China’s Auto Industry: Embracing a New Era of ‘Technology for Market’

06/29 2026

06/29 2026

392

392

Text by | Intelligent Relativity

China’s auto industry is quietly undergoing fundamental changes that may redefine its core industrial model—transitioning from a “market for technology” approach to a “technology for market” paradigm.

This transformation marks the end of an all-out price war.

01

In the first quarter, the overall profit margin of China’s domestic auto industry stood at just 3.2%, teetering on the edge of operational safety. Low-price competition had reached its physical limits. Meanwhile, in May, the retail penetration rate of new energy passenger vehicles soared to a record 63%. Surpassing the 60% threshold signifies that new energy vehicles have officially entered the mainstream market. The era of relying on price cuts to lure fuel vehicle users is over; further reductions would only lead to a zero-sum game.

This shift is compounded by evolving consumer decision-making logic. Car buyers no longer prioritize low prices above all else. Instead, factors such as driving range, charging efficiency, advanced intelligent driving capabilities, and after-sales service systems are gaining prominence.

Against this backdrop, the nearly two-year-long price war has fully receded since 2026, giving way to value-based competition centered on products, technology, and brands. The average transaction price has replaced sales volume as the key metric for evaluating automakers’ operational quality.

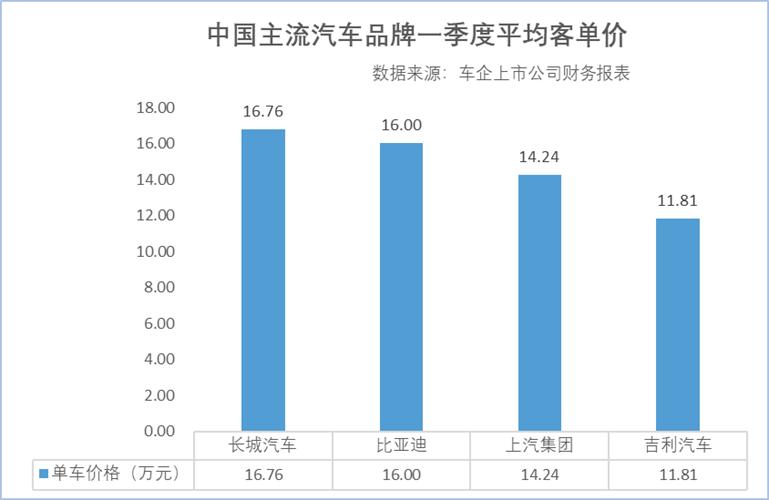

BYD exemplifies this new logic. Despite its dominant sales volume, the company maintained a stable average transaction price around 160,000 yuan in the first quarter, achieving a delicate balance between scale and premium positioning.

Signs of technological prowess abound: the second-generation Blade Battery, Flash Charging Technology, and Divine Eyes Advanced Intelligent Driving system all underscore BYD’s resilience through core technological barriers.

02

In the domestic market, automakers are bidding farewell to price wars and leveraging cutting-edge technologies to earn user trust and brand premium, fostering a virtuous cycle of “technology-scale-technology.”

For instance, in May, BYD topped China’s auto market brand sales with 330,000 units, accumulating 1.208 million units from January to May. Its lead is even more pronounced in the new energy vehicle segment: 383,000 units in May alone and 1.405 million units year-to-date.

Scale fuels technological iteration, particularly in intelligent driving. Advanced systems rely heavily on real-world driving data. As of May 28, BYD’s assisted driving models boasted an installed base exceeding 3.15 million units, with the Divine Eyes system generating over 200 million kilometers of data daily—enabling algorithm updates at speeds far exceeding industry averages.

When technologies trickle down from high-end to mass-market models as standard features, the perceived value of the entire brand rises. This explains how BYD can sustain an average price of 160,000 yuan despite selling over a million units—the value added by technological inclusivity offsets the price dilution from lower-priced models.

03

While domestic value resurgence reflects internal strength, consecutive overseas breakthroughs serve as external validation.

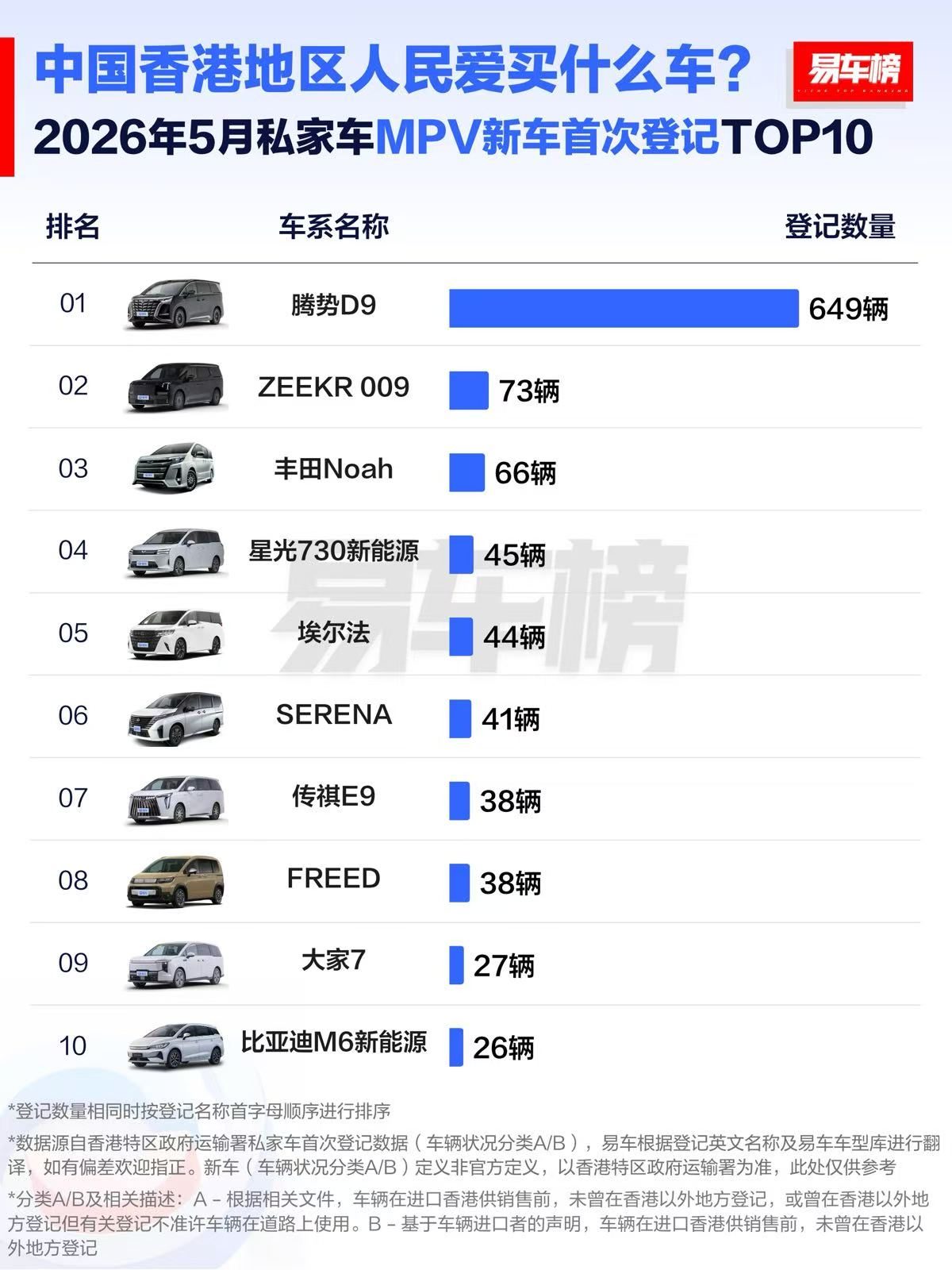

In Hong Kong, China, the Denza D9 led May’s TOP 10 newly registered MPVs with 649 units, with Chinese brands occupying more than half of the top ten. A decade ago, this market was dominated by Japanese brands.

In South Korea, BYD sold 2,023 units in April, surpassing the combined sales of Lexus, Toyota, and Honda—three major Japanese brands—and ranking among the top three imported vehicles by country. Known for its fiercely competitive auto market, home to Hyundai and Kia, South Korea saw BYD achieve over 10,000 cumulative sales in less than a year, setting the fastest record for an imported brand to reach this scale.

In these two mature markets—one in the south, one in the north—the breakthrough strategies were remarkably consistent: not through low-price dumping, but by leveraging electrification and intelligent technologies to dismantle foreign brands’ long-held defenses.

As technology becomes increasingly decisive, the decades-long “market for technology” era is drawing to a close. China’s auto industry has fully entered a new cycle of “technology for market.”

Overall data reinforces this trend: In May, BYD’s overseas sales of passenger vehicles and pickups reached 160,000 units, up 80.7% year-on-year—a new record. From January to May, cumulative overseas new energy vehicle sales exceeded 610,000 units. Export offerings have expanded from economy cars to a full range of categories, with multiple models topping new energy sales charts globally.

The decades-long “market for technology” era has officially ended. China’s auto industry now operates in a new cycle of “technology for market.”

04

Price cuts may deliver temporary sales spikes, but only technology secures long-term market dominance. By shifting from price wars to technological competition, the auto industry can create high value domestically and expand globally.

The “technology for market” era has just begun. The journey from product exports to brand exports and standard exports remains long and arduous.

*All images in this article are sourced from the internet.

-

![]()

Luna Ultra Entangled in 'National Subsidy Fraud' Controversy, Insta360 Pushed to the Brink by DJI

-

![]()

People have long suffered from splash ads. Will the 'temporarily disappeared' traffic behemoth make a comeback?

-

![]()

GPT 5.6 Reclaims the Throne, Only to Face Strict Controls Again! Has AI Truly Reached a Turning Point?

-

![]()

When the Traffic Bubble Fades, AI Giants Start to Compete on 'Real Skills'

-

![]()

Wenxin Once Integrated Multiple Web Portals, but Its Impact Has Diminished

-

![]()

A 1.388 Million Yuan Answer Sheet: Insights into Huawei's Ultra-Luxury Car Strategy and Potential Concerns from the Debut of Zunjie S800 Grand Design and V800

-

![]()

Luna Ultra Mired in 'National Subsidy Fraud' Controversy, Insta360 Cornered by DJI

-

![]()

Legal Disputes, Share Unlock, and Pricing Controversies Converge: Insta360 Reaches a Pivotal Juncture