing-power intelligent driving platforms, high-definition maps, and multi-screen intelligent cockpits consume 4 to 8 times more storage chips per vehicle than basic entry-level models.

In terms of actual cost changes, the storage cost per vehicle for mid- to high-end models has risen from $40-$90 in the early stages to $90-$220 currently. For top-tier intelligent models equipped with urban NOA (Navigate on Autopilot) and on-device large models, the storage cost per vehicle has even surpassed $500.

Based on these calculations, the two main types of storage chips, DRAM and NAND Flash, alone added RMB 7,000 to RMB 10,000 to the cost of each NEV in the first quarter of 2026. When factoring in the simultaneous price increases of other automotive-grade chips, such as MCUs and power semiconductors, the total cost for most NEVs has risen by over RMB 10,000 compared to 2025. For an industry already operating on thin profit margins, such cost pressures are nearly impossible for automakers to fully absorb internally and are inevitably partially passed on to the consumer market.

Price Adjustment Strategies of Select Automakers

As of mid-May 2026, several domestic NEV manufacturers have already adjusted their prices or tightened terminal incentives. Price increases are primarily concentrated in the RMB 2,000 to RMB 6,000 range, while high-level intelligent driving option packages have generally seen increases exceeding 20%. Notably, in this round of price hikes, models with higher levels of intelligence have experienced greater price increases, while entry-level pure electric and plug-in hybrid models have been relatively less affected. Meanwhile, the fuel vehicle market is moving in the opposite direction, with most fuel vehicle brands increasing their discounts and promotions, and some models seeing terminal price reductions approaching 30%.

▍AI Capacity Siphoning: A Key Variable

The primary reason for the current surge in storage chip prices lies in the global capacity being siphoned off by the AI sector. Statistical data reveals that HBM (High Bandwidth Memory) usage in AI clusters has surged 1,800-fold over the past three years, with overall HBM usage in AI systems increasing 65-fold. The amount of HBM per AI chip has increased sevenfold, and the storage usage per cutting-edge AI training cluster now exceeds the total global HBM production in 2020.

Samsung, SK Hynix, and Micron, the three global storage giants, monopolize over 90% of the market share, and their capacity allocation decisions directly dictate global storage chip price trends. Starting from the second half of 2025, the global AI server market has experienced explosive growth, driving exponential demand for HBM high-bandwidth memory.

As the core component of AI servers, HBM boasts profit margins as high as 85% to 90%, far exceeding those of automotive-grade storage chips. To pursue these ultra-high profits, the three major manufacturers have, since the second half of 2025, allocated 70% to 80% of their advanced wafer capacity to AI server-specific HBM and high-end DDR5 products. Consequently, the capacity for automotive-grade storage chips, which offer low profits and small demand volumes, has been continuously squeezed, widening the industry's supply-demand gap.

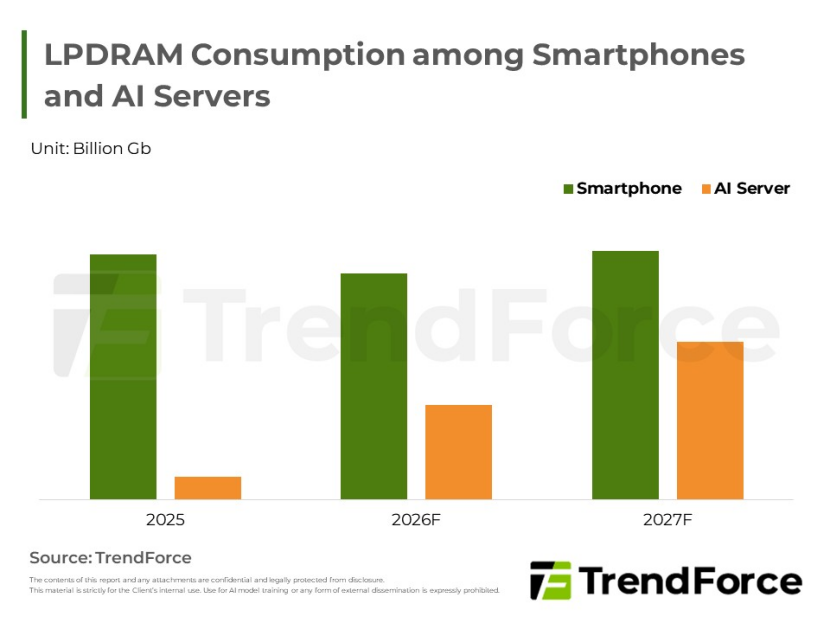

TrendForce's forecast data indicates that by 2028, server-side demand will account for 59% of global DRAM capacity, while smartphone and PC shares will shrink to 19% and 5%, respectively. Consumer electronics and the automotive industry have been relegated to the bottom of the supply chain, forced to purchase high-priced chips on the spot market. Terminal product price hikes, specification reductions, and declining shipments have become inevitable trends, ushering the entire industry into a new normal of "higher prices and reduced volumes."

As an industry insider aptly put it, "AI server orders are worth billions of dollars, while automakers' orders barely register on the radar of the big three." The automotive industry has little leverage and can only passively accept price increases and extended delivery cycles. Currently, the delivery cycle for automotive-grade storage chips has lengthened from 1-2 months to 6-12 months, with "chip shortages" once again becoming a frequently mentioned term in the industry post-pandemic.

Meanwhile, the automotive industry's own demand for storage chips continues to grow rapidly, with the rapid expansion of intelligent NEVs further exacerbating the "chip shortage." With the large-scale adoption of 800V high-voltage platforms, the rapid rollout of urban NOA functions, and the standardization of V2X (Vehicle-to-Everything) communication modules, the demand for storage capacity per vehicle is growing at an annual rate of over 30%. This severe imbalance between supply and demand ensures that the upward trend in storage chip prices will be difficult to reverse in the short term.

However, advancements by domestic storage manufacturers offer a glimmer of hope. In recent years, domestic companies such as Yangtze Memory Technologies (YMTC), GigaDevice, and ChangXin Memory Technologies (CXMT) have made significant strides in the storage chip sector, gradually breaking the monopoly of overseas giants. Data shows that as of April 2026, China's overall self-sufficiency rate for automotive chips (including storage, computing, and power) is approximately 25%, but advanced products such as high-end LPDDR5X and UFS4.0 still rely on imports, with an import dependency exceeding 70%.

Currently, domestic manufacturers are accelerating the research, development, and mass production of automotive-grade products. GigaDevice, as the world's second-largest supplier of automotive NOR Flash, holds over 40% of the domestic market share, with its automotive-grade products covering more than 90% of China's autonomous vehicle manufacturers, including BYD, NIO, and XPeng.

CXMT, the only domestic company mass-producing DRAM on a large scale, has had some of its automotive-grade products certified by AEC-Q100 and successfully entered the supply chains of automakers such as BYD and NIO, as well as covering terminal brands like Lenovo and Xiaomi. YMTC maintains a leading position in the 3D NAND sector, with its fourth-generation TLC 3D NAND based on the Xtacking architecture offering excellent storage density and I/O speed, suitable for high-bandwidth scenarios such as in-vehicle big data processing, high-definition map loading, and real-time intelligent driving data recording.

Despite the accelerating process of domestic substitution, it still cannot fully bridge the supply-demand gap in the short term. Automotive-grade chips are subject to extremely stringent certification standards and lengthy introduction cycles, with a new product typically taking 2-3 years from research and development to final mass production and vehicle integration. Industry forecasts suggest that China's domestic production rate for storage chips could exceed 30% by 2030. This means that for at least the entirety of 2026, the domestic automotive industry will continue to grapple with supply shortages and price increases for storage chips.

Given the current landscape, the wave of NEV price hikes triggered by storage chip price increases shows no signs of abating. TrendForce predicts that storage chip prices will maintain an upward trajectory throughout 2026, with the supply-demand gap unlikely to be bridged in the near term. May and June are typically stable price-protection windows for the industry, with most brands maintaining original prices for inventory models.

However, as the second half of the year approaches and inventories are depleted, a new round of price adjustments is likely to erupt comprehensively, with price increases spreading from current high-level intelligent driving models to more entry-level models. In addition to price hikes, some popular models may also face production and delivery delays due to chip shortages, further disrupting the supply-demand balance in the terminal market.

Layout 丨 Yang Shuo Image Sources: Qianku, TrendForce

-

![]()

Honda CEO Faces Vote of No Confidence Due to Alleged Neglect of China Market

-

![]()

The Flip Side of 618: New Arrivals Steal the Spotlight as Major Sales Event Hits Midpoint

-

![]()

Wang Chuanfu's Goal of Becoming the World's No.1 Relies on a 'Production Schedule'

-

![]()

Jensen Huang: The Embodiment of a Bull Market

-

![]()

Joint Interview with Five Major E-commerce Platforms: Ending Involution for a Healthier 618 Shopping Environment

-

![]()

Does It Become More User-Friendly Over Time? The Rising Product Prowess of Hunyuan Hy3 and Tencent Yuanbao's Quiet Resurgence

-

![]()

Gross Profit Margin, Supplier Payments, and Dividends Undergo 'Abrupt Shifts': Indicators of Tianbo Intelligence's IPO Performance Manipulation", "Tianbo Intelligence, gross profit margin, financial i

-

Top Ten in May Sales Rankings Feature No Fuel Vehicles: Has China’s Auto Market Undergone a Complete Transformation?