Huazhu: Lightening the Load and Marching Ahead with Agility, Remaining a Leader in the Hotel Industry!

05/18 2026

05/18 2026

576

576

Prior to the U.S. market opening on May 15, 2026 (Beijing Time), Huazhu (1179.HK/HTHT.O) unveiled its financial report for the first quarter of 2026. Overall, Huazhu's performance in the first quarter was impressive, with underlying operational data continuing to show improvement since turning positive in the latter half of the previous year. However, the only hiccup was the increased sales expenses amid a weaker recovery in business travel, which somewhat dampened profit growth.

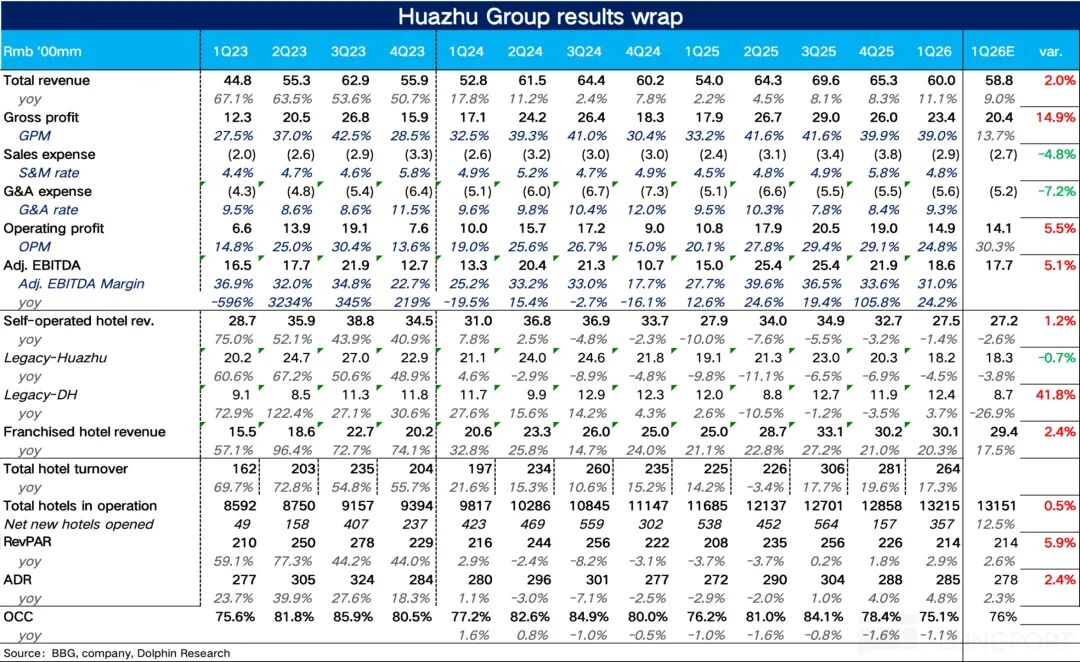

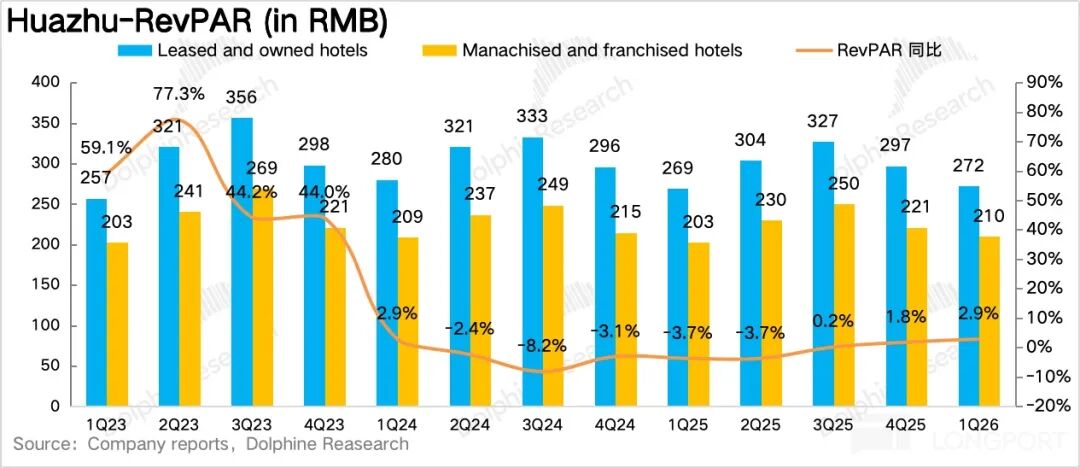

1. Year-on-Year Expansion in RevPAR. Focusing on the core operational metric of Revenue Per Available Room (RevPAR), Huazhu's RevPAR in the first quarter reached RMB 214 per night, marking a 2.9% increase year-on-year. This positive trend has persisted since the second half of the previous year.

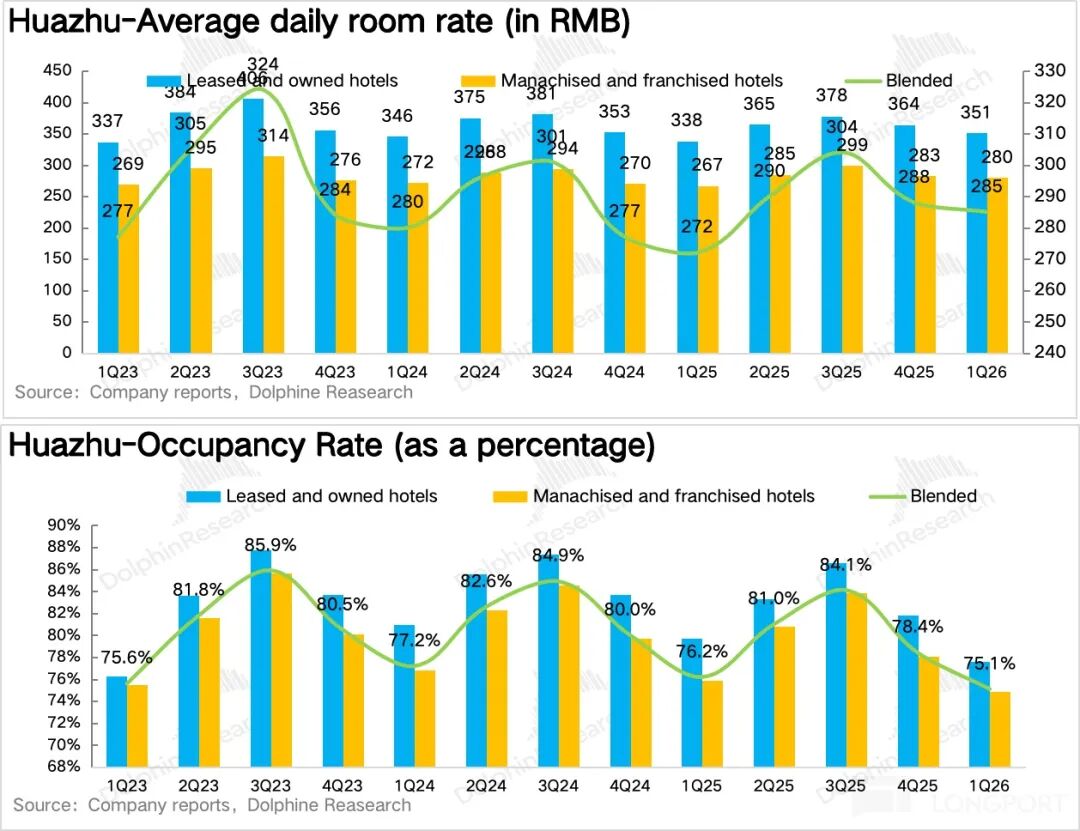

Breaking it down, the Average Daily Rate (ADR) rose by 4.8% year-on-year to RMB 285 per night, serving as the primary growth driver. This was mainly due to the ongoing release of structural premiums from the increased proportion of new product versions, such as Hanting 3.5/4.0 and Ji Hotel 5.0. The Occupancy Rate (OCC) stood at 75.1%, down 1.1 percentage points year-on-year, indicating that while leisure travel remained robust, overall business travel was still sluggish, dragging down the overall occupancy rate.

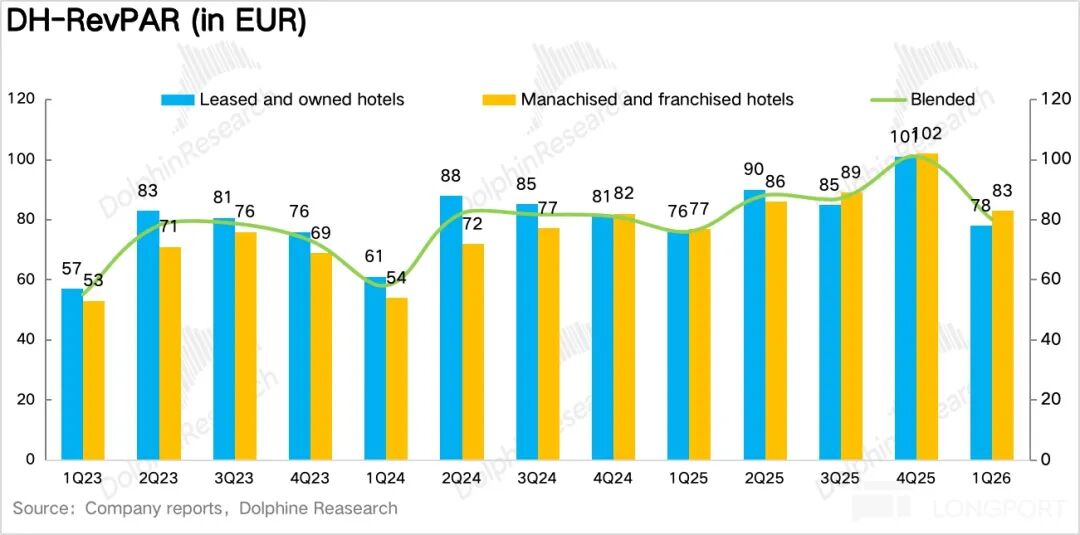

In the European market, the first quarter witnessed a surge in corporate meetings within the EU and a recovery in inbound tourism to Europe. This led to a 5.3% year-on-year increase in RevPAR to EUR 80 per night, with balanced contributions from volume and price, outperforming the domestic market.

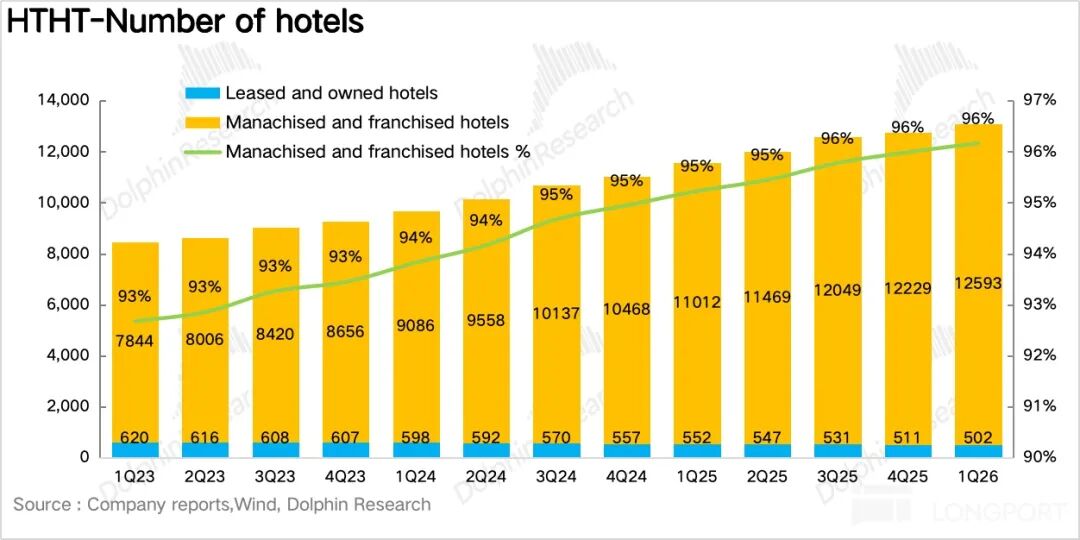

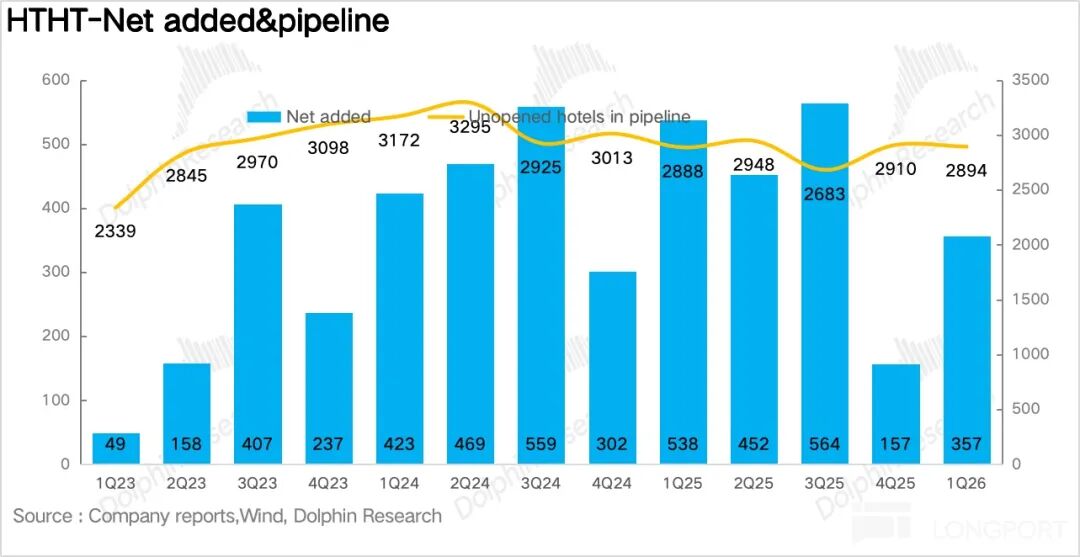

2. Steady Pace of Store Openings. In terms of store openings, a net of 357 new stores were added in the first quarter, including 537 new openings, maintaining a relatively high pace. Mid-to-high-end brands (Ji Hotel, Crystal Orange, Mercure) continued to be the key growth drivers, while economy hotels focused more on renovations. Notably, Huazhu closed 180 stores in the first quarter, significantly increasing the elimination of poorly located, aged, and unprofitable stores in pursuit of high-quality growth.

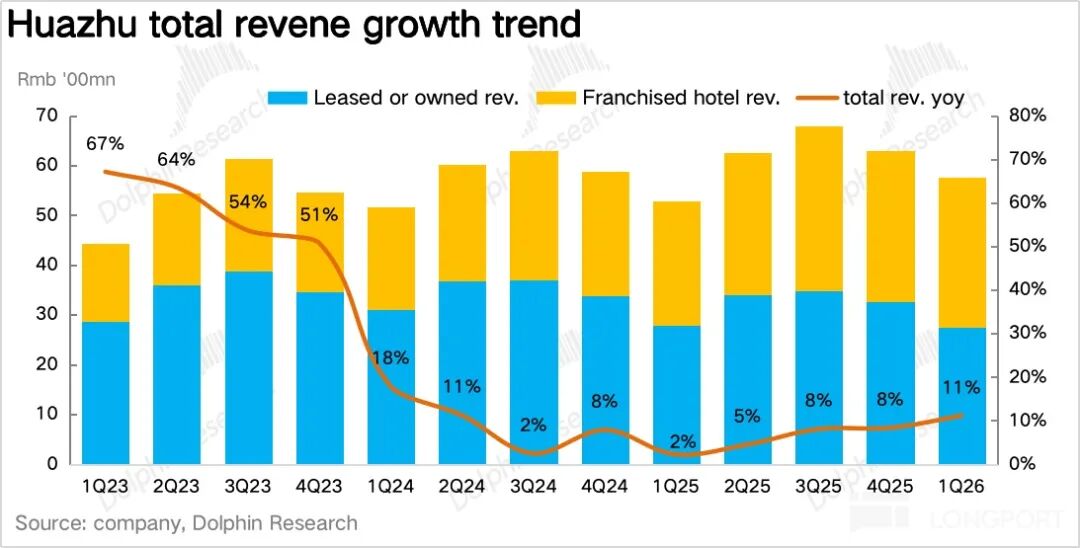

3. Sequential Acceleration in Revenue Growth. In the first quarter, Huazhu Group's total revenue amounted to RMB 6 billion, up 11% year-on-year and accelerating sequentially from the fourth quarter of the previous year. The franchise business, benefiting from an increase in the number of rooms and improved single-store revenue due to positive RevPAR, grew by 20% year-on-year to RMB 3 billion, accounting for a further increase of 3.7 percentage points to 50%.

Revenue from directly operated businesses was approximately RMB 2.8 billion, down 1.4% year-on-year, with the decline narrowing sequentially. Dolphin Research speculates that this was mainly due to the relatively strong performance of high-end directly operated brands (Xiyue, Blossom Hill, etc.).

4. Temporary Uptick in Sales Expenses. Due to the continuous advancement of the company's asset-light strategy, the proportion of franchise businesses increased significantly year-on-year, driving a 5.8 percentage point increase in gross profit margin to 39%. (Franchise models save on rigid costs such as rent and labor, resulting in higher gross profit margins).

On the expense side, Dolphin Research speculates that due to a weaker recovery in business travel and increased industry competition, Huazhu temporarily increased its promotion of mid-to-high-end brands on emerging channels such as social media and short videos. This led to a slight 0.3 percentage point increase in the sales expense ratio to 4.8%. The administrative expense ratio remained stable overall. Ultimately, Huazhu's adjusted EBITDA reached RMB 1.86 billion, up 24% year-on-year, slightly exceeding market consensus expectations (RMB 1.77 billion).

5. Review of Key Financial Information

/>

/>

Dolphin Research's Overall View:

Overall, except for a slight increase in the company's temporary sales expenses, the quality of growth in the first quarter was relatively high. Whether it's the consecutive three quarters of positive RevPAR growth (the first in the industry to turn positive), the continuously increasing proportion of franchise revenue, or the profitability of the DH business after turning around, all indicate that Huazhu is transitioning from cyclical recovery to structural growth.

Furthermore, leveraging Huazhu's financial report, let's discuss the marginal changes in the hotel industry:

On the supply side, the biggest challenge in the hotel industry over the past two years has not been a lack of guests but rather an overly rapid increase in supply, disrupting the pricing system. Especially for mid-to-high-end hotels, projects have been concentrated in recent years, with rapid property renovations and high franchisee expectations. As a result, a large amount of new supply entered the market when demand had not fully caught up, leading to a collapse in pricing.

With the extension of franchisees' investment return periods, the year-on-year growth rate of the number of hotel rooms nationwide has fallen from 9% in November 2025 to around 6.5% currently. Although still high compared to the normal level of 3%-5%, the trend clearly reflects a structural cooling on the supply side.

From the demand side, according to data released by the Ministry of Culture and Tourism, the average person made 3.2 trips in Q1, a significant year-on-year increase of 41%. Among optional consumer spending from January to April, tourism recovered the fastest, reaching 128% of the level in 2019 (higher than catering at 115% and retail at 108%).

Breaking it down, the most significant increase was in the proportion of short weekend trips, which rose by 7-8 percentage points to 78%. Combined with the decline in the proportion of ticket expenditures in the consumption structure (from 42% in 2019 to 28%) and the increase in the proportions of accommodation, experiences, and dining, it suggests that leisure travel demand is gradually shifting from "holiday-driven impulse consumption" to "high-frequency, normalized, experiential daily necessities."

This change means that for hotels, a decrease in occupancy rate fluctuations also implies that they no longer need to fill vacant rooms during off-peak seasons through extreme price cuts. The focus can shift from price wars to upgrading the quality of their own products. In Dolphin Research's view, the first to benefit from this trend will be leading companies like Huazhu, which have a high proportion of mid-to-high-end brands, strong membership programs, and more mature revenue management systems.

Looking ahead to 2026, from Huazhu's own execution perspective, brand upgrades and continued store openings in emerging markets (lower-tier cities) remain the two core growth drivers.

On the one hand, by focusing on developing four major brands—Ji Hotel Grand View (high-end business), Intercity (urban select), Crystal Orange (light luxury), and Mercure (international mid-range)—in first- and second-tier cities, Huazhu aims to further increase the proportion of mid-to-high-end brands. On the other hand, by introducing lightweight products such as "Hanting Express," it lowers the franchise threshold and accelerates its penetration into emerging markets (lower-tier cities). The value of such upgrades lies not just in making stores "look better" but also in supporting stronger ADRs, shorter construction cycles, and stronger competitive advantages in lower-tier cities.

A more detailed value analysis has been published in the article with the same title in the "Insights-Deep Dive" section of the Longbridge App.

The following is a detailed interpretation:

I. Year-on-Year Expansion in RevPAR

As usual, before delving into the financials, let's first look at the most fundamental operational metrics:

1.1 Accelerated Recovery in ADR, Continued Release of Structural Premiums

From the core operational metric of Revenue Per Available Room (RevPAR), Huazhu China's RevPAR in the first quarter was RMB 214 per night, up approximately 2.8% year-on-year, continuing the positive growth trend for three consecutive quarters since Q3 2025, with an acceleration in the growth rate compared to Q4 (+1.8%). Breaking it down by volume and price:

ADR (Average Daily Rate): RMB 285 per night, up approximately 4.8% year-on-year, with the growth rate further increasing compared to Q4 (+4.0%). In addition to improvements in the industry's supply-demand balance, for Huazhu, in Dolphin Research's view, the core reason for its earlier ADR recovery compared to some peers lies in its proactive product structure upgrades ahead of the industry.

After all, Hanting 3.5, Ji Hotel 4.0, and Orange Hotel 2.0 are not simply "better renovations" but represent comprehensive improvements in design, efficiency, construction cycles, customer segmentation, and membership conversion.

OCC (Occupancy Rate): 75.1%, down approximately 1.1 percentage points year-on-year. While leisure travel was strong, business travel demand, although recovering, cannot yet be considered robust, more of a "bottoming out and stabilization." Additionally, it's worth noting that the decline in OCC for mature stores (operating for more than 18 months) was significantly smaller than the overall decline, indicating that the ramp-up of new stores also put pressure on OCC.

/>

/>

/>

/>

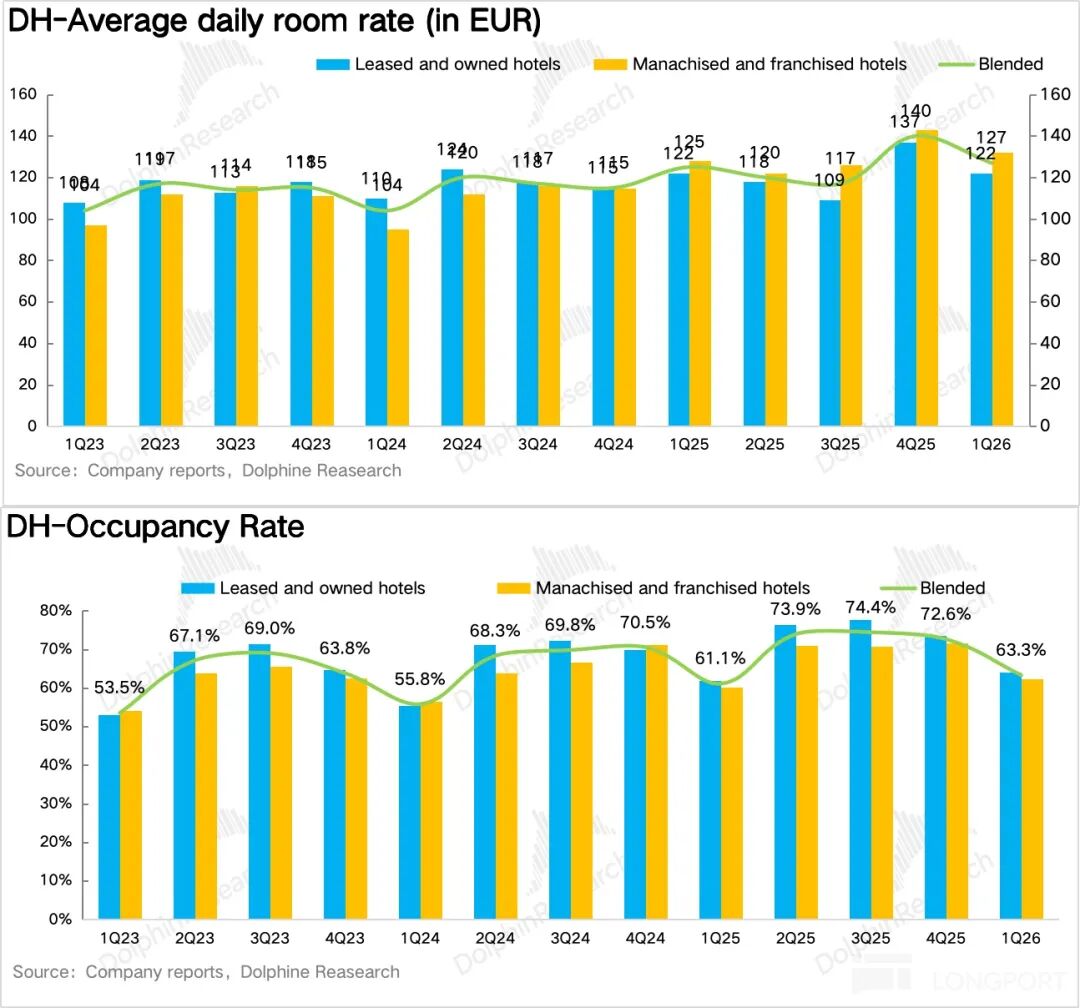

1.2 Steady Recovery in the European Market, DH Starts to "Generate Blood"

In Q1 2026, Legacy-DH's RevPAR was approximately EUR 80 per night, up approximately 5% year-on-year. In terms of volume and price contributions:

OCC: 63.3%, up approximately 2.1 percentage points year-on-year, primarily benefiting from the recovery of European spring business activities and sustained growth in inbound tourism demand.

ADR: Approximately EUR 127 per night, up approximately 1.6% year-on-year, showing stable performance.

However, what's more important here is the change in profitability. In the past, the market viewed DH with two keywords: heavy assets and low efficiency. But in Q1, DH's adjusted EBITDA was approximately USD 60 million, continuing the profitable trend after turning around in Q4 2025, indicating that the previous restructuring (property sale-and-leaseback, franchise conversion, cost optimization) has produced tangible results. DH will transform from a "historical burden" to a "growth option."

Looking ahead, the recovery of the European hotel and tourism market is still ongoing, especially in Germany, Huazhu's core market for the DH business, which is benefiting from the recovery of exhibition economy and business travel. The performance of the Intercity brand has also been notable.

/>

/>

/>

/>

1.3 Sustained High Pace of Store Openings, Continuous Structural Optimization

In terms of the number of store openings, a net of 357 new stores were added in the first quarter, including 537 new openings, maintaining a relatively high pace. Mid-to-high-end brands (Ji Hotel, Crystal Orange, Mercure) remained the absolute growth engines, while economy hotels focused more on renovations. Additionally, it's worth noting that Huazhu closed 180 stores in the first quarter, significantly increasing the elimination of poorly located, aged, and unprofitable stores in pursuit of high-quality growth.

The future direction of Huazhu's expansion is clear: one path is brand upgrading, with mid-to-high-end brands such as Ji Hotel, Orange Hotel, Intercity, Crystal Orange, Manxin, and Mercure continuing to drive structural upgrades; the other path is market penetration, introducing upgraded versions of Hanting and Ji Hotel in lower-tier cities, leveraging brand and efficiency advantages to outcompete independent hotels.

/>

/>

/>

/>

II. High Growth in Franchise Revenue, Acceleration of the Asset-Light Flywheel

2.1 Group's Overall Revenue Exceeds Expectations

In the first quarter, Huazhu Group's total revenue was RMB 6 billion, up 11% year-on-year, accelerating sequentially from the fourth quarter of the previous year. The franchise business, benefiting from an increase in the number of rooms and improved single-store revenue due to positive RevPAR, grew by 20% year-on-year to RMB 3 billion, accounting for a further increase of 3.7 percentage points to 50%.

Revenue from directly operated businesses was approximately RMB 2.8 billion, down 1.4% year-on-year, with the decline narrowing sequentially. Dolphin Research speculates that this was mainly due to the recovery of business activities in first-tier cities and the stable contributions from high-end directly operated brands such as Xiyue and Blossom Hill.

/>

/>

/>

/>

/>

/>

2.2 Asset-Light Transformation Drives Continuous Expansion in Gross Profit Margin

Due to the continuous increase in the proportion of franchise businesses (which save on rigid costs such as rent and labor, resulting in significantly higher gross profit margins than directly operated businesses), the gross profit margin increased by 5.8 percentage points to 39%.

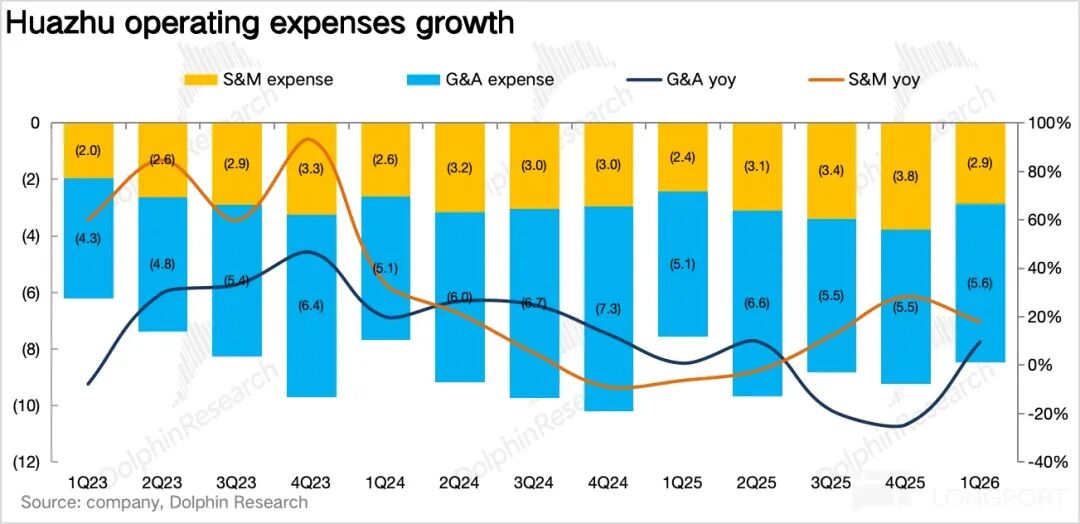

2.3 Periodic Surge in Sales Expenses

From an expenditure perspective, Dolphin Research posits that, given the sluggish revival of business travel and escalating industry rivalry, Huazhu has opted to temporarily amplify its promotion of mid-to-high-end brands across burgeoning platforms like social media and short videos. Consequently, the sales expense ratio saw a modest uptick of 0.3 percentage points, reaching 4.8%, while the administrative expense ratio maintained overall stability. Ultimately, Huazhu's adjusted EBITDA soared to RMB 1.86 billion, marking a 24% year-on-year surge and marginally surpassing the market consensus estimate of RMB 1.77 billion.

- END -

// Reprint Authorization

This article represents an original work by Dolphin Research. Any reproduction necessitates prior authorization.

// Disclaimer and General Disclosure Notice

This report is crafted solely for the purpose of providing general, comprehensive data. It is intended for general perusal and data reference by users of Dolphin Research and its affiliated entities. It does not cater to the specific investment objectives, preferences for investment products, risk tolerance levels, financial circumstances, or unique needs of any individual recipient. Investors are strongly advised to consult with independent professional advisors prior to making any investment decisions based on this report. Any individual who makes investment decisions utilizing or referencing the content or information presented in this report assumes all associated risks. Dolphin Research shall not be held accountable for any direct or indirect liabilities or losses that may arise from the utilization of the data contained within this report. The information and data herein are sourced from publicly available channels and are provided solely for reference. Dolphin Research endeavors to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the viewpoints expressed in this report shall not, under any jurisdiction, be deemed or construed as an offer to sell securities or an invitation to purchase or sell securities. Furthermore, they shall not constitute advice, solicitation, or recommendation concerning relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for, nor are they to be distributed to, jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials would violate applicable laws or regulations. Additionally, they should not be distributed to citizens or residents of such jurisdictions where it would result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in those jurisdictions.

This report solely reflects the personal viewpoints, insights, and analytical methodologies of the relevant authors and does not represent the stance of Dolphin Research and/or its affiliated entities.

This report is produced by Dolphin Research, and the copyright is exclusively owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) create, copy, reproduce, duplicate, forward, or generate any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized individuals. Dolphin Research reserves all related rights.

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan