OpenClaw Ignites the AI Wave—The Lobster Wealth Creation Fantasy

03/06 2026

03/06 2026

600

600

What does the "lobster" craze sparked by OpenClaw signify?

Will MiniMax, Moonshot AI, Zhipu AI, and Deepseek capitalize on this momentum to surge in the capital markets?

In early 2026, the global explosion of the open-source agent product OpenClaw ("Lobster") not only tore open a new market for large model token consumption but also became the core driver for the value ascent of Chinese AI firms.

Simply put, tokens are the "computational unit of measure" for large models, representing the smallest unit of AI processing for text, code, images, and other information. Whether users ask questions, AI responds, or models execute tasks and generate content, tokens are consumed. Enterprises charge developers and corporate clients based on token usage, with token consumption directly determining the revenue scale of large model companies.

The proliferation of OpenClaw propelled the large model industry from conversational interaction to task execution, with token consumption growing exponentially. Data shows that Chinese models accounted for 61% of token consumption among the top 10 global models on the OpenRouter platform, with MiniMax, Moonshot AI, and Zhipu AI dominating the rankings, fundamentally altering the global AI competition landscape. At the capital market level, MiniMax and Zhipu AI both surpassed HK$300 billion in Hong Kong stock market value, while Moonshot AI completed large-scale financing, with its valuation rapidly climbing to the US$10 billion level.

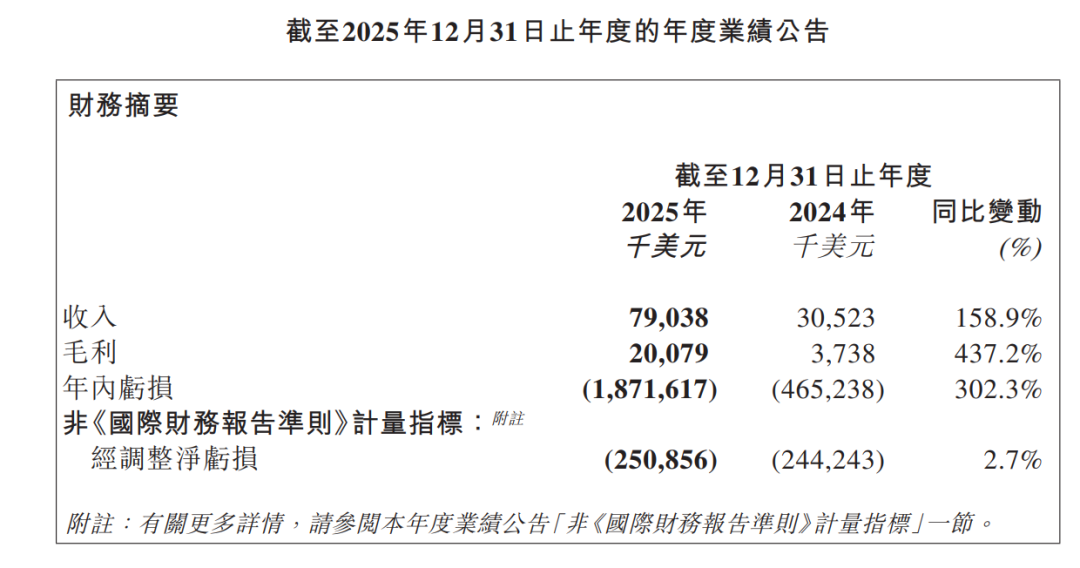

As MiniMax disclosed the industry's first financial report, its revenue model, growth drivers, and the rationale behind its high valuation drew significant market attention.

As the first large model company to disclose a complete financial report, MiniMax's business model became a sample for industry observation. The report revealed that the company achieved US$79.04 million in revenue in FY2025, a 158.9% YoY increase, with overseas revenue accounting for 73% and gross margin improving from 12.2% to 25%. The core revenue came from B-side API interface services and enterprise solutions billed by tokens, with this business segment exceeding 60% gross margin, serving as the primary profit pillar. After the OpenClaw boom, the daily average token consumption of its core model surged sixfold compared to December 2025, with demand for programming-related packages skyrocketing tenfold, directly validating the commercialization path of "tokens as revenue, models as income."

In terms of business layout, MiniMax explicitly abandoned the general-purpose AI assistant track, focusing on agents, multimodality, and vertical scenario applications. It launched deployment tools compatible with the OpenClaw ecosystem, swiftly meeting global developer demand. Moonshot AI achieved breakthroughs in overseas markets with extreme cost-effectiveness, experiencing rapid growth in API revenue and user base. Zhipu AI leveraged its technical strength to dominate the developer market but faced issues like computational strain and service fluctuations due to surging traffic, exposing the widespread infrastructure pressures in the industry.

Industry analysts pointed out that the current high valuations of leading companies are primarily based on long-term growth expectations in the agent era: scenarios like programming, office automation, and multimodality will drive sustained token demand, redefining industry potential.

However, multiple risks lie behind these high valuations: the industry has yet to achieve profitability, with sustained investments creating significant financial pressure. Intensifying price wars may compress per-token profit margins. Insufficient computational reserves, slowed technological iteration, and stricter overseas regulations could all impact corporate development.

Market perspectives suggest that MiniMax holds relative advantages in globalization, commercialization, and stability, with a currently clear business model. However, its HK$300 billion valuation already highly reflects future growth expectations. If subsequent token growth falls short, competition intensifies, or operational fluctuations occur, valuation adjustments may follow. In the long run, the large model industry will gradually consolidate, with platform-based companies possessing technological barriers, ecological capabilities, and cost advantages more likely to navigate cycles.

As the industry dividends driven by OpenClaw continue to spread, the commercialization of large models officially enters the deep waters. The competitive landscape among MiniMax, Moonshot AI, and Zhipu AI has preliminary taken shape, with the future focus shifting from technical parameters to commercialization efficiency, computational power security, and globalization capabilities. The industry's final outcome remains undetermined.

01 The Lobster Wealth Boom: Token Extravaganza, AI Wealth Race

From dominating the OpenRouter rankings to soaring market caps and valuations, from surging API revenue to open financing windows, this wealth creation movement sparked by OpenClaw has solidified the global AI competition standing of Chinese large model companies. The differentiated performances of the three players also outline a new competitive and cooperative landscape for China's large model industry in the agent era.

The explosion of OpenClaw is essentially a token consumption extravaganza. As a desktop-level agent tool, its continuous background process execution feature (characteristic) drives geometric growth in per-task token consumption compared to ordinary chatbots, directly activating massive global model invocation demand. In the latest weekly ranking from February 16-22, four of the top five models by platform invocation volume came from Chinese vendors: MiniMax's M2.5, Moonshot AI's Kimi K2.5, Zhipu's GLM-5, and DeepSeek's V3.2. These four models collectively contributed 85.7% of the total Top 5 invocation volume. A year earlier, Chinese models held less than 2% of this platform's share.

The underlying logic of commercial realization has also been thoroughly activated (thoroughly activated) by OpenClaw. MiniMax's first publicly disclosed financial report from a global large model company revealed US$79.04 million in FY2025 revenue, a 158.9% YoY surge, with 73% from overseas markets and gross margin doubling from 12.2% to 25%. The core driver was the explosion in token invocations—the M2 text model's daily average token consumption in February 2026 surged sixfold compared to December 2025, with programming packages skyrocketing tenfold, officially validating the "models as income" business model. Moonshot AI leveraged the price advantage of Kimi K2.5 to become the top choice for overseas SMEs. A European development studio noted that 80% of its daily reasoning tasks were completed by K2.5, costing just US$5-10 per day, whereas using Claude exclusively would cost US$800-1,500 monthly—a sixfold price difference enabling Moonshot AI's rapid overseas breakthrough. Zhipu's GLM-5, with programming capabilities approaching Claude Opus 4.5, once dominated the OpenRouter rankings, becoming a popular choice for developers worldwide and experiencing explosive short-term traffic growth.

Assuming a production-grade agent processes 1 billion output tokens daily (i.e., 1,000 million-token units), using Claude would cost approximately US$15,000 per day; the same scale would cost around US$1,100 with MiniMax.

Facing this surging trend, Moonshot AI took the lead by launching the one-click deployment tool Kimi Claw on February 18, with advanced users spending at least 199 yuan monthly to capture the first wave of ecological dividends. MiniMax followed with MaxClaw on February 26, supporting cloud-based server-free and API key-free deployment, accessible to basic members. After launch, it completed four emergency expansions within 120 hours due to overwhelming demand and officially announced a mobile version for multi-terminal collaboration. Zhipu also deeply integrated GLM-5 with OpenClaw, becoming a core choice for early developers and rapidly implementing ecological layout (layout).

02 Divergent Competition: The Capability Test Behind the Dividends

While sharing OpenClaw's dividends, MiniMax, Moonshot AI, and Zhipu have followed starkly different growth trajectories. Their differentiated performances essentially reflect an ultimate test of comprehensive corporate capabilities, with gaps in computational reserves, commercialization efficiency, and product iteration speed gradually widening the distance among the three players in the wealth race.

Model differences have evolved into competitions over unit cost, stability, and reasoning smoothness in long-flow, high-frequency invocation, and long-context environments.

As the "trendsetter" in this wealth boom, MiniMax's core strengths lie in globalization + stable computational power + commercialization efficiency. Its 73% overseas revenue share makes it one of the few Chinese large model companies achieving global scaled revenue, laying the foundation for meeting global OpenClaw demand. Amid surging token volumes, MiniMax avoided significant service disruptions, while its enterprise services' over 60% gross margin significantly boosted overall profitability. The implemented "token fee - inference cloud cost" profit model makes it a viable option for large model commercialization.

Caption: MiniMax achieved US$79.04 million in FY2025 revenue

MiniMax founder Yan Junjie abandoned the general-purpose AI assistant track as early as 2023, focusing on agent products, vertical domains like Xingye and Hailuo Video, and proposing the core formula "AI platform value = intelligence density × token throughput," aligning with OpenClaw's agent wave.

03 Moonshot AI: Cost-Effectiveness Breakthrough, Overseas Dark Horse

Moonshot AI's rise represents a victory of extreme cost-effectiveness + rapid iteration. As the youngest player among the three, Moonshot AI avoided direct competition with industry giants, leveraging the high cost-effectiveness and rapid iteration capabilities of its Kimi series models to achieve rapid overseas breakthroughs. Switching Kimi Code Plan to token-based billing and launching a limited-time "3x quota" promotion precisely met developers' cost needs under the OpenClaw ecosystem, driving daily token consumption and stable service user counts to multiply. Its early launch of Kimi Claw also secured an ecological binding advantage, becoming a key choice for overseas developers accessing OpenClaw.

From a financing perspective, Moonshot AI's valuation doubling and over US$1.2 billion in funding reflect capital market recognition of its overseas layout (layout) and product strategy, while overseas revenue surpassing domestic performance makes it a typical sample of Chinese large model companies going global.

Zhipu emerged as the most dramatic player in this wave, soaring to the top of the rankings before falling, exposing core shortcomings of insufficient computational reserves and delayed resource expansion. GLM-5, with programming capabilities approaching top overseas models, briefly dominated the OpenRouter rankings, driving explosive demand from developers worldwide. However, rapid traffic growth directly strained computational resources, causing service queues, response delays, and disruptions. Despite multiple expansions of domestic chip clusters and limited sales of GLM Coding Plan packages, fundamental issues remained unresolved.

The ripple effects of the computational crisis became apparent quickly: on February 21, Zhipu issued an apology letter acknowledging three major issues—surging computational consumption, delayed resource expansion, and volatile user experience. On February 23, its stock price plummeted 22% at market open, erasing over HK$100 billion in a single day. From February 23-28, GLM-5 fell out of the OpenRouter top 9 rankings, with many developers switching to more stable models like MiniMax and Moonshot AI, missing a critical window of OpenClaw dividends. Although the stock price later recovered, this crisis raised market doubts about Zhipu's computational shortcomings.

04 Industry Restructuring: The Agent Era Arrives, Large Model Competition Enters a New Cycle

The wealth boom sparked by OpenClaw represents more than a simple industry dividend—it marks a fundamental shift in the large model industry's competitive core from model parameters and conversational capabilities to agent adaptability, commercialization efficiency, and computational stability. China's large model industry has entered a Thoroughly Refactoring (completely restructured) development cycle, with MiniMax, Moonshot AI, and Zhipu providing crucial insights for the sector.

From an industry trend perspective, agents have become the core entry point for large model commercialization, with token consumption serving as the key metric for corporate commercial value. MiniMax founder Yan Junjie predicts that programming, office agents, and multimodal content output will drive token demand to grow by 1-2 orders of magnitude, with future competition among large model companies revolving around token throughput. NVIDIA CEO Jensen Huang's proposition of "computational power as revenue" aligns with this trend, making computational reserves and resource allocation capabilities core corporate barriers.

From a market landscape perspective, Chinese large model companies have significantly elevated their global market influence, but industry differentiation will intensify further. The differentiated performances of MiniMax, Moonshot AI, and Zhipu demonstrate that technological superiority alone cannot sustain corporate development. A comprehensive competition of global layout , commercialization efficiency, computational reserves, and ecological binding capabilities will become the market's core. Meanwhile, entries from Alibaba, Tencent, and Baidu further intensify industry competition—Baidu launched one-click OpenClaw deployment services, Tencent internally tested WorkBuddy, and Alibaba open-sourced CoPaw while introducing cost-effective Coding Plan packages. The resource advantages of these tech giants will further squeeze the survival space of smaller players, potentially leaving only a few core players in the future.

The dividends brought by OpenClaw are just the starting point—the true competition in the agent era has only begun. How to continuously improve (continuously improve) model capabilities and consolidate global market positions, how to improve (perfect) computational reserves to meet growing token demand, and how to deepen ecological layout (layout) to build irreplaceable core competitiveness will become the core issues Chinese companies must address. This wealth race sparked by "lobster" will continue reshaping China's large model industry landscape, propelling Chinese AI to take firmer strides in global competition.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once