From Advanced Technology to Profitable Business: How Will the Self-Driving Narrative Continue?

02/28 2026

02/28 2026

612

612

2026 signifies the year when China's autonomous driving industry definitively moves away from the narrative of technological utopia and fully enters the challenging waters of commercialization.

Over the past decade, this sector has been dominated by the ultimate vision of 'L4 singularity,' driving relentless, almost frenzied arms races fueled by capital. Computing power for intelligent driving chips soared from hundreds of TOPS to thousands, while LiDAR, once an exclusive option for high-end models, became a standard feature in the fierce competition among automakers. The number of cities covered by urban NOA became a core KPI for both legacy and new automakers. Countless players bet on 'full self-driving in one leap,' treating the ceiling of technical parameters as the final showdown in industry competition.

However, this years-long frenzy came to a collective halt by late 2025. After users underwent a whirlwind of market education, hardware configurations based on excessive features could no longer boost terminal sales or valuations in the capital market. As the bubble gradually cleared, the entire autonomous driving sector underwent a complete cognitive reset. The core proposition of autonomous driving is not 'how fast technology can advance,' but 'how far commerce can go.'

This year's self-driving narrative is no longer a wild sci-fi fantasy but a realistic business battle focused on survival, breakthroughs, profitability, and the rise of domestic supply chains. The hype of past trends has given way to the laws of survival, and technological showcases have yielded to genuine user experiences. This year, instead of an eagerly anticipated technological singularity, there will be a decisive battle for the industry's future landscape over the next decade.

Ending the Arms Race: The First Principle is 'Survival'

Looking back at the past two years in the autonomous driving industry, the key phrase has been 'arms race.' Automakers competed on who had higher chip computing power, more LiDAR sensors, and broader urban NOA coverage. 1000 TOPS computing power became the entry threshold, four or more LiDAR sensors became standard for high-end models, and leading players all proclaimed 'nationwide urban NOA coverage.'

However, this year, the industry's core logic has shifted from 'technological showmanship' to 'commercial survival.' The most apparent change is that the logic of excessive features has completely failed. Before 2025, nearly all new energy vehicle models priced above 300,000 yuan were equipped with dual Orin chips and four LiDAR sensors, with intelligent driving hardware costs often exceeding 30,000 yuan. In contrast, multiple models priced between 100,000 and 200,000 yuan launched in early 2026 achieved urban NOA functionality with just one low-cost LiDAR sensor or even pure vision solutions, reducing intelligent driving hardware costs to under 5,000 yuan.

Behind this shift is a fundamental reset in user perceptions of autonomous driving. What users need is no longer increasingly inflated technical parameters but intelligent driving functions that are useful, reliable, and affordable. Over the past three years, many automakers have piled on industry-leading hardware configurations, yet in real-world experiences, the disengagement rates in urban driving scenarios remained high, performance frequently faltered in extreme weather, and daily usage rates by users were below 10%, ultimately becoming 'impressive on paper but useless in practice' features.

Tesla's FSD provided a valuable lesson to the industry, demonstrating that with just eight cameras and a pure vision solution, it could deliver intelligent driving performance comparable to LiDAR-based solutions, thanks to end-to-end large model algorithm optimization and massive data training iterations.

Consequently, a comprehensive cost-reduction trend has swept the industry. Leading automakers are adjusting their hardware configurations, eliminating redundant LiDAR sensors and computing power in favor of 'just enough' hardware solutions. Smaller automakers are abandoning full-stack self-development and turning to collaborations with domestic solution providers like Horizon Robotics, Black Sesame Technologies, and Baidu to reduce intelligent driving costs through scaling procurement (large-scale purchasing).

More brutally, 2026 will become the 'year of consolidation' for the autonomous driving industry. Over the past three years, smaller intelligent driving solution providers that survived on capital infusions have reached a critical point amid the funding winter. Players lacking Large scale landing capability (large-scale implementation capabilities), stable automaker orders, and profitability prospects will exit the market in droves, leading to a significant increase in industry concentration.

Ultimately, the first principle of the autonomous driving industry has shifted from 'running faster' to 'surviving longer.' The focus has moved from who tells the sexier story to who has the healthier cash flow and stronger commercialization capabilities.

Commercialization Breakthrough: It's About Rules, Not Just Technology

If 2025 was the 'year of regulatory implementation' for L3 autonomous driving, then 2026 will be the 'year of large-scale implementation' for L3. This year, the commercialization narrative of autonomous driving will be completely rewritten by L3.

For the past decade, the biggest paradox in the autonomous driving industry has been that while L3-level functionality has been technically achievable, it has never been implemented on a large scale. The core bottleneck has never been computing power or sensors but regulations. For L2 intelligent driving, regardless of accidents, responsibility lies with the driver. For L3, during system activation, accident responsibility shifts to the automaker.

This rule directly determines that L3 is not just a technological issue but a comprehensive game involving law, commerce, and insurance.

In November 2022, the Ministry of Industry and Information Technology (MIIT) released a draft for access pilot programs, proposing for the first time at the institutional level to implement access management for L3/L4 vehicles, aiming to address the long-standing 'liability vacuum' plaguing the industry.

2023 became the 'breakthrough year' for testing licenses. In July, BYD obtained China's first high-speed L3 testing license in Shenzhen. In December, a wave of licenses followed, with GAC Aion (GAC Aion), BMW, Zhiji, Mercedes-Benz, Chang'an, and Huawei-affiliated entities obtaining qualifications in multiple regions, forming a pilot pattern of 'simultaneous breakthroughs in the South (Shenzhen, Chongqing) and North (Beijing).'

From 2024 to November 2025, the testing scope expanded, and pilot programs deepened. In June 2024, MIIT announced the first batch of nine automakers for access pilot programs, shifting from 'single testing' to a dual approach of 'access + on-road operation.'

Finally, in September 2025, eight departments included 'conditional approval of L3 vehicle production access' in their plan, paving the way for product access approval in December.

MIIT's restrictions on the two approved models were highly specific: The Chang'an Deepal SL03 could only operate on designated sections of Chongqing's inner ring expressway at a maximum speed of 50 km/h in traffic congestion scenarios. The BAIC Arcfox Alpha S was limited to certain highways in Beijing, with a speed limit of 80 km/h. More critically, the vehicles were not delivered directly to individual users but operated in fleets by designated 'usage entities.'

This approach reveals China's underlying logic in promoting L3: The policy's core objective is not aggressive technological promotion but establishing a real-world 'pressure test field' while minimizing risks.

It is predictable that almost all mid-to-high-end models launched this year will feature L3 autonomous driving as a core selling point. More importantly, L3 implementation will completely open up the commercialization space for autonomous driving.

Meanwhile, users have not yet formed a consensus on intelligent driving functions, and automakers' subscription models for intelligent driving have remained tepid. The core reason is that L2+ intelligent driving can only assist and cannot truly free the driver's hands and feet, so users are unwilling to pay for 'half-baked' functions. Even industry leader Tesla has an FSD subscription rate of less than 5% in China; domestic new energy automakers generally have subscription rates below 3%.

L3 implementation will completely change this dynamic. When the system can assume driving responsibility and truly enable 'hands-free, eyes-free' driving on highways and urban expressways, intelligent driving functions will transform from 'value-added services' to 'standard services.'

Simultaneously, a supporting ecosystem around L3 will quickly take shape, with dedicated autonomous driving insurance products launching to address concerns for both automakers and users. Road infrastructure upgrades for L3 scenarios will gradually progress, enabling large-scale vehicle-infrastructure coordination on highways and urban expressways to further reduce L3 disengagement and accident rates.

This year, L3 will become the core theme of the autonomous driving industry, not only opening the door to high-level intelligent driving implementation but also closing the loop from technological research and development to commercial realization for autonomous driving.

Mapless Showdown: Turning High-End Features into Standard Equipment

While the industry debated whether urban NOA was a Pseudo demand (fake demand) last year, it has now become standard in 150,000-yuan family cars, fully entering the 'mass adoption' era.

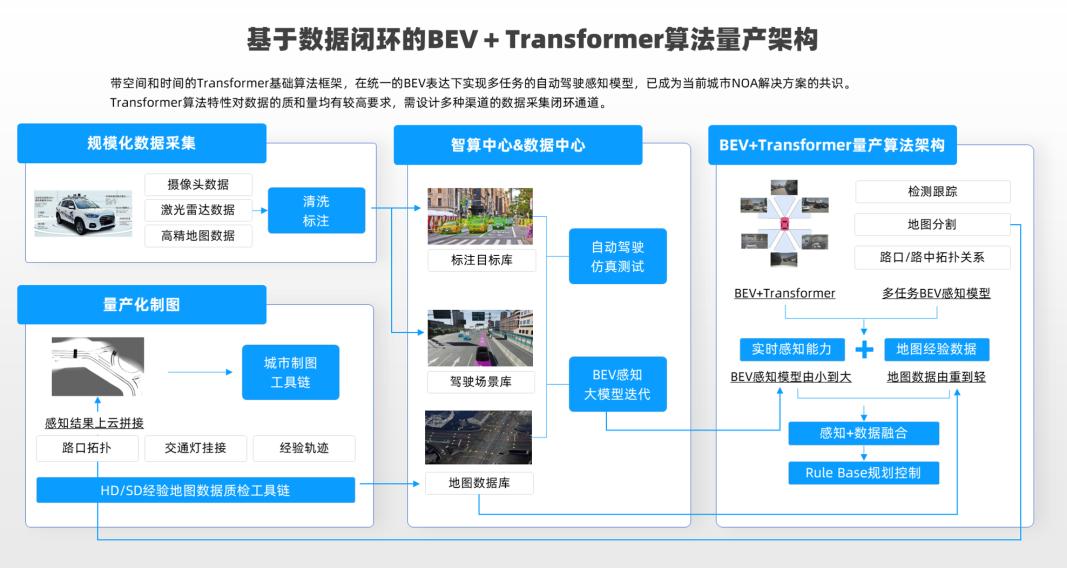

The core driver behind urban NOA's proliferation is the full maturity of 'mapless' solutions.

Previously, urban NOA relied heavily on high-definition maps. Maintaining a national high-definition map cost hundreds of millions of yuan annually, and due to map review policies, updates often took 1-3 months after road changes, causing intelligent driving systems to frequently malfunction on newly built or construction-affected roads. More critically, high-definition map licensing fees directly increased the cost of intelligent driving solutions, limiting urban NOA to high-end models priced above 300,000 yuan.

Mapless solutions eliminate dependence on high-definition maps. Through end-to-end large models, vehicles can use real-time perception from cameras and LiDAR to identify roads, assess conditions, and plan routes like human drivers, enabling autonomous driving on urban roads. This not only reduces urban NOA solution costs by over 60% but also resolves the pain point of outdated map updates, significantly improving system adaptability.

A crucial factor enabling practical application of mapless solutions is the enhanced perception capabilities of individual vehicles at this stage. BEV bird's-eye view and large model Transformer applications can unify static road information and dynamic road participants into a single coordinate system, generating 'live maps' in real-time through perception and conversion while driving, facilitating the 'perception-decision-planning' tasks in autonomous driving.

As mapless solutions become mainstream for urban NOA, Tesla's FSD pure vision mapless solution, XPENG's XNGP all-scenario mapless solution, and Huawei's ADS mapless advanced solution have achieved nationwide city coverage. Meanwhile, solution providers like Horizon Robotics and Baidu Apollo have launched mapless urban NOA solutions for smaller automakers, enabling models priced between 100,000 and 200,000 yuan to easily incorporate urban NOA functionality.

Consequently, urban NOA penetration has surged. According to the China Association of Automobile Manufacturers' '2025 Urban NOA Vehicle Assisted Driving Research Report,' from January to November 2025, cumulative sales of passenger vehicles equipped with urban NOA functionality reached 3.129 million units, accounting for 15.1% of passenger vehicle insurance registrations. In 2026, urban NOA functionality will accelerate its extension to models priced below 200,000 yuan.

Of course, the mass adoption of urban NOA also accompanies a complete industry reshuffle, with a brutal elimination race underway. While mapless solutions lower the barrier to urban NOA implementation, they actually raise the industry's technological moat. Success now hinges not on supply chain integration or map procurement capabilities but on end-to-end large model R&D, closed-loop capabilities with massive real-world testing data, and rapid algorithm iteration.

Achieving stable mapless urban NOA requires not only billions in R&D investment but also millions of vehicles on the road generating massive real-world data—two barriers that smaller players cannot overcome. Huawei, XPENG, and Tesla lead the first tier with their full-stack self-developed mapless solutions, while BYD, NIO, and Li Auto rapidly catch up. In the third-party solution market, Horizon Robotics and Baidu Apollo dominate orders from smaller automakers, while those without mapless technology—relying solely on high-definition maps—are exiting the market en masse.

The mass adoption of urban NOA is not merely about feature decentralization and price reductions. Over three years, it has transformed from a high-end exclusive to a standard feature in family cars, broken through technological and cost barriers with mapless solutions, and, most critically, educated millions of ordinary car owners to accept and habit (get used to) intelligent driving, turning high-level intelligent driving from a lab concept into part of daily travel for millions of families.

From 'Storytelling' to 'Real Profits': The Last Chance

If intelligent driving in passenger vehicles enters large-scale adoption in 2026, then Robotaxi, Robobus, and autonomous trucking for mainline logistics reach critical inflection points.

For the past decade, Robotaxi has been the 'ultimate dream' of the autonomous driving industry, with capital investing hundreds of billions. By 2026, the industry has awakened to the reality that full-scenario, full-geography L4 Robotaxi cannot be achieved shortly. Survival now hinges on profitability in specific regions.

Starting this year, the Robotaxi industry will polarize.

On one side, leading players will strive for profitability. Baidu Apollo Go, Pony.ai, and WeRide will expand operations in core areas of first-tier cities like Guangzhou, Shenzhen, Beijing, and Shanghai, significantly reducing Robotaxi operating costs through Large scale operation (large-scale operations) to achieve profitability. This year, these leaders will further expand their operational scope, transitioning from 'pilot operations' to 'commercial operations.'

On the other side, smaller players will exit en masse. Robotaxi companies without automaker backing, massive data, or financial support will leave the market, with no possibility of further capital infusions. They will either be acquired or disappear quietly.

Compared to Robotaxi, Robobus and autonomous trucking for mainline logistics face faster commercialization.

Highway mainline logistics scenarios, with relatively simple road conditions and no pedestrians or non-motorized vehicles, are ideal for autonomous driving. More importantly, the logistics industry has a strong demand for cost reduction. Driver costs account for over 30% of total logistics expenses, while autonomous driving enables 'single-driver' or even 'driverless' operations, significantly cutting labor costs. Meanwhile, autonomous driving's smooth operation can reduce fuel consumption by about 10%, further lowering logistics costs.

In 2025, leading companies like Plus.ai and Inceptio Technology partnered with logistics giants like SF Express, JD Logistics, and ZTO Express to commercialize thousands of autonomous heavy trucks. This year, autonomous trucking for mainline logistics will enter a large-scale outbreak period (boom phase), achieving normalization operations on major national highways.

Robobus, leveraging its public transportation attributes and policy support, precisely targets high-frequency, Rigid demand (rigid demand) scenarios like urban micro-circulation, public transit connections, and park/scenic area shuttles, becoming one of the most certain tracks for implementation.

Unlike Robovan's role in supplementing last-mile logistics and Robotruck's efficiency improvements in trunk logistics, Robobus directly serves public transportation, covering scenarios with strong demand for public travel and stable needs. It effectively alleviates traffic congestion, enhances travel experiences, and enjoys stronger policy priority and social recognition. With advantages such as strong scene adaptability, high policy certainty, and a clear commercialization path, it has found the optimal balance between technical implementation difficulty and commercial value return.

In urban microcirculation transportation, traditional buses suffer from “uneven capacity and insufficient coverage”. In enclosed areas like industrial parks and scenic spots, there is a high demand for short-distance shuttles, but labor costs remain high. The emergence of Robobus precisely fills these demand gaps. This essential nature ensures stable market demand for Robobus, providing a foundation for commercialization.

From a policy perspective, multiple countries and economies worldwide have incorporated Robobus into their public transportation upgrade plans, providing clear policy support for its commercialization. The United Nations Economic Commission for Europe (UNECE) has approved a regulatory framework for Level 3 autonomous driving, paving the way for Level 4 commercialization. Singapore has explicitly proposed achieving Collaborative operation (collaborative operation) of autonomous buses with regular buses within three years. Domestically, as of 2025, 28 cities have opened Level 4 autonomous driving tests, supporting Robobus demonstration applications through policy sandboxes.

Chinese autonomous driving companies hold a first-mover advantage in the Robobus sector. Last year, WeRide partnered with Shenzhen Bus Group to officially launch Shenzhen's first L4 autonomous bus operation route—B888—in Luohu District, marking the city's first autonomous minibus project operating in a bustling urban center.

In October last year, Mushroom Auto won Singapore's first official L4 autonomous bus project, marking the first time autonomous buses were integrated into an overseas public transportation system. This confirms international market recognition of China's autonomous driving technology solutions. Leveraging a technical approach combining “front-loading mass production with visual and solid-state LiDAR fusion” and a consortium model of “core technology + vehicle manufacturing + localized operations,” Mushroom Auto effectively addresses localization challenges in overseas markets, laying the groundwork for subsequent expansion into Southeast Asia, Europe, and the Americas.

TianTong Vision recently announced plans to launch an autonomous bus route in Taihu New City, connecting the University of the Chinese Academy of Medical Sciences with the Muli Station on Metro Line 7, with operations scheduled to begin in the first quarter of this year. The route will utilize a 6.5-meter microcirculation bus jointly developed by TianTong Vision and CRRC, equipped with its self-developed L4 intelligent driving system based on the Horizon J6M chip platform.

By 2026, there will be no room for “storytelling” among autonomous driving players. Capital and markets will focus on one metric: profitability. Players capable of achieving commercial profitability will unlock new growth opportunities, while those unable to deploy will be eliminated by the industry.

No Finale, Only Step-by-Step Implementation

Of course, the autonomous driving narrative is not entirely one of rapid progress; the industry still faces numerous unavoidable challenges that will shape its development pace.

First and foremost is data security and compliance. The iteration of autonomous driving relies on massive amounts of road and user driving data, much of which involves national geographic information and user privacy. By 2026, domestic data compliance requirements for autonomous driving will further tighten, with stricter regulations on cross-border data transmission, road data collection, and user privacy protection. Achieving efficient data iteration within compliance frameworks will become a critical challenge for all players.

Second is the issue of user trust. Despite qualitative advancements in autonomous driving technology, general user trust remains low. Many users still worry about potential system bugs and liability in accidents. Any autonomous driving safety incident could be amplified, damaging the industry's reputation. Building user trust through technological iteration and public education remains a long-term challenge for the industry.

Finally, there is the ultimate technical bottleneck. Today's autonomous driving systems operate stably in 99% of conventional scenarios but struggle with the remaining 1% of extreme cases, such as heavy rain or snow, unmarked rural roads, or sudden traffic accidents. Human drivers can rely on experience and instinct to navigate these scenarios, while autonomous systems require vast amounts of data training and algorithm optimization to address these shortcomings. To date, autonomous driving cannot achieve “full-scenario, all-weather” coverage and must continue to improve incrementally.

In reality, autonomous driving has never experienced a “singularity moment” or a sudden, all-encompassing breakthrough. The transition from L2 to L3, L3 to L4, and from specific to full scenarios is destined to be a prolonged, gradual process.

From this point onward, the autonomous driving narrative will no longer feature fantastical sci-fi elements but will focus on practical commercial deployment. Some players will exit the stage, while others will break through against the odds; some technologies will be phased out, while others will prove viable. Ultimately, the players that remain will be those who truly respect technology, users, and commercial principles.

After all, the end goal of autonomous driving is not to replace human drivers but to make every journey safer, easier, and more enjoyable. And 2026 will mark just one critical step in this long journey.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once