AI’s Promise Shines, but NVIDIA Shouldn’t Be the Sole Star

02/28 2026

02/28 2026

606

606

The AI boom is real, not a speculative bubble, and its validity cannot be judged solely by NVIDIA’s performance.

Written by | Landong Business Zhao Weiwei

NVIDIA once again reported stellar financial results, only to see its stock price drop 5.7% the next day. While the AI industry bubble has yet to materialize, market sentiment remains a mix of optimism and skepticism.

Revenue surged 73% year-over-year to $68.1 billion; data center revenue hit $62 billion, up 75% year-over-year; net profit soared 94% year-over-year to $42.9 billion. Despite significant price hikes in components like memory, gross margin reached 75.2%. More importantly, NVIDIA raised its revenue guidance for the next quarter to $78 billion, excluding data center computing revenue from the Chinese market.

These are NVIDIA’s recently released fourth-quarter results, which continue to demonstrate strong momentum and boost confidence in the AI market.

However, on the flip side, the market has grown accustomed to such extraordinary performance, as NVIDIA has exceeded revenue expectations for 14 consecutive quarters. Even with these significantly better-than-expected results, NVIDIA’s stock price rose just 1.41% on the day of the announcement and fell 5.7% the next day. Over the past seven months, NVIDIA’s stock price has been hovering near its all-time highs, struggling to replicate the rapid valuation growth seen two years ago.

High valuations amplify market sensitivity. If the vast majority of AI spending flows solely to NVIDIA, short-term sentiment will become increasingly reactive to its valuation.

More critically, NVIDIA’s strong financial performance has raised pressure across the AI industry. The impact of AI coding tools and intelligent agents on enterprise software continues, and questions linger about when downstream infrastructure and “AI factories” will see prosperity. How can their revenue growth keep pace with NVIDIA’s profit surge? Will AI-related revenue proportions increase for Microsoft, Google, and other major tech firms? These questions demand clearer answers in their upcoming financial reports.

The AI boom is real, not a bubble, and its legitimacy cannot be proven by NVIDIA alone. The more profitable the upstream sector becomes, the stronger concerns grow about downstream returns.

During NVIDIA’s earnings call, “Token” emerged as a key term frequently mentioned by founder Jensen Huang. Inference has shifted from a cost center to a direct revenue generator, with Tokens defining a new economic model. “Computing demand is growing exponentially—the inflection point for Agentic AI has arrived.” “In the new AI world, computing equals revenue. Without computing, there is no way to generate Tokens; without Tokens, there is no way to grow revenue.”

Thus, for the AI market, NVIDIA’s performance remains a stabilizing force, but the focus is on how to convert computing power investments into a true revenue engine and how to extend the logic of AI infrastructure construction to AI application monetization.

Infrastructure Profits Remain Optimistic

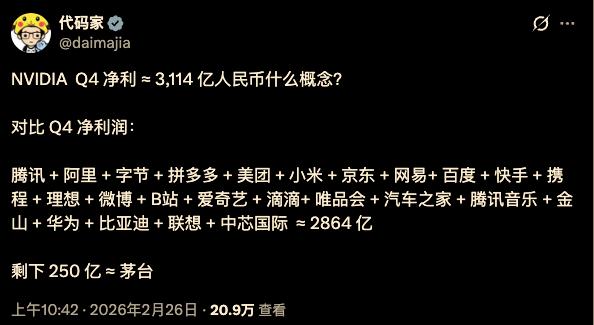

Emotions often outweigh facts. After NVIDIA’s financial results were released, a meme circulated widely on social media.

The author compared the profit data of Chinese concept stocks in the fourth quarter of 2024 with NVIDIA’s profit data for the fourth quarter of 2025, aiming to highlight NVIDIA’s extreme profitability, which significantly surpasses that of mainstream Chinese internet companies. Despite flaws in statistical dimensions, the meme was exaggerated enough in terms of communication and emotional impact.

More importantly, it reflects a market sentiment of resistance, suggesting that NVIDIA’s profits and market value have peaked, and the premium for upstream suppliers in the AI gold rush is excessively high. People are growing increasingly impatient, while downstream AI application companies have yet to achieve a major breakthrough, especially Chinese concept stocks, which have not yet reaped corresponding returns from the AI competition.

Customers invest heavily in NVIDIA’s GPUs but ultimately need to achieve profitability at the application level to sustain the AI economy.

Today, NVIDIA continues to surge ahead, proving that the AI bubble has not arrived on at least three fronts: significantly better-than-expected results, gross margins unaffected by memory price hikes, and strong guidance for the next quarter.

Especially in terms of gross margin, despite industry-wide impacts from rising memory and optical module prices, NVIDIA maintained a Non-GAAP gross margin of 75.2%, up 1.7% year-over-year, reaching a one-and-a-half-year high. This demonstrates NVIDIA’s ability to optimize inventory write-downs, benefiting from the ramp-up of its new generation Blackwell chips, which offer superior product and cost structures.

In its guidance for the next quarter, NVIDIA continues to build an irreplaceable integrated solution barrier with “computing power + interconnectivity + systems.”

Demand for AI computing power has not diminished and continues to generate a steady stream of orders for NVIDIA. Compared to industry analysts’ expectations of $72.7 billion, NVIDIA’s guidance for the next quarter is expected to reach $78 billion, with a 2% fluctuation range. This means that even taking the midpoint of the guidance, NVIDIA’s performance will be 4% higher than the most optimistic expectations, with revenue surging 77% year-over-year.

More notably, AI demand is diversifying into more markets, continuously contributing to NVIDIA’s revenue.

OpenAI, Oracle, Microsoft, Meta, and Google’s parent company Alphabet are all major buyers of NVIDIA’s chips. Revenue from hyperscalers accounts for over 50% of NVIDIA’s total, remaining the largest customer category. However, more revenue growth in the quarter came from non-hyperscale data center customers, indicating that NVIDIA’s ecosystem has further expanded to meet customer diversity.

Huang mentioned that NVIDIA’s CUDA ecosystem is the only accelerated computing platform deployed in every cloud, accessible through every computer manufacturer, and available at the edge. Various open-source projects running on the CUDA ecosystem make it the world’s second-largest model collection, with OpenAI being the largest.

Why Do Bubble Concerns Persist?

Despite releasing better-than-expected results and providing strong guidance for the next quarter, NVIDIA cannot shake off the shadow of stock price declines. Concerns over an AI bubble have persisted in the market in recent months.

AI Agents brought by artificial intelligence are poised to disrupt the software industry, and “AI replacement” is putting pressure on the entire tech sector. Represented by Microsoft, its stock price has fallen 17% in just two months since the beginning of 2026. Microsoft Azure’s cloud business grew 39% in the fourth quarter, far below Google Cloud’s 48% growth, and capital expenditures continue to increase. Investors are dissatisfied with Microsoft’s decision to allocate more computing resources to internal projects.

If the software industry is replaced, will there still be a need for so many GPUs?

Behind this logic is the anxiety over AI replacement, driven by the pressure from the popularity of AI agents like OpenClaw. As AI agents become tools for low-cost automated work, they may erode traditional SaaS revenue, leading enterprises to shift IT spending toward building their own Agents instead of purchasing software, ultimately dragging down demand for AI infrastructure.

Despite market doubts about AI’s prospects, NVIDIA remains the only company among the seven major U.S. tech giants to see its stock price rise this year. However, the ongoing excitement over infrastructure construction is raising increasing concerns in the market. This year, Alphabet, Amazon, Meta, and Microsoft are expected to spend a total of $610 billion, with Amazon’s capital expenditures exceeding $200 billion.

But Huang clearly stands on the opposite side of this logic, believing that computing is the future and Tokens represent productivity.

“Traditional software + Agents” is a more mainstream narrative, as AI will bring efficiency improvements. Whether it's Meta deploying millions of NVIDIA Blackwell chips or Anthropic receiving $10 billion in investment and conducting inference on its platform, both point to amplified demand for computing power. Huang believes, “Without sufficient computing, Tokens cannot be generated; without Tokens, enterprises cannot grow revenue.”

Computing power equals revenue. Spending real money is not the issue, but delivering tangible returns is the true logic to dispel AI bubble concerns.

Therefore, short-term market concerns over an AI bubble will persist. The market is not just testing NVIDIA’s profitability but whether the overall return on investment in the entire AI industry chain can be delivered, turning “AI spending” into “AI profit expansion” rather than just burning money.

In the long run, the AI economy has evolved from the “infrastructure construction” phase to the “commercial monetization” phase, a necessary stage for any industry’s growth. Once investments at the application layer translate into high-profit expansion, the market will form a positive cycle, with traditional software industries reshaping themselves with AI and cloud service providers achieving higher returns, enabling NVIDIA to drive trillion-dollar-level new computing power demand.

The Transition Period's Test Continues

The shift from “infrastructure construction” to “commercial monetization” represents a prolonged transition period for many Chinese companies. Baidu’s performance serves as a microcosm of the transformation faced by many AI companies: AI business is surging, but the decline in traditional business continues.

Baidu’s latest financial results for the fourth quarter and full year of 2025 show a 4.1% year-over-year decline in fourth-quarter revenue to 32.7 billion yuan, with net profit at 1.8 billion yuan. For the full year of 2025, Baidu’s revenue was 129.1 billion yuan, down 3% year-over-year, and net profit attributable to shareholders (net profit attributable to parent company) under non-GAAP was 18.9 billion yuan, down 30% year-over-year.

Notably, AI-related new businesses, including smart cloud infrastructure, AI applications, and AI-native marketing services, accounted for 43% of general business revenue, contributing over 11 billion yuan in revenue, up from 39% in the previous quarter. Among them, the AI cloud business performed particularly well, with annual revenue reaching 30 billion yuan for the first time.

A real pain point of this transition is financial pressure. Baidu’s financial report disclosed a long-term asset impairment loss of 16.2 billion yuan, amplifying the pain points of AI transformation. To meet future demand, old assets that no longer meet current AI computing efficiency requirements must be actively impaired to optimize the asset portfolio and better support investments in the latest AI technologies.

Despite pressure on traditional businesses, Baidu stated in its earnings call that it will maintain its AI investment intensity, a concern for the market.

“Even with significant AI investments, future operating cash flow will remain positive,” Baidu said. It achieved positive operating cash flow in the third quarter of last year, with 2.6 billion yuan in operating cash flow and 637 million yuan in free cash flow in the fourth quarter, indicating steady improvement in operating conditions.

The inflection point of the transition period remains to be seen. Baidu’s decade-long investment in Kunlunxin will also become a crucial asset in advancing its AI business. In January this year, Baidu announced the independent listing of Kunlunxin, the core carrier of its AI chip business, which will drive greater value growth in Baidu’s infrastructure construction and establish it as an “AI hard tech asset,” making it one of the few Chinese vendors with full-stack technical capabilities in “chips-frameworks-models-applications.”

How to control unit marginal costs amid exponentially growing computing power consumption is a challenge faced by Baidu and many other Chinese internet companies. With the upcoming release of the latest financial results from internet companies like JD.com, Tencent, and Meituan in March, answers will emerge regarding AI capital expenditures and return realization.

After the AI red envelope user acquisition battle during the Chinese New Year, will 2026 bring more surprises in terms of monetization capabilities for Chinese AI products?

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once