Gross Profit Margin, Supplier Payments, and Dividends Undergo 'Abrupt Shifts': Indicators of Tianbo Intelligence's IPO Performance Manipulation", "Tianbo Intelligence, gross profit margin, financial i

06/11 2026

06/11 2026

387

387

Introduction

Kicking off in April this year, the China Securities Regulatory Commission (CSRC) officially initiated a dedicated campaign in 2026 aimed at combating and preventing financial fraud among listed companies. Yize Finance has observed that this year's campaign focuses on regulatory objectives and strategies that emphasize "early detection, robust prevention, and streamlined mechanisms."

Figure 1: The campaign against financial fraud commenced in April this year (Source: CSRC official website)

"'Early detection' involves extending supervision to include IPO companies," a local securities regulator informed Yize Finance. "The emphasis is on overseeing and early identifying third-party collusion in fraud, utilizing AI models to monitor and detect financial data anomalies promptly."

Yize Finance learned from the Shanghai Stock Exchange (SSE) official website that the SSE Listing Review Committee is set to convene its 36th review session for 2026 on June 12, 2026, to deliberate on the initial public offering (IPO) of Tianbo Intelligent Technology (Shandong) Co., Ltd. (abbreviated as Tianbo Intelligence). The market suspects that Tianbo Intelligence has witnessed "abrupt shifts" in its gross profit margin, accounts receivable, supplier relationships, and dividends, potentially signaling significant concerns over performance manipulation and even financial fraud.

Figure 2: Tianbo Intelligence's IPO Progress (Source: SSE)

I. 'Abrupt Shift' in Gross Profit Margin of Core Products: Are Costs Being Hidden by Relatives?

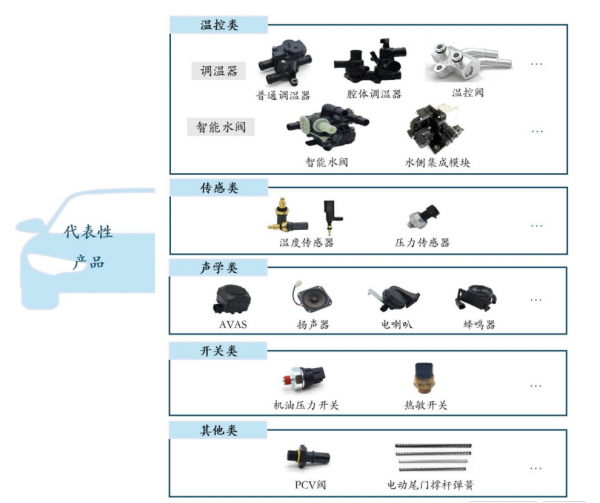

Tianbo Intelligence primarily manufactures automotive thermal management components and also ventures into automotive acoustic components. According to the prospectus, Tianbo Intelligence mainly produces four categories of products: temperature control, sensing, electro-acoustic, and switching. Temperature control products, which include thermostats and intelligent water valves (primarily electronic water valves), contribute roughly 60% of its revenue.

During the reporting period, Tianbo Intelligence's revenue from temperature control products surged, increasing by nearly 40% in 2024 compared to 2023. Thermostats, a subset of temperature control products, are mainly used in fuel vehicles, while electronic water valves are developed for new energy vehicles (NEVs). The rapid growth of NEVs has propelled the revenue increase from electronic water valves.

Figure 3: Electronic water valves are the flagship product (Source: Prospectus)

In essence, electronic water valves represent the "crux" of Tianbo Intelligence's revenue growth and its flagship product.

However, Yize Finance has observed an "abrupt shift" in the gross profit margin of electronic water valves, the flagship product.

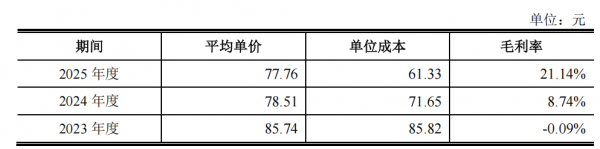

According to the prospectus, from 2023 to 2025, Tianbo Intelligence's electronic water valves generated sales revenue of RMB 98.22 million, RMB 203 million, and RMB 270 million, respectively, with their share in temperature control product revenue rising from 13% to 23%. However, Yize Finance noted that in 2023, the gross profit margin of electronic water valves was -0.09%, but by 2025, it had soared to 21%.

Figure 4: The gross profit margin of electronic water valves undergoes a 'dramatic shift' (Source: Prospectus)

Why has the gross profit margin of electronic water valves for NEV manufacturers undergone such an "abrupt shift" in just three years?

Tianbo Intelligence attributes the increase in the gross profit margin of electronic water valves to economies of scale achieved from development to mass production, along with a decrease in unit material costs, labor, and manufacturing expenses, leading to reduced costs and a significant rise in the gross profit margin. The substantial increase in the gross profit margin of electronic water valves has even boosted the gross profit margin of the company's temperature control products.

The market, however, remains unconvinced by this explanation.

While economies of scale can indeed reduce costs, this typically occurs when a product transitions from the development stage to initial production, not from established mass production to higher volumes.

In 2023, electronic water valves already generated nearly RMB 100 million in revenue, clearly indicating mass production and sales. Yet, the gross profit margin was negative and swiftly turned positive, rising to over 20%. This is not an effect that can be solely attributed to "cost reductions due to economies of scale."

Therefore, the market questions whether the secret to Tianbo Intelligence's core product, electronic water valves, "generating profits" lies not in "economies of scale" but elsewhere.

According to the prospectus, during the reporting period, the price of electronic water valves has been declining, from RMB 86 in 2023 to RMB 78 in 2025, while the gross profit margin has shifted from a loss to 20%. In other words, the unit cost of electronic water valves has decreased more than the selling price. The prospectus reveals that the unit cost of electronic water valves dropped from RMB 85 in 2023 to RMB 61 in 2025.

Figure 5: Unit price and cost of electronic water valves (Source: Prospectus)

How was this "excessive cost reduction" achieved?

Yize Finance's investigation revealed that the primary materials for electronic water valves include engineering plastics (for valve bodies, spools, gear sets), rubber (for seals), metal inserts (to enhance structural strength), springs, bearings, and electronic components (such as chips, motors, sensors).

Who are the main suppliers of raw materials for manufacturing electronic water valves? Are suppliers reducing the manufacturing costs of electronic water valves and boosting Tianbo Intelligence's gross profit margin by supplying at low or even loss-making prices? Are they transferring benefits at unfair prices to assist Tianbo Intelligence in going public? If these suspicions hold true, it would constitute blatant third-party collusion in fraud.

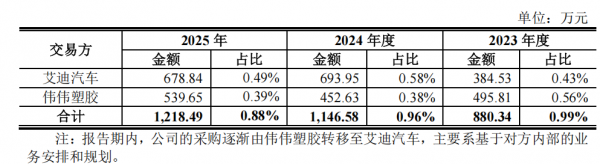

Yize Finance has taken note of Tianbo Intelligence's related party transactions.

Figure 6: Tianbo Intelligence's related party transactions (Source: Prospectus)

Tianbo Intelligence has two major regular related party transaction counterparts: Aidi Auto and Weiwei Plastics. During the reporting period, Tianbo Intelligence's cumulative purchases from Aidi Auto and Weiwei Plastics were RMB 8.8 million, RMB 11.46 million, and RMB 12.18 million, respectively. Yize Finance believes that if these related party transactions are linked to electronic water valve products, the following characteristics emerge:

First, the content of related party transactions may involve the main components of electronic water valves.

According to the prospectus, Aidi Auto and Weiwei Plastics are primarily engaged in the production, processing, and sales of rubber valves, injection-molded products, and sealing products. The main components required for electronic water valves include valves, rubber, and plastic parts.

Second, the related parties have a close relationship with the actual controller.

Yize Finance discovered that the actual controller of Aidi Auto is Lv Shiwei, the nephew of Tianbo Intelligence's actual controller, Lv Xinmin. The actual controller of Weiwei Plastics is Lv Jianguo, the sister-in-law of Lv Xinmin, with Lv Shiwei serving as a supervisor. In other words, the actual controllers of the two related parties are from Lv Xinmin's brother's family. Even when Tianbo Intelligence needs to purchase firefighting equipment, it buys from Qufu Hengji Fire Protection Company, controlled by Lv Xinmin's brother's family.

From the perspectives of procurement content and the closeness of the relationship between the related parties and the actual controller, if someone is needed to conceal costs and expenses, "Lv Xinmin's brother and his controlled company" would undoubtedly be the prime candidates.

Therefore, market analysts believe that Lv Xinmin's brother's family and their controlled companies have concealed the costs and expenses of the "electronic water valve" business, which is why the gross profit margin of the electronic water valve business has shifted from a loss to a high level in a short period.

In particular, regarding Aidi Auto, Yize Finance noted that the company once had a registered capital of RMB 20 million and possessed multiple utility model patents, as well as a trade union committee. This suggests that the company is quite capable, so it is not out of the question that the company may have even covered the manufacturing costs of electronic water valves.

II. 'Abrupt Shift' in Payment Settlement Methods: Concealing Deteriorating Receivables?

According to the prospectus, from 2023 to 2025, Tianbo Intelligence's accounts receivable were RMB 440 million, RMB 680 million, and RMB 570 million, respectively, accounting for 35%, 40%, and 29% of operating revenue. During the reporting period, the proportion of accounts receivable in operating revenue rose sharply and then fell to a low and safe level, indicating an improvement in the company's "liquidity."

However, from 2023 to 2025, the amounts of Tianbo Intelligence's accounts receivable converted into notes receivable were RMB 600 million, RMB 850 million, and RMB 1.26 billion, respectively, accounting for 48%, 50%, and 65% of main business revenue.

In other words, the decrease in the proportion of accounts receivable in Tianbo Intelligence's operating revenue is not due to an enhancement in the company's ability to collect payments but mainly due to a change in settlement methods—customers increasingly opt to settle in the form of notes rather than "direct cash payments."

What are the "benefits" of this settlement method for Tianbo Intelligence?

In Yize Finance's view, there are at least two "benefits":

First, it may extend the sales credit period and stimulate sales.

Yize Finance's research found that Tianbo Intelligence's customer credit periods are mostly 60-90 days after receiving the invoice, while the terms for notes receivable can extend to six months or even longer. Consequently, more payments being settled in the form of notes receivable actually prolongs the settlement cycle. This is naturally advantageous for customers and can incentivize them to purchase more products.

'Since there's no rush to pay, there's no downside to buying more,' an industry insider in the automotive component supply chain analyzed to Yize Finance.

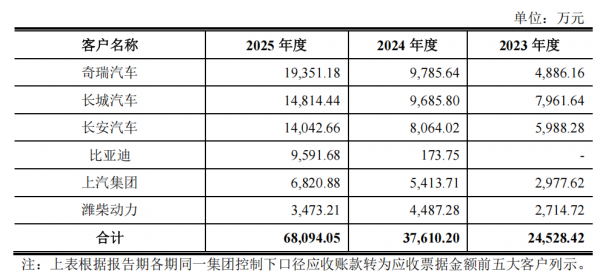

According to the prospectus, from 2023 to 2025, Tianbo Intelligence achieved operating revenue of RMB 1.27 billion, RMB 1.69 billion, and RMB 1.96 billion, with growth rates of 31%, 33%, and 16%, respectively. In particular, the purchase amounts of major customers settling with notes increased from RMB 260 million in 2023 to RMB 680 million in 2025, 2.6 times the initial amount.

The growth rate of purchase amounts by customers settling with notes far exceeds the overall growth rate of the company's revenue, sufficiently demonstrating the power of "note" settlement—it spurs an increase in purchases by some major customers.

Figure 7: Customers settling with notes (Source: Prospectus)

Second, it may beautify data and manipulate performance.

Yize Finance believes that converting a significant portion of accounts receivable into notes receivable can "beautify" performance in two ways.

If accounts receivable become overdue, bad debt provisions must be made, increasing long-term aged receivables. However, if accounts receivable are converted into notes receivable before they become overdue, medium- and long-term aged accounts receivable will decrease, making the company's ability to collect payments appear stronger to the outside world.

Yize Finance noted that from 2023 to 2024, the amount of Tianbo Intelligence's accounts receivable converted into notes receivable increased from RMB 600 million to RMB 850 million, directly causing the company's short-term (within one year) accounts receivable to surge from RMB 460 million to RMB 710 million, a growth of RMB 250 million. In other words, Tianbo Intelligence is highly likely to have classified accounts receivable that would otherwise be long-term aged (over one year) as short-term accounts receivable by settling them with notes. This makes the company's ability to collect payments appear even stronger.

'It's like having one pool of water, now divided into two, and moving the 'murky water' from one pool (accounts receivable) to another (notes receivable),' an analyst pointed out, 'allowing the outside world to see only the clean pool, while the water in the other pool is even murkier.'

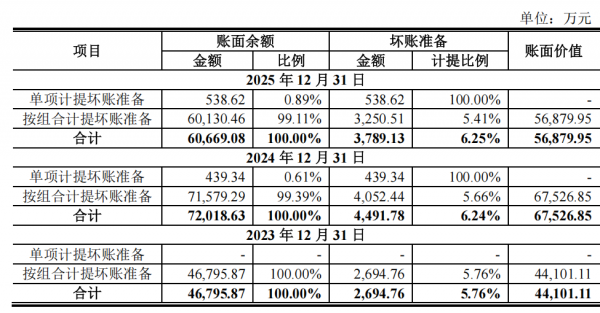

Figure 8: Tianbo Intelligence's bad debt provisions (Source: Prospectus)

'Our customers settle payments for goods very promptly, basically within one year, and do not default for extended periods.'

The reality may be quite the opposite.

Yize Finance also observed that notes receivable generally do not necessitate bad debt provisions, or they entail a lower provision ratio compared to accounts receivable, which require bad debt provisions based on their age. By converting accounts receivable into notes receivable, Tianbo Intelligence managed to reduce its bad debt provisions to a certain extent, thereby boosting its net profit. According to the prospectus, after converting RMB 1.26 billion of accounts receivable into notes receivable in 2025, Tianbo Intelligence's bad debt provisions decreased from RMB 44.91 million in 2024 to RMB 37.89 million.

This reduction clearly contributed to an increase in net profit. In 2025, Tianbo Intelligence's net profit attributable to shareholders rose from RMB 280 million to RMB 350 million.

Considering the above, it is not hard to see that, under the pressure of "annual price reductions," how can the company ensure increased sales, timely receipts, and a low default rate?

Therefore, Tianbo Intelligence has resorted to "tricks" by altering the payment settlement method to notes receivable. This not only boosts sales but also enhances the appearance of data emphasized in IPO reviews, such as the "proportion of accounts receivable," "aging distribution," and "bad debt provisions."

However, it is crucial to remember that such "good looks" are merely "beautified" and not genuine. Once facing investors directly, this could potentially harm investor interests.

III. 'Sudden Change' in Supplier Loans: A Sign of Tunneling?

Tianbo Intelligence was restructured from a collective enterprise, Qufu Auto Parts Factory, and its actual controller is Lv Xinmin, the former factory director of Qufu Auto Parts Factory. Yize Finance has noticed that many of Tianbo Intelligence's major suppliers are automotive component enterprises based in Qufu and have relatively close ties with the actual controller, Lv Xinmin, and his son, Lv Yawei.

This raises questions—are there local suppliers in Qufu selling products to Tianbo Intelligence at unfair prices, thereby transferring benefits? Or are they covering costs and expenses for the issuer? Or is the actual controller siphoning funds from the issuer?

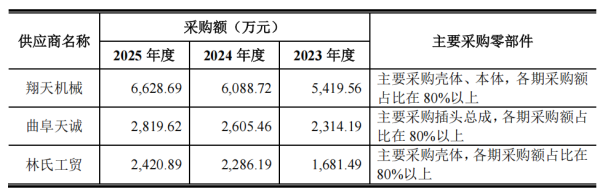

Take the major supplier Qufu Tiancheng as an example.

Figure 9: Local suppliers in Qufu (Source: Response Document)

"Yize Finance" discovered that the actual controller of Qufu Tiancheng is Niu Xiaojun. Niu Xiaojun and Yu Kenan, the actual controller of Qufu Tianze, jointly invested in Yueqing Tianshun Auto Parts Factory. Yu Kenan and Lv Xinmin jointly established Yueqing Luqu Auto Parts Manufacturing Co., Ltd. Yu Kenan actually controls several auto parts enterprises, such as Qufu Tianshun and Wenzhou Tianshun. These enterprises primarily produce products like thermostats and sensors, which are similar to Tianbo Intelligence's business.

From this, it can be inferred that through Yu Kenan's introduction to Lv Xinmin, Qufu Tiancheng entered Tianbo Intelligence's supplier list and became one of its top five customers. For Lv Xinmin, Qufu Tiancheng is a business associate introduced by his peer, Yu Kenan.

Figure 10: Equity Relationship between Qufu Tiancheng and Tianbo Intelligence (Source: Aiqicha)

Take another major supplier also located in Qufu, Lin's Industrial and Trading, as an example.

The response document shows that during the reporting period, Lin's Industrial and Trading mainly sold housings to Tianbo Intelligence, with 80% of its sales going to Tianbo Intelligence, accumulating sales of over RMB 60 million. The supervisor of Lin's Industrial and Trading, Lin Yuanyuan, once served as the supervisor of Shandong Zhonghan Precision Machinery Manufacturing Co., Ltd. Zhonghan Precision and the first major supplier jointly invested in a company. Zhonghan Precision's main business is the manufacturing and processing of precision metal parts, and its legal representative is Yao Kun.

Figure 11: Association between Lin's Industrial and Trading and the First Major Supplier (Source: Aiqicha)

Another example is Suzhou Wutong Intelligence.

Suzhou Wutong Intelligent Electronics Co., Ltd. is one of Tianbo Intelligence's top five suppliers. In 2024 and 2025, its sales to Tianbo Intelligence both exceeded RMB 40 million. The Aiqicha platform shows that the parent company of Wutong Intelligent Electronics is Wutong Holdings, and its legal representative, Wan Weifang, has equity investment associations with Tianbo Intelligence's actual controller, Lv Xinmin.

Figure 12: Association between Wan Weifang and Lv Xinmin (Source: Aiqicha)

Analyzing several major suppliers of Tianbo Intelligence raises two significant questions:

First, why are there always 'larger potential suppliers' behind Tianbo Intelligence's core suppliers?

Such as Qufu Tianze and Wenzhou Tianshun behind Qufu Tiancheng; Zhonghan Precision behind Lin's Industrial and Trading. These 'larger potential suppliers' are in the same industry as Tianbo Intelligence. Do their products flow to Tianbo Intelligence?

Second, why are the actual controllers of the suppliers so closely related to Tianbo Intelligence's actual controller, Lv Xinmin?

Such as Niu Xiaojun, Yu Kenan, Lin Yuanyuan, Wan Weifang, etc. Does the 'transaction + personal relationship' model affect the fairness of transactions? Are there any instances of cost padding and benefit transfers?

Another concerning point about the relationship between Tianbo Intelligence and several major local suppliers in Qufu is that several suppliers have borrowed funds from Tianbo Intelligence.

A typical example is Qufu Tianze.

In 2022, it borrowed RMB 7.23 million from Tianbo Intelligence and repaid the principal and interest in two batches in 2024 and 2025.

Another example is Qufu Kangli Electromechanical.

At the end of 2022, it borrowed RMB 2.5 million in two loans and repaid the principal and interest one year later. Both companies are suppliers of Tianbo Intelligence.

There is also Qufu Zhengtong Instrument Accessories, which borrowed RMB 150,000 in 2022 and repaid the principal and interest in 2025.

What does it indicate when several local suppliers in Qufu borrow and repay funds in a short period? Does it point to the concealment of cost padding or benefit transfers through short-term fund lending?

IV. Does the 'Sudden Change' in Dividends Before the IPO Challenge Regulatory Boundaries?

"Yize Finance" noted that Tianbo Intelligence has made substantial dividend payments during the reporting period.

In 2023, Tianbo Intelligence paid cash dividends of RMB 558 million, and in 2024, it continued to pay dividends of RMB 36.49 million, accumulating nearly RMB 600 million in dividends during the reporting period. Particularly in 2023, the company's net profit attributable to shareholders was RMB 220 million, with dividend payments being 2.5 times the net profit; the net cash flow from operating activities was RMB 170 million, with dividend payments being 3.3 times the annual net cash flow.

Figure 13: Tianbo Intelligence has made large dividend payments (Source: Prospectus)

In other words, in 2023, Tianbo Intelligence distributed all the cash on its books to shareholders.

'Approaching the listing with a clean slate and empty pockets.'

"Yize Finance" noted that after the new 'National Nine Articles,' regulators have set two red lines for dividend payments by IPO companies. First, liquidation-style dividends are not allowed, with the cumulative dividend amount not exceeding 80% of the net profit for the same period; second, 'dividends followed by capital raising' are not allowed. If the cumulative dividend amount for the reporting period exceeds 50% of the net profit for the same period, and the cumulative dividend amount exceeds RMB 300 million, and the proportion of funds raised for supplementing working capital and repaying bank loans exceeds 20%, it also touches the red line and listing is not allowed.

Does Tianbo Intelligence touch the above two red lines?

First, check the first line.

During the reporting period, Tianbo Intelligence paid cumulative dividends of RMB 594 million, with a total net profit attributable to shareholders of RMB 786 million for the same period, a ratio of 75.57%. This value is below 80%, so it does not touch the first red line.

'It didn't touch the red line, but it has a strong implication of challenging it, almost paying dividends right at the line,' an investor told "Yize Finance."

Next, check the second line.

Tianbo Intelligence's cumulative dividends exceed the 50% red line of net profit, and the dividend amount also exceeds the RMB 300 million red line. However, Tianbo Intelligence has not arranged any projects to supplement working capital, so it does not touch the second red line.

'Although there are no projects to supplement working capital, there is idle production capacity, so it cannot be ruled out that the company will change the use of funds after listing,' an analyst pointed out.

"Yize Finance" also noted that Tianbo Intelligence plans to raise RMB 2.057 billion in this IPO, primarily for four projects. The prospectus shows that in 2025, the capacity utilization rates of Tianbo Intelligence's core products, including thermostats, intelligent water valves, temperature sensors, and AVAS, are 94%, 97%, 101%, and 92%, respectively. Only the temperature sensors are overloaded, while other products have idle capacity. Given the existing capacity, the urgency and necessity of raising substantial funds for expansion are questionable.

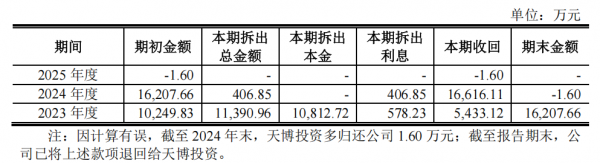

"Yize Finance" also noted that during the reporting period, the controlling shareholder borrowed large amounts of funds from Tianbo Intelligence, accumulating nearly RMB 120 million. The sources of repayment mainly include dividends, property transfers, and bank loans. Particularly noteworthy are dividends and property transfers.

Figure 14: Large-scale Fund Borrowing by Tianbo Investment (Source: Prospectus)

Some investors have raised doubts: on the one hand, the controlling shareholder relies on a large proportion of shares to 'siphon' funds from Tianbo Intelligence through dividends; on the other hand, the controlling shareholder and actual controller transfer 'illiquid assets' such as 'employee dormitories' and 'offices' to Tianbo Intelligence in exchange for 'hard cash.'

'At the IPO stage, they are already heavily taking advantage of the listed company's earnings. After listing, they will only become more aggressive and unscrupulous, leaving little chance for small and medium investors to make money,' an investor said angrily.

Conclusion

Tianbo Intelligence's products are primarily used in fuel vehicles. Over the past three years, fuel vehicle sales have continuously declined. Particularly this year, it is expected that fuel vehicle sales will decline by more than 50% year-on-year.

However, Tianbo Intelligence has experienced sustained sales growth, significant net profit growth, continuous scale expansion, and can still maintain an average gross margin of 30%.

Using an inappropriate metaphor, Tianbo Intelligence is like a 'delicate flower blooming in a barren land.'

And such a flower, lightly spined at best, and poisonous at worst.

-

![]()

Honda CEO Faces Vote of No Confidence Due to Alleged Neglect of China Market

-

![]()

The Flip Side of 618: New Arrivals Steal the Spotlight as Major Sales Event Hits Midpoint

-

![]()

Wang Chuanfu's Goal of Becoming the World's No.1 Relies on a 'Production Schedule'

-

![]()

Jensen Huang: The Embodiment of a Bull Market

-

![]()

Joint Interview with Five Major E-commerce Platforms: Ending Involution for a Healthier 618 Shopping Environment

-

![]()

Does It Become More User-Friendly Over Time? The Rising Product Prowess of Hunyuan Hy3 and Tencent Yuanbao's Quiet Resurgence

-

![]()

Gross Profit Margin, Supplier Payments, and Dividends Undergo 'Abrupt Shifts': Indicators of Tianbo Intelligence's IPO Performance Manipulation", "Tianbo Intelligence, gross profit margin, financial i

-

Top Ten in May Sales Rankings Feature No Fuel Vehicles: Has China’s Auto Market Undergone a Complete Transformation?