Overseas Contribution at 73%, MiniMax Sets an Example for AI Global Expansion

03/04 2026

03/04 2026

545

545

Author: Tang Fei

On March 2, artificial intelligence (AI) company MiniMax released its first annual performance report since going public, marking its first full-year results since listing on the Hong Kong Stock Exchange.

The financial report reveals two distinct sides: on one hand, rapid revenue growth, sustained overseas market expansion, and a steady increase in user base; on the other hand, losses have also widened, particularly due to fair value changes in financial liabilities, which have significantly pressured net profit.

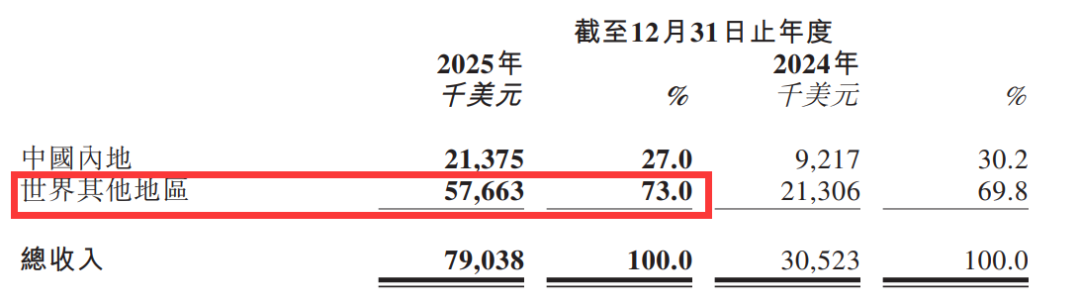

Specifically, MiniMax's total revenue in 2025 reached $79.038 million, a year-on-year increase of 158.9%, with over 70% of revenue coming from international markets. The annual loss was $1.872 billion, a 302.3% increase year-on-year, including nearly $1.6 billion in losses from fair value changes in financial liabilities, with an adjusted net loss of $250 million.

During the recently concluded conference call, Yan Junjie, founder and CEO of MiniMax, disclosed the growth momentum for the new year—by February 2026, the company's ARR (Annual Recurring Revenue) exceeded $150 million; for open platform products targeting enterprise clients and individual developers, the number of new registered users in February 2026 reached more than four times that of December 2025.

While most AI companies are still fiercely competing in the domestic market, why has MiniMax been able to lead the charge overseas? Does the answer to AI commercialization lie behind this high growth? This article will delve into the financial report to analyze MiniMax's globalization path, success logic, and the joys and concerns supporting its high valuation.

Since its listing on January 9, MiniMax's stock price has been on a steady rise in less than two months. With an initial offering price of HK$165 per share, as of March 3, MiniMax's stock closed at HK$821 per share, with a total market capitalization of HK$257.5 billion, representing a cumulative increase of nearly 500%.

The strong market confidence primarily stems from MiniMax's outstanding 'report card.' If one were to summarize MiniMax's financial report in a sentence, it would be that the revenue structure has significantly optimized, and economies of scale are beginning to show.

First, let's look at the core data. In 2025, MiniMax achieved total revenue exceeding $79 million, a 158.9% year-on-year increase from approximately $30.5 million in 2024.

More noteworthy than the growth rate is the change in profit structure. The company's gross margin jumped from 12.2% to 25.4%, with gross profit increasing by 437.2% year-on-year to approximately $20.1 million, a significantly higher increase than revenue growth, reflecting that model efficiency and infrastructure optimization are translating into real economic returns.

The most eye-catching aspect is its global achievements—international market revenue accounted for 73%, further increasing from 69.8% in 2024. This means that the primary market for this Chinese AI company is actually overseas, with an absolute value of approximately $57.7 million.

Breaking down the business segments, there are two main 'engines' driving the high performance.

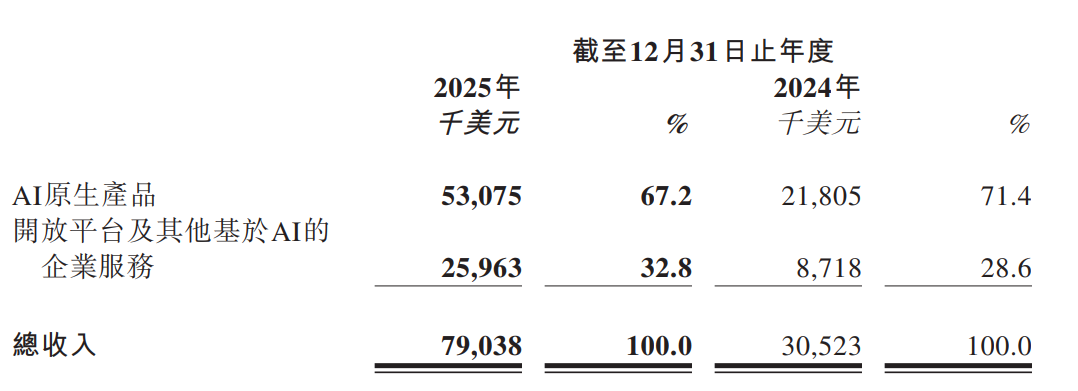

Consumer-side (AI-native products) revenue reached $53.075 million, a 143.4% year-on-year increase, accounting for 67% of total revenue. The growth mainly comes from the continued promotion of overseas hit applications Talkie (the overseas version of Xingye) and Hailuo AI. The financial report specifically mentions that Talkie's paying users have grown from less than 500,000 in 2024 to 1.77 million, indicating a significant increase in user willingness to pay.

Enterprise-side (open platform and enterprise services) revenue reached $25.963 million, a 197.8% year-on-year increase. This growth is mainly driven by the popularity of the M2 series models in overseas developer communities, leading to a significant increase in the number of paying clients.

This dual-wheel-driven business model of 'Consumer + Enterprise' provides MiniMax with stable, predictable recurring revenue and has significantly improved profitability.

Soochow Securities pointed out in a related research report that MiniMax's business model is highly sustainable, primarily due to three factors:

First, its positioning at the model layer places it upstream in the value chain. Application-layer players rely on underlying models and have weak bargaining power, while MiniMax's full-stack self-research ensures technological independence and leading cost control capabilities.

Second, the dual-wheel structure balances growth and profitability. The consumer business provides flexibility, while the enterprise business provides stability, making the overall operation resilient to macroeconomic fluctuations.

Third, the flywheel effect continues to strengthen with model iteration. Industry experience shows that once a company enters the leading echelon (leading group), technology and data accumulation create a Matthew effect, making it extremely difficult for latecomers to catch up.

Additionally, another noteworthy point in the financial report is its losses—in 2025, the loss was $1.872 billion, a 302.3% year-on-year increase. However, a closer look reveals that $1.6 billion of this $1.872 billion loss was due to fair value losses on financial liabilities, i.e., 'paper losses' caused by changes in the fair value of preferred shares. This can be understood as stock gains for early investors, not losses from actual business operations.

Therefore, this revenue report carries even more weight.

For MiniMax, 2025 was a year of comprehensive technological advancement and accelerated commercialization. That year, MiniMax built full-modal research and development capabilities, with models in major modalities such as language, video, voice, and music achieving global competitiveness.

Taking text models as an example, from the MiniMax M1 released in June last year to M2 and M2.1 in the fourth quarter, and then to M2.5 released in February this year, the technological iteration cycle has been compressed to monthly updates. MiniMax's latest self-developed native Agent RL framework, Forge, has brought about a 40-fold training acceleration for text models.

In terms of model performance, its recently released M2.5 model has shown impressive results in programming and office scenarios. According to the SWE-Bench Verified test, M2.5 scored 80.2%, less than 1 percentage point behind Anthropic's Claude Opus 4.6, which scored 80.8%.

While the performance gap narrows, the price gap is significant.

According to OpenRouter's public pricing in February this year, the input price for M2.5 is $0.3 per million Tokens, and the output price is $1.1; while the corresponding prices for Claude Opus 4.6 are $5 and $25, respectively. In other words, at similar capability scores, the latter's cost is about 10 to 20 times that of the former.

The model's capabilities are close, and the calling cost is lower, enabling M2.5 to rapidly spread in the developer community. Especially after the popularity of OpenClaw, this 'cost-effectiveness advantage' has been further amplified.

In addition, the optimization of the model architecture has also broadened commercialization scenarios. The M2 series models adopt a hybrid MoE architecture, with a total parameter scale of 230 billion but only about 10 billion activated parameters. The lower number of activated parameters makes private deployment of top-tier large models a reality, addressing concerns about data security in industries such as finance, healthcare, and government affairs, and opening up previously inaccessible market spaces.

Beyond technological strength, Talkie/Xingye's 'human-like' gameplay represents another path to rise. The overseas version of Talkie and the domestic version of Xingye are AI companionship products focused on real-time human-machine interaction. In addition to free chat, users can also interact with intelligent agents and participate in scripted or themed 'stories,' which are semi-guided narratives. Stories can be created by users or based on popular templates, supporting structured storytelling and open-ended dialogue.

According to data from CIC Consulting, as of the end of September 2025, Talkie/Xingye ranked among the top five in average daily usage time among global large model applications, with users spending an average of over 70 minutes per day, very close to TikTok's average daily usage time during the same period.

Analysts from Soochow Securities believe that the key to MiniMax's success lies in product differentiation. The deep role interactions in Talkie/Xingye create barriers in the emotional companionship field, while Hailuo AI's video generation capitalizes on the global trend of short videos. Compared to most domestic large model companies still focused on local deployment, MiniMax's global vision results in a healthier revenue structure and more dispersed exchange rate fluctuations and regional policy risks.

With a market capitalization exceeding HK$250 billion, MiniMax has surpassed several major Hong Kong-listed internet companies such as Baidu, Ctrip, Meitu, and China Literature.

In a February research report, Morgan Stanley gave MiniMax an 'Overweight' rating with a target price of HK$930, believing that the fulcrum of its performance lies in whether its model technology can consistently rank among the global top tier and whether its revenue structure has the flexibility for global expansion. UBS set a target price of HK$1,000, citing optimism about the prospects of the foundational model industry and the company's accelerated commercialization.

In other words, capital is still paying for future growth. However, the logic behind this high valuation is easy to understand. In the Hong Kong stock market, there are only two pure AI concept companies—MiniMax and Zhipu. Supply and demand determine prices, and scarcity brings a premium.

The issue, however, is that this valuation requires a high level of performance growth to match.

Morgan Stanley predicts that by 2027, MiniMax's revenue will increase to around $700 million, with a gross margin of 32%. UBS forecasts that MiniMax's revenue from 2025 to 2027 will be $73 million, $209 million, and $809 million, respectively, with a compound growth rate exceeding 200%.

Only then can MiniMax justify a target price of HK$930 or even HK$1,000 and a future market capitalization that may approach HK$300 billion.

However, the road ahead is not smooth. A securities analyst told us that MiniMax still needs to overcome 'three hurdles' to maintain high growth and valuation.

The first is the 'stress test' of technological iteration. For high-valuation AI companies, each model release is a major test. In today's technology innovation cycle measured in months, whether the next-generation model can achieve significant breakthroughs will directly affect capital market confidence. If technology falls behind or stagnates, valuations may quickly contract.

The second is the 'litigation risk' of overseas copyright. In September 2025, several major film and television giants, including Disney, Universal Pictures, and Warner Bros. Discovery, sued MiniMax, alleging that Hailuo AI infringed upon rights during training, generation, and promotion stages, with potential damages of up to $75 million. If legal precedents become stricter, model training and compliance costs will rise significantly, directly impacting the already low gross margin.

The third is the 'geopolitical risk' of the macro environment. With over 70% of revenue coming from overseas, the company is highly sensitive to changes in cross-border regulations and computing power environments. Any technology export restrictions, increased platform access thresholds, or even brief 'power outages' at computing centers could directly hinder its growth path.

Vention's '2026 State of Artificial Intelligence (AI) Report' points out that the current global AI boom shares similarities with the historical internet bubble, but the fundamental difference lies in the depth of integration with core business processes. The bursting of the internet bubble did not kill the internet but cleared the noise, laying the foundation for subsequent development.

The report also suggests that the market is becoming more selective, with the early stages of excitement, heavy investment, and expectations surpassing reality feeling familiar. However, now, simply launching AI products is no longer enough; the key is whether they solve practical problems and integrate into existing workflows.

Combining the trends outlined in the report, it can be observed that the competitive routes of domestic leading large model companies such as MiniMax, Zhipu, Yuezhi'anmian, and Jieyue Xingchen have also changed. They have shifted from the early arms race stage focused on parameters, scale, patents, and papers to a stage emphasizing efficiency in implementation scenarios, cost control, and commercialization capabilities.

When discussing the company's next development strategy, Yan Junjie revealed, 'At the corporate strategy level, we will evolve from a large model company to a platform company in the AI era, continuously defining and promoting new intelligent paradigms, providing global users and partners with more powerful intelligence through scalable infrastructure and token throughput capabilities.'

At least for now, MiniMax is at the forefront of the industry in terms of both strategy and technology. In this case, book losses are no longer the core benchmark for evaluating an investment target; instead, platform potential and growth potential have taken their place. From this perspective, MiniMax remains a good investment target, with Goldman Sachs even considering it "one of the best-positioned AI model companies in China."

For readers who focus on AI companies going global, the future performance of MiniMax is worth continuous tracking.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once