Horizon and Momenta: A Collision Course

07/02 2026

07/02 2026

516

516

Momenta is hurtling towards a Hong Kong Initial Public Offering (IPO), and Horizon is already feeling the pressure.

Yu Kai took to social media, self-deprecatingly admitting he's "not a master of social navigation" and shunning the hype around "xxx first stock," seemingly poking fun at Momenta's claim as the "first physical AI stock."

Soon after, a photo emerged of Yu Kai meeting with Wang Chuanfu, followed by Yu Kai's social media post declaring, "We've achieved something monumental," hinting at a deep collaboration in intelligent driving. This single remark from the CEO sent Horizon's stock price soaring nearly 15% in a single day.

Interestingly, according to Momenta's prospectus, BYD is one of its 14 cornerstone investors; BYD is also a significant customer for Horizon's Journey series chips.

Behind this subtle rivalry lies the accelerating consolidation of China's intelligent driving market. Momenta's founder, Cao Xudong, publicly stated in April that the global intelligent driving landscape will shrink to just 2-3 Chinese players and 3-4 global ones—a prediction even more stringent than Li Xiang's earlier forecast of CR3 and CR5 (industry concentration ratios) for Chinese automakers.

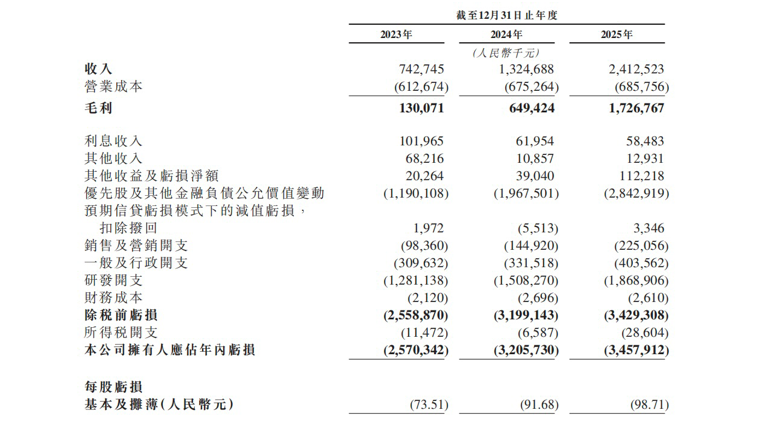

Financial data from Momenta's prospectus reveals significant growth in revenue and gross profit from 2023-2025, yet the company remains in a persistent loss-making state, primarily due to massive R&D investments. This underscores another aspect of the "brutal" competition: maintaining technological leadership demands such high stakes.

This is true not just for Momenta, the so-called "intelligent driving leader," but also for players like Huawei and Horizon.

Horizon and Momenta: A Collision Course

For both Horizon and Momenta, BYD represents a critical presence.

In early 2025, BYD sparked a wave of mass-market intelligent driving adoption, prompting mainstream automakers like Geely, Chery, and Changan to follow suit, driving down prices for new vehicles equipped with advanced intelligent driving systems. As the core algorithm provider for BYD's "Divine Eye" solution, Momenta delivers algorithmic support on NVIDIA chips.

According to Momenta's prospectus, BYD invested $15 million as a cornerstone investor.

BYD is also a major customer for Horizon, with their collaboration centered around Horizon's Journey series intelligent driving chips.

Behind this subtle rivalry lies the accelerating consolidation of China's intelligent driving market. The automotive industry's long-standing fear that "only 3-5 players will survive" has now spread to the intelligent driving sector.

A showdown between Horizon and Momenta is inevitable. Not only because chip-focused Horizon is transforming into an intelligent driving solution provider, while algorithm-strong Momenta is also pursuing "software-hardware integration." The SAIC Volkswagen ID. ERA 9X, featuring Momenta's R7, utilizes Momenta's self-developed chips.

Indeed, Momenta is a formidable force that other intelligent driving players must contend with. Prospectus data shows that Momenta's revenue over the past three years (2023, 2024, and 2025) primarily comes from providing intelligent driving solutions to automakers, consisting mainly of two parts: technology development services and licensing services.

Among these, licensing services surged from 3.8% to 40.1% of revenue. Licensing services refer to per-vehicle royalties or licensing fees based on sales volumes after model mass production. This explosive growth in licensing revenue directly reflects Momenta's market appeal and delivery capabilities.

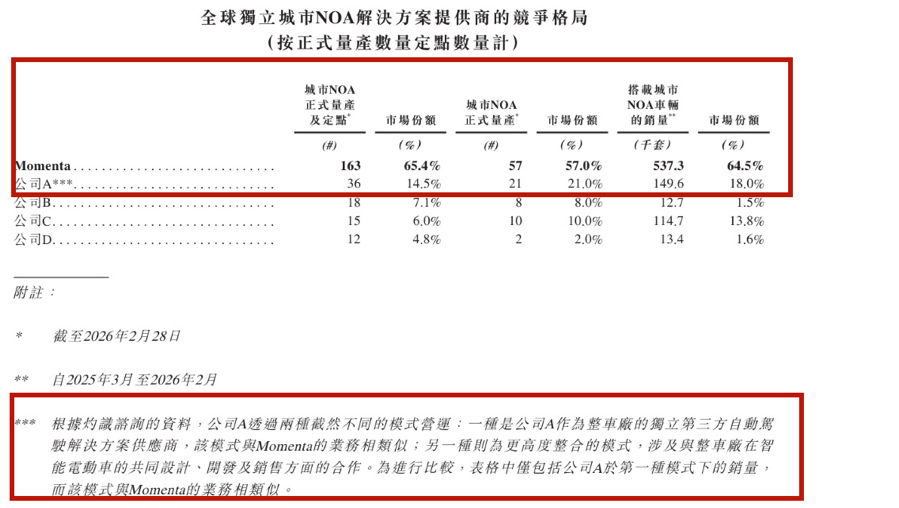

The prospectus reveals that Momenta has secured over 65.4% market share in mass-produced urban NOA, far surpassing Huawei's 14.5% in second place.

However, Momenta clarified that this ranking excludes Huawei's highly integrated models, such as the "Jie" series under Harmony Intelligent Mobility and the "Jing" series from partnerships with Dongfeng and GAC, focusing solely on data as a third-party supplier.

Recently, Horizon officially launched HSD V2.0, its most significant Over-The-Air (OTA) update yet, with iCAR V27 set to be the first model to upgrade.

Horizon's HSD solution has so far been mass-produced in Chery's Exeed and iCAR models, remaining in the "comfort zone" of the 150,000-yuan price segment. According to Yu Kai's public statement late last year, Horizon aims to make urban intelligent driving standard in 100,000-yuan vehicles by 2026.

Bringing the battle to the 100,000-yuan market is the catalyst for this inevitable clash. The Guangqi Toyota Platinum Intelligence 3X (GAC Toyota bZ3X) recently introduced Momenta's 5.0 Flywheel in its OTA update, enabling features like automated ETC gate passage and cross-traffic avoidance. This model starts at around 100,000 yuan. The Aion N60, a collaboration between Aion and WeRide, launched in late April with urban intelligent driving capabilities in the 100,000-yuan segment.

The Cost-Effectiveness Race in Intelligent Driving Forces Automakers to Choose Sides

After a period of market shakeout, China's intelligent driving landscape is gradually taking shape. Setting aside new energy automakers developing both chips and intelligent driving solutions in-house, other automakers face three main paths:

The first is the Huawei model of full outsourcing. This involves not just deep technical integration but also systematic integration of branding, channels, and ecosystems. Beyond the "Jie" and "Jing" series, more automakers are fully embracing Huawei. While automakers avoid building thousand-strong algorithm teams and gain access to top-tier intelligent driving capabilities, they cede core decision-making power and face higher cost-sharing, resulting in model pricing typically above 250,000 yuan.

The second is the mid-cost-effectiveness model represented by Momenta. Its strength lies in strong "adaptability flexibility." Its underlying chips are compatible with NVIDIA, Qualcomm, and even self-developed chips, while its algorithm flywheel covers models ranging from 100,000 to over 300,000 yuan. This model's examples are rapidly expanding: beyond deep collaborations with Buick, Toyota, and IM Motors, future mass-market luxury models like the all-new Mercedes-Benz electric GLC and BMW's next-gen iX3 will also adopt Momenta's R7 solution. If a few blockbuster models emerge among these new vehicles, Momenta will gain the confidence to compete with Huawei in the 200,000-yuan market.

Additionally, there's the high-cost-effectiveness Horizon model. Automakers can choose to only adopt Horizon's Journey series chips while developing their own upper-layer algorithms, or opt for a complete high-level intelligent driving solution like HSD. This model's greatest advantage is pricing—leveraging the cost advantages of domestic chips, Horizon can deploy intelligent driving functions in mid-to-low-end models at extremely low marginal costs.

According to Momenta's prospectus data, Huawei's main strength lies in its highly integrated model, dominating the premium market above 300,000 yuan. However, the market below 300,000 yuan remains undecided, representing the core battleground with annual sales in the millions.

Returning to Momenta's IPO, its shift from the U.S. to Hong Kong reflects the fleeting nature of the autonomous driving opportunity. Global policy and capital market windows may only remain open for 2-3 years. As the sole strategic cornerstone investors, Mercedes-Benz and BYD's relatively modest investment amounts send a critical signal: these automakers will likely secure first access to new technologies, deeper data closed-loop permissions, and even priority collaboration in defining next-gen intelligent driving platforms or Robotaxi ventures—effectively locking in technology roadmaps for the next 3-5 years.

For the vast majority of automakers not planning to go all-in on self-development, now is not the time for hesitation but for decisive action. Huawei has already established brand recognition in the premium market; Momenta and Horizon are locked in a fierce mid-market competition; while the low-end market tests dual capabilities in "deployment speed" and "cost control." Automakers still "waiting to see for two more years" risk finding themselves without a team to join—after all, when competitors' 100,000-yuan models achieve urban intelligent driving, consumers won't wait for hesitant brands.

-

![]()

MathWorks: Generative AI Holds Great Potential, Yet a Trusted Toolchain is Essential for Flawless Operation

-

![]()

Small Earphones, Big Business

-

![]()

Volkswagen Slashes 100,000 Jobs, Mercedes-Benz Axes Year-End Bonuses: What’s Ailing German Auto Titans?

-

![]()

Doubao Can No Longer Offer Free Services to 345 Million Users: China's Era of Free AI Is Drawing to a Close

-

![]()

How Can Chinese Small Home Appliances Conquer Southeast Asia Through 'Dimensional Competition'?

-

![]()

Why are top intelligent driving players betting on reinforcement learning?

-

![]()

June 2026 Automobile Complaint Index Rankings: Persistent Problems Ignite Grievances Among Long-term Vehicle Owners

-

![]()

Avita Takes Another Stab at HKEX Listing: Facing the Urgency of Sustaining Operations Amid 11.2 Billion Yuan Loss Over Three Years