Over 100 Billion Invested in Three Years: Baidu's AI Business 'Must' Lead the Charge

02/28 2026

02/28 2026

441

441

"In the foreseeable future, revenue from core AI businesses will constitute half of Baidu's main business revenue."

In February 2026, Baidu released its unaudited financial report for the fourth quarter and full year of 2025. This report marks a milestone for Baidu: it not only signifies Baidu's strategic move to officially place AI business at the forefront but also, for the first time, provides a detailed breakdown of its AI business revenue composition to the market.

As Baidu CEO Robin Li stated, 2025 was a pivotal year for AI to become Baidu's new core.

Starting from the fourth quarter of 2025, Baidu redefined its core business as Baidu's general business. Hence, in terms of financial reporting, Baidu's general business includes Baidu's core AI new businesses (intelligent cloud infrastructure, AI applications, and AI-native marketing services), traditional businesses (search and information feed advertising), and others.

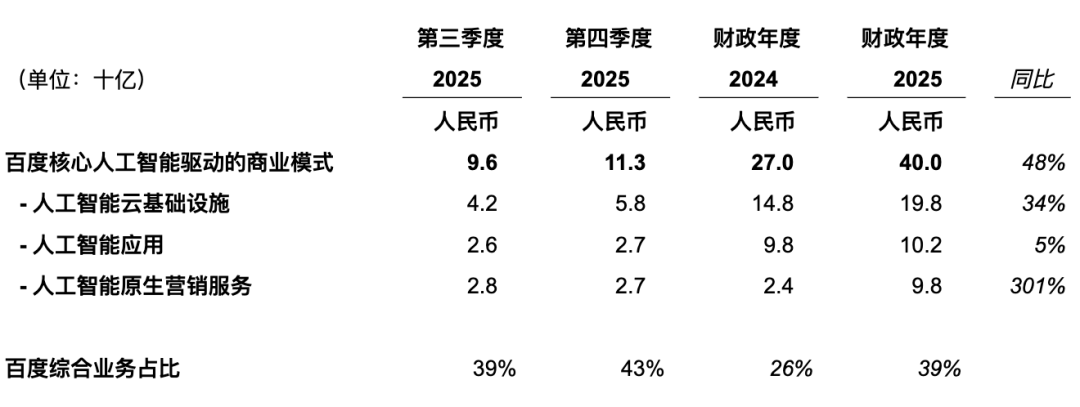

Baidu's Core AI Business Revenue

Baidu's Core AI Business Revenue

Although traditional businesses still hold a slight edge in scale, the growth rate of AI new businesses is more pronounced. Data shows that Baidu's total revenue in 2025 was 129.1 billion yuan, with AI business revenue reaching 40 billion yuan. In the fourth quarter, AI business revenue accounted for 43% of Baidu's core business, dispelling the market's stereotype of Baidu as just an "advertising company."

Based on this, Robin Li made the initial judgment.

During the subsequent conference call, Robin Li also provided an update on the progress of various AI businesses. When asked whether "Robotaxi business Luobo Kuaipao would be spun off and listed," Robin Li did not provide a clear response but stated that the entire autonomous driving industry's value is currently underestimated. As the industry develops, market valuations will gradually reflect the transformative potential of this technology, and Luobo Kuaipao will also see significant value appreciation.

However, behind the impressive AI data, Baidu also faces multiple concerns, including the decline of traditional businesses, profit pressures, and high transformation costs.

Baidu CFO Hai Jian He revealed that since the release of Wenxin Yiyan in 2023, Baidu's cumulative investment in the AI field has exceeded 100 billion yuan.

Now, it's time for AI to 'lead the charge.'

01

Robotaxi, Large Models, and AI Cloud: A Comprehensive Offensive

If Baidu's previous financial reports were still telling the story of AI, the 2025 report aims to prove AI's 'profitability' with data.

Robin Li introduced that in the fourth quarter of 2025, Baidu's AI business revenue exceeded 11 billion yuan, accounting for 43% of Baidu's main business revenue. Artificial intelligence has become the core engine driving Baidu's overall revenue growth.

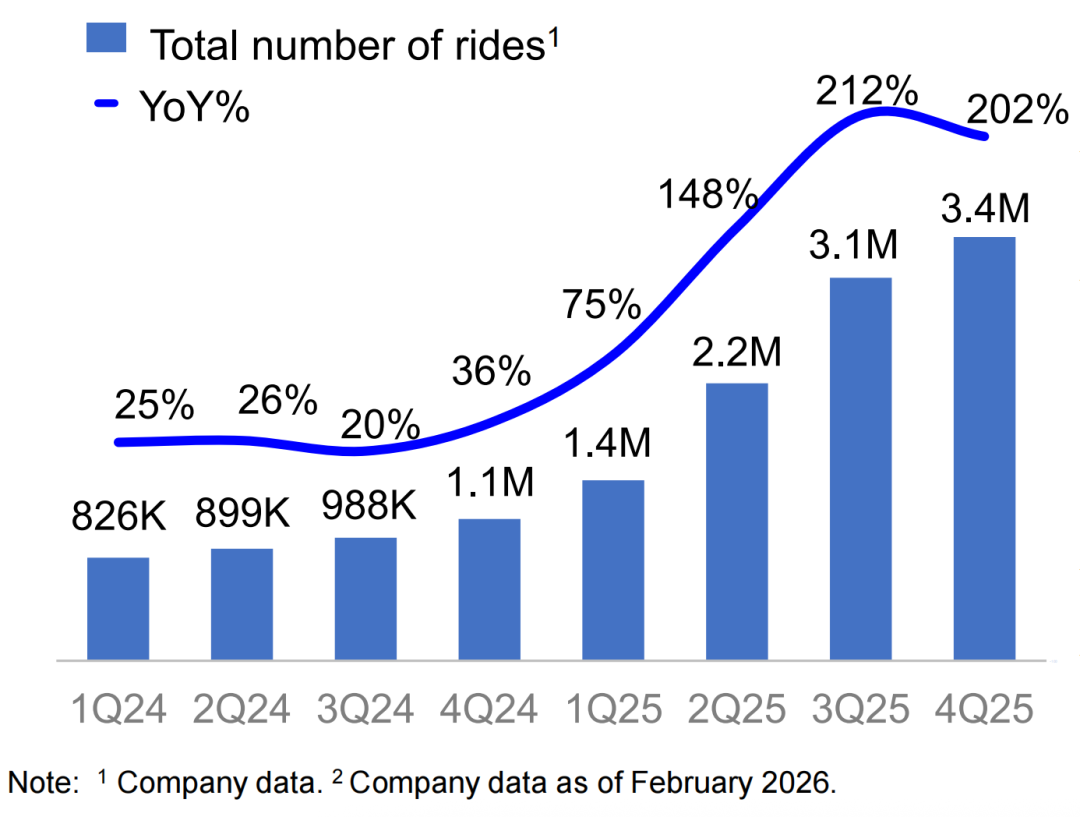

As a model of physical AI implementation, Luobo Kuaipao saw explosive growth in 2025. In the fourth quarter, Luobo Kuaipao provided 3.4 million fully driverless ride-hailing services, a year-on-year increase of over 200%. As of February 2026, cumulative orders have surpassed 20 million.

Progress of Baidu's Robotaxi Business

Progress of Baidu's Robotaxi Business

Meanwhile, Luobo Kuaipao is accelerating its global expansion. As of February 2026, its global operations cover 26 cities. To date, the fleet has accumulated over 300 million kilometers in autonomous driving, with over 190 million kilometers in fully driverless mode.

In Robin Li's view, the Robotaxi industry will see accelerated development in 2026. Besides operational data, Luobo Kuaipao also has a core cost advantage. "The sixth-generation vehicle is the world's first mass-produced model specifically designed for L4 autonomous driving, with a cost per unit below $30,000."

According to him, in Wuhan, where Luobo Kuaipao has the most deployments domestically, Bicycle profit and loss balance (per-vehicle break-even) was achieved by the end of 2024. Most major cities have higher pricing for mobility services than Wuhan.

Based on this, Luobo Kuaipao will focus on three main directions in the future: deploying more vehicles; continuously optimizing the unit economic model, aiming to achieve profitability in more cities by 2026; and adopting flexible business models to continuously expand markets domestically and internationally.

Baidu's Sixth-Generation Robotaxi Driverless Vehicle RT6

Baidu's Sixth-Generation Robotaxi Driverless Vehicle RT6

Robin Li believes that Luobo Kuaipao holds significant strategic potential. On the one hand, many large cities currently face a shortage of drivers. The implementation of driverless mobility services not only provides safer travel options but also stimulates travel demand and increases tax revenue for governments. On the other hand, it frees up valuable land resources occupied by parking lots, creating more commercialization opportunities for real estate assets.

Regarding whether it will be spun off and listed, Robin Li stated that Baidu will remain open and evaluate all ways to create long-term value for shareholders. "Of course, our core remains efficient execution and sustainable growth."

Compared to Robotaxi, the competition in large models has been more intense and rapid in recent times.

"In competition, we always believe that applications are more important than models because the value of models is ultimately realized through applications," Robin Li said. This is also the approach taken in each iteration of the Wenxin large model.

According to him, Baidu recently released the 2025 upgraded version of the Wenxin large model while proactively adjusting its organizational structure. "We split the large model R&D team and laid out different directions: one team continues to tackle the cutting-edge capabilities of foundational large models to maintain technological leadership; the other team is closer to specific business needs and application scenarios, focusing on cost reduction, efficiency improvement, and speed enhancement, or selecting the most suitable models for specific scenarios. The core is to help enterprises better implement artificial intelligence based on actual needs."

In addition, Baidu Intelligent Cloud performed outstandingly in 2025, with AI cloud revenue increasing by 34% year-on-year, of which AI infrastructure revenue reached approximately 20 billion yuan. In the fourth quarter, subscription revenue for AI high-performance computing facilities surged by 143% year-on-year.

Shen Dou, President of Baidu Intelligent Cloud Business Group, is confident in maintaining strong growth in 2026, driven by the accelerating implementation of enterprise artificial intelligence. "Currently, demand for both training and inference is increasing, and we expect the demand for artificial intelligence computing to continue to expand."

Kunlun Core's Five-Year Development Roadmap

Kunlun Core's Five-Year Development Roadmap

Supporting the growth of Baidu's various AI businesses is its self-developed Kunlun Core. In November 2025, Baidu Intelligent Cloud released the new-generation Kunlun Core and Tianchi Hypernode and announced that new Kunlun Core products would be launched annually over the next five years. Among them, the Kunlun Core M100 is optimized for large-scale inference scenarios, offering ultimate cost-effectiveness, and will be launched in 2026; the Kunlun Core M300 is designed for training and inference of ultra-large-scale multimodal models, providing ultimate performance, and is expected to be launched in 2027.

Hai Jian He revealed that the preparatory work for Kunlun Core's listing is progressing smoothly. "We believe that the spin-off and listing of Kunlun Core will receive high market recognition, unlocking tremendous value for Baidu as a whole."

02

Pressure from Traditional Business 'Bleeding' and New Business 'Filling In'

Despite the good news from the AI business, Baidu's 2025 financial report also reveals many concerns.

First is the continuous decline of the traditional advertising business.

As a former revenue pillar, Baidu's traditional online marketing business is facing irreversible decline. In the fourth quarter of 2025, revenue from traditional businesses (mainly search and information feed advertising) was 12.3 billion yuan. Although still slightly higher than the 11.3 billion yuan from AI new businesses, it already shows signs of fatigue.

With emerging content platforms like Douyin and Xiaohongshu continuously diverting advertising budgets and AI search disrupting traditional search models, Baidu's core business still faces challenges. The 3% decline in total annual revenue directly reflects the difficulty of sustaining the old model reliant on traditional business 'blood transfusions.'

Second is the significant decline in net profit and high transformation costs.

Although profit after excluding non-recurring items is still acceptable, the 76% drop in net profit remains a sword hanging over investors' heads.

The financial report shows that to fully increase investment in cutting-edge artificial intelligence computing technology, Baidu conducted a comprehensive assessment of its existing infrastructure assets. As some assets could no longer meet current computing efficiency requirements, Baidu wrote off 16.2 billion yuan in long-term asset impairments within the year. Although a one-time operation, it exposes the rapid iteration speed of AI technology: yesterday's core assets may face obsolescence today.

According to Hai Jian He, since the release of Wenxin Yiyan in 2023, Baidu's cumulative investment in the AI field has exceeded 100 billion yuan.

In the future, to maintain its leading position in areas like large models and autonomous driving, this high-intensity capital expenditure will continue. Finding a balance between huge investments and profit returns is a long-term challenge for the CFO.

Third is the fierce competition faced by C-end products.

Although Wenxin Assistant has surpassed 200 million monthly active users, the "AI Red Packet War" during the Spring Festival also shows the intensifying market competition. Currently, in the Apple App Store's popular downloads, Doubao and Qianwen rank first and second, respectively, while Yuanbao ranks tenth, with no sign of the Wenxin app.

Luo Rong, Executive Vice President of Baidu Group, admitted during the earnings call that competitors have adopted aggressive market strategies. This indicates that in the C-end traffic acquisition war, although Baidu has the Stock advantage (existing user base advantage) of search entry, it still faces significant challenges in acquiring and retaining users for independent apps, along with potential pressure from user acquisition costs.

03

The Difficult Transition to 'Stop the Bleeding' with AI

From a core financial perspective, Baidu is at the intersection of pain and harvest during the transition from old to new growth drivers.

A noticeable change is the qualitative shift in revenue structure.

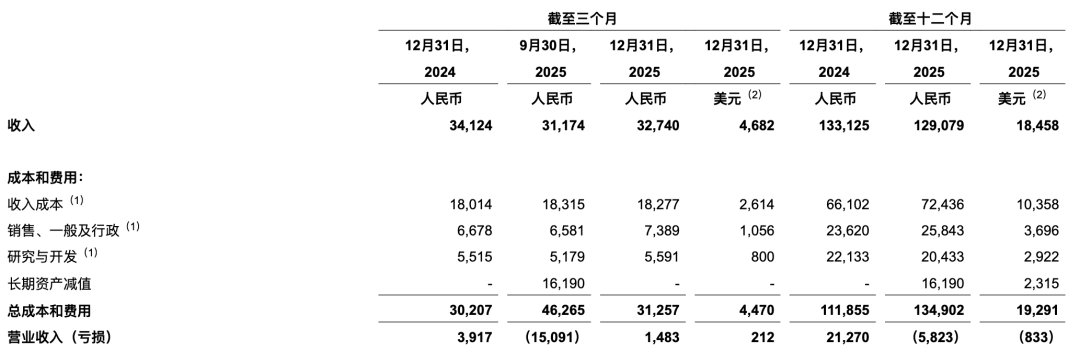

In 2025, Baidu's total revenue was 129.1 billion yuan, a 3% year-on-year decline. This reflects the broader trend of Baidu's revenue decline over multiple quarters, primarily due to the continuous contraction of traditional search advertising business.

Under this pressure, the growth of new businesses becomes particularly crucial. In the fourth quarter, Baidu's core AI new businesses contributed 11.3 billion yuan in revenue, the "bright spot" in the financial report.

Baidu's Financial Information

Baidu's Financial Information

Baidu's profitability faces challenges.

The financial report shows that Baidu's net profit attributable to the company in 2025 was 5.6 billion yuan, a significant 76% decrease from 23.8 billion yuan in 2024.

This is mainly due to the one-time write-off of 16.2 billion yuan in long-term asset impairments during the reporting period to eliminate outdated infrastructure that could no longer meet current AI computing efficiency requirements. After excluding this impairment and Non-GAAP adjustments, the adjusted net profit was 18.9 billion yuan, a 30% year-on-year decrease.

Meanwhile, R&D expenses also declined. In 2025, Baidu's R&D expenses were 20.4 billion yuan, an 8% year-on-year decrease, mainly due to reduced personnel-related expenses.

However, as of the end of 2025, Baidu's operating cash flow turned positive in the second half of the year, generating a total of 3.9 billion yuan.

Based on this, Baidu announced two major shareholder return plans in early 2026: first, the board approved a new stock repurchase plan of up to $5 billion (approximately 10% of the market value); second, the company adopted a dividend policy for the first time in its history, expecting to pay its first dividend by the end of 2026.

Looking at the 2025 financial report, it serves as Baidu's declaration of a complete transformation into an "AI company." The 43% revenue share, AI investments in the hundreds of billions, and the first disclosure of billion-dollar AI application revenue all prove the initial success of its strategy. However, it should be noted that this achievement was made against the backdrop of traditional business decline and profit pressure.

For Baidu, AI business is no longer just the "stars and the sea" for storytelling but the "prime time" that must lead growth. How to quickly fill the gaps left by old businesses with new business profits while maintaining high-intensity investments will be Baidu's biggest test in 2026 and beyond.

-END-

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once