The Consensus Between Li Shufu and Li Bin Indicates the Obsolescence of Blockbuster Logic

06/15 2026

06/15 2026

539

539

May, traditionally a small peak season, saw sales hit their lowest point in recent years, with domestic retail sales down by 20% year-on-year. Discussions about the "shakeout" have never been as serious as in 2026.

At the 2026 China Automotive Chongqing Forum (hereinafter referred to as the "Chongqing Forum"), Li Shufu, head of Geely Group, publicly proposed "shutting down, merging, and transferring redundant entities to concentrate resources on advantageous platforms" after "One Geely." As a Chinese automaker with annual sales exceeding 3 million units and ranking among the top three in scale, Geely's proactive downsizing serves as a warning to the industry.

On the eve of the Chongqing Forum, Li Xiang no longer maintained his 2023 forecast. At a recent shareholders' meeting, he pointed out that the automotive industry would only converge to five or six global companies, similar to today's smartphone industry, after reaching L4 autonomy. Three years ago, he had asserted, "The CR5 (market share) in 2025 will likely be the same as the CR5 in 2030."

There is no need to elaborate further on the commencement of the shakeout. More critically, an increasing number of automakers have reached a consensus that the industry's gameplay has begun to change before the arrival of a CR5 or CR3 landscape.

Countdown to the End of Price Wars

"The simultaneous decline in sales, revenue, and profits is historically rare," said Wang Xia, President of the Automobile Industry Branch of the China Council for the Promotion of International Trade, in his speech, pouring cold water on the seemingly booming automotive market. In the first five months of this year, hundreds of new models flooded the market, but the result was a nearly 20% year-on-year decline in national passenger vehicle retail sales. More worryingly, the automotive industry's profit margin in the first quarter was only 3.2%, not only a new low but also significantly below the national average of 4.9% for industrial enterprises above a certain size.

Behind these cold numbers lies a harsh reality: the diminishing marginal effects of price wars. Years of frenzied internal competition have not only severely injured companies but also caused severe "aesthetic fatigue" among consumers. Wang Xia pointedly noted that sales without profit support are merely hollow numerical games, and profits sustained by subsidies are ultimately castles built on sand.

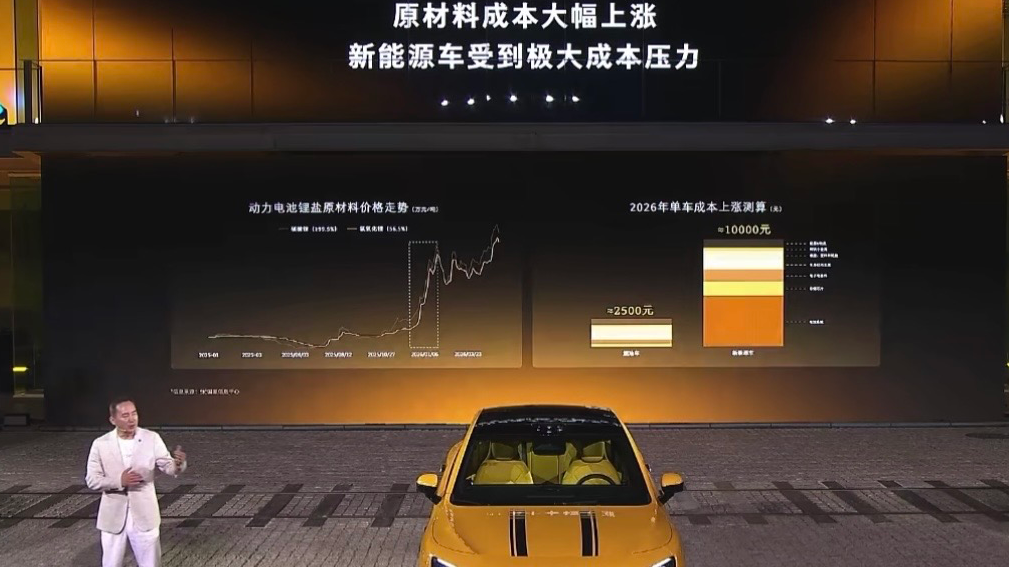

Cost pressures have further exacerbated the situation for automakers. Zhang Xinghai, Chairman of Seres Group, revealed in his speech that Vehicle companies (vehicle manufacturers) currently face significant cost challenges, particularly due to price hikes in key components. He noted that storage chips have surged from 20 yuan per unit to nearly 100 yuan per unit, a fivefold increase, while lithium carbonate prices have skyrocketed from 80,000 yuan per ton to 180,000 yuan per ton year-on-year. Taking the Aito model as an example, the average cost per vehicle has increased by 15,000 to 20,000 yuan. Against a backdrop of rising materials and costs, some automakers are still choosing to cut prices.

This "scorched-earth" competition model is no longer sustainable. Li Xiang, CEO of Li Auto, bluntly stated at a recent shareholders' meeting, "At least in the premium brand segment, no one will engage in malicious price wars anymore because everyone may realize that no one can defeat the other."

Policy is also applying the brakes. Just before the 2026 Chongqing Forum, the Ministry of Industry and Information Technology and the State Administration for Market Regulation conducted interviews and reminders with automotive manufacturers suspected of engaging in irrational competition, urging them to strengthen price compliance and enhance product quality control.

With the triple pressures of regulatory intervention, high costs, and market weakness, the industry has reached a consensus: price wars not only fail to bring true industry prosperity but also The future of the overdraft industry ( overdraft the industry's future). The demise of price wars has entered its countdown.

After the Obsolescence of Traditional Blockbuster Models, Slow Is Fast

If price wars are no longer the key to breaking the deadlock, where lies the future for automakers? The speeches by Li Shufu, Chairman of Geely Holding Group, and Li Bin, Founder and CEO of NIO, at the forum Coincidentally, at the same time (coincidentally) pointed to the same answer: systemic strength.

In his speech, Li Shufu emphasized corporate governance and succession. He proposed that Geely would further streamline its group structure, orderly shut down, merge, and transfer redundant entities, and concentrate superior resources to strengthen its core listed platforms. Behind this strategic adjustment lies the recognition that the upcoming competition is no longer a simple product war but a comprehensive battle of organizational efficiency, operational precision, strategic choices, and other aspects of systemic strength. Only by building a modern corporate operation system with a clear governance structure, well-defined responsibilities, and efficient operations can one win this protracted war.

Li Bin provided a more straightforward explanation of the shift in industry competition logic. He believes that the automotive industry has moved from "single-point competition" to a new stage of "systemic competition." In the past, automakers might have achieved breakthroughs through a single technology, a blockbuster model, or unique configurations like "refrigerators, color TVs, and large sofas." However, these advantages have now become standard in the industry.

Li Bin pointed out that the current market competition covers multiple dimensions, including product definition, core technologies, supply chain management, manufacturing, sales services, and even brand building. In today's increasingly homogeneous new energy products, simple parameter comparisons are no longer effective. A complete, mature, and efficient development system is the key for automakers to differentiate themselves and build core barriers.

In fact, the traditional "blockbuster model" is now backfiring. Earlier this year, Li Bin stated at a forum, "It's too difficult for a new model to remain a bestseller for a year." While Intensive listing ( dense launches) of new models may bring a temporary surge in orders, market enthusiasm often declines rapidly within a year. To maintain sales, companies have to Crazy investment in research and development (frantically invest in R&D) and accelerate the pace of new model launches. However, the lifecycle of models is drastically shortened, making it impossible to amortize the enormous R&D and manufacturing costs. This seemingly lively "new model feast" is dragging the entire industry into a vicious cycle of "failing to iterate means death, but iterating invites criticism."

Faced with this anxiety, an increasing number of automakers are beginning to reflect and proactively slow down. He Xiaopeng, Chairman of XPeng Motors, recently stated that XPeng is reducing the speed of product updates and iterations in global markets. He believes that future hardware iterations in automobiles will slow down, while software iterations will accelerate, with more capabilities delivered through OTA updates. Li Xiang also emphasized that automobiles must not iterate as rapidly as smartphones because they involve the safety of an entire family and require extensive real-world road testing and physical verification. Any short-sighted approach would be irresponsible to users.

In fact, before the 2026 Chongqing Forum, signs of fatigue in the automotive price war were already evident. Several mainstream automakers, including BYD, Geely, and Chery, officially announced price increases for some of their products.

As price wars subside and the blockbuster logic loses its universality, the Chinese automotive industry is undergoing a profound value restoration. Shortcuts may be the longest road, and slowing down is truly the fastest way.

-

![]()

The Big Three Telecom Giants Face Accusations of Overcharging Loyal Customers: Why Do Costs Rise with Tenure?

-

![]()

Competitor’s CTO Criticizes Extended-Range Tech; Seres’ Zhang Xinghai Fires Back: It’s Far From “Pointless”

-

![]()

"Football Unites the World," But Not the North American Auto Industry

-

![]()

Electric vehicles are indeed cheaper, but who says gasoline cars are doomed?

-

![]()

The Consensus Between Li Shufu and Li Bin Indicates the Obsolescence of Blockbuster Logic

-

![]()

Used Fuel-Powered Vehicle Prices Plummet, Losing Two Years' Value in Just Two Months

-

![]()

Hidden Presence: Chinese Automakers 'Lurking' in the U.S. Market

-

![]()

BBA Struggles to Keep Pace with Domestic Car Competitors