Could BYD Achieve the Title of 'World's Largest Automaker' by 2030?

06/15 2026

06/15 2026

544

544

At BYD's 2025 Annual Shareholder Meeting on June 9, Wang Chuanfu, the company's chairman, articulated an ambitious vision: to become the "world's largest automaker" by 2030. He also called for investors' patience, a statement that has since ignited widespread discussion across the industry.

First, let's set the scene. BYD's Hong Kong-listed shares have plummeted by 33% year-to-date, dropping from HKD 132.2 to HKD 88.40. This decline mirrors a broader downturn in the automotive sector.

Readers of our previous article, "Morgan Stanley's 2026 China Auto Market Forecast: Navigating the End of 'Growth Inertia'," will recall the industry's "darkest hour" in early 2026. During this period, a halved purchase tax policy spurred a surge in demand, effectively pulling forward sales.

Fortunately, BYD's sales began to rebound on a month-by-month basis from March to April. By May, wholesale volumes had reached 383,000 units, marking a slight year-on-year increase of 0.26% and ending eight consecutive months of decline.

So, is BYD's goal of becoming the "global leader" by 2030 a mere rallying cry or a credible commitment?

BYD's Comprehensive Technological Strategy

To evaluate this, we must first examine the strategic cards Wang Chuanfu holds. At the shareholder meeting, BYD showcased its decade-long technological prowess in electric powertrains, batteries, and intelligent systems.

The second-generation Blade Battery, featuring ultra-fast charging capabilities, represents BYD's bid to dominate the "second half of electrification" by addressing range anxiety—the final hurdle for pure electric vehicles (EVs). Following its launch, domestic and international orders surged, although current production capacity remains at 20,000-30,000 units per month. Management aims to ramp up production to full capacity by 2026 and establish a "global ultra-fast charging network" by 2027, partnering with Sinopec for energy infrastructure. Notably, BYD is opening its ultra-fast charging technology to the entire industry—not just its own brands—with future solid-state batteries and external battery supplies also being compatible. This move, a typical "tech-driven standard-setting" gamble, aims to expand the market pie while securing BYD's position as the rule-maker.

Intelligent systems represent BYD's most ambitious yet underdeveloped area. Its ace in the hole is data: 200 million daily kilometers of driving data and over 3.15 million vehicles equipped with Level 2 (L2) autonomous driving technology on the road—a "data flywheel" that any smart driving company would envy.

Building on this foundation, BYD is pursuing full-stack self-research, from sensors and controllers to data processing. Its 4nm autonomous driving chip has already been launched, with smart driving training centers established in Europe, South America, Southeast Asia, and the Middle East. BYD targets achieving Level 3 (L3) autonomy by July 1, 2027 (pending regulatory approval), emphasizing "dual safety redundancy" for parking and urban navigation.

AI integration is another focal point: upgrading the vehicle operating system to a hybrid "AI OS" with "super intelligent agent" capabilities. BYD has assembled a 5,000-strong algorithm team with lucrative salaries, going "all in on AI" since 2023.

However, it's important to note that announcements do not equate to real technology, real technology does not necessarily translate into genuine user perception, and user needs are often shaped by brand image.

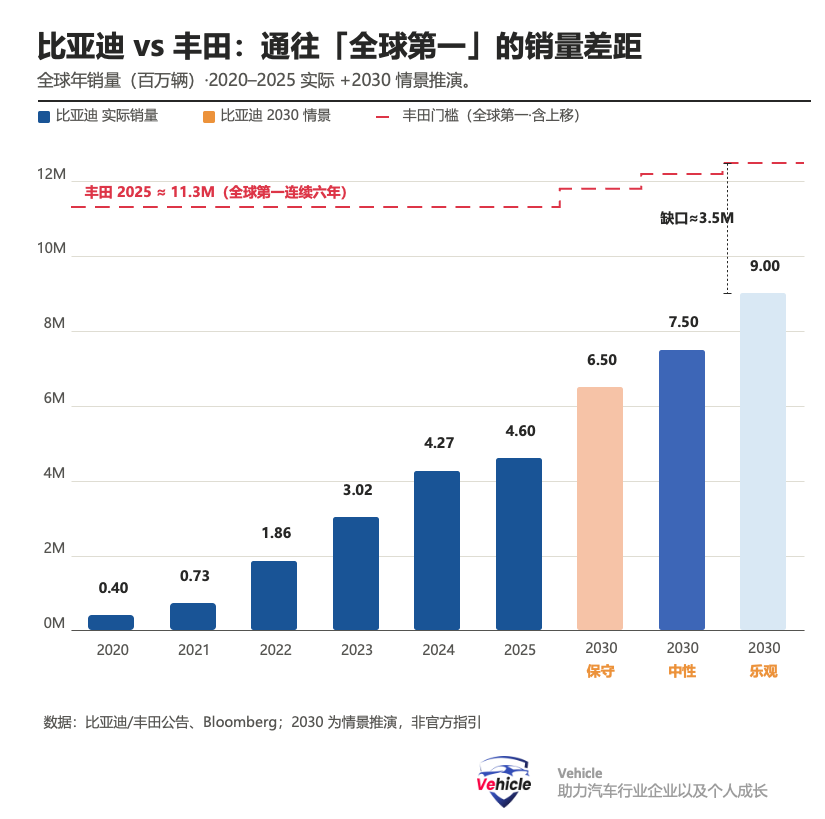

Ultimately, sales figures matter. BYD sold 4.6 million vehicles in 2025, achieving its revised target and surpassing Tesla to become the world's largest EV maker.

Yet, this 4.6 million figure was a downward revision from an initial target of 5.5 million units, representing just 7% growth—the slowest pace since 2020. According to our previous analysis, "Top 10 Global Automakers by Sales in 2025," Toyota sold 11.32 million vehicles (including Lexus, Daihatsu, and Hino) in 2025, securing its sixth consecutive year as the global leader with a 4.65% year-on-year increase. Volkswagen (8.98 million), Hyundai-Kia (7.27 million), GM (6.18 million), and Stellantis (5.48 million) followed, with BYD ranking sixth overall.

This implies that to grow from 4.6 million to approximately 11.3 million units (Toyota's level), BYD needs to achieve a compound annual growth rate (CAGR) of around 21% over five years. Yet, it just slashed its growth rate from over 40% to 7%, with negative growth likely in the second half of the year. This is the core contradiction.

Three Major Barriers

For BYD to exceed 10 million units by 2030, it must overcome at least three significant barriers:

Barrier 1: Domestic Market Saturation

Of BYD's 4.6 million 2025 sales, 1.05 million were overseas, with approximately 3.55 million sold domestically. The domestic market is now hyper-competitive:

China's total auto market (passenger + commercial vehicles) has plateaued at 23-27 million units, with new energy vehicle (NEV) penetration exceeding 50%. Regulatory crackdowns on price wars and intense competition from Geely Galaxy, Changan Deepal, and others in the core RMB 100,000-200,000 price segment limit growth. Foreign brands, though still holding a 29% market share, face shrinking margins.

In short, stabilizing domestic sales is challenging; expecting multi-million incremental growth is unrealistic.

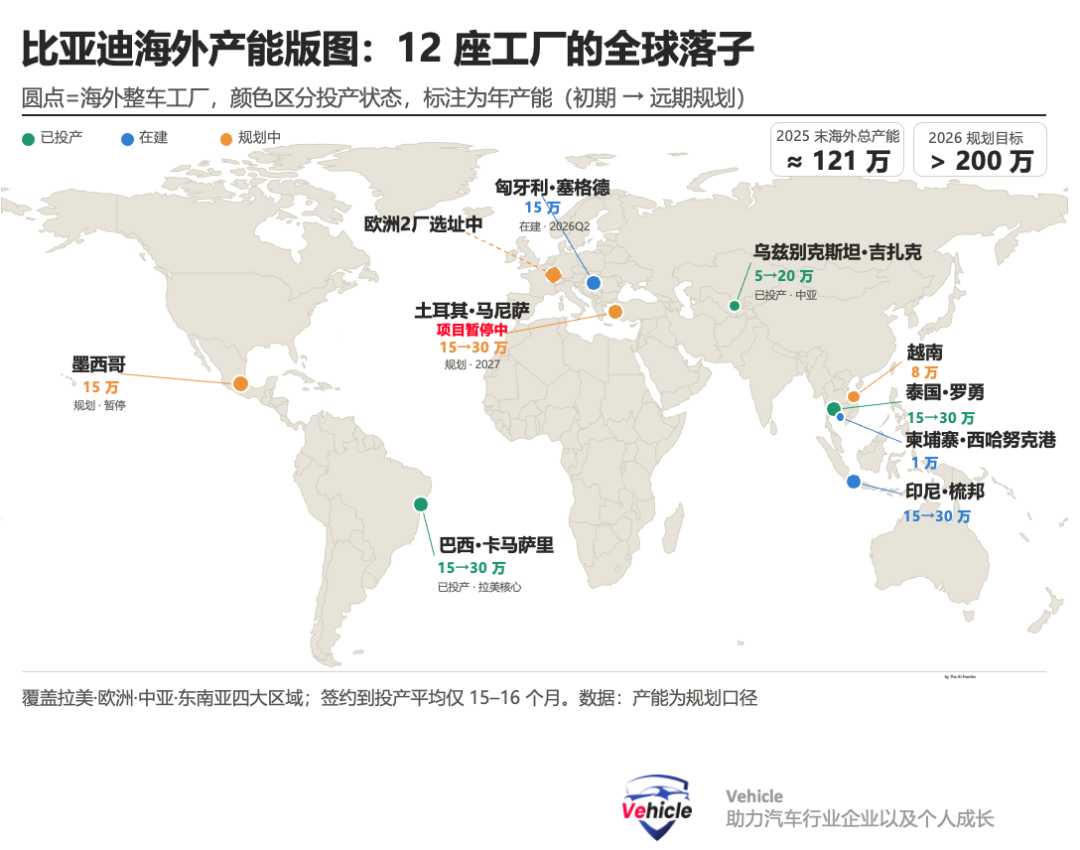

Barrier 2: Overseas Ceilings—Capacity Constraints and Tariffs

BYD's overseas performance is a bright spot—1.05 million exports in 2025 (+140% year-on-year) became a new growth engine. This year's target is 1.6 million units, likely to be exceeded. However, BYD aims for overseas sales to account for over 50% of total sales by 2030 (800,000 in 2025, 50% by 2030), implying 5 million units. Two hard constraints exist:

1. Slow capacity ramp-up: Thailand (150,000 units per year, operational), Brazil (ex-Ford, ~150,000 units per year), Hungary (~150,000 units per year), and Turkey (~150,000 units per year). Hungary's Szeged plant starts trial production in the first quarter of 2026, with initial capacity of 150,000 units (scaling to 300,000 units long-term). Turkey's plant is stalled due to geopolitical issues. Total overseas capacity: ~1.3 million units.

To reach 1 million units in Europe alone, several more plants are needed. Even if all overseas capacity runs at full tilt (~1.6 million units), a ~3 million-unit gap remains. Can exports fill this gap?

2. Tariffs and policies: The EU imposed anti-subsidy tariffs on top of the 10% base duties. As discussed in our article, "EU's Industrial Acceleration Act: Rewriting China's Auto Export Rules," European policies incentivize local production. BYD must localize to mitigate this pressure, locking it into a factory-building race. Acquiring existing brands' plants (e.g., Stellantis) becomes a priority, as seen in recent news.

Barrier 3: The U.S. Market—A Geopolitical Wall

The U.S. market presents the toughest barrier. The Department of Commerce finalized rules banning nearly all Chinese EV imports on national security grounds: software bans take effect in 2027, and hardware bans in 2029. The 2026 Connected Vehicle Security Act further bans Chinese-made vehicles and connected components. BYD sued the U.S. government over tariff overreach under the International Emergency Economic Powers Act (IEEPA), but even a win would only lower tariff thresholds—the connected vehicle ban remains. Combined with 100% complete vehicle tariffs, passenger vehicle entry is nearly impossible. Excluding a 16-million-unit market that nourished Toyota, Hyundai, and GM leaves a structural gap in BYD's global ambitions.

Scenario Analysis

Conservative (~6.5 million units): Domestic sales stabilize at 3.5 million units, exports at ~1.5 million units, and overseas capacity (Thailand/Brazil/Hungary) ramps to 1.5 million units. This is the most likely outcome, placing BYD between the global third and second place, surpassing shrinking rivals but trailing Toyota.

Neutral (~8 million units): Domestic sales grow slightly to 4-4.5 million units, exports at ~2 million units, and overseas capacity reaches 1.8 million units. This would surpass Volkswagen, securing second place but not first.

Optimistic (~9.5 million units): Domestic sales rebound to 4.5-5 million units, exports at ~2.5 million units, and overseas capacity hits 2 million units. This is BYD's ceiling scenario, approaching Toyota but remaining below 10 million units.

To truly reach the top, three conditions must align: no domestic decline, overseas production/exports surging to 5 million units, and Toyota's EV transition stalling. However, overseas growth is capped by capacity and tariffs, making this scenario highly unlikely.

Conclusion

Wang Chuanfu's "2030 Global First" vision is more of a confidence anchor and strategic rallying cry than a commitment backed by a detailed capacity roadmap (he referred to it as a "strive" target). A realistic, achievable goal is securing a top-three global position and surpassing Volkswagen in volume within five years—an unprecedented feat for a Chinese automaker.

However, three significant barriers stand in the way: a saturated and cutthroat domestic market, sluggish overseas capacity growth hampered by tariffs, and an impenetrable U.S. market.

*Unauthorized reproduction or excerpting is strictly prohibited.

-

![]()

Bridging the 'Reality-Virtuality Gap' in VLA: China's Embodied AI Large Models Grow 'New Brains'

-

![]()

Executives Exit in Style: Alibaba's AI Doesn't Need a 'Top Dog'

-

![]()

From 'Daydream' to 'Inestimable Wealth': Is SpaceX Truly So 'Sci-Fi'?

-

![]()

Zhongji Innolight and Its Peers Turned into AI Scratch Cards by Wall Street

-

![]()

Li Jie's 'High-Speed Charge' and J&T Express's 'Abrupt Halt'

-

![]()

Two Departments Jointly Announce the 2026 Special Initiative for Practical Training of Humanoid Robots and Embodied AI

-

Who Can Challenge SpaceX: Global Commercial Rockets Enter a New Phase of Differentiation

-

![]()

Could BYD Achieve the Title of 'World's Largest Automaker' by 2030?