Marvell: ASIC Single Card Falls Short, Makes a Comeback in AI via Interconnection!

03/06 2026

03/06 2026

441

441

Marvell Technology (MRVL.O) unveiled its financial results for the fourth quarter of FY2026 (as of January 2026) after the close of the U.S. market on the morning of March 6 (Beijing Time):

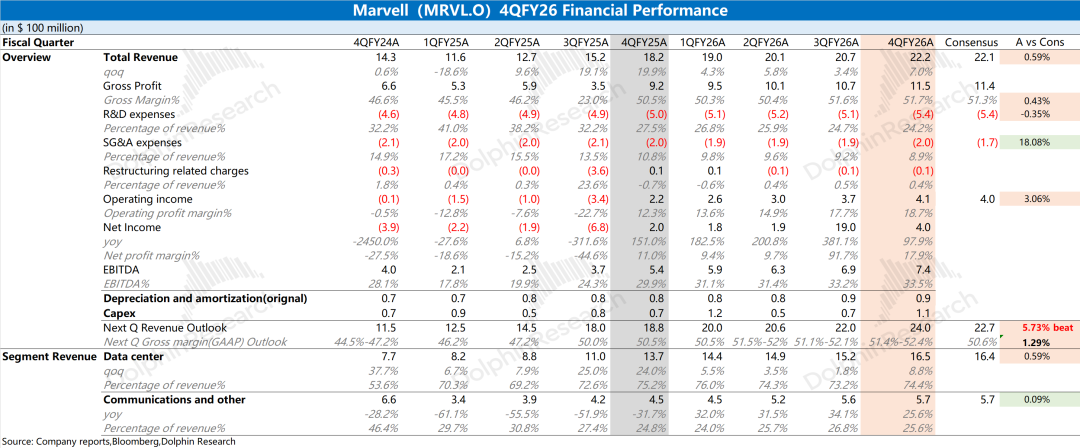

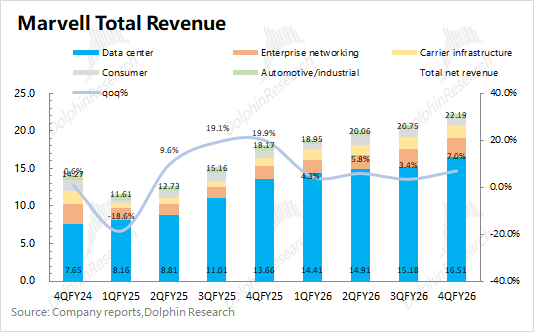

1. Revenue: This quarter, revenue soared to $2.22 billion, marking a 7% increase from the previous quarter and meeting market expectations of $2.21 billion. The sequential rise of $150 million was primarily fueled by growth in the data center segment.

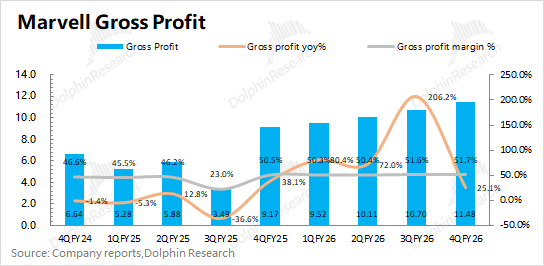

2. Gross Margin: This quarter, the gross margin stood at 51.7%, showing a slight 0.1% increase from the previous quarter. However, the reported margin does not directly mirror operational performance due to the impact of amortization from acquired assets on the company's gross margin.

After adjusting for this impact, Dolphin Research refers to the adjusted gross margin, which was 58.5% this quarter, experiencing a slight 0.5% decrease sequentially. This dip is attributed to the structural impact of a higher proportion of lower-margin custom ASIC and other businesses.

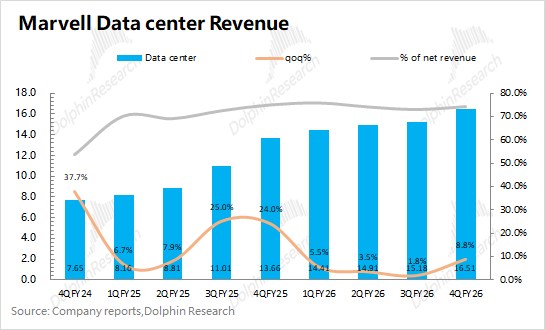

3. Data Center Business: This was a focal point for the market. Revenue in this segment reached $1.65 billion this quarter, up 8.8% from the previous quarter, primarily driven by custom ASIC and optical interconnect products. The data center business contributed 74.4% to the total revenue this quarter. Dolphin Research estimates that the company's AI business revenue was approximately $960 million this quarter, showing a sequential increase of $110 million.

Amazon launched Trainium 3, but given market conditions, Trainium 3 is mainly supplied by Alchip. Marvell remains a key supplier for Amazon, primarily providing Trainium 2.5 products (an upgraded version of Trainium 2), in line with the company's earlier statement of "no revenue gap."

4. Next Quarter Guidance: Revenue is projected at $2.4 billion, surpassing market expectations of $2.27 billion, with sequential growth primarily driven by custom ASIC and data center businesses. The gross margin (GAAP) is expected to range between 51.4%-52.4%, remaining relatively stable.

5. Full-Year Outlook: The revenue outlook for FY2027 has been raised to $11 billion (previously $10 billion), representing a 34% year-over-year increase. ASIC growth is anticipated to exceed 20%, with optical interconnect products growing by over 50%. The revenue outlook for FY2028 has been elevated to $15 billion (previously $13 billion), marking an approximate 40% year-over-year increase.

Dolphin Research's Comprehensive View: Guidance Raised Again, Emphasizing 'Large-Scale Cluster' Capabilities

Marvell Technology's financial results this time largely aligned with market expectations, with revenue growth primarily driven by the data center business. After adjusting for amortization and other impacts, the company's adjusted gross margin was 58.5%, showing a slight 0.5% decrease sequentially due to the structural impact of a higher proportion of lower-margin custom ASIC and other businesses.

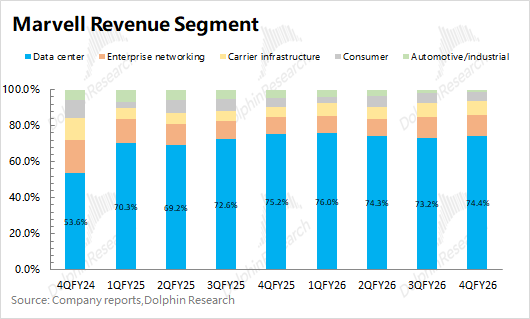

The company revamped its business disclosure metrics this quarter, consolidating its business segments from five to two (Data Center, Communications & Others), further underscoring the significance of the data center business. The data center segment was the main growth driver this quarter, with an 8.8% sequential increase. Dolphin Research estimates AI revenue at approximately $960 million this quarter.

Beyond the financial figures, the company's guidance was "quite promising." Marvell Technology expects next quarter's revenue to reach $2.4 billion, up 8% sequentially, outperforming market expectations of $2.27 billion, with growth primarily driven by optical module chips and custom ASICs.

Company management once again raised its future operational outlook, projecting FY2027 revenue to reach $11 billion (previously guided at $10 billion), up 34% year-over-year, with the data center AI business contributing the majority of incremental growth.

Key Focus Areas for Marvell Technology's AI Business:

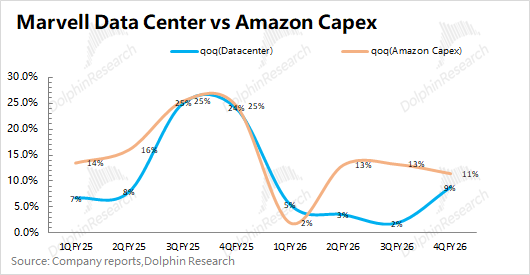

a) Major Clients' Capital Expenditures: Amazon is Marvell's primary AI business client, and its capital expenditures lay the foundation for AI business growth.

Combining Marvell Technology's data center performance with Amazon's capital expenditures, it is evident that the company's data center growth rate is significantly lower than Amazon's capital expenditures.

Even if Amazon boosts its 2026 capital expenditures to $200 billion, up approximately 50% year-over-year, Marvell can only capture a portion of this increase. The company's management now expects data center business growth to exceed 40%, still lower than Amazon's capital expenditure growth rate.

Dolphin Research believes this is primarily due to the slower growth of custom ASICs (the company expects growth to exceed 20%), indicating that Amazon is not entirely satisfied with Marvell's ASIC products.

Previously, the company supplied Amazon with Trainium 2/Inferentia 3, but Amazon has largely entrusted the latest Trainium 3 products to Taiwanese firm Alchip, with Marvell providing Trainium 2.5 (an upgraded version of Trainium 2).

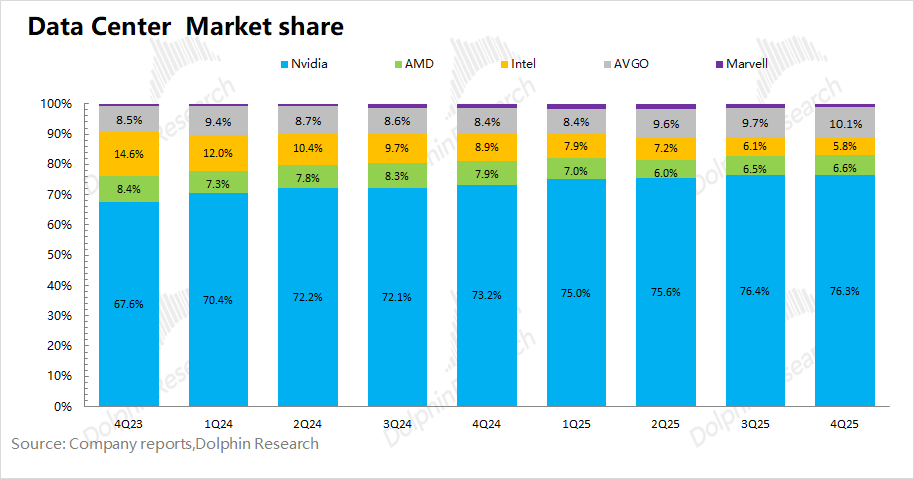

b) AI Chip Market Share: Compared to industry giants like NVIDIA and Broadcom, Marvell Technology's market share is relatively small, at around 1%.

Consequently, the market had high hopes for the company's ability to gain market share. However, its current performance remains "underwhelming," with Amazon still its only core client, and its share of Amazon's Trainium products declining, indicating insufficient product competitiveness.

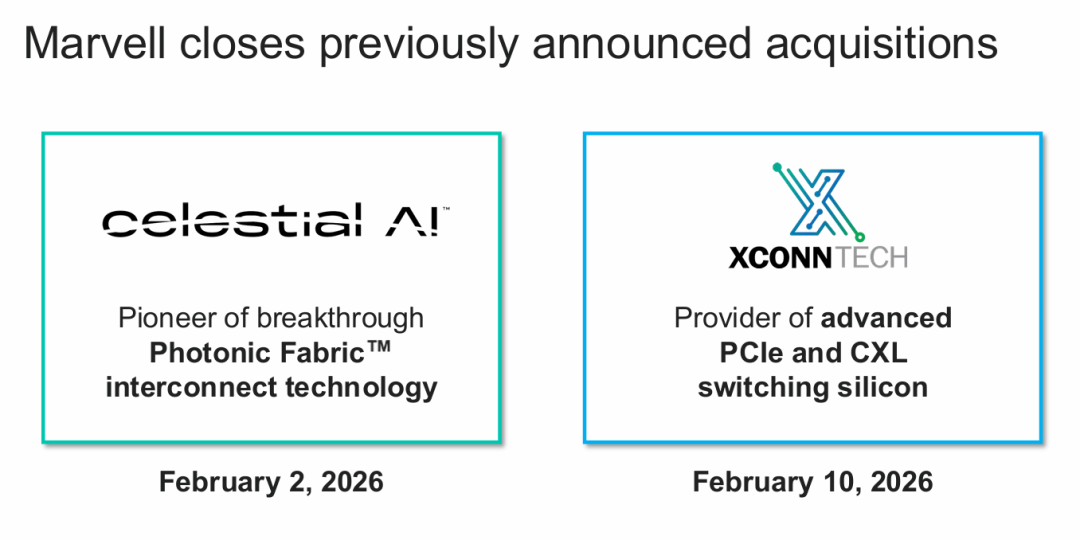

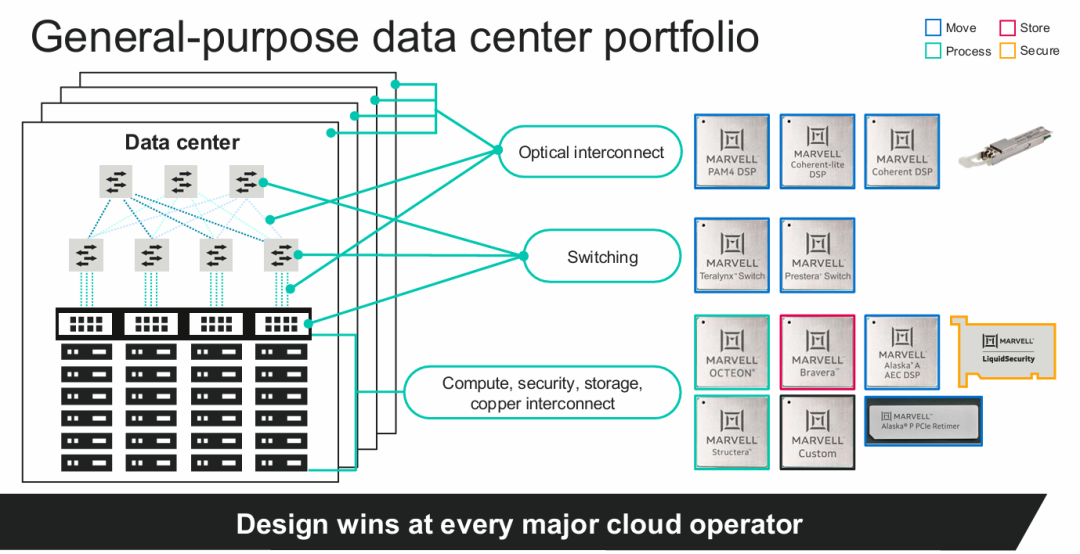

c) Acquisitions of Celestial AI & XConn: Expanding into 'Scale Out + Scale Up' Full-Scenario Solutions

① Celestial AI: Strengthens silicon photonics and CPO technology, crucial for large-scale interconnects.

Its core technology is Photonic Fabric (PF), enabling large-scale commercial deployment of CPO, with revenue contributions starting in 2028.

The company is advancing the mass production of its first-generation chiplets, targeting CPO annualized revenue of $500 million by Q4 FY2028 (i.e., $125 million per quarter) and $1 billion by Q4 FY2029 (i.e., $250 million per quarter).

② XConn: Enhances PCIe/CXL switching capabilities, expanding AI infrastructure interfaces.

With over 20 clients pre-acquisition, XConn is expected to rapidly expand through Marvell's global sales network, becoming a core player in the PCIe/CXL switching market while strengthening UA-LINK technology and accelerating large-scale switching roadmaps.

Overall (a+b+c), while the company's collaboration with Amazon in custom ASICs has not proceeded smoothly, it continues to expand its data center and related interconnect capabilities. Rather than merely 'selling cards,' the company aims to become a service provider with 'large-scale cluster capabilities.'

Given Marvell Technology's current market capitalization ($64.2 billion), it trades at approximately 23 times the adjusted P/E for FY2027 (assuming revenue +34% YoY, adjusted gross margin of 57.6%, adjusted tax rate of 10.6%), valuing it between NVIDIA (20 times P/E) and Broadcom (27 times P/E).

Recently, concerns over uncertainty in major players' future capital expenditures (a sharp slowdown in growth by 2028) and the fact that Trainium 3 is primarily handled by Taiwanese firm Alchip have contributed to the company's relatively 'sluggish' stock performance.

The company's management once again raised its operational outlook this time, directly instilling confidence. FY2027 revenue is expected to reach $11 billion, up 34% year-over-year. Even if the 'disappointing' ASIC business grows just over 20%, the high growth of optical interconnect products still presents growth opportunities.

Comparing the performances of AMD and Broadcom AVGO in the AI data center market, large cloud providers prioritize 'large-scale cluster' capabilities over merely 'selling cards.'

The acquisitions of Celestial AI & XConn, while not generating incremental revenue in the short term, demonstrate that the company has identified its strategic focus. Expanding and enriching its interconnect capabilities to become a 'large-scale cluster' service provider will help it attract more clients and enhance market competitiveness.

Here is a detailed analysis:

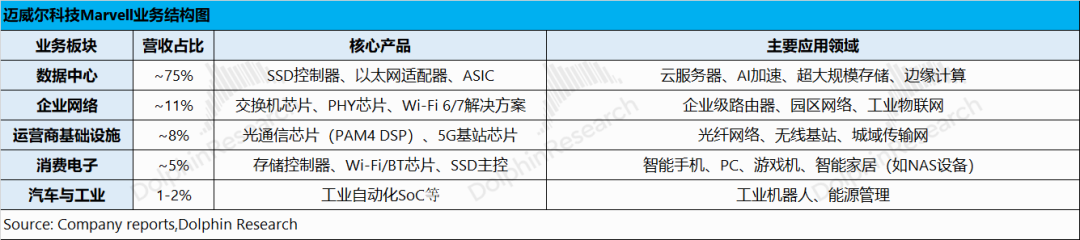

I. Marvell Technology's Business

Marvell Technology began with storage technology and later expanded its business through a series of 'external mergers and acquisitions.' The data center business has emerged as the company's largest revenue source.

Specific business segments:

1) Data Center Business (~75%): A high-growth segment driven by demand for data centers and ASICs, it is the market's primary focus. It includes optical interconnect products, SSD controllers, custom ASIC businesses (custom chips for Amazon AWS, Google Axion CPU, etc.), primarily used in cloud servers, edge computing, and other scenarios.

2) Other Businesses (~25%): The company has consolidated 'Enterprise Networking, Operator Infrastructure, Consumer, Automotive + Industrial' into a 'Communications & Others' segment.

II. Core Metrics: Steady EBITDA Growth

2.1 Revenue

Marvell Technology achieved revenue of $2.22 billion in Q4 FY2026, up 7% sequentially, meeting market expectations of $2.21 billion. The company's revenue growth this quarter was primarily driven by the data center segment, with custom ASIC and optical interconnect products as the main contributors.

2.2 Gross Profit

Marvell Technology achieved a gross profit of $1.15 billion in Q4 FY2026, up $80 million sequentially. The gross margin for the quarter was 51.7%.

Due to the impact of amortization from acquired assets on the company's gross margin, the reported margin does not directly reflect operational performance. After excluding this impact, Dolphin Research refers to the adjusted gross margin.

The company's adjusted gross margin was 58.5% this quarter, down 0.5 percentage points sequentially, primarily due to the structural impact of a higher proportion of lower-margin custom ASIC business.

2.3 Operating Expenses and Profit

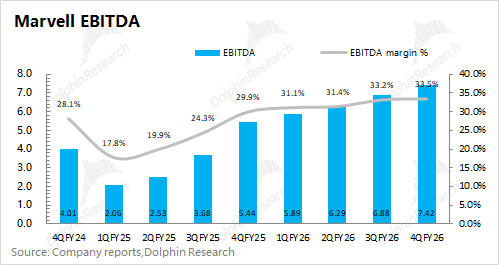

Marvell Technology achieved a net profit of $400 million in Q4 FY2026.

Excluding non-recurring factors, from an EBITDA perspective, the company's EBITDA was $740 million this quarter, with the EBITDA margin continuing to rise to 33.5%. The company's operating expenses remained stable or declined slightly this quarter, with the overall operational improvement primarily driven by increased revenue.

III. Business Segment Performance: Guidance Raised Again, Building 'Large-Scale Cluster' Capabilities

Since 2018, Marvell Technology has acquired companies like Cavium and Innovium, enhancing its ASIC and data center capabilities. With growing demand for custom ASICs and optical interconnect products from companies like Amazon and Google, the company's data center business has been on an upward trajectory, becoming the biggest driver of its performance.

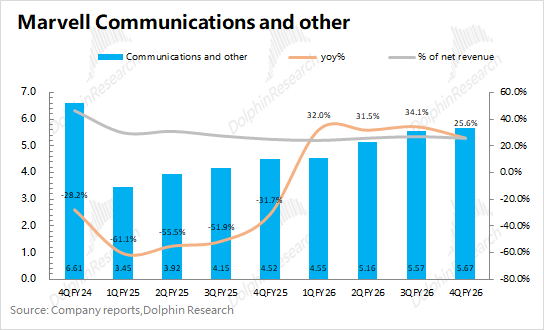

Starting this quarter, the company has consolidated its traditional businesses into 'Communications & Others,' with revenue contributions from enterprise networking, operator infrastructure, consumer electronics, and automotive & industrial all declining to around 10% or less.

3.1 Data Center Business

Marvell Technology achieved data center revenue of $1.65 billion in Q4 FY2026, up 8.8% sequentially, meeting market expectations of $1.64 billion. The growth in the company's data center business this quarter was primarily driven by custom ASIC and optical interconnect products.

Currently, AI business accounts for the majority of data center operations. Dolphin Research expects the company's AI revenue for this quarter to be approximately $960 million, a quarter-on-quarter increase of $110 million. Meanwhile, non-AI businesses such as storage products have experienced a slight quarter-on-quarter increase this quarter. The proportion of AI business in total revenue remains above 40%, aligning with the company management's previous goal of raising the AI revenue share to over 50%.

The company management has once again raised its future outlook. The company anticipates over 40% growth in its data center business in fiscal 2027, with over 50% growth in optoelectronic interconnect business and over 20% growth in custom ASIC business. The growth rate of the data center business is expected to further increase to around 50% in fiscal 2028.

Regarding the ASIC business, the company's current major client is Amazon. Amazon has recently significantly increased its capital expenditures for 2026 (with a year-on-year increase of about 50%). However, Marvell's custom ASIC business, with an annual growth rate of over 20%, still appears notably low.

From a market perspective, Amazon's latest-generation Trainium3 is manufactured by Alchip, while Marvell primarily supplies Trainium2.5 (a mid-generation upgrade of Trainium2). Marvell's market share in Amazon's supply chain has declined, resulting in Mar

① Celestial AI: Focusing on bolstering silicon photonics and Co-Packaged Optics (CPO) technology as the cornerstone for large-scale interconnection. Its core innovation lies in the Photonic Fabric (PF), which paves the way for the widespread commercial deployment of CPO, with revenue contributions slated to commence in 2028. The company is making strides towards the mass production of its inaugural generation of chiplets. It anticipates that the annualized revenue from CPO will surge to US$500 million by the fourth quarter of fiscal 2028 (US$125 million per quarter) and double to US$1 billion by the fourth quarter of fiscal 2029 (US$250 million per quarter).

② XConn: Enhancing its capabilities in PCIe/CXL switching and broadening the interfaces for AI infrastructure. Prior to its acquisition, XConn already boasted a clientele of over 20. Leveraging Marvell's global sales network, XConn is poised for rapid expansion, emerging as a pivotal force in the PCIe/CXL switching market. Additionally, it is refining its UA-LINK technology to expedite the development roadmap for large-scale switching.

When comparing the stock performance of AMD and Broadcom (AVGO) in the AI data center market, it becomes evident that major cloud providers (downstream customers) prioritize "large-scale cluster" capabilities over the mere act of "selling cards."

The acquisitions of Celestial AI and XConn, although not yielding incremental revenue in the short term, underscore the company's strategic focus. By expanding and diversifying its capabilities in the interconnect field to become a service provider for "large-scale clusters," the company aims to attract a broader customer base and bolster its market competitiveness.

3.2 Communication and Other Business Segments

This quarter, the company has revamped its business disclosure strategy, opting to present communication and other business segments as a unified entity without further segmenting them into enterprise networking, carrier infrastructure, consumer electronics, industrial, etc.

Marvell Technology reported revenue of US$570 million from communication and other business segments in the fourth quarter of fiscal 2026, marking a 25% year-on-year increase. This growth was primarily fueled by the recovery of the enterprise networking and carrier infrastructure businesses.

Looking ahead, the company anticipates steady growth in communication and other business segments, projecting around 10% growth in fiscal 2027 and single-digit growth in fiscal 2028.

- END -

// Reprint Authorization Notice

This article is an original work by Dolphin Research. Any reproduction requires prior authorization.

// Disclaimer and General Information

This report is intended solely for general comprehensive data purposes, catering to the general reading and data reference needs of users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, product preferences, risk tolerance, financial status, or unique needs of any individual recipient. Investors are strongly advised to consult independent professional advisors before making any investment decisions based on this report. Any individual who makes investment decisions using or referring to the content or information in this report assumes all associated risks. Dolphin Research shall not be held liable for any direct or indirect responsibilities or losses arising from the use of the data contained in this report. The information and data in this report are sourced from publicly available materials and are provided for reference purposes only. Dolphin Research endeavors to ensure, but does not guarantee, the reliability, accuracy, or completeness of the information and data.

The information or opinions presented in this report shall not, under any circumstances, be regarded or construed as an offer to sell securities, an invitation to buy or sell securities, nor do they constitute advice, inquiries, or recommendations regarding relevant securities or related financial instruments in any jurisdiction. The information, tools, and materials in this report are not intended for or proposed for distribution to jurisdictions where such distribution, publication, provision, or use would violate applicable laws or regulations, or to citizens or residents of jurisdictions where Dolphin Research and/or its subsidiaries or affiliated companies are subject to any registration or licensing requirements.

This report solely reflects the personal views, insights, and analytical methods of the relevant authors and does not represent the official stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is exclusively owned by Dolphin Research. Without prior written consent from Dolphin Research, no institution or individual may (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once