The Hidden Downside of the AI Boom: Smartphones' Waning Influence

02/28 2026

02/28 2026

568

568

The Spring Festival has historically been a fiercely contested arena for smartphone manufacturers. However, this year, the market appears notably muted.

In shopping malls and phone stores, aside from Huawei, Apple, and Samsung, brands such as Xiaomi, Vivo, OPPO, and Honor have largely refrained from significant price reductions. Only a handful of models offer minor discounts through platforms or stores. Additionally, "zodiac-themed limited edition" phones have nearly vanished from the scene.

Even in the vast lower-tier markets, which typically experience heightened activity during the Spring Festival, smartphone sales are sluggish. At a phone store in a Hunan county, a young man frowned at the price tag of a new model, exclaiming, "Last year, it started at 1,999 yuan. Now it's 2,199 yuan?" Several mid-range models released during this year's Spring Festival holiday have seen their starting prices increase by 200 to 400 yuan, dampening consumer enthusiasm. Many consumers even prefer to spend the same amount on a two-year-old flagship model rather than a new release.

This phenomenon can be attributed to the soaring prices of memory chips, with the root cause lying in the AI technology wave. The computational arms race sparked by AI has significantly consumed memory production capacity that was once dedicated to the smartphone industry, leading to severe supply shortages. But is AI's impact on smartphones limited to this?

A Small Chip Causing Big Disruptions in the Smartphone Market

Before the holiday, Transsion Holdings, dubbed the "King of Africa," issued a gloomy earnings forecast that garnered widespread attention. According to the forecast, Transsion expects to achieve revenue of 65.568 billion yuan in 2025, down 4.58% from 68.715 billion yuan in 2024. Net profit attributable to shareholders is projected at 2.546 billion yuan, a staggering 54.11% drop from 3.003 billion yuan—effectively halving its profits.

Transsion's sudden decline vividly illustrates how rising memory chip prices first impact low-end phones. With limited pricing power and profit margins, the increased cost of memory—a core component—has rapidly eroded manufacturers' profitability. Transsion is not alone; low-end phones in the Chinese market are facing an unprecedented crisis, with manufacturers sharply revising downward their shipment forecasts for models priced around 1,000 yuan.

However, this may only be the beginning. Even more significant changes are unfolding in the vast mid-range market, which supports the majority of sales for most Chinese smartphone makers.

Mid-range phones cater to the largest user base. Among nearly 1 billion smartphone users in China, 500 million use mid-range models priced between 2,000 and 4,000 yuan. These devices once accounted for more than half of the smartphone market share. In recent years, the mid-range segment has become overcrowded with homogeneous products, while high-end models have encroached on their pricing territory, intensifying competition. Now, rising memory chip costs have exacerbated the situation.

Fundamentally, whether manufacturers choose to raise prices or reduce specifications, it undermines the cost-effectiveness that mid-range phones rely on for survival.

Facts bear this out. During the Spring Festival, the prevalence of higher new phone prices drove many consumers toward older models with slightly outdated chips but comparable memory configurations. A phone store owner pointed to display models and said, "Nowadays, many young people come in asking for flagship models from a couple of years ago."

According to IDC forecasts, by 2026, the market share of smartphones priced below $200 in China will shrink by 4.3 percentage points to 20.0%. The share for the $200-$400 segment will fall by 0.3 percentage points to 34.0%, while the $400-$600 segment will drop by 0.8 percentage points to 10.1%. Goldman Sachs analysis also indicates that the mid-range market share has plummeted from 35% in 2021 and is expected to decline to 23% by 2027.

However, as the low- and mid-end markets contract, the high-end segment is showing resilience and is poised to expand. IDC predicts that smartphones priced above $600 will capture 35.9% of the Chinese market, a 5.4 percentage point increase.

With fewer low-end models, sluggish mid-range sales, and an expanding but high-threshold high-end market, the industry's growing polarization may leave Chinese smartphone makers with limited room to maneuver. Pessimistically, this could drag the entire industry into a new slump.

On the surface, this is a normal chain reaction triggered by supply chain fluctuations. However, at its core, it reveals that while AI's technological wave brings innovative possibilities, it may also impose unpredictable impacts—or pressures—on the smartphone industry's development.

Smartphones No Longer Dominate the Top-Tier Supply Chain

The industry is generally pessimistic about how long the memory price surge will last.

Intel CEO Lip-Bu Tan stated bluntly that AI-related demand increases have strained traditional supply chains for PCs and smartphones, leading to memory chip shortages and sustained price hikes that will not ease before 2028. This aligns with UBS analyst team projections, which note that amid ongoing AI data center expansion, the global memory industry is experiencing significant structural differentiation. A "meaningful supply relief" is unlikely before around 2028.

In other words, the entire smartphone market will bear the pressure of insufficient upstream memory supply for the next two to three years. However, the industry's concerns extend beyond just this price hike. The booming AI industry, with its "siphon effect," is poised to compete for all core computing resources, from underlying chips, memory, and storage to end-user graphics cards, CPUs, and complete systems.

Moreover, the smartphone industry—long a dominant force in the consumer electronics market—is losing its absolute grip on premium supply chain resources.

From current chipmakers' capacity allocations, it is inevitable that resources will shift toward AI-related businesses. The three major memory chip giants—Samsung, SK Hynix, and Micron—increased their production capacity for data center-grade memory chips to over 40% in 2025, up 15-20 percentage points from 2023. At TSMC and Samsung's foundry businesses, capacity reserved for AI chips (such as GPUs and ASICs) continues to grow, squeezing production space for consumer-grade chips.

A tech industry observer noted that the current capacity allocation priority is: AI > servers > data centers... with smartphones and PCs at the bottom of the list.

Over the past decade, smartphones have driven unprecedented prosperity in the mobile internet economy, fostering a vast, mature supply chain encompassing cutting-edge manufacturing technologies. Apple, in particular, has long occupied the core of this supply chain, wielding priority supply rights, strong bargaining power, and direct influence over suppliers' R&D directions.

However, Apple's "hegemony" in the supply chain has weakened. It is no longer the top priority customer for wafer foundries, substrate manufacturers, or key component suppliers—AI giants have taken that role.

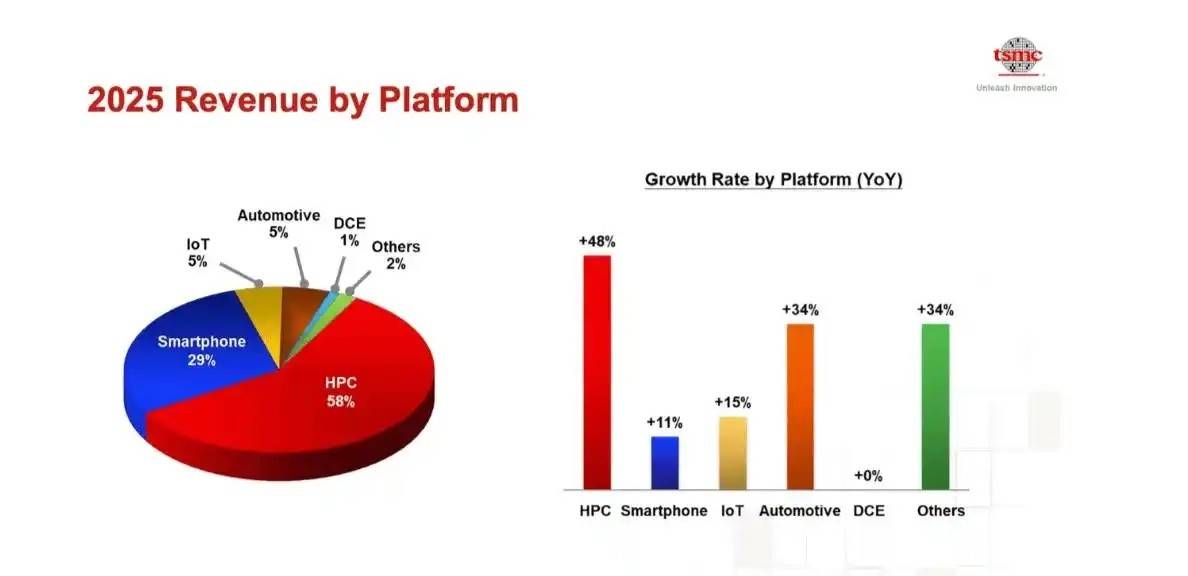

Take TSMC as an example. Its high-performance computing business, which primarily manufactures AI chips for NVIDIA and large-scale cloud service providers, now accounts for about 58% of its revenue—far exceeding the 29% from smartphone processor business. Consequently, Apple must compete with AI giants for TSMC's capacity and accept increasingly higher prices. Additionally, in memory supply negotiations, Apple has been forced to adjust its procurement cycle. Analyst Ming-Chi Kuo stated that Apple's memory supply negotiations have shifted from traditional semi-annual talks to quarterly consultations.

If even Apple faces such challenges, other smartphone manufacturers are even more powerless against AI giants' capacity squeezes.

The Race to Replace Smartphones Has Begun

The AI industry's development has created a "siphon effect" on consumer electronics, weakening smartphones' supply chain influence. Meanwhile, AI technological breakthroughs offer hope for innovating existing smart hardware while sparking competition for the next mainstream device. In the end-user market, this undoubtedly challenges smartphones' dominance.

Currently, tech giants are already making moves. First, AI "newcomers" like OpenAI are secretly advancing R&D on a series of native AI hardware devices. Recent reports indicate that OpenAI plans to launch its first AI-powered speaker with a camera in 2027, alongside smart glasses, smart lamps, and other hardware products.

Second, internet tech giants like Meta are leveraging their strengths and AI accumulations to introduce new smart hardware. Meta, for instance, is prioritizing smart glasses development. Its Ribbon Meta series smart glasses, created in partnership with Ray-Ban, have sold millions of units, becoming a key pillar in its post-smartphone era strategy.

Chinese tech giants also cannot be ignored. ByteDance, which recently caused a stir online with its "Doubao Phone," uses its "Doubao Phone Assistant" to enable AI to understand smartphone screens and simulate clicks, achieving "automatic phone operation." This showcases another possibility for future AI phones and fuels imagination around highly autonomous smart agents.

Compared to these imaginative and controversial smart hardware devices, smartphones' integration with AI has yielded lackluster results.

While many AI phones now dominate the smartphone market, they mostly represent "old wine in new bottles"—merely enhancing existing AI features on phones without delivering innovative experiences. Most users have not even perceived the "intelligence" of these so-called AI phones.

Of course, given the current sales of products like smart glasses, new smart hardware poses minimal threats to smartphone giants for now. However, the AI wave will continuously spawn more intelligent products that will inevitably compete with smartphones for users and attention. Once they penetrate deeper into the user base and scale up, smartphones' long-standing position as consumer electronics market leaders may vanish.

This applies not just to hardware but to the entire technological and application ecosystem built around smartphones. Google's integration of Gemini technology into Apple's ecosystem hints at looming crises. If smartphone giants fail to master core technologies in the AI era, they may soon cede control and rely on external forces for product upgrades.

The AI wave initially offered hope for reviving the sluggish consumer electronics industry. However, for smartphones, it raises a critical question: Is this hope or crisis?

Dao Zong You Li, formerly known as Waidaodao, is a new media outlet covering the internet and tech sectors. This is an original article. Any form of reprinting without retaining the author's information is strictly prohibited.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once