Tencent and NetEase Music: Easy Profits Persist, Yet Platforms Are Not the Key Drivers

03/19 2026

03/19 2026

456

456

Is Listening to Music on Platforms Becoming a Niche Activity?

The capital markets have once again voiced their skepticism towards music platforms.

On March 17, Tencent Music unveiled its financial results for the fourth quarter and full fiscal year of 2025. The total revenue for 2025 soared to RMB 32.9 billion, marking a 15.8% year-on-year increase. Meanwhile, the adjusted net profit skyrocketed to RMB 9.92 billion, reflecting a significant 22.0% growth. Judging solely by these figures, it appears to be a resounding success.

However, following the announcement, Tencent Music's shares listed in the U.S. took a nosedive, plummeting 24.65% in a single day and closing at a mere $11.37. This drastic fall wiped out more than a quarter of its market value in one trading session, with trading volume surging to an astonishing 63.9 million shares—over eight times the average daily volume. The panic even spilled over to the Hong Kong stock market the next day, triggering similarly sharp fluctuations.

This was not an isolated incident. Just a month prior, on February 12, a similar scenario unfolded when NetEase Cloud Music released its earnings. The company's stock price tumbled 9.62% thereafter. Looking further back, both companies experienced comparable stock price collapses following the release of their Q3 2025 financial reports.

Curiously, despite rising revenues, increasing profits, and growing high-value membership income, the capital markets responded with stark indifference. The root of this contradiction lies in the persistent decline of monthly active users (MAUs).

The logic of capital is straightforward: users are the bedrock of a platform's value. When this foundation begins to crumble, even the most impressive financial metrics become mere castles built on sand. The market is not questioning Tencent Music's improved profitability but rather expressing deep skepticism about its future growth potential.

This skepticism is not confined to Tencent Music or NetEase Cloud Music; it extends to the entire online music industry.

01

Global Plateau and the End of the Old Logic

Tencent Music's financial reports over the past two years illustrate what can be described as "hollow growth."

In 2024, Tencent Music's quarterly net increase in paying users was 6.8 million, 3.5 million, 2 million, and 2 million, respectively, showing a gradual slowdown. This trend intensified in 2025, with the figures dropping to 1.9 million, 1.5 million, 1.3 million, and 1.7 million across the four quarters.

Meanwhile, the company's marketing expenditures continued to rise, increasing from approximately RMB 865 million in 2024 to RMB 941 million in 2025, an 8.8% year-on-year jump.

The growth rate of marketing expenses significantly outpaced that of free and paying users, indicating diminishing returns on marketing efforts. In essence, the company was investing heavily in promotion, but the market was not responding favorably.

This set of contradictory data points to a clear strategic shift: Unable to effectively acquire new users and even facing user attrition, Tencent Music Entertainment (TME) opted for an "inward-focused" approach. By optimizing membership benefits, introducing higher-priced subscription packages, and strengthening value-added services like long-form audio, it sought to extract more commercial value from its existing user base, particularly high-value paying users.

This is a classic "contraction strategy," shifting from pursuing broad coverage to deep mining. From a business perspective, this is understandable and an inevitable choice for mature companies. However, both users and capital markets have been unimpressed.

Wall Street investors are enamored with "growth" narratives, and user scale—especially MAUs—is the most intuitive metric for gauging a platform's future growth potential. A platform with shrinking MAUs, even if profitable in the short term, is seen as having reached its ceiling. The stock price collapse is a punishment for the collapse of this "growth story."

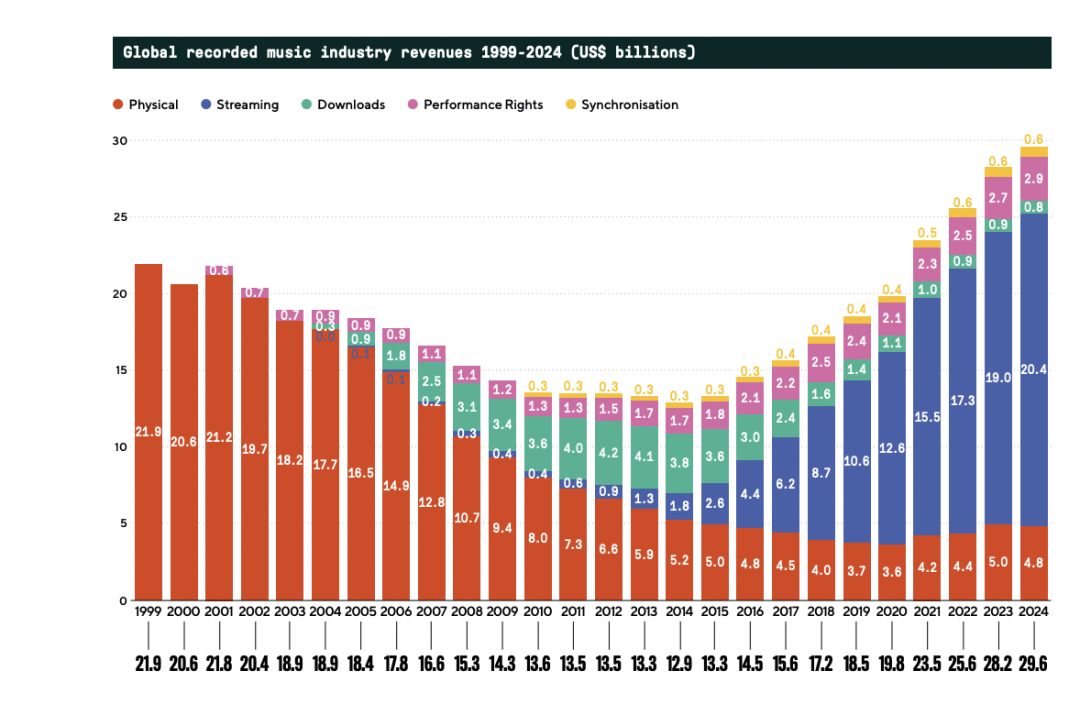

Tencent Music's predicament reflects the broader industry. According to the International Federation of the Phonographic Industry's (IFPI) latest Global Music Report 2025, while global streaming revenue surpassed $20 billion for the first time in 2024, reaching $20.4 billion and accounting for 69% of total global recorded music revenue, its 7.3% growth rate reveals signs of fatigue. In mature markets like North America and Europe, user growth has nearly stalled.

This means the golden age of growth driven solely by "membership subscriptions" has ended. Platforms must now answer a critical question: When user inflows cease, where will new revenue come from?

Tencent Music's answer is to transform itself into a comprehensive entertainment platform that transcends being merely a "music-listening tool." However, this narrative has clearly failed to convince everyone.

02

When "Jay Chou" Is No Longer a Universal Cure

There was a time when the competitive logic of music platforms revolved almost entirely around an "arms race" for top-tier artist copyrights. Whoever secured superstars like Jay Chou held the key to social media traffic and user growth engines.

Tencent Music was the biggest winner in this race. By signing exclusive licensing deals with Universal, Sony, Warner Music, and numerous Chinese labels, TME once built an impenetrable copyright moat. This strategy proved highly effective in the early stages, helping it rapidly accumulate a massive user base and establish market dominance.

However, this "universal cure" is gradually losing its potency.

On one hand, regulatory intervention has broken the monopoly on exclusive copyrights. Under antitrust pressure, major platforms have been forced to open their music libraries to competitors, significantly eroding the advantage of exclusive content. Today, the overlap of songs available on TME and NetEase Cloud Music is increasing, and the era of "I have what you don't" is over.

On the other hand, astronomical licensing fees have become a heavy burden on platforms. As the user growth dividend disappears, high copyright costs directly erode profit margins, making the "burn money for market share" model unsustainable. The relationship between platforms and upstream record labels has also shifted from early win-win cooperation to a tense, game-theory-filled dynamic.

For today's Gen Z and even younger demographics, the primary way they encounter new music is through background audio in short videos or various types of video content, where music serves primarily as an emotional and atmospheric enhancer. Meanwhile, the near-depletion of Chinese pop music superstars has accelerated platform transitions.

The value of platforms no longer lies in "music" itself but in the "added value" it provides. The rise of Qishui Music (a rival platform) is precisely because it accurately captured the significant changes brought about by generational shifts in listener preferences, aligning with new market demands not as a pure music platform but in a different capacity.

This is the fundamental reason Tencent Music and NetEase Cloud Music are heading down different paths. After the dust settles from the copyright wars, the core of this duel is no longer "what songs I have that you don't" but "what unique experiences I can offer you."

With copyright homogenization becoming the norm, TME and NetEase Cloud Music have each adopted their own solutions, reflecting two distinct product philosophies: a top-down "ecosystem empire" versus a bottom-up "community tribe."

Tencent Music has chosen a "heavier" path—building a pan-entertainment ecosystem centered on music but extending into social networking, live streaming, performances, and more.

Open QQ Music or Kugou Music, and you'll find that "music listening" is just one part of the experience.

TME's heavily promoted social entertainment business, such as WeSing (a karaoke app), was once a cash cow for the group. TME Live, its online concert platform, became a vital bridge connecting artists and fans during special periods. Additionally, long-form audio, podcasts, and musician support programs—TME aims to encompass all user needs related to sound within its ecosystem.

The advantage of this model is that it provides diversified monetization channels. When music subscription revenue growth falters, income from live streaming tips, virtual gifts, and paid concerts can serve as robust supplements. The rising ARPPU (Average Revenue Per Paying User) in financial reports largely stems from this "multi-pronged" business model.

However, the drawbacks of a "heavy ecosystem" are also evident. Bloated functional modules may undermine the purity of the core music-listening experience, while excessive commercialization can alienate users. More importantly, it ties the company's fate to the broader entertainment industry's prosperity, especially as live streaming faces heightened regulation and fierce competition, amplifying risks.

In contrast, NetEase Cloud Music has chosen a "lighter" path—deepening its focus on the "music community."

From its inception, the "Cloud Village" label has been deeply ingrained in NetEase Cloud Music's DNA. Emotional resonance in the comments section, precise personalized recommendation algorithms, the surprise of "Daily Recommendations," and a unique community atmosphere collectively form its core competitive moat. Here, music is not just a consumer good but also social currency and an emotional carrier.

This "small but beautiful" community model fosters extremely high user stickiness and engagement. NetEase Cloud users are more willing to pay for nostalgia and a sense of belonging. This is why, despite relatively weaker copyright holdings, NetEase Cloud Music has maintained a loyal core user base.

However, the Achilles' heel of a "light community" is its fragile monetization capability. How to translate community atmosphere and user emotions into sustainable commercial revenue remains an unsolved challenge for NetEase Cloud Music. Whether through live streaming, social features, or membership subscriptions, the company treads carefully, fearful of disrupting its hard-won community tone. The post-earnings stock price plunge also reflects capital market concerns about its single-dimensional business model and monetization limitations.

At this point, the strengths and weaknesses of both paths are clear. Tencent Music has earned more money through its "ecosystem," but the platform's identity as a "music player" has been diluted. NetEase Cloud Music has preserved its "community" heart but struggles commercially.

This clash between ecosystem and community essentially asks: Should the music platform of the future be an "entertainment consumption venue" or an "emotional exchange space"? Based on current market reactions, neither answer seems capable of sustaining the high-growth valuation models of the past.

03

Is AI a New Variable or a Gravedigger?

While the two major music platforms grapple with business model dilemmas, a more powerful variable has quietly entered the fray. AI is reshaping the underlying logic of the entire music industry in a fundamental way.

AI initially intervened in the "distribution" link of music.

Represented by Spotify's AI DJ and TME's "Smart Recommendations," algorithms have long become the primary way users discover music. An AI application that can instantly perceive your emotions and environment to generate a unique background music track holds immense appeal for young people seeking personalization.

In this scenario, traditional concepts of "songs" and "playlists" will be deconstructed, and music consumption will transform into a highly personalized, on-demand "ambient service." A platform's core competitiveness will shift from the size of its music library to the sophistication of its AI models and contextual service capabilities.

Even more disruptive is AI's encroachment into the "creation" link of music.

The emergence of AI music generation tools like Suno and Udio has lowered the barrier for ordinary people to write and compose songs to near zero. Simply input a text prompt, and AI can generate a complete, decent-quality song in a short time.

This has two profound implications: First, the supply of music content will explode exponentially. When millions of UGC (user-generated content) or even AIGC (AI-generated content) flood platforms, existing copyright systems, recommendation algorithms, and distribution logics will face severe challenges. Screening, reviewing, and recommending vast amounts of content will become platforms' primary dilemma.

Second, the music value system will be reconstructed. When "creation" itself becomes cheap or even free, what defines good music? Who decides? How should royalties be distributed? These questions fundamentally challenge the existing music industrial system. For streaming platforms heavily reliant on copyright licensing models, this amounts to a seismic revolution.

In this AI-driven paradigm shift, the role of music platforms will be redefined. They may no longer be mere copyright distributors but transform into providers of AI creation tools, originators of massive AIGC content, and incubators of new music experiences.

This may explain why Tencent Music is desperately trying to shed its "player" label.

Because it knows that in a future where AI can infinitely generate music, a platform offering only "playback" functionality will see its value infinitely diluted. Money can still be made, but only by providing "new services" for the AI era—whether smarter recommendations, more immersive experiences, or more powerful creation tools.

What Tencent Music is experiencing may not just be a capital market revaluation but a clear signal of an era's transition.

The age of achieving effortless success by capitalizing on demographic dividends and copyright monopolies has come to an end. Both Tencent Music's strategic breakthrough in leveraging its "ecosystem" and NetEase Cloud Music's steadfast (persistent) commitment to its "community" approach signify arduous explorations undertaken after the collapse of traditional models. Although they continue to turn a profit, the engines of growth have transitioned from platform-driven user acquisition to extracting multi-dimensional value from existing users and expanding ecosystem services.

However, AI is fundamentally transforming the entire landscape of music production, distribution, and consumption, thereby posing a significant threat of disruption to all established business models.

For Tencent Music and its counterparts, maintaining current profitability is important, but the paramount existential challenge lies in securing their position in the new world shaped by AI. While future profits will undoubtedly persist, they will accrue to those who can effectively harness emerging technologies and craft innovative experiences—rather than simply to the platform boasting the largest song library.

- END -

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan