Beijing Launches Six Major Vehicle-Road-Cloud Integration Projects, with 2.8 Billion Yuan Investment Being Just the Beginning

07/06 2026

07/06 2026

330

330

This marks the 82nd original article from the Thinking AI Society.

The full text comprises approximately 1,810 words, with an estimated reading time of 6 minutes.

Recently, Beijing has been making significant strides in vehicle-road-cloud integration.

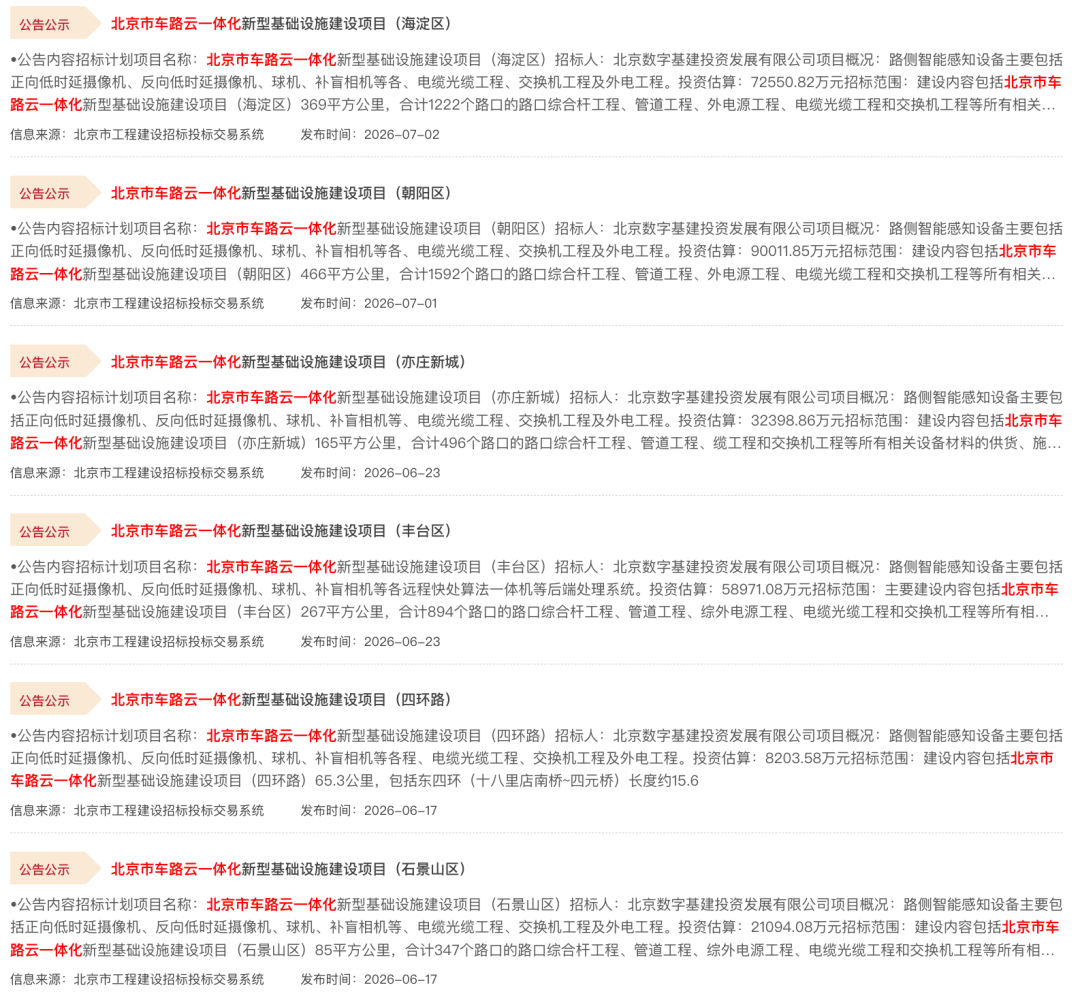

In early July, bidding plans for vehicle-road-cloud integration construction projects in Chaoyang and Haidian districts were unveiled, amounting to a total investment of 1.63 billion yuan.

Looking back to June, projects were also announced for Shijingshan, the Fourth Ring Road, Fengtai, and Yizhuang New City, encompassing six projects with a combined investment of 1.21 billion yuan.

In total, these six projects across five districts and one ring road represent an investment of 2.84 billion yuan, covering 4,551 intersections and spanning an area of 1,419 square kilometers.

While these figures may seem abstract, the scale and density of these projects are quite substantial on a national level.

How Significant Are These Six Projects? Let's Delve Deeper

First, let's outline the specifics of the six projects. I've compiled the key data below:

All data sources stem from the bidding plan announcements on the Beijing Municipal Public Resources Trading Services Platform, targeting the zonal sections of the "Beijing Vehicle-Road-Cloud Integrated New Infrastructure Construction Project."

Several aspects of these projects are particularly noteworthy.

Firstly, all bidders are unified under Beijing Digital Infrastructure Investment and Development Co., Ltd. Rather than each district conducting its own bidding process, a municipal-level platform is handling it uniformly.

What does this signify? It indicates a city-wide, coordinated effort with standardized procurement, construction, and unified standards, rather than scattered pilot projects in each district.

Secondly, the construction content is highly standardized across projects. The description for each project is nearly identical: roadside sensing equipment (including forward and reverse low-latency cameras, radar-vision integrated machines, blind-spot cameras, and edge computing nodes) + backend processing (intelligent sensing engine, video analysis, data distribution nodes, accident rapid response algorithms) + supporting infrastructure (composite poles, pipelines, optical cables, and external power).

This is no longer a trial project in the exploratory phase; it has reached the engineering stage of mass replication.

Thirdly, Yizhuang stands out somewhat. Covering the same 165 square kilometers and 496 intersections, but with sensing equipment deployed at only 100 intersections and an investment of 320 million yuan, the lowest among the six projects.

Why? Because Yizhuang was Beijing's earliest area for vehicle-road-cloud development, with several phases already completed. This time, the focus is on incremental additions and standard upgrades.

2.8 Billion Yuan Is Just the Tip of the Iceberg; What's the Total Investment?

If you think 2.8 billion yuan is already a substantial amount, let me clarify that it's just a small fraction of Beijing's total vehicle-road-cloud initiative.

The initial total investment was announced in May 2024, amounting to 9.939 billion yuan, covering 13 districts, 2,324 square kilometers, and 6,050 intersections across the city.

Funding is sourced from 70% government investment and 30% corporate self-financing.

By 2025, contiguous coverage of 600 square kilometers had been achieved. The cloud control platform processes approximately 420TB of data daily, connecting around 1,100 test vehicles.

Now, in 2026, the combined coverage of Chaoyang, Haidian, Fengtai, Shijingshan, and Yizhuang New City spans 1,419 square kilometers and 4,551 intersections, with an investment of 2.84 billion yuan.

It's important to note that these are newly released sections, part of the phased advancement of the 9.9 billion yuan total, not additional new projects.

Let's crunch the numbers: With a total investment of 9.9 billion yuan covering 2,324 square kilometers and 6,050 intersections, that's approximately 4.26 million yuan per square kilometer and around 1.64 million yuan per intersection.

What does this cost level imply on a national scale?

To be honest, it's not cheap, but it's also not unreasonable.

Each intersection requires a significant amount of equipment: low-latency cameras, radar-vision integrated machines, edge computing nodes, intelligent sensing engines, plus composite poles, pipelines, optical cables, and external power support. The cost for a complete setup can easily reach tens of thousands of yuan.

Moreover, Beijing has a characteristic—high construction costs.

Consider excavating pipelines and erecting composite poles on main roads in Chaoyang District, involving traffic diversions, nighttime construction, and coordinating with various property rights units. These hidden costs are much higher than in second- and third-tier cities.

Why Beijing, and Why Now?

I believe there are three driving forces behind this wave of concentrated bidding.

The first is policy-driven.

In early 2024, the Ministry of Industry and Information Technology and four other departments issued the "Notice on Conducting Application Pilots for 'Vehicle-Road-Cloud Integration' of Intelligent Connected Vehicles," announcing 20 pilot cities, with Beijing ranked first. Pilots have assessments and deadlines, so construction progress cannot lag.

The second is driven by the implementation of L3 autonomy.

At the end of last year, L3-level autonomous driving access and road testing pilots were launched, with automakers subsequently obtaining L3 testing licenses this year.

However, L3 cannot rely solely on vehicle intelligence, especially in complex urban scenarios. Roadside sensing and cloud control platforms provide vehicles with a "god's-eye view"—enabling blind spot visibility, beyond-line-of-sight prediction, and rapid accident response.

Vehicle-road-cloud integration is not just an enhancement; it's a necessary condition for the large-scale implementation of high-level autonomous driving.

The third is industry implementation.

Beijing has long aimed to build a "world-class intelligent connected vehicle industry hub," but mere demonstration zones and test fields are insufficient. Real construction projects and sustained orders are essential for the survival and growth of enterprises along the supply chain.

With the release of 2.8 billion yuan in projects, the entire supply chain benefits:

Upstream: Cameras, millimeter-wave radars, radar-vision integrated machines, edge computing devices, fiber optic cables

Midstream: System integrators, intelligent road OS, sensing algorithms, cloud control platforms

Downstream: Testing operations, mobility services, logistics distribution

Looking at Yizhuang, companies like Baidu, Pony.ai, and Baidu Apollo Go are already operating there. The more complete the infrastructure, the larger their operational scope can expand, accelerating commercialization.

Another detail many might overlook: Among these six projects, bidding plans for Chaoyang and Haidian were only hung in early July, with formal announcements expected in early August; for Fengtai, Yizhuang, and the Fourth Ring Road, they were hung in mid-to-late June, with formal announcements in mid-to-late July.

What does this mean? From now until early August, Beijing will intensively release formal bidding announcements for vehicle-road-cloud projects.

These are just six sections; there may be more from districts like Shunyi, Changping, and Daxing later.

For those in the industry, the next one to two months represent a critical window for securing projects.

From an industry observation perspective, once information on who wins the bids, the bid prices, and the equipment and solutions used becomes available, we can truly discern Beijing's technological approach and industry landscape for vehicle-road-cloud integration.

In fact, debates about vehicle-road-cloud integration have never ceased.

Some argue, "Vehicle intelligence alone is the right path; vehicle-road-cloud integration is a heavy-asset money pit." Others say, "China's national conditions necessitate the vehicle-road coordination approach."

I believe it doesn't have to be an either-or situation. Vehicle intelligence and vehicle-road-cloud integration are not substitutes but complementary;

vehicle intelligence handles "on-board intelligence," while vehicle-road-cloud integration provides "roadside safety redundancy and beyond-line-of-sight capabilities."

Beijing's 2.8 billion yuan investment in six projects, covering 4,551 intersections, is not the endpoint but just the starting point of a new round of construction.

When the day comes that all 2,324 square kilometers and 6,050 intersections across the city are completed, what will Beijing look like?

Perhaps by then, "smart vehicles, intelligent roads, and powerful clouds" will truly be more than just a slogan.

All article content is sourced from publicly available information and compiled.

Written casually in my spare time for sharing, representing only personal views.

-

![]()

In the AI-Driven Office Era, Is WPS Becoming a Hidden Threat to Hard Drives?

-

![]()

When AI Begins to Reshape Infrastructure: A Reshuffle in the U.S. Cloud Market

-

![]()

Tencent’s Strategic Maneuver: Selling Kuaishou, Investing in Kling

-

Has the Semi-Annual Achievement Rate Dipped Below 40%? Can AIVA Circumvent the 'Multi-Shareholder Death Spiral'?

-

![]()

Stepping Out of the Humanoid Robot Concept: Why is Autonomous Driving the First Large-Scale Implementation Track for Physical AI?

-

![]()

WPS: Criticism Warranted, Yet Open to Improvement

-

![]()

Farewell to Image-First: Robotic Vision is Undergoing a Fundamental Reconstruction

-

![]()

Former Huawei 'Genius Teen' Encounters a 'Hiccup' in DeepSeek's Recruitment Process