'Old Deng' Tencent: It's Time to Lose the 'Deng' Flavor and Embrace AI!

03/19 2026

03/19 2026

595

595

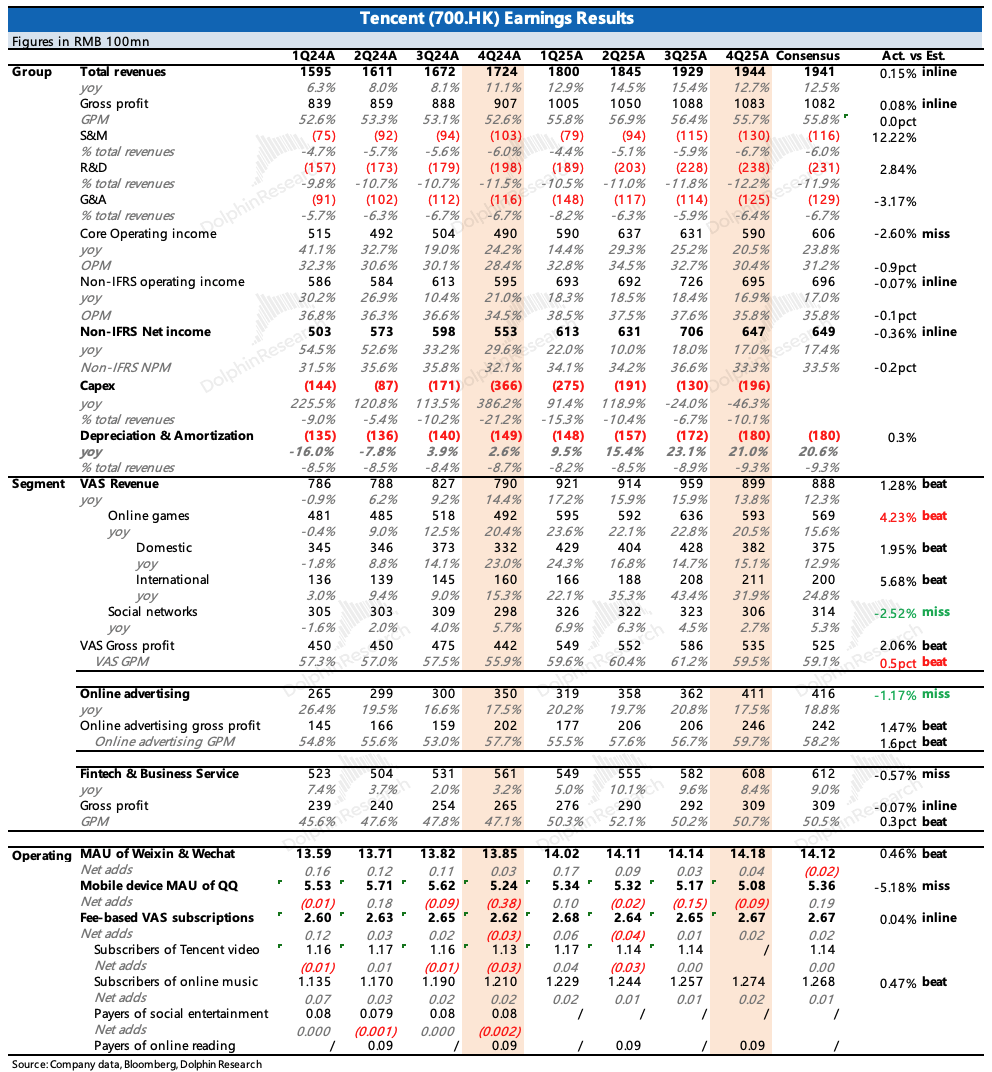

After the Hong Kong market closed on March 18 (Beijing Time), Tencent released its Q4 2025 earnings. Overall, there were no major surprises, with slight deviations from expectations in specific areas. Compared to current performance, management's guidance on business investment and growth expectations for the year is more critical to mid-term valuation amid the key AI transformation window.

Key takeaways:

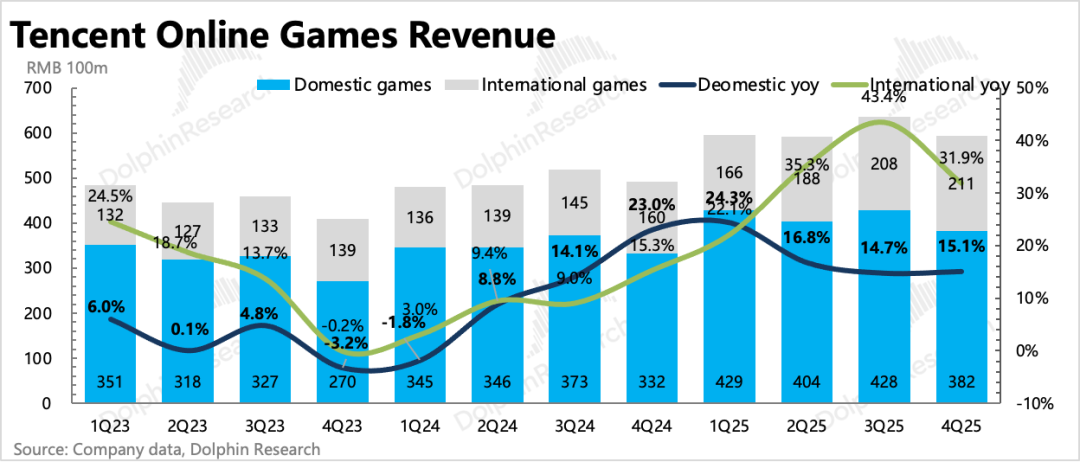

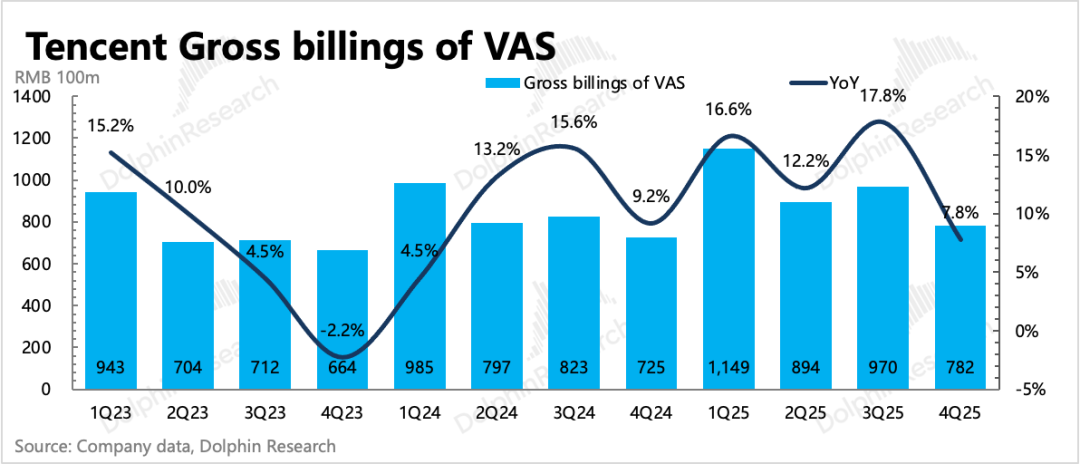

1. Gaming exceeds expectations, expected to remain growth core this year: This product cycle has been strong, with not only new games performing well but also sustained growth driven by evergreen titles. Q4 revenue grew 21%, with 15% growth domestically and 32% overseas.

Since no major new games launched in Q4, domestic growth was primarily driven by relatively new titles like Delta Force and VALORANT series, along with evergreen titles like Peacekeeper Elite. Overseas performance still relied on Supercell and PUBG MOBILE.

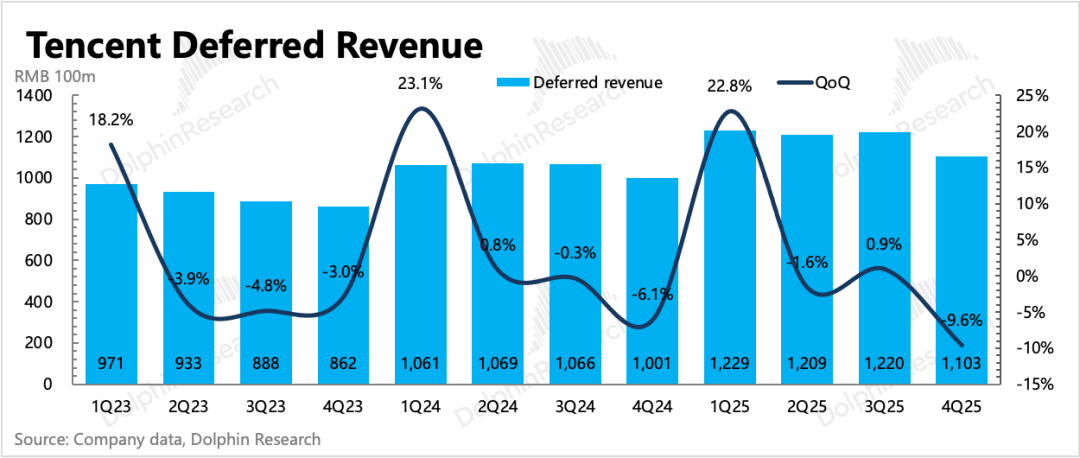

Deferred revenue shows Q4 value-added services revenue declined 10% QoQ, a larger drop than usual. Besides slower music and video subscription growth directly dragging down revenue, game revenue itself performed normally.

Tencent's games performed well during Chinese New Year. While Peacekeeper Elite weakened in Q4, it rebounded during the holiday. Additionally, two major new titles—Rock Kingdom and Honor of Kings World—are scheduled for release in H1, expected to quickly fill gaps.

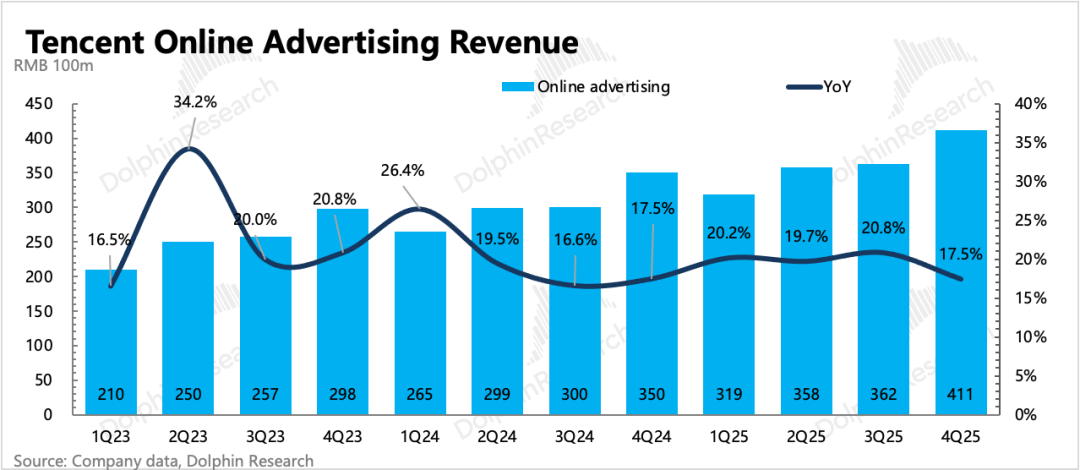

2. Advertising slows, inventory release potential remains: Ad revenue grew 18% in Q4, decelerating by 3pct QoQ. Besides high base effects, weak consumer sentiment also contributed. According to Dolphin Research, ads on Weixin Channels, mini-games, search, and Tencent Music performed well in Q4, but Weixin Official Accounts declined significantly, while media ads (QQ, Sogou, Tencent News) continued to drag.

Currently, Weixin Channels' ad load remains low at 4-5%, with cautious increases. Short-term ad growth relies on AI-driven recommendation efficiency improvements, while mid-long-term growth can be achieved through more inventory release.

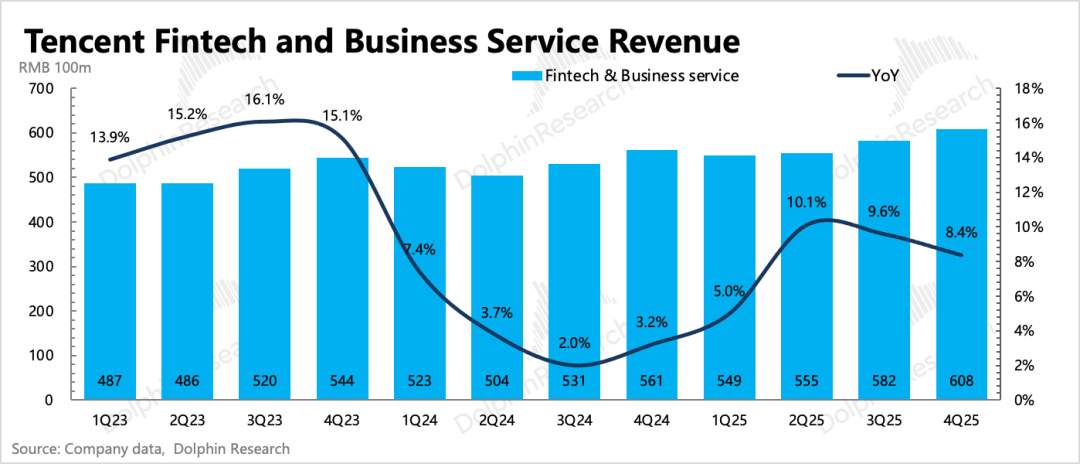

3. Fintech recovery sluggish, pure compute leasing not preferred: Combined fintech and enterprise services revenue grew 8%, roughly in line with expectations, with enterprise services up 22% (including Weixin Store commissions) and fintech estimated at low-single-digit growth. No clear sustained recovery trend compared to previous quarters.

Tencent Cloud revenue within enterprise services is expected to remain stable at 10-20% growth, not following the current compute demand trend. The core reason is that with limited compute supply, Tencent prioritizes internal use and shows little interest in pure GPU leasing services unless Agent clients explicitly demand compute resources.

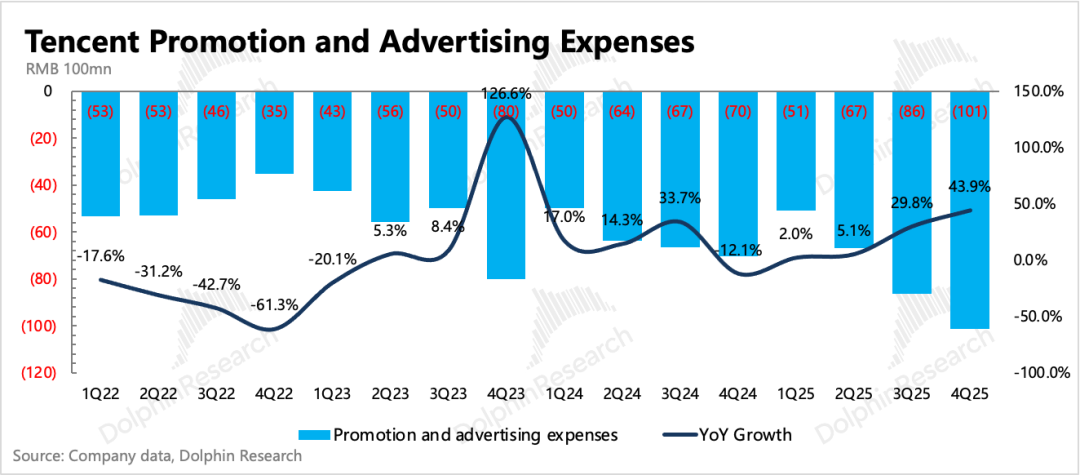

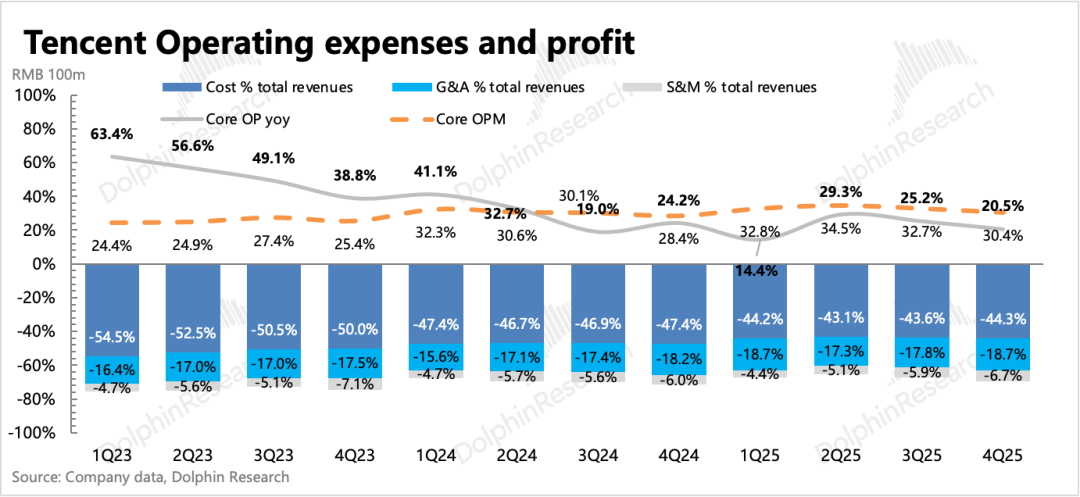

4. Cost optimization but expenses rise: Operating profit margin improved by 2pct YoY. However, Q4 saw significant marketing spend on AI products like Yuanbao, with promotion expenses up 44% YoY and increasing by RMB 1.5 billion QoQ. Besides minor new game marketing, most was spent on Yuanbao user acquisition, suggesting Q1 sales expenses will be even higher.

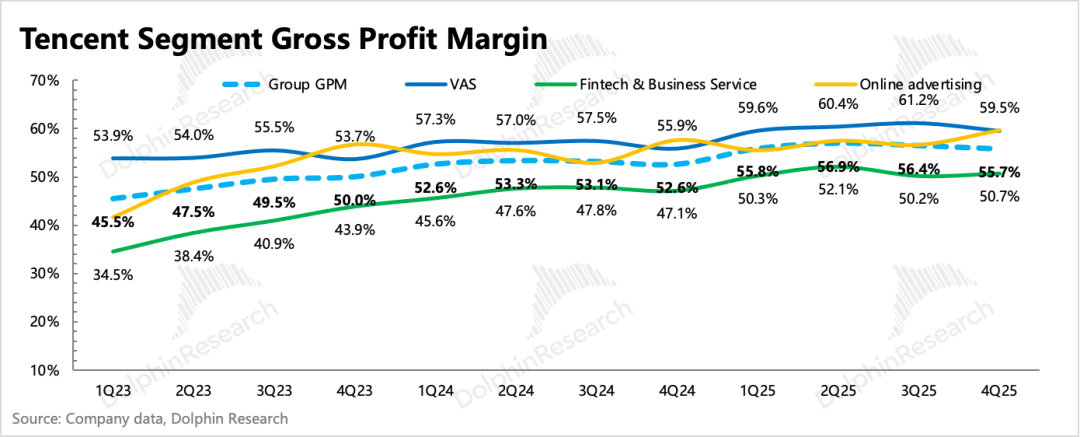

Other major expense increases came from AI-related server costs and R&D personnel. Overall operating expenses rose 0.5pct YoY, offset by gross margin improvements. Gross margins for all three major businesses improved to varying degrees, driven by increased self-developed game ratios (reducing revenue sharing) and higher Weixin Channels ad ratios.

5. Increased investment may compress shareholder returns: Regarding cash flow and capital allocation, Dolphin Research focuses on capital expenditures and buybacks. Net cash on hand was RMB 107.1 billion in Q4 (cash + short-term investments minus short-term borrowings and notes payable), up nearly RMB 5 billion QoQ.

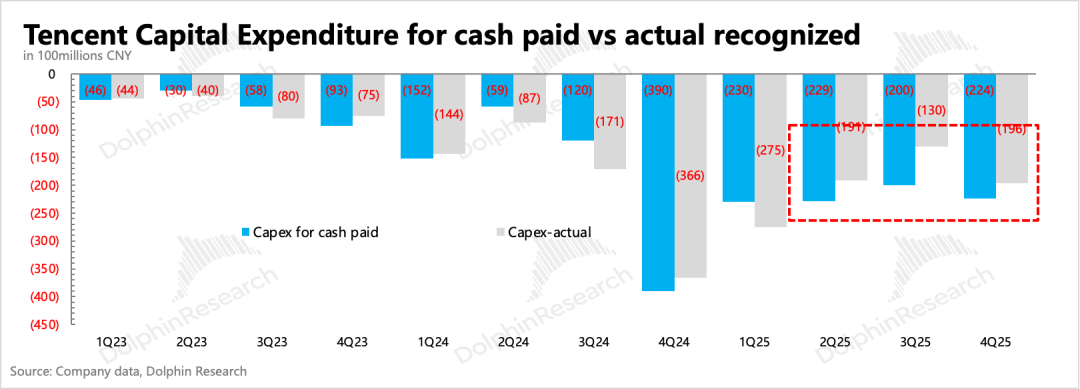

Q4 capex was RMB 19.6 billion, increasing QoQ. However, actual cash outflow was RMB 22.4 billion, indicating prepayments. Even considering cash outflow scale, 2025 full-year capex will likely be under RMB 90 billion, suggesting a significant budget increase this year.

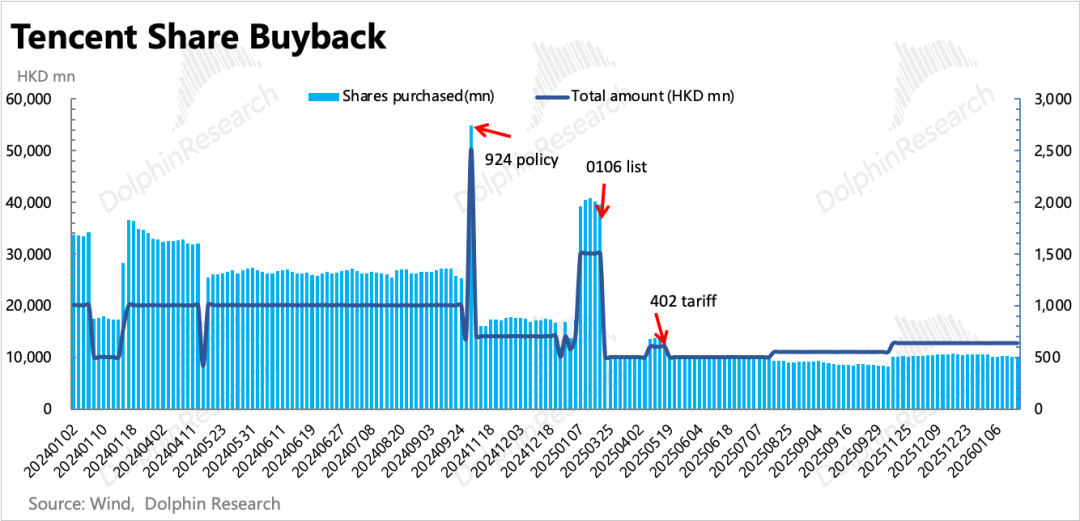

Q4 share buybacks totaled HKD 19.6 billion, with HKD 77.2 billion for the full year. Additionally, a HKD 5.3 per share dividend was announced, projecting HKD 48 billion in dividends, up 18% YoY. If all excess funds go to AI investment (domestic/overseas compute deployment, more product model development), buybacks may remain constrained, potentially lowering shareholder returns below 2.5%.

6. Detailed earnings data overview

Dolphin Research's View

Tencent's stock price has corrected significantly recently, now trading near historical lows at 13-14x P/E. This decline relates less to current performance and more to concerns about AI or competitor-driven growth erosion. Thus, a lackluster earnings report alone won't directly boost the stock price.

Compared to static results, funds will focus more on management's strategic vision and AI progress during this critical AI competition window.

Early this month, Tencent rushed multiple 'Lobster' products to market, reflecting anxiety after losing the Chinese New Year battle with Yuanbao, despite imperfect product launches. This urgent shift is crucial and necessary.

Currently, Weixin's entry points seem unshakable amid AI-native app proliferation, but rapid industry changes remind us no one can be 100% confident.

From this perspective, Dolphin Research welcomes Tencent's increased capex over shareholder returns. Management's style suggests Tencent won't blindly squander funds like Meta on unnecessary expenses.

While Q2-Q3 discussions revealed cautious investment (capex at 10% of revenue, below global tech peers), we also see supply-side improvements through policy easing, domestic capabilities, and overseas data center deployments.

In the short-medium term, gaming product cycles and ad inventory release can provide Tencent with confidence during its investment phase. Both growth momentum and business model scale effects offer room for overall efficiency gains, supporting AI and business expansion investments while maintaining stable cash flows.

Detailed analysis below:

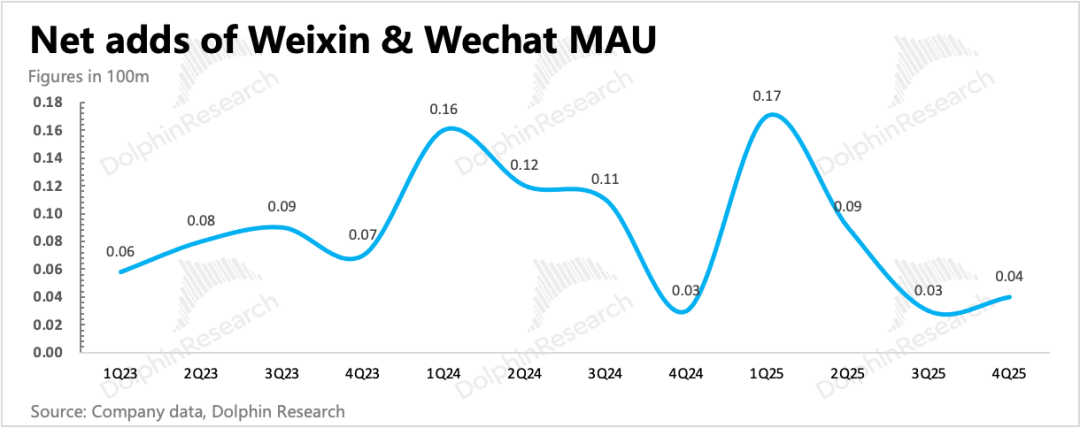

1. Stable Weixin ecosystem

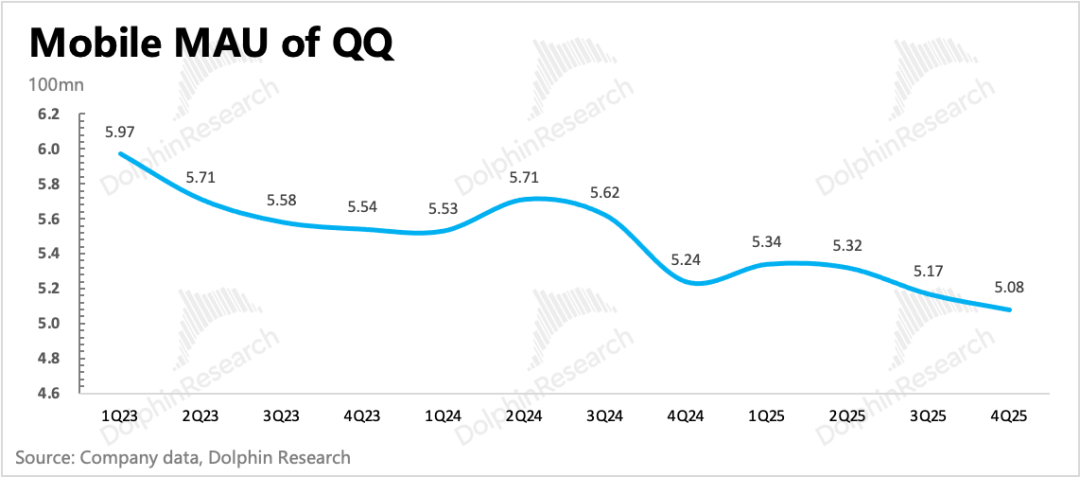

Weixin MAUs reached 1.418 billion in Q4, up 4 million QoQ, maintaining steady but slowing expansion. QQ continued declining.

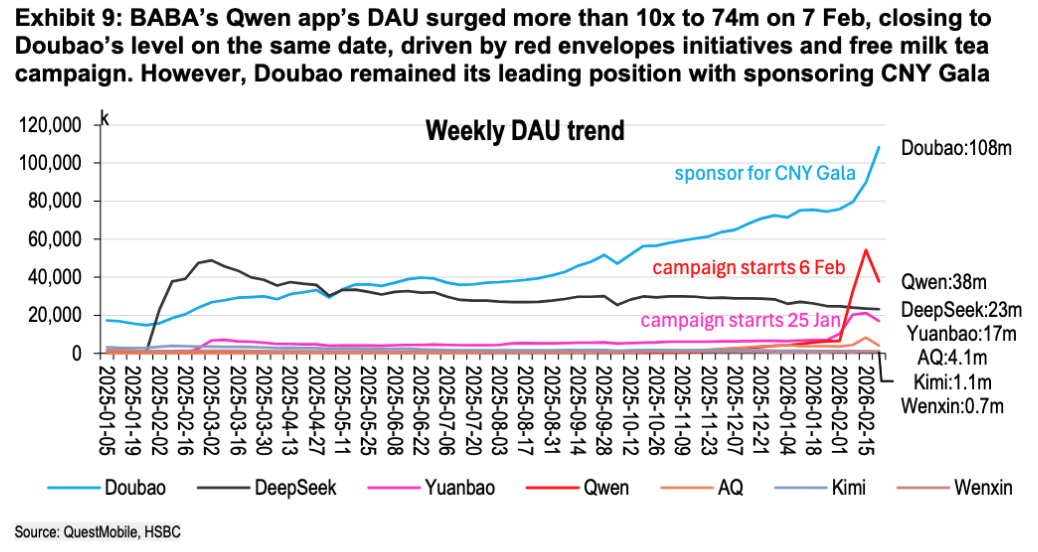

Among AI chatbots, Yuanbao app downloads rebounded significantly from early-year marketing but face fierce competition from Qianwen (boosted by food delivery red packets) and Doubao (gaining traction from Spring Festival Gala sponsorship).

However, Tencent now focuses on developing Agent or OpenClaw-related products within Weixin/QQ entry points. This aligns with our view that while Yuanbao remains Tencent's key AI product, it serves more as a testing ground medium-to-long term.

Once mature, these products will integrate with Weixin/QQ entry points—a core tenet of Tencent's AI strategy: making AI ubiquitous in its ecosystem for instant user access and experience.

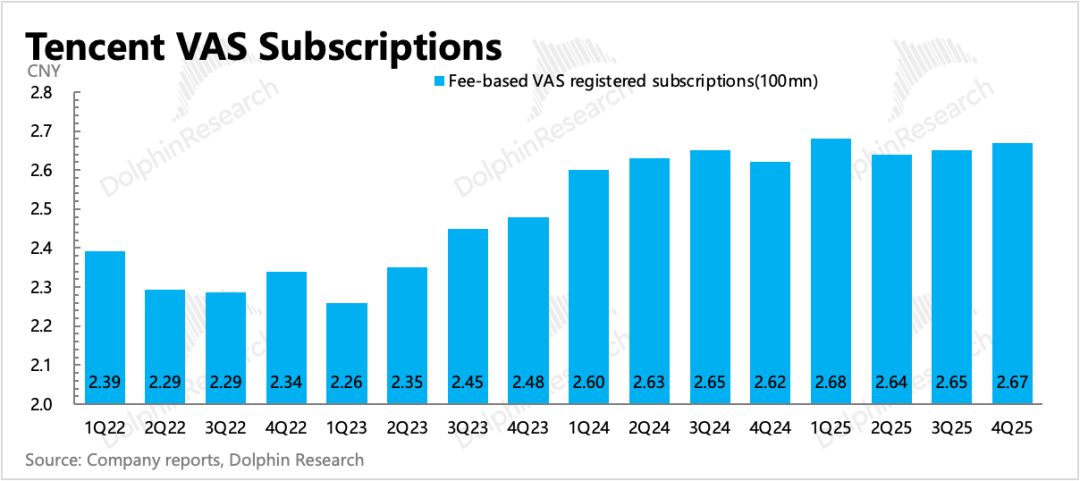

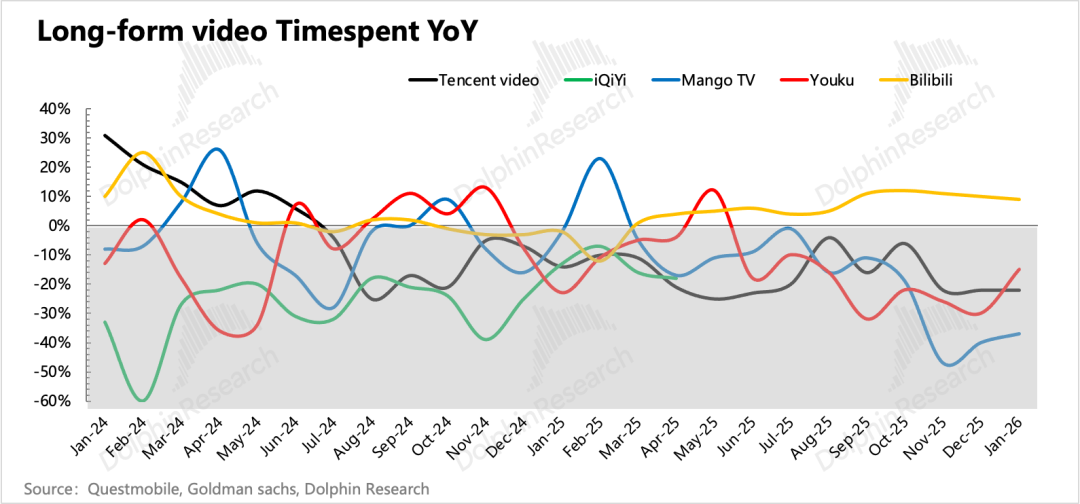

Q4 value-added services paid users increased by 2 million to 267 million. Growth mainly came from Tencent Music (1.7 million). Tencent Video membership numbers weren't disclosed, but QM data shows long-form video engagement has 'plummeted'.

2. Gaming exceeds expectations, remains growth pillar this year

Q4 online games revenue grew 21% YoY to RMB 59.3 billion, with 15% domestic and 32% overseas growth (1pct FX tailwind).

With no major new game launches in the quarter, domestic growth came from titles released in the previous year like VALORANT Mobile, Delta Force, and Wuthering Waves.

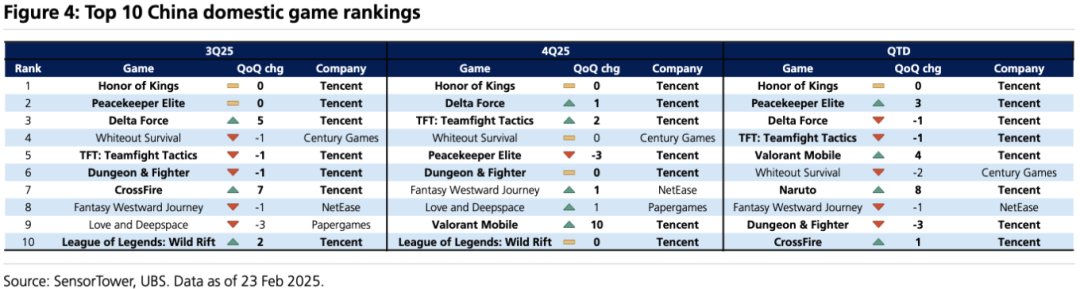

However, for a leading gaming company like Tencent, new game reserves no longer fully represent future revenue fluctuations. Operational improvements and content updates for existing games contribute as much as mid-sized new titles.

For example, Legend of Runeterra returned to iOS's top 3 revenue charts in November-December, while Peacekeeper Elite (weak in Q4, down 3 ranks) rebounded during Chinese New Year after a Dunhuang map update, setting new DAU records.

Deferred revenue-derived flow indicators better represent true demand. Q4 value-added services flow declined 10% QoQ, a larger drop than usual. Besides slower music/video subscriptions dragging down revenue, game flow performed normally.

Tencent still has rich pipeline reserves. While Reverse: Future underperformed after its early-year launch, scheduled titles like Rock Kingdom: World and Honor of Kings World will significantly boost Q2 game flow, with titles like Yi Ren Zhi Xia, Lost Control Evolution, and Honor Arena Chess planned for 2026.

3. Ad growth slows slightly but inventory release potential remains

Despite weak consumer sentiment in Q4, Tencent's advertising maintained ~18% growth, slightly missing BBG consensus. Some firms have slightly lowered ad expectations since early 2026 due to weak consumption.

Short-term AI-driven recommendation efficiency gains allow Weixin Channels and Search ads to maintain high growth at low ad loads. However, sustained mid-long-term growth will require inventory release.

4. Weak consumption slows fintech recovery

Q4 fintech enterprise services grew ~8% YoY, slowing QoQ. Enterprise services grew 22% (including Weixin Store commissions), while fintech likely grew at low-single digits. No clear sustained recovery trend compared to previous quarters.

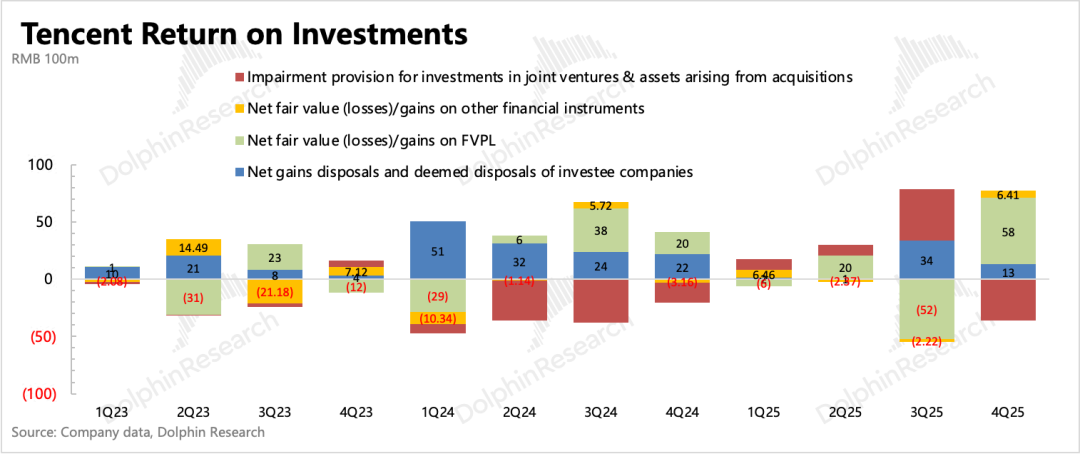

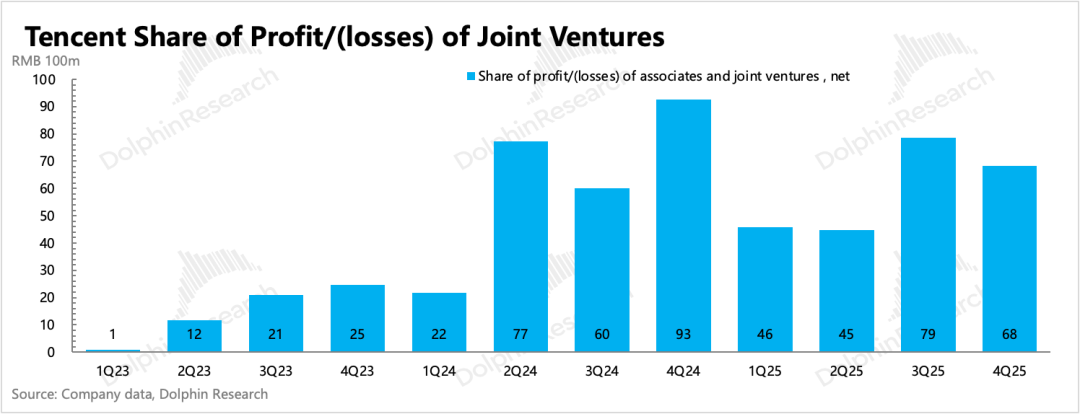

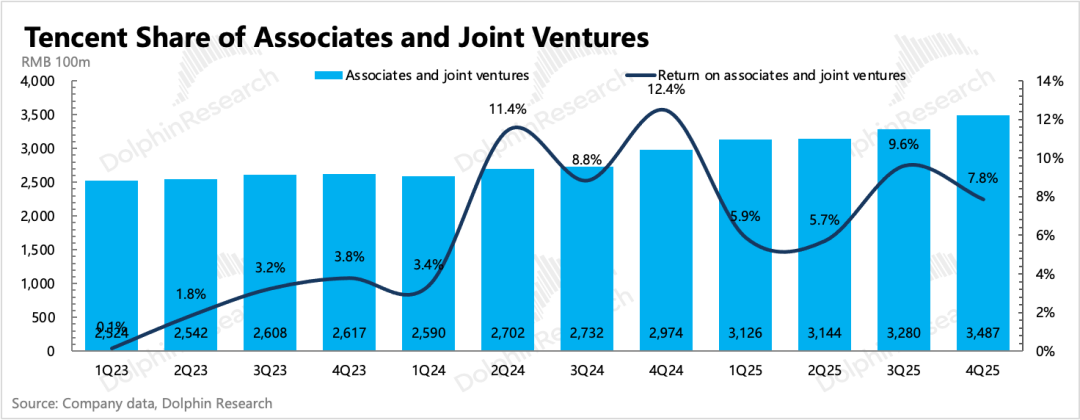

5. Investment gains: Fair value increases in investment assets

Regarding investment gains, Dolphin Research focuses primarily on two components based on the original indicator definitions (confirmation scope before 2025): net other income (including investment gains) and share of profits from associates/joint ventures.

In Q4, comprehensive investment gains increased quarter-over-quarter, primarily driven by fluctuations in financial fair value, offsetting impairment provisions for intangible assets from invested companies. Regarding share of profits, nearly RMB 6.8 billion was confirmed in Q4, representing a significant year-over-year decline mainly due to a large non-recurring gain recognized by an associate company last year, resulting in a high base.

As of the end of Q4, the combined asset scale of the company's associates/joint ventures totaled RMB 348.7 billion, resulting in a calculated investment return rate of 7.8% (annualized) for Tencent, a slight decline from Q3.

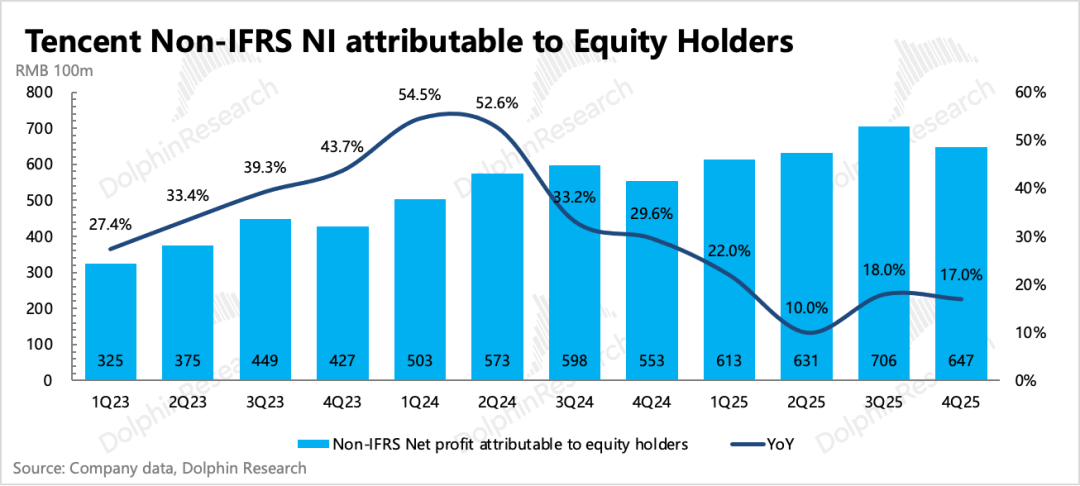

VI. Steady Improvement in Profitability, but Growth Investments Expected to Continue Impacting

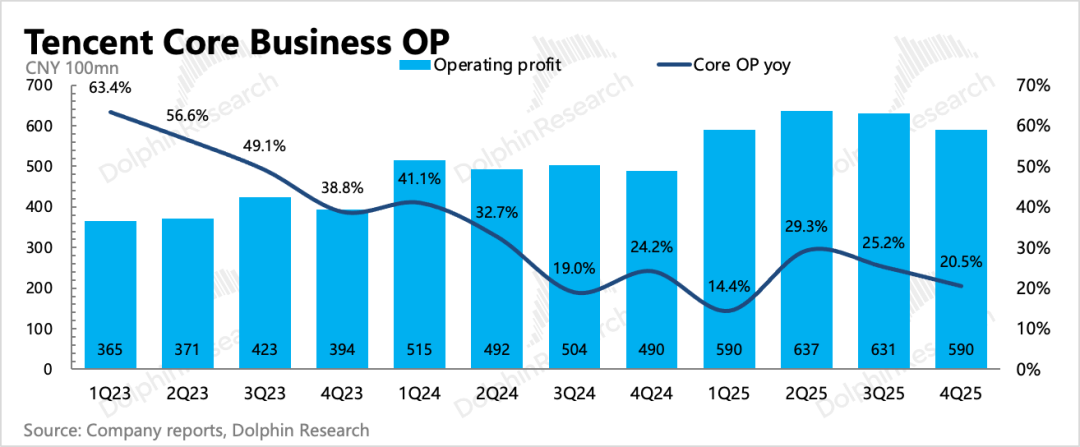

In Q4, adjusted net profit reached RMB 64.7 billion, up 17% year-over-year, meeting expectations. However, operating profit from core businesses (gross profit - operating expenses), which excludes the fluctuating impact of share of profits from associates + certain miscellaneous items, actually grew by 21% year-over-year, slightly below expectations, primarily due to increased marketing expenses. The core operating profit margin stood at 30.4%, up 2 percentage points year-over-year, continuing the trend of profitability improvement.

In Q4 alone, promotion expenses surged 44% year-over-year, with an additional RMB 1.5 billion spent quarter-over-quarter. Apart from a small amount spent on promoting new games, the majority was likely used for user acquisition for Yuanbao, indicating that Q1 sales expenses will only be higher. Other significant expense increases were mainly related to AI server costs and R&D personnel expenses.

Overall operating expense ratio continued to rise by 0.5 percentage points year-over-year but was offset by improvements in gross profit margin. Gross profit margins for all three major businesses improved to varying degrees, driven by factors such as an increased proportion of self-developed games (reducing revenue sharing) and a higher proportion of WeChat Channels advertising.

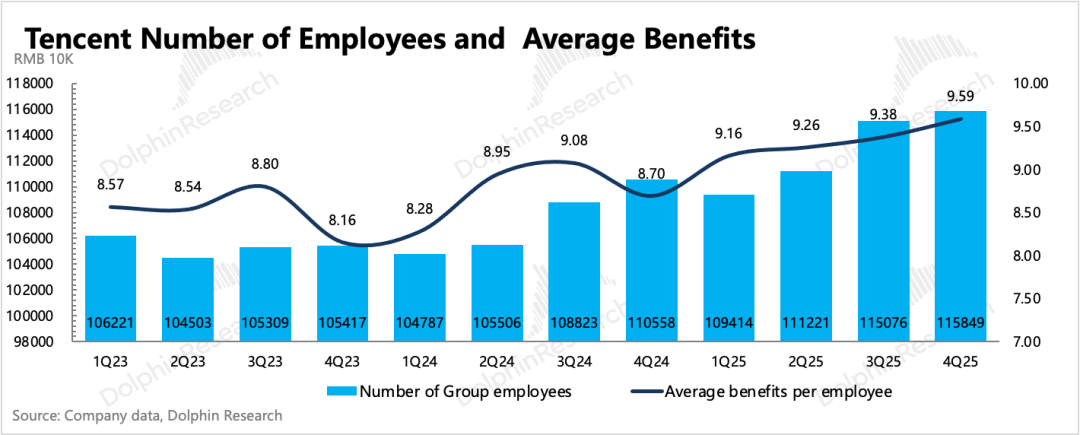

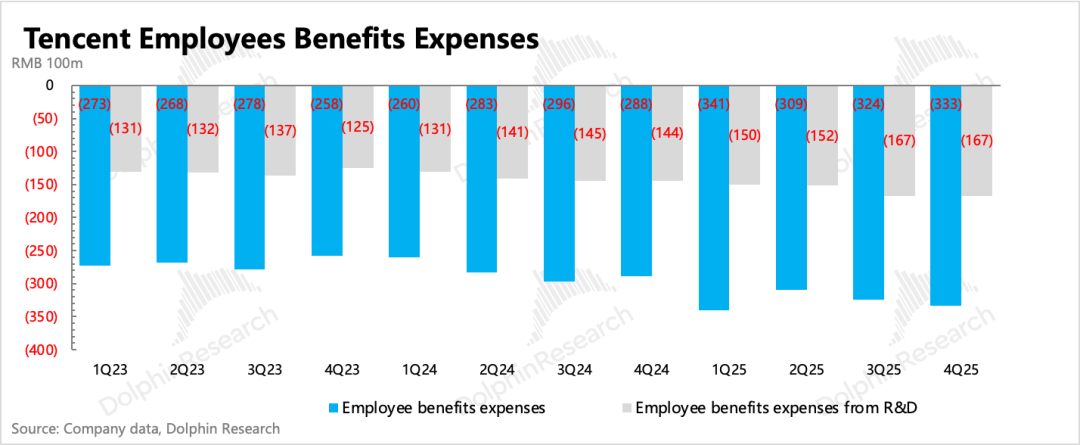

Future short-to-medium-term profit margin changes may be affected by ongoing investments. Although adjustments to Apple's fees will benefit the improvement of Tencent's value-added services' gross profit margin, AI investments will gradually be reflected in depreciation costs, computing power leasing fees, and potentially increased R&D personnel costs in the short term (the company stated last quarter that it prefers to increase business revenue generation through AI efficiency gains rather than layoffs, suggesting no significant short-term layoffs but rather control over personnel growth, as evidenced by a net increase of 773 employees in Q4, a significant decrease from the previous quarter). In the medium to long term, overall operating efficiency improvements may positively drive profit margins.

On the other hand, Tencent's diverse business structure and commercial models facilitate resource reuse and allocation, reducing unnecessary expenditure waste and striving to maintain overall profit margin stability.

In Q4, capital expenditures reached RMB 19.6 billion, increasing quarter-over-quarter. However, compared to cash outflows, there were still instances of prepayment without delivery. Although Tencent's management, known for its prudent operating style, indeed places greater emphasis on ROI, the occurrence of prepayment issues for three consecutive quarters reflects that the problem primarily lies in the computing power supply side.

VII. Slowdown in Major Shareholder's Share Reduction

Finally, let's briefly examine the repurchase and selling situation.

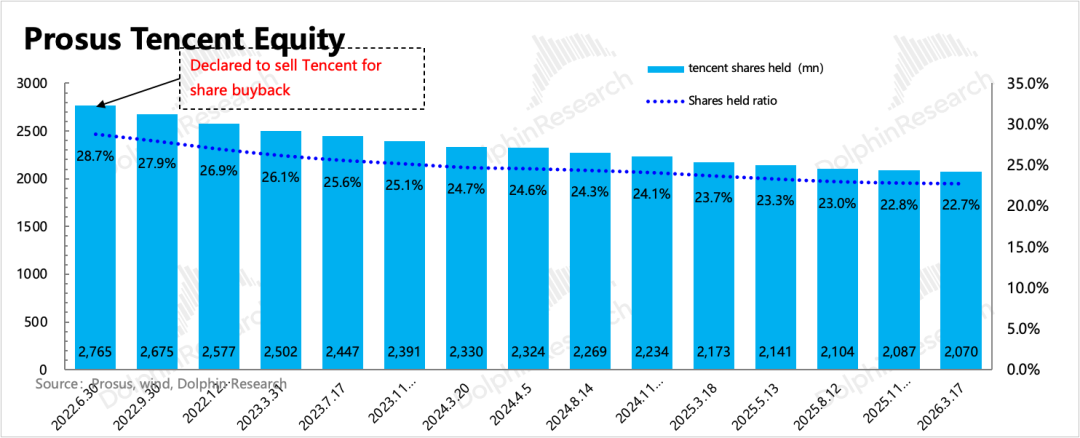

Over the four months since the last earnings report, Tencent's total share count decreased by 39 million shares net. However, the major shareholder's selling intensity remained flat quarter-over-quarter, slowing down compared to previous periods. The monthly average selling volume continued to decline, totaling 16 million shares sold. As of yesterday, Prosus's equity stake in Tencent decreased to 22.74%, down 0.08 percentage points from the end of Q3.

Regarding the company's own repurchases, nearly HKD 20 billion was spent in Q4, a slight quarter-over-quarter decline. In terms of daily average repurchase volume, after resuming repurchases following the last earnings report and before this quiet period, the daily repurchase amount increased to around HKD 635 million, significantly higher than the previous HKD 550 million.

Given the recent significant stock price correction, even with a focus on capital allocation investments this year, the resumption of repurchases post-earnings report is expected to maintain high intensity in the short term.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reprinting requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report bears their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from using the data contained in this report. The information and data in this report are based on publicly available materials and are for reference purposes only. Dolphin Research strives but does not guarantee the reliability, accuracy, and completeness of the relevant information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be considered or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for or proposed for distribution to jurisdictions where distribution, publication, provision, or use of such information, tools, and materials conflicts with applicable laws or regulations, or where Dolphin Research and/or its subsidiaries or affiliated companies are required to comply with any registration or licensing requirements in such jurisdictions, or to citizens or residents of such jurisdictions.

This report only reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any way, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

WeChat Collaborates with Huawei/Honor/Xiaomi on A2A: Is This the Dawn of AI Integration?

-

![]()

NVIDIA RTX Spark: Powerful, Yet Not the Ideal Choice for the Agent Era

-

![]()

NVIDIA RTX Spark: Powerful, but Is It the Right Fit for the Age of Agents?

-

![]()

A Genuine Threat or Just a Publicity Stunt? World's Premier AI Firm Warns: AI Evolving Autonomously, Slipping Beyond Human Control

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital