Baidu Intelligent Cloud Sets 2026 Goal: Growth Rate Amplified to 200%, AI Cloud Embarks on Systemic Competition

01/28 2026

01/28 2026

594

594

A fresh wave of intense competition in the AI cloud arena is currently unfolding.

Shuzhi Qianxian has discovered that Baidu Intelligent Cloud recently convened a strategic meeting, elevating its 2026 revenue growth target for AI-related businesses from 100% to 200%, with a clear ambition to "claim the top position" in the AI cloud market. This adjustment sends a definitive signal to the market: the AI cloud sector is heating up, with major cloud service providers engaging in fierce competition centered around AI chips, large-scale computing clusters, price wars, large model iterations, and capturing user mindshare.

The AI cloud industry stands at the threshold of a new growth phase. Relevant institutions forecast that the global AI cloud market will reach $89.4 billion by 2025 and is projected to exceed $400 billion by 2030, boasting a compound annual growth rate exceeding 30% over the next five years. This trend is already evident in the operating data of leading providers. According to Baidu's Q3 2025 financial report, AI cloud revenue witnessed a 33% year-on-year increase, with subscription revenue for AI high-performance computing infrastructure surging by 128% year-on-year.

A more notable shift is that the primary driver of this growth phase is transitioning from large model competitions to large-scale deployments, exemplified by intelligent agents. Capability, cost, and speed have emerged as the three pivotal indicators for industrialization. The previous approach of relying on stacking GPUs and competing on computing power scale during the training phase can no longer sustain the continuous expansion of AI large model deployments.

Against this backdrop, competition in the AI cloud sector is evolving into a systemic capability battle, centered on integrated hardware-software solutions. This spans from underlying chips and computing architectures to inference systems and engineering platforms, extending to the organization and scheduling capabilities of large models, intelligent agents, and tools.

01

AI Deployment: Large-Scale Adoption on the Horizon

"By 2025, AI deployment will have been validated across multiple scenarios, setting the stage for large-scale adoption, with the industry poised for explosive growth," multiple industry insiders shared with Shuzhi Qianxian earlier this year.

The industry widely believes that AI deployment has progressed beyond early pilot stages and entered a critical phase of value creation. Both consumer-end (C-end) penetration and business-end (B-end) commercialization are accelerating, with 2026 expected to mark the first year of substantial returns for the AI industry.

On the consumer front, AI application usage is rapidly increasing, with AI assistant app markets experiencing swift growth. Competition for C-end traffic entry points is intensifying, with Tencent, Baidu, and ByteDance already launching their AI marketing campaigns for the 2026 Spring Festival. AIGC tools are becoming everyday utilities, with smartphone manufacturers' intelligent assistants achieving high penetration rates in second- and third-tier markets, some reaching nearly 200 million monthly active users.

In contrast, changes on the enterprise front are more profound. While market perception may not align with that of the C-end, B-end clients exhibit a stronger willingness to pay, with their potential often underestimated.

For instance, AIGC is experiencing explosive growth. Following Google's VEO 2 release in 2025, text-to-video capabilities gradually became commercialized, with AI-generated comics witnessing astonishing growth rates. Industry insiders claim it has "achieved three years of short drama growth in a single year." Data from Feifan Industry Research reveals that over 3,000 AI-generated comics were launched domestically in the first half of 2025, with a monthly compound growth rate of approximately 80%.

In sectors such as automotive, finance, government, energy, education, pharmaceuticals, and agriculture, AI has deeply integrated into core business processes. For example, in finance, Galaxy Securities' over-the-counter trading agent, developed in collaboration with Baidu Intelligent Cloud, tripled the conversion rate from customer inquiries to orders; in agriculture, a veterinary large model was developed for pig farming; in automotive, besides new energy vehicles, traditional fuel vehicles and heavy trucks are also implementing intelligent driving systems.

In critical industrial sectors, industry insiders told Shuzhi Qianxian that while many AI deployment scenarios remain unsolved, enterprise confidence in AI's value has significantly increased. In some effective scenarios, even if AI software currently delivers only 80% of traditional solutions' effectiveness at higher costs and with certain risks, many enterprises are still willing to invest, believing long-term efficiency will double.

Through continuous scenario exploration and validation, some high-value scenarios began to witness success in 2025, with intelligent agent products like predictive maintenance replicating from top clients to mid-tier and smaller clients.

Shuzhi Qianxian learned that a service provider has successfully deployed an equipment maintenance intelligent agent in the shipping sector, refining it into a standardized integrated hardware-software product for rapid replication. Another agent service provider developed an industrial energy-saving intelligent agent product, driving replication within client organizations and across industries, with business already fully booked for the first half of 2026.

During this window, both demand-side enterprises and supply-side cloud providers and AI service providers are fully committed to transitioning AI from pilot validations to large-scale value realization. Sources close to Baidu Intelligent Cloud revealed that the company has been in a "constant battle" state. Third-party data shows that in 2025, domestic mainstream cloud providers secured 341 large model-related bids totaling approximately 2.7 billion yuan. Among them, Baidu Intelligent Cloud ranked first for two consecutive years with 109 projects and 900 million yuan in bids, followed by Volcano Engine and Alibaba Cloud.

This business outcome is closely tied to Baidu Intelligent Cloud's early large model deployments and industry scenario co-creation. For example, in finance, it secured 38 projects in 2025, ranking first. In power scenarios, its Bright Power large model, developed in collaboration with State Grid, covers over 100 application scenarios, reducing manual tower inspections by 40%, and helped China Southern Power Grid build a new computing cluster. Its power distribution network monitoring agent can complete alarm analysis and notify sites within one minute.

Baidu has also begun exploring more complex scenarios, launching the commercially available self-evolving super intelligent agent "Baidu Famous Strategy" in November 2025. Capable of finding "global optimal solutions" in real industrial scenarios through self-evolving algorithms, it has attracted thousands of enterprise trials. For example, it helped Alte reduce single wind resistance verification time from 10 hours to 1 minute in automotive R&D; in finance, it assisted CITIC Baixin Bank in upgrading intelligent risk control, improving feature mining efficiency by 100%, risk model differentiation by 2.41%, and significantly enhancing risk control capabilities.

Building on this momentum, Baidu Intelligent Cloud further raised its 2026 growth target, indicating a deeper commitment to driving large-scale AI application deployment.

02

The Ultimate Battle in AI Cloud: Integrated Hardware-Software Solutions

As the industry moves toward large-scale intelligent agent applications, the early model of competing solely on cards and computing power scale is no longer viable. Intelligent agent industrialization demands three core elements: capability, cost, and speed.

Firstly, the cost issue looms large. IDC predicted in December 2025 that by 2026, 40% of jobs will involve collaboration with AI agents, and by 2027, global Fortune 2000 companies' agent usage will grow 10-fold with call volumes increasing 1,000-fold. However, as of January 2026 market quotes show, for public cloud services, overseas mainstream models charge $1-5 for input and $8-15 for output per million tokens; domestically, it's 0.8-4 yuan for input and 2-8 yuan for output. This cost structure cannot sustain large-scale AI commercialization.

Furthermore, China's core AI competitiveness lies in AI+application deployment. For AI to become a foundational resource like "water, electricity, and coal," costs must decrease significantly to support large-scale agent deployment and complete the "AI+" transformation.

Secondly, the speed issue is paramount. In the intelligent agent era, especially in enterprise markets, latency has become a critical metric. Financial fraud detection, quantitative trading, and live-stream e-commerce scenarios all require AI generation speeds below 10 milliseconds. More importantly, as most future interactions will occur between machines, the demands for generation and response speeds will far exceed human-machine interactions. Research from Tsinghua University and the China Software Testing Center (CSTC) clearly states that latency is the primary technical threshold directly determining user retention and differentiated competition.

Capability extends beyond model "intelligence." For intelligent agents to operate effectively in real industrial settings, models alone are insufficient. A complete engineering system spanning data, models, tools, scheduling, and maintenance is required to effectively utilize models.

Under these three pressures, the logic of AI cloud competition has shifted from computing power stacking to integrated hardware-software solutions, reconstructing unit computing power output efficiency. Reviewing multiple highly competitive technology markets, all have ultimately risen to chip-level hardware-software synergy. Take smartphone AI cameras as an example—ultimately, everything relies on chips, using AI chips to process each image frame for the fastest speed and lowest power consumption.

Compared to traditional CPU-based cloud computing, AI cloud software stacks are more complex. CPUs focus on virtualization, but for AI systems, integrated hardware-software solutions involve underlying chips, computing management platforms, and upper-layer models and tools. To achieve better performance, lower latency, and lower costs, computing infrastructure must innovate collaboratively at key points like system architecture, interconnection protocols, and software frameworks.

Globally, few AI cloud providers have truly implemented this model. Google is the most typical case. As early as 2015, Google launched its TPU chip self-development project, forming end-to-end capabilities across chips, frameworks (TensorFlow, etc.), models, and applications, differing from OpenAI's reliance on external computing power. Today, the Gemini series models are entirely trained and inferred on the TPU system, with 650 million monthly active users. Combined with massive application scenarios like search and Android, it has surpassed OpenAI on multiple levels. In Q3 2025, Google Cloud revenue grew by 34% year-on-year, with market recognition of its AI cloud system continuously improving.

Domestically, Baidu Intelligent Cloud follows a highly similar path. Baidu established its Kunlunxin team in 2011, forming systemic capabilities across chips, AI cloud, models, and applications. In 2025, the Kunlunxin P800 32,000-card cluster became operational, with Baidu migrating most inference tasks to its self-developed chip system; training a multimodal model now requires clusters exceeding 10,000 cards, with a "five-year, five-generation" strategy announced.

Above AI Infra, Baidu Intelligent Cloud's Agent Infra, through the Qianfan platform, provides the Wenxin large model and multimodel system, covering data services, tool calls, model customization, and enterprise-level agent construction to help clients embed intelligent agents into core business processes.

This evolutionary path did not happen overnight. Both Google and Baidu have built their integrated hardware-software capabilities through over a decade of continuous investment. As a result, they can more swiftly adapt to structural changes in industrial demand during the intelligent agent wave.

Shuzhi Qianxian learned that the industry is entering a new peak of large model iterations in spring 2026. Industry insiders anticipate key breakthroughs in multimodal, coding, and world models, again driving a new wave of application-layer explosions. During this critical window, Baidu Intelligent Cloud's decision to raise business growth targets sends a clear offensive signal. With multiple variables at play, 2026 may become the pivotal year that truly differentiates levels in this round of AI cloud competition.

-

![]()

【OFweek Weike Cup】YOFC Officially Enters for the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Mass Production Achieved and Delivered to Premier Clients! Sunny Optical Unveils Comprehensive Optical Coating Solutions

-

![]()

Model Crisis: Navigating the Challenges of AI Evolution

-

![]()

Securing 250 Million Yuan in Strategic Investment! How Does Aishun Optoelectronics Win the Favor of an Optical Industry Leader?

-

![]()

AI Won't Replace You, But Your Work Style Will Be Transformed by Agentic AI

-

![]()

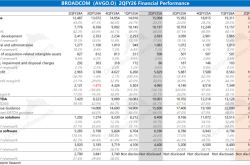

Broadcom AVGO: A Clash of Titans—Is the ASIC Camp Fragmenting?

-

![]()

Siri-like Assistants Gain Momentum: Will Humans Abandon 'App Tapping' in the Future?

-

![]()

Masayoshi Son's 'Revenge': From Defeat to Deification via AI, Regaining Asia's Richest Title After a Decade