Wang Chuanfu's Goal of Becoming the World's No.1 Relies on a 'Production Schedule'

06/11 2026

06/11 2026

341

341

Challenging Toyota.

Original content from Autopix (ID: autopix)

On June 9th, BYD held its 2025 annual shareholder meeting at its headquarters in Pingshan, Shenzhen, as it does every year.

The turnout was higher than in previous years, prompting the company to temporarily move the venue from a meeting room to a larger hall typically used for product launches. Wang Chuanfu stated on stage that nearly a thousand people were present, the largest attendance in history.

During the Q&A session, a long-time major shareholder stood up, curious about the company's future direction.

In Wang Chuanfu's response, the term 'global number one' appeared for the first time. He said that BYD would continue to grow over the next three to five years and aim to become 'truly the world's number one in scale' within five years.

This meant surpassing not just new energy leaders or Chinese rivals, but achieving the largest overall vehicle sales volume, including Toyota, Volkswagen, Hyundai-Kia, and others.

At the time, BYD was experiencing its most significant slowdown since the new energy era began. In the first five months of 2026, BYD sold 788,000 vehicles domestically, a 43.3% year-on-year decline. The Chinese market could no longer provide the same growth momentum as before.

Thus, Wang Chuanfu's goal was clearly aimed at overseas markets.

Examining BYD's actions over the past two to three years, this goal is not surprising. Its approach no longer resembles that of a company merely seeking a foothold overseas.

01

BYD Aims to Capture Toyota's and Hyundai's Core Markets

To understand how far BYD is from its goal, we must first examine the gap.

Today, the world's top automaker is Toyota, selling just over 10 million vehicles annually. BYD sold 4.6 million vehicles in 2025, ranking sixth globally. The gap exceeds five million vehicles, roughly equivalent to building another BYD at its current scale.

Most of this additional volume will not come from the domestic market.

In 2025, China's new energy vehicle penetration rate reached 53.9%, nearing its ceiling. BYD's domestic sales declined compared to 2024, dropping by around 300,000 units.

With Geely, Chery, and Changan closing in, the domestic market is nearing saturation, leaving limited room for further growth. The growth gap has shifted overseas, where the global new energy penetration rate remains just over 11%.

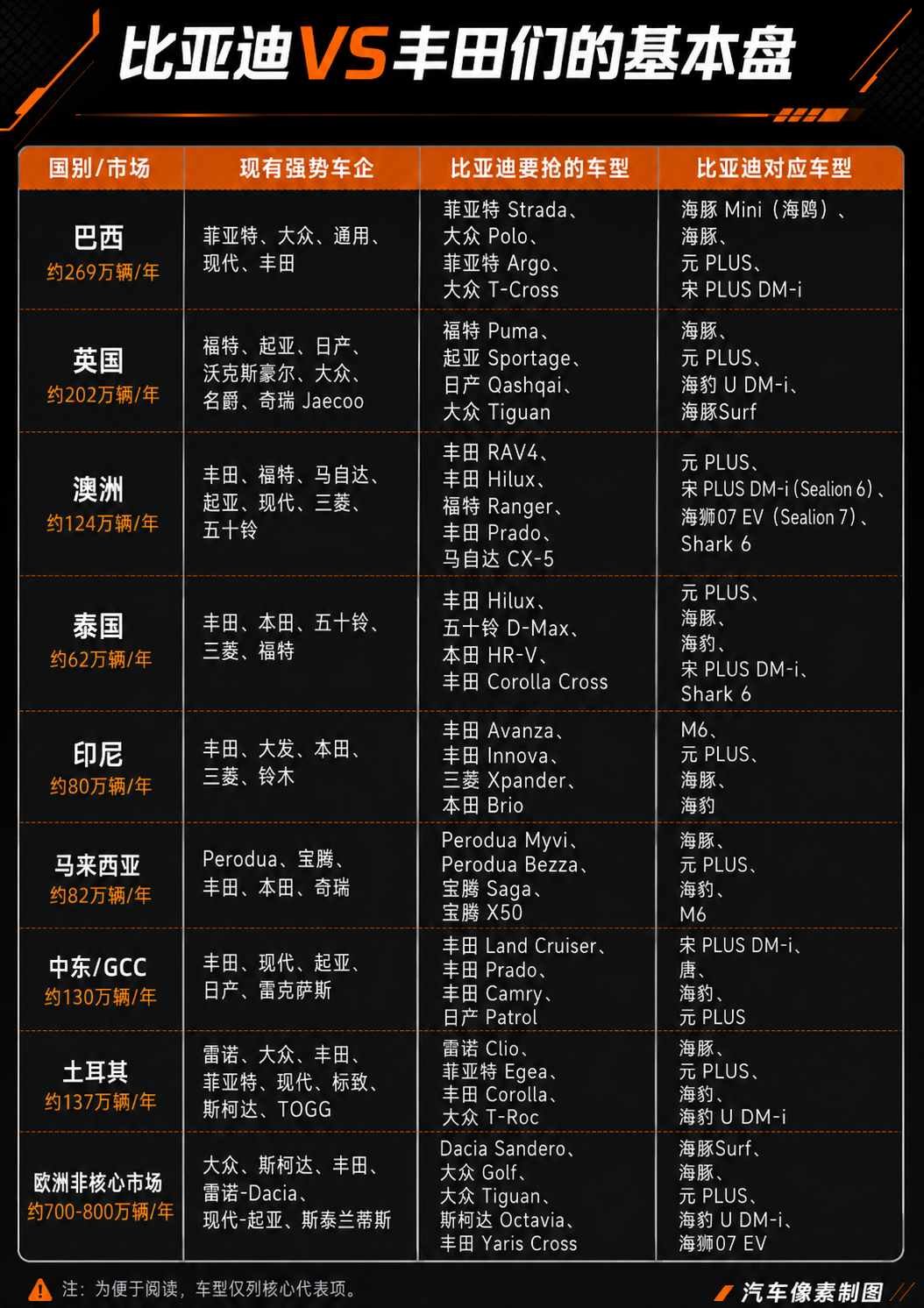

However, 'overseas' is not a monolithic market. The most lucrative segments are precisely those BYD struggles to enter. The United States uses tariffs and regulatory barriers to protect its largest and most profitable market. Japan and South Korea are strongly defended by local brands, while India uses high tariffs and entry barriers to keep Chinese vehicles out.

The remaining viable markets include South America, Southeast Asia, Central Asia, Australia, the UK, Gulf countries, and parts of Europe and Mexico. These markets are smaller, requiring heavier market share commitments in each.

Moreover, none of these open markets are vacant.

Southeast Asia is Toyota's home turf, where it holds nearly 40% market share. BYD only recently cracked the top three in Thailand. Australia is even more extreme, with Toyota leading sales for 23 consecutive years, selling two and a half times more than the runner-up. Gulf countries are dominated by Toyota and Hyundai-Kia, with Toyota leading in Saudi Arabia, the UAE, and Oman.

Only in Brazil does Stellantis, Volkswagen, Hyundai-Kia, and Renault hold sway.

Listing the owners of these markets reveals a recurring pattern: Toyota appears most frequently, followed by Hyundai-Kia, and then European automakers like Volkswagen and Stellantis.

Thus, BYD's targeted overseas markets represent a specific inventory (existing market share) built by Japanese and Korean automakers over decades with gasoline-powered vehicles.

What BYD truly aims to replace are models like the Toyota RAV4, Corolla, Hyundai Elantra, and Creta—affordable, durable vehicles that have sold for decades. BYD plans to substitute these with its DM-i plug-in hybrids and blade battery-powered EVs, vehicle by vehicle, in the most popular price segments of each market.

Stripped down, the slogan 'global number one' translates to a simpler proposition: BYD must capture decades of market share from Toyota and Hyundai-Kia in their core markets.

This will be a brutal battle. What are its chances?

02 Wang Chuanfu Frames Growth as a Production Schedule

When asked how BYD would move from sixth to first place, Wang Chuanfu's habit is to reframe the question as a supply-side calculation.

On June 9th, he spoke more about production capacity than markets. He stated that annual vehicle sales depend on battery production capacity. The second-generation blade battery's output is ramping up monthly, adding 20,000 to 30,000 units per month. Full-scale capacity release is expected by 2027, when domestic and overseas sales will surge simultaneously.

A question that should have focused on markets and products was instead explained in terms of 'how much I can produce.' In his narrative, demand seems implicitly sufficient, with bottlenecks lying in production lines.

Wang Chuanfu appears to believe that if the technological trajectory of China's new energy vehicle market repeats overseas, all remaining challenges can be addressed through production schedules.

This mindset explains BYD's overseas layout (strategic layout ) over the past two years.

BYD has at least six factories under construction or planned overseas. The Camacari plant in Brazil, repurposed from a former Ford factory, began production in July 2025 and aims for 300,000 units annually by the end of 2026. The Thailand plant launched in 2024 with 150,000 units of annual capacity. The Szeged plant in Hungary doubles as its European headquarters, while a $1 billion investment in Turkey may be delayed. Uzbekistan and Indonesia also have facilities.

BYD's approach is a bet on speed.

Looking back at BYD's domestic rise, it succeeded through technological leadership. In 2021, its fourth-generation DM-i plug-in hybrid achieved price parity with gasoline vehicles while offering lower fuel consumption. The blade battery simultaneously addressed safety and cost concerns, boosting plug-in hybrid sales from 270,000 to over 2 million units in two to three years.

During that period, China's new energy vehicle market was largely untapped. Whoever first offered affordable, high-quality EVs could capture entire market segments.

This strategy persists today. At this year's shareholder meeting, Wang Chuanfu said, 'I spend about half my week swimming in the ocean of technology,' identifying himself as 'one of BYD's 120,000 engineers.'

However, this approach no longer translates as smoothly into sales. Rivals like Geely, Chery, and Leapmotor are catching up. DM-i is no longer unique, nor is fast-charging technology exclusive to BYD.

As technologies become more homogeneous and approach physical limits, each incremental improvement yields diminishing sales returns.

The overseas market is different. Outside China, new energy vehicles remain at the stage BYD faced years ago: low penetration, few quality models, high prices, and dominance by gasoline vehicles.

The technological curve that elevated BYD to sixth place globally has barely begun to rise overseas. BYD aims to position itself advantageously before this curve steepens, replicating its domestic success on a larger scale.

This explains the urgency and heaviness of BYD's overseas strategy. The company believes the window of opportunity is limited. Once overseas new energy vehicle markets mature, competitors will flood in as they did domestically, leaving little time for first-movers.

BYD refuses to wait for markets to mature or surrender initiative to others.

In June, foreign media reported that BYD was considering acquiring an old European factory, having inspected 'numerous plants' and held discussions with automakers including Stellantis.

BYD prefers independently operated factories, targeting brownfield sites that can be quickly renovated and operated with clear ownership and operational boundaries, rather than becoming entangled in existing joint ventures, leases, or multi-stakeholder structures with European automakers.

BYD seeks to control key factories, supply chains, distribution, and branding to maximize efficiency and speed. It prefers a fast decision-making chain over risk-sharing partners.

The Brazil factory, repurposed from an old site, went from construction to first vehicle rollout in just 16 months. For exports, BYD operates a fleet of six to eight ships to control logistics. In Thailand, it acquired a local distributor; in Latin America, it partnered with a dealership group operating over 100 stores. In the UK, authorized dealerships grew from 52 to 125 in a year, and it signed a 100,000-unit order with Uber.

Following this logic, BYD's overseas actions form a coherent strategy. Wang Chuanfu advocates a replicable template, which is why he responds to sales questions with 'production schedule' logic.

Its validity hinges on a fundamental assumption: the technological curve that drove rapid market growth in China over the past few years will follow a similarly steep trajectory in many overseas markets in the coming years.

If this assumption holds, simplifying the challenge to a production schedule is the fastest solution.

03 BYD vs. Geely: Different Overseas Gambling Strategies

A common misconception is that BYD's overseas expansion is simply 'more aggressive' than Chery's or Geely's.

In terms of aggressiveness, all three are comparable. In overseas volume, Chery sold 1.34 million vehicles in 2025, nearly 300,000 more than BYD, maintaining its two-decade-plus reign as China's top passenger vehicle exporter. In terms of capital boldness, Geely has acquired Volvo, Lotus, Polestar, and formed a powertrain joint venture with Renault.

The true difference lies in the strategic assumptions behind their aggressiveness.

Chery bets on export breadth, using Vehicle export (complete vehicle exports) and Assembly of individual parts (CKD assembly) to reach underserved markets, representing a light-asset approach.

Geely bets on capital and alliances. Li Shufu acts more as an allocator, refining core capabilities in intelligence and new energy technologies while seeking partnerships for factory and channel operations.

▍Li Shufu

This year, Geely's Qianli Haohan G-ASD received EU UN R171 certification, becoming the first Chinese advanced driver-assistance system to pass this regulation, allowing its models to sell in the EU without country-by-country re-certification.

Meanwhile, Geely integrated its Gothenburg and Frankfurt R&D teams into Geely Technology Europe, aiming to reduce the time gap between Chinese and overseas model launches from over a year to under six months.

Also this year, Lynk & Co's European sales leveraged Volvo's resources, while Geely utilized Renault's networks in South Korea and South America. Gan Jiayue of Geely Automobile explained that Chinese brands should not just 'occupy' overseas markets but 'integrate' by forming local joint ventures and leveraging local resources for win-win outcomes.

These three approaches reflect three strategic assumptions and three views on where competitive moats should be built.

Geely is less urgent about technological disruption. At its 2025 fiscal year results briefing in March, Gui Shengyue, CEO of Geely Holding, said the economical passenger vehicle market might eventually be replaced by robotaxis. Shortly after, Geely became one of NVIDIA's automotive partners.

This suggests Geely does not view today's new energy competition as final. It believes the automotive industry will undergo longer-term technological reshuffles and thus prefers flexibility through partnerships and capital allocation.

Given these differences, Geely does not rush to claim 'number one' or set a five-year timeline. It is betting on the future rather than going all-in on the current new energy transition. Thus, Geely's overseas choices are nearly the opposite of BYD's, accepting slower, more dispersed, and complex approaches.

BYD aims to rapidly achieve scale through batteries, factories, shipping fleets, and channels, while Geely prefers to secure positions across technology routes, regional markets, and partnerships.

04 The Flip Side of the Production Schedule

Striving for scale to become number one is a goal, a strategic assumption, and ultimately a structural outcome.

In 2026, while Geely, Chery, Changan, and Great Wall introduced hybrid-electric vehicles to compete with Toyota's THS in markets with poor charging infrastructure, BYD was absent.

Technologically, BYD could develop such models. Chinese automakers' current HEVs do not replicate Toyota's THS. They bypass traditional strengths in engines, planetary gearsets, and long-term calibration, instead leveraging electric drivetrains—a system Chinese automakers know better. These hybrids feature smaller batteries, no external charging, and retain the low fuel consumption logic of plug-in hybrids, becoming EVs that do not require charging.

However, BYD chose not to develop such models, opting instead to invest in overseas charging infrastructure.

In March, BYD leased an 18,000-seat stadium to launch its second-generation blade battery and announced the 'Flash-Charge China, Change the World' initiative. Wang Chuanfu spoke alone for 90 minutes, extending the two-hour event to three hours. BYD set a goal of building 20,000 flash-charging stations domestically by year-end, with capital expenditures in the billions. It upgraded these stations to integrated storage-charging solutions with built-in energy storage cabinets, avoiding grid capacity upgrade requests and enabling deployment in just three parking spaces.

From year-end onward, these charging stations will begin rolling out overseas, with a megawatt-scale network already demonstrated at the Munich Auto Show.

Building charging networks in target markets represents BYD's latest and potentially most capital-intensive chapter overseas. BYD is betting that once charging networks are established, transitional technologies matter less. While competitors retain hybrids, BYD chooses not to hedge its bets, going all-in on the new energy transition.

Putting these pieces together, we can see a consistent logic: growth is achieved step by step through factories, technology, and charging stations.

BYD is almost the only domestic automaker that maintains a high degree of control over its supply chain, from vertical integration to overseas assets. This asset-heavy model makes scale a necessity, with "number one" sales being merely a byproduct in this context.

Vertical integration only pays off when scaled to a global level. Operating your own fleet requires sufficient exports to fill it; building battery cell production capacity at that scale demands enough vehicles to absorb it; investing billions to deploy 20,000 charging stations requires a sufficient vehicle base to sustain them.

Chery can remain as the export champion, and Geely can build a sizable multi-brand group, but if BYD's scale is not even larger than theirs, the efficiency of this setup cannot be guaranteed.

This gives BYD the potential to become the world's number one, making it difficult for the company to accept anything less than significant growth.

This article is original content from AutoPix and may not be reproduced without authorization.

-

![]()

Honda CEO Faces Vote of No Confidence Due to Alleged Neglect of China Market

-

![]()

The Flip Side of 618: New Arrivals Steal the Spotlight as Major Sales Event Hits Midpoint

-

![]()

Wang Chuanfu's Goal of Becoming the World's No.1 Relies on a 'Production Schedule'

-

![]()

Jensen Huang: The Embodiment of a Bull Market

-

![]()

Joint Interview with Five Major E-commerce Platforms: Ending Involution for a Healthier 618 Shopping Environment

-

![]()

Does It Become More User-Friendly Over Time? The Rising Product Prowess of Hunyuan Hy3 and Tencent Yuanbao's Quiet Resurgence

-

![]()

Gross Profit Margin, Supplier Payments, and Dividends Undergo 'Abrupt Shifts': Indicators of Tianbo Intelligence's IPO Performance Manipulation", "Tianbo Intelligence, gross profit margin, financial i

-

Top Ten in May Sales Rankings Feature No Fuel Vehicles: Has China’s Auto Market Undergone a Complete Transformation?