Salesforce: Will AI Substitution Theory Crush It, Has the SaaS Leader Become a 'Pariah'?

02/28 2026

02/28 2026

605

605

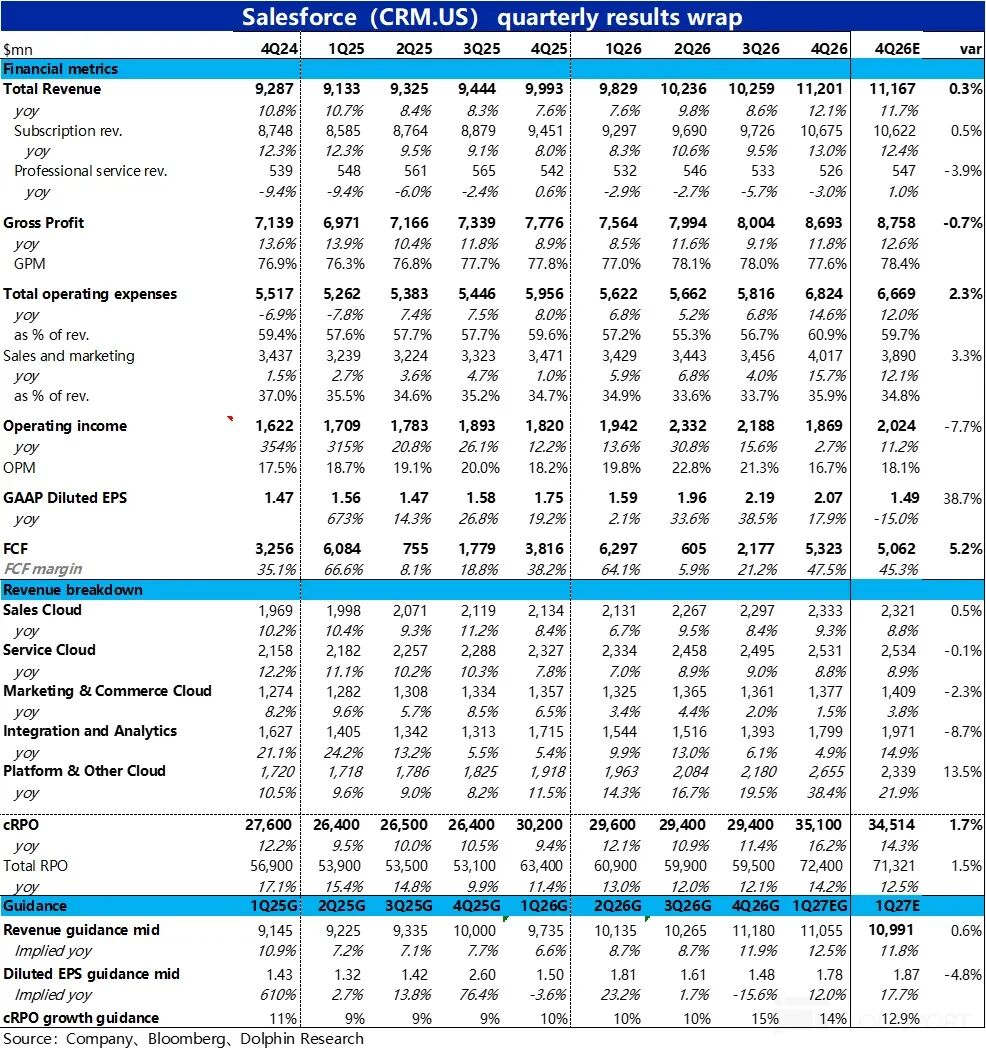

Recently, under the narrative of 'AI kills SaaS,' CRM, one of the hardest-hit sectors, released its Q4 FY2026 earnings report (as of January 31) after the market closed on February 25 (US Eastern Time). Overall, performance was mediocre.

Revenue growth did accelerate slightly as expected, but this was mainly due to the impact of acquisitions and consolidations. The growth of existing businesses remained weak. Gross margins continued to decline under pressure, and expenses increased significantly across the board, causing GAAP operating profits to significantly fall short of expectations. Another core metric—the growth rate of the short-term unfulfilled balance of cRPO—also fell short of buyer expectations, resulting in negative market feedback.

A detailed look:

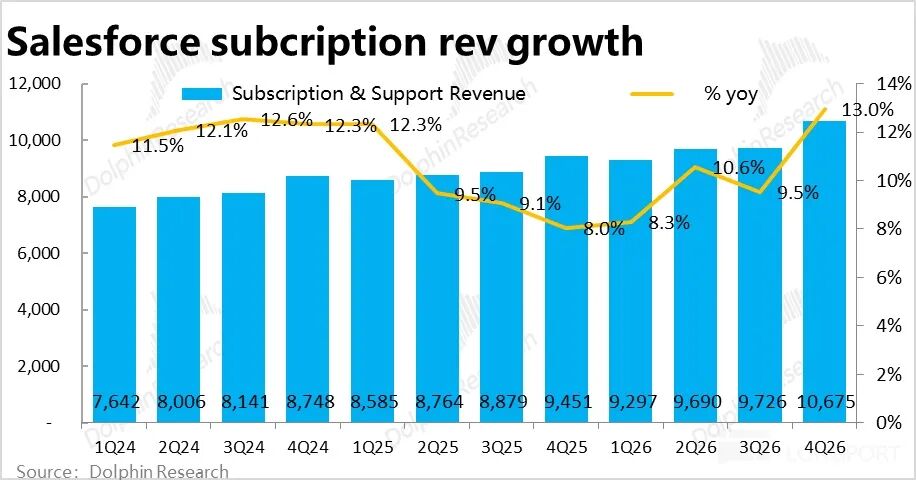

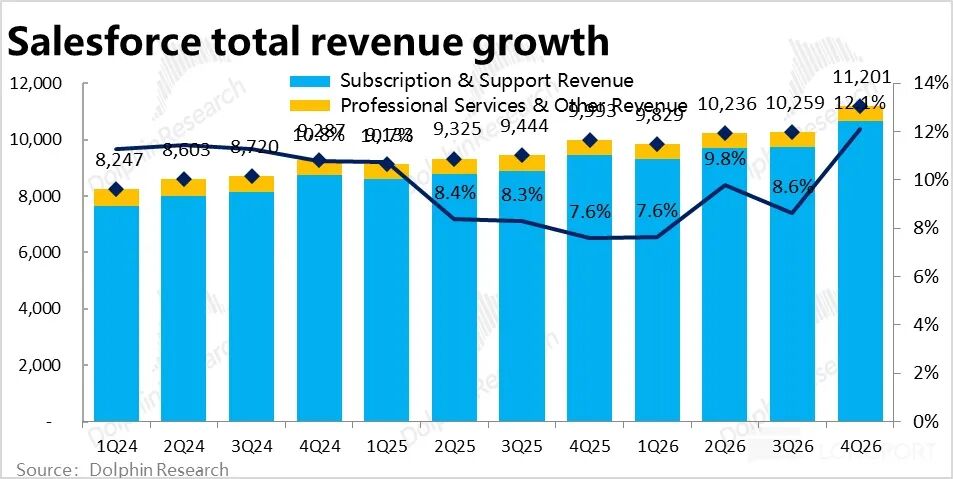

1. Growth Appears to Accelerate but is Actually Slowing Down: In this quarter, core business—subscription revenue—grew 13% year-over-year, or 11% excluding favorable exchange rates, accelerating by 2 percentage points from the previous quarter. However, 4 percentage points of this growth came from the contribution of the consolidated Informatica. After excluding this impact, the growth of existing businesses actually slowed down.

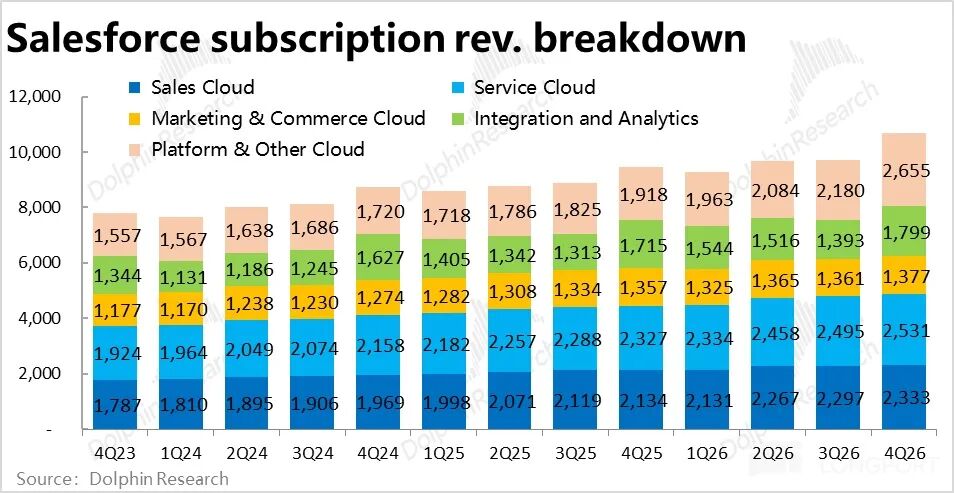

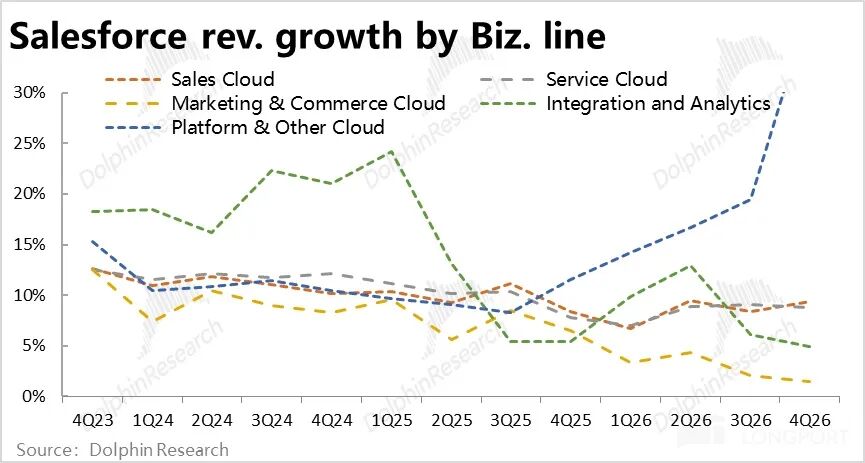

Breaking it down by business line, except for the platform cloud, which absorbed Informatica and saw a significant acceleration in growth, the growth of other business lines (at constant exchange rates) generally declined sequentially, with the best performing roughly flat. It is evident that although the company's previous guidance expected revenue growth to bottom out and rebound, there was little sign of this as of this quarter.

2. AI Business Revenue Accelerates Slightly but is Still Very Early: In this quarter, the annualized revenue of the Data & Agentforce business reached $2.9 billion, but about $1.1 billion of this came from consolidations. After excluding this impact, AI-related revenue grew 29% sequentially, marking the fastest growth since this data was disclosed.

Among this, annualized revenue from Agentforce reached $800 million, up nearly 170% year-over-year. The company's AI business growth did accelerate slightly. However, in absolute terms, AI-related revenue accounted for less than 7% of total revenue, and Agentforce alone accounted for less than 2%. It is clear that customer adoption is still in a very early and trial stage, and 'acceleration' is only relative to this small base.

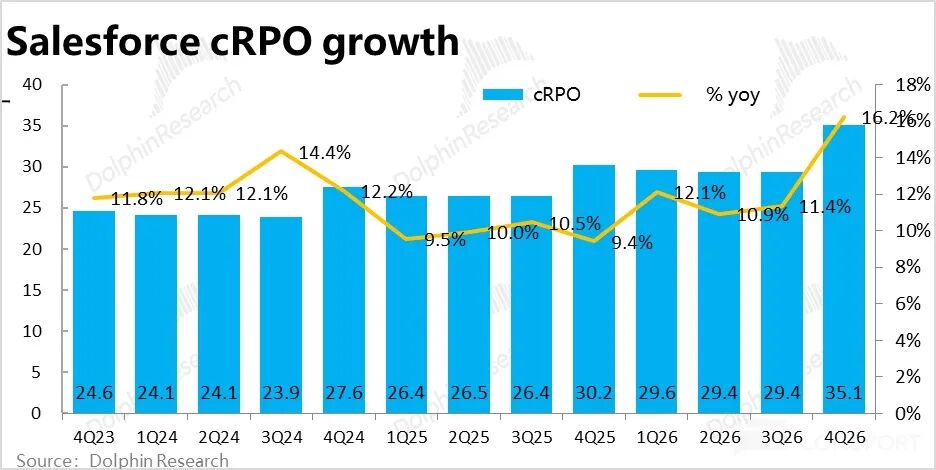

3. Leading Indicator Growth is Also Mediocre: Although the nominal growth rate of the core metric cRPO (short-term unfulfilled balance) surged to 16%, which looks good at first glance, after excluding favorable exchange rates, the actual year-over-year growth rate was 13%. Among this, 4 percentage points of growth also came from consolidations. After excluding this impact, the growth rate of cRPO for existing businesses actually slowed down compared to the previous quarter.

Dolphin Research understands that before the earnings release, optimistic buyer expectations were for a growth rate of 14%-15%. The actual performance was somewhat disappointing for bullish investors. Again, there was no sign of acceleration.

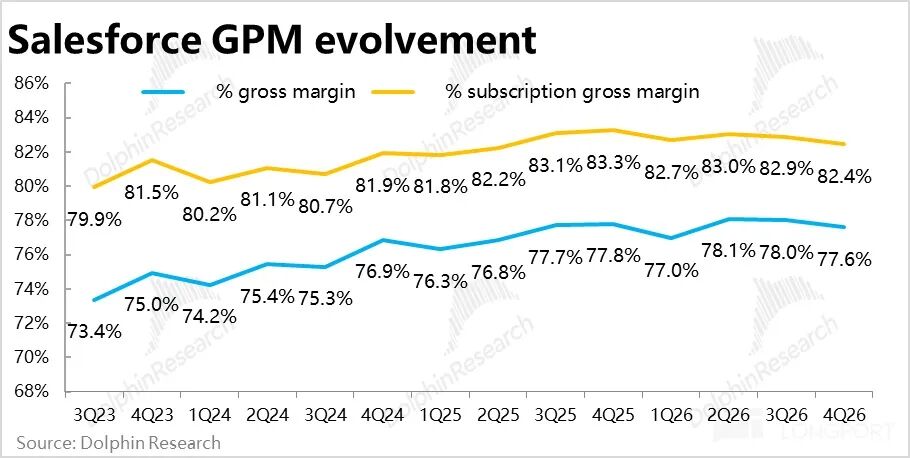

4. Gross Margin Continues to Decline Amid AI Investments: The trend of margin pressure continued this quarter, with the overall gross margin at 77.6%, slightly lower both year-over-year and sequentially, and below Bloomberg's expectation of 78.4%.

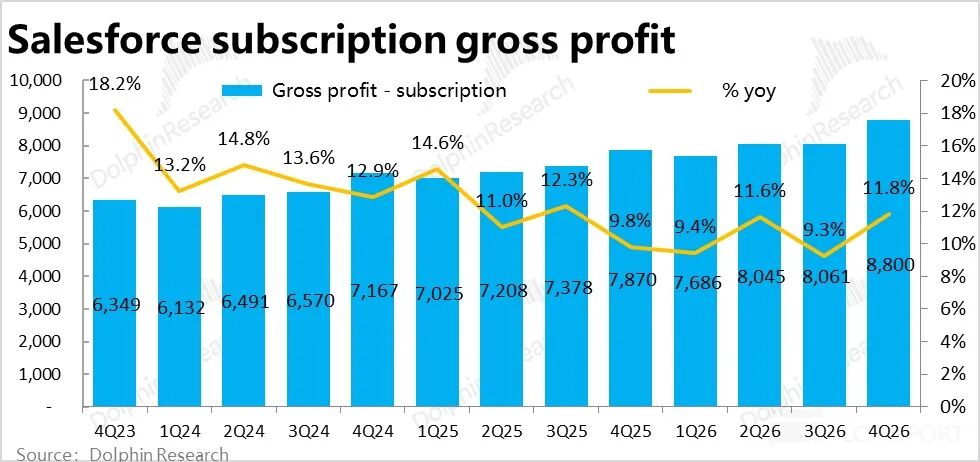

Looking solely at the core subscription business, the gross margin was 82.4% this quarter, down about 0.5 percentage points sequentially and nearly 1 percentage point year-over-year. Dolphin Research believes this is likely due to the drag of AI-related businesses such as Agentforce, which require more backend computing power and thus have lower margins.

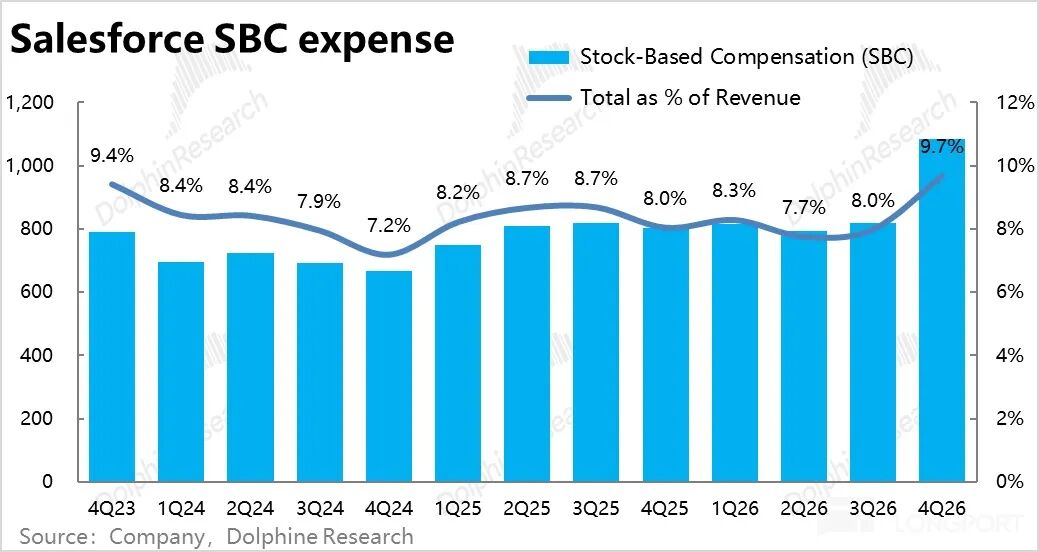

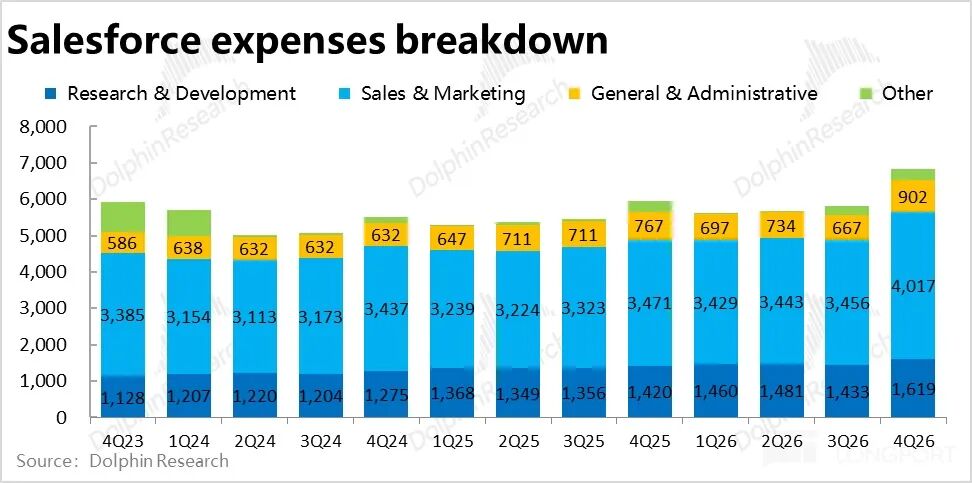

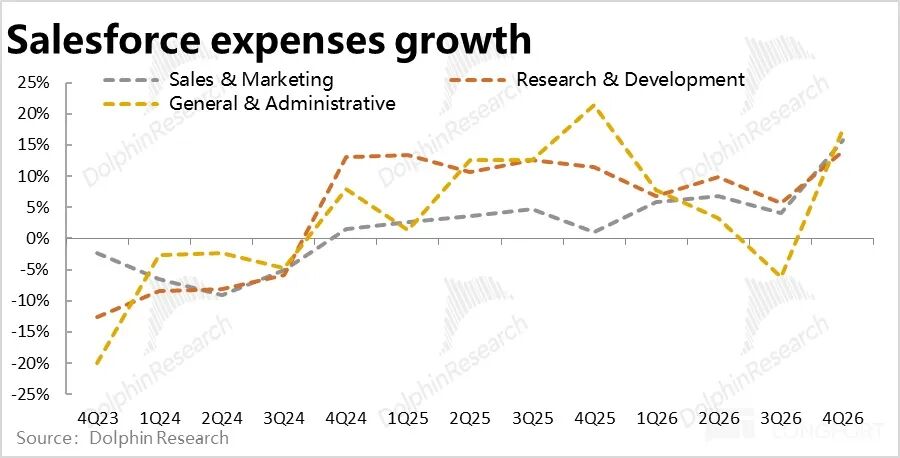

5. Expense Growth Accelerates Significantly: While revenue growth was mediocre, the year-over-year growth rate of total operating expenses surged to nearly 15% this quarter (compared to single-digit growth in previous years), higher than both market expectations and this quarter's revenue growth rate.

Specifically, R&D, marketing, and administrative expense growth were all around 15%, indicating a comprehensive increase in investments. Last quarter, the company was still strictly controlling costs, but this quarter it shifted dramatically, suggesting a clear intention from management to accelerate growth.

6. Margin Pressure and Expense Expansion Lead to Poor Profits: With mediocre growth, margin contraction, and significantly higher expenses, the result was that the GAAP operating profit margin for the quarter was 16.7%, narrowing by 1.5 percentage points year-over-year. This marked the first year-over-year decline since FY2023 (i.e., the trough year of 2022 post-pandemic).

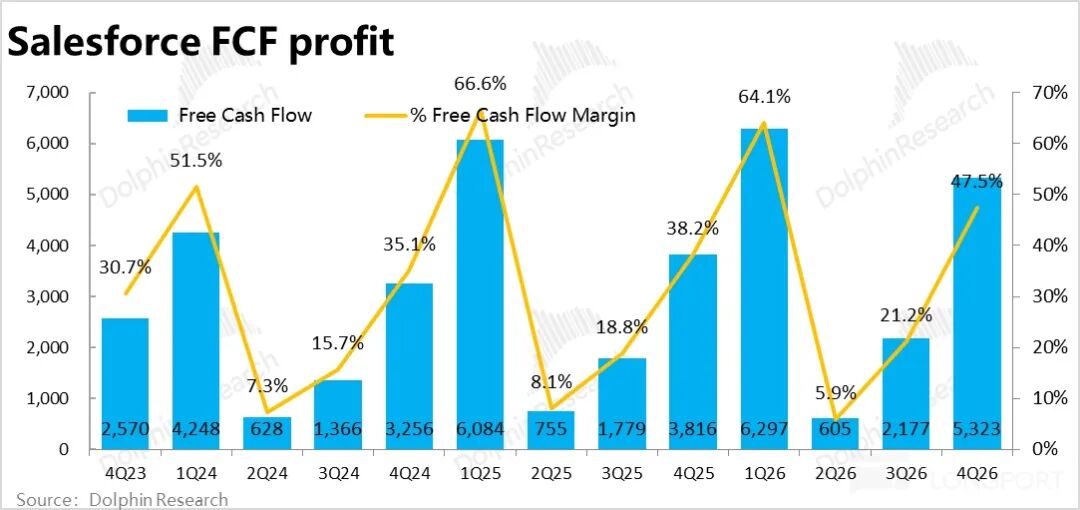

Profit amounted to $1.87 billion, up less than 3% year-over-year, nearly 8% below Bloomberg's expectations, which looks quite bad. Excluding non-cash expenses (mainly stock-based compensation and changes in operating assets), free cash flow profit, which the company focuses on more, was $5.32 billion this quarter, better than expected and previous guidance. The divergence between the two metrics is mainly due to the recognition of significant advance payments on the balance sheet.

7. Shareholder Returns Remain Generous: As promised at the previous Dreamforce conference, after the company's growth became limited, shareholder returns became one of the main means to maintain its attractiveness to equity investors. Throughout FY2026, the company spent a total of $14.3 billion on shareholder returns, mostly through buybacks. This corresponds to an 8% return rate relative to the company's current market cap, which is quite substantial.

Additionally, the company announced a new buyback authorization of up to $50 billion (replacing the previous authorization). The company is quite generous when it comes to shareholder returns.

Dolphin Research's Viewpoint:

1. From the above analysis, it is clear that Salesforce's performance this quarter was far from good. After excluding the positive impacts of consolidations and exchange rates, the growth of the company's existing businesses did not accelerate but continued to slow down. The revenue rebound guidance provided by management at the conference earlier this year has not materialized as of this quarter. (Including exchange rate and consolidation benefits, total revenue growth did recover to over 10%, but this is not very meaningful.)

Although after more than a year of promotion and iteration, the revenue of AI-related businesses such as Agentforce has indeed accelerated, it is still 'playing around' with a small base and has little substantive impact on driving overall revenue growth.

At the same time, due to the higher costs of AI-related businesses and the significant increase in investments (whether to accelerate revenue growth again or as a defensive move in response to the threat of AI substitution), profit performance has also suffered.

The overall impression is mediocre growth and poor profits.

As for future guidance and outlook:

In the short term, at constant exchange rates, total revenue is expected to grow 10%-11% year-over-year next quarter, similar to this quarter with a slight improvement. The growth contribution from consolidations will still be 4 percentage points, roughly in line with Bloomberg's expectations. This means a slight improvement over this quarter but still implies no significant acceleration in existing businesses.

cRPO is guided to grow 13% year-over-year (at constant exchange rates), exactly the same as this quarter. Although the contribution from consolidations has not been disclosed, there is no sign of acceleration.

On profits, guided diluted EPS is about 5% below Bloomberg's expectations, although it is slightly higher on a Non-GAAP basis. However, unlike the market, Dolphin Research generally does not agree with the view that stock-based compensation is not an expense. Therefore, from a GAAP perspective, the outlook is also not good.

Overall, growth is expected to remain steady next quarter with no significant acceleration, while profits will remain under pressure.

2. However, as Openclaw has shown the market that AI Agents are evolving and maturing faster than expected, and recent top large models like Claude/Gemini are also accelerating their iterations, the narrative of 'how AI will change/revolutionize software and even all industries' is evolving. This narrative's shift now has a greater impact on stock prices than earnings performance.

To be honest, Dolphin Research believes that: a. Existing software giants possess sufficient industry 'know-how' and exclusive data to maintain their leading positions in the AI era, making AI an enabler rather than a competitor;

b. AI will significantly reduce the costs for companies to develop in-house tools and achieve office automation, making 'expensive' SaaS services less competitive. Alternatively, as Agents replace employees, the number of billable seats (Seats) for SaaS services could decrease significantly. These are various scenarios that could severely damage the profitability of SaaS companies.

Which of these two starkly different scenarios is more likely is currently an unanswered question. The only certainty is the high level of uncertainty. And uncertainty means risk, which will likely amplify further as AI evolves.

Therefore, similar to our view on Uber previously, while the company's current performance is still relatively stable with no clear signs of being significantly disrupted by AI, given the possibility of complete disruption ('going to zero'), Dolphin Research tends to adopt a wait-and-see approach in the short to medium term, adhering to the principle of 'a gentleman does not stand under a precarious wall.'

3. Overall, unlike other SaaS stocks, even if AI does not truly disrupt them, SaaS stocks' overly high valuations still leave significant room for a sharp decline. The advantage of the mature Salesforce is that its valuation is not high, leaving limited room for further pure valuation declines, especially with strong buyback support.

Therefore, existing investors need not worry excessively about the risk of a significant further decline. However, relatively, there is currently no clear upward catalyst.

A more detailed value analysis has been published in the article of the same name under the 'Insights-Depth (Research)' section of the Changqiao App.

Below are the core performance charts and a brief introduction to the business.

I. Brief Introduction to Salesforce's Business & Revenue

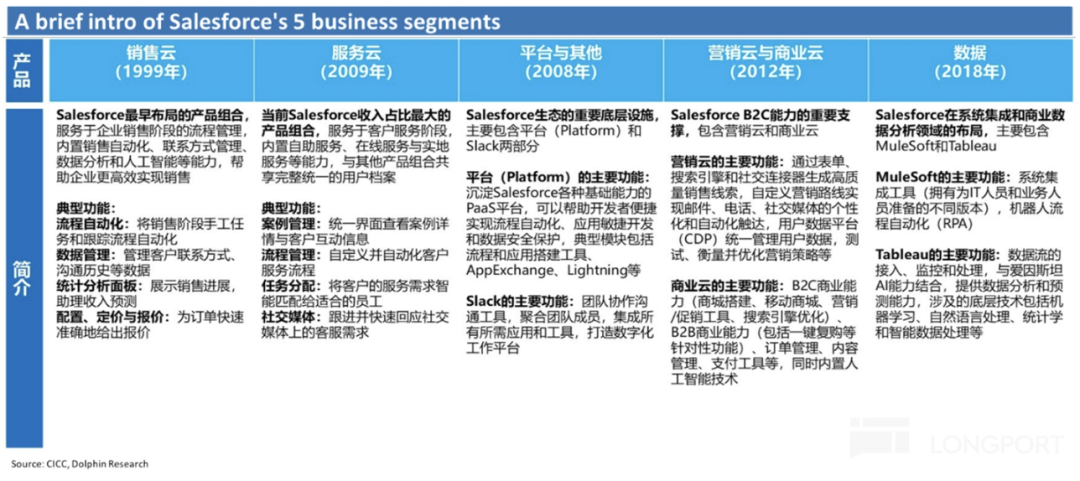

Salesforce was the pioneer in proposing the concept of SaaS (Software-as-a-Service) in the CRM (Client Relationship Management) industry across the United States and even globally. The model's key characteristic is its adoption of cloud services rather than on-premise deployment and a subscription-based payment model rather than outright purchase.

Therefore, Salesforce's business and revenue structure mainly consist of two categories: ① Over 95% of revenue comes from various types of SaaS service subscription income; ② The remaining small portion, about 5%, comes from expert service income such as project consulting and product training.

Further breaking it down, the dominant subscription income is composed of five major SaaS service categories, with roughly equal revenue volumes across each plate (board):

① Sales Cloud: The core of CRM and the company's earliest business, mainly comprising various process management tools for the enterprise sales stage, such as customer contact, quoting, and order signing functions.

② Service Cloud: The company's other core business, mainly including various functions related to customer service, such as customer information management and online customer service.

③ Marketing & Commerce Cloud: Marketing Cloud involves systematic marketing through various channels such as search, social media, and email; Commerce Cloud mainly includes virtual store setup, order management, payment, and other functions required for e-commerce.

④ Data & Integration (Integration & Analytics): Salesforce's internally integrated database services and business analysis tools, mainly composed of MuleSoft and Tableau.

⑤ Platform Cloud (Platform & Others): The infrastructure and services that other Salesforce SaaS services rely on, similar to PaaS (Platform-as-a-Service). It also includes team collaboration SaaS services like Slack, similar to Microsoft Teams.

II. Revenue Growth Appears to Accelerate but is Actually Mediocre

III. Leading Indicators Show Similar Trends, Appearing Strong but Actually Slightly Below Expectations

IV. Gross Margin Under Pressure and Declines

5. Significant Increase in Cost Investment

6. Nearly No Growth in Profit

- END -

// Reprint Authorization

This article is an original work of Dolphin Research. Reprinting is permitted only with authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available sources and are intended for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the views expressed in this report shall not, under any jurisdiction, be considered or construed as an offer to sell or a solicitation to buy securities, nor shall it constitute advice, a quotation, or a recommendation regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for, nor intended to be distributed to, jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials would conflict with applicable laws or regulations, or would result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in such jurisdictions, nor to citizens or residents of such jurisdictions.

This report reflects only the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

The World's First Trillionaire Emerges: Is SpaceX's $2 Trillion Valuation Justified?

-

Volkswagen to Implement 19,000 Job Cuts in Germany This Year

-

![]()

Tremble, Humans: AI Continues to Accelerate at Breakneck Speed

-

![]()

A Strategic Vision: Taking a Leaf Out of Apple’s Book in China’s Operation-Intensive Auto Market

-

![]()

Yu Chengdong Declares, ‘Only First Place Exists in My Lexicon.’ Is This Bold Claim or a Promise of Excellence?

-

![]()

Agent OS is Here! HarmonyOS 7 Unveiled, Huawei Redefines OS

-

![]()

Agent OS is Here! Huawei Unveils HarmonyOS 7, Redefining Operating Systems

-

DingTalk’s Evolution and the Dilemma Facing Alibaba