Is MiniMax Worth 330 Billion?

03/26 2026

03/26 2026

523

523

Author / Liang Tian

Source / Node AI

Less than three months after going public, MiniMax's market capitalization has surpassed HK$330 billion, overtaking the long-established internet company Baidu.

The mainstream feedback has been nearly unanimous, with some media outlets hailing it as a shift in power and wealth, and others predicting the advent of the third reshuffling period in the internet sector.

The narrative of a fledgling tech upstart outperforming established giants is indeed a crowd-pleaser, but market capitalization primarily reflects current market sentiment. The long-term valuation ceiling hinges on two questions: Is MiniMax's technology irreplaceable, and has its business model proven viable? After all, the upcoming large model competition will be a hardcore showdown among the players at the table.

So, can Minimax justify this figure?

How Did the Financial Report Improve?

The OpenClaw trend has spurred a wave of API enthusiasm (hereinafter referred to as the "lobster economy"). Coinciding with the release of M2.5 and M2.7, MiniMax seized the opportunity, and its market capitalization soared. However, to analyze the company itself, we must first examine its financial report.

Let's start with the overall performance.

In 2025, MiniMax reported revenue of $79.038 million, up 158.9% year-on-year, with overseas revenue accounting for over 70%. This growth rate is impressive enough to sustain market optimism about commercialization and internationalization.

However, upon closer inspection, it's not flawless.

Fourth-quarter revenue was approximately $26 million, with the year-on-year growth rate dropping from 175% in the first three quarters to 130%, indicating a slowdown in growth.

The revenue structure is particularly noteworthy, with accelerated B-side growth being the biggest highlight.

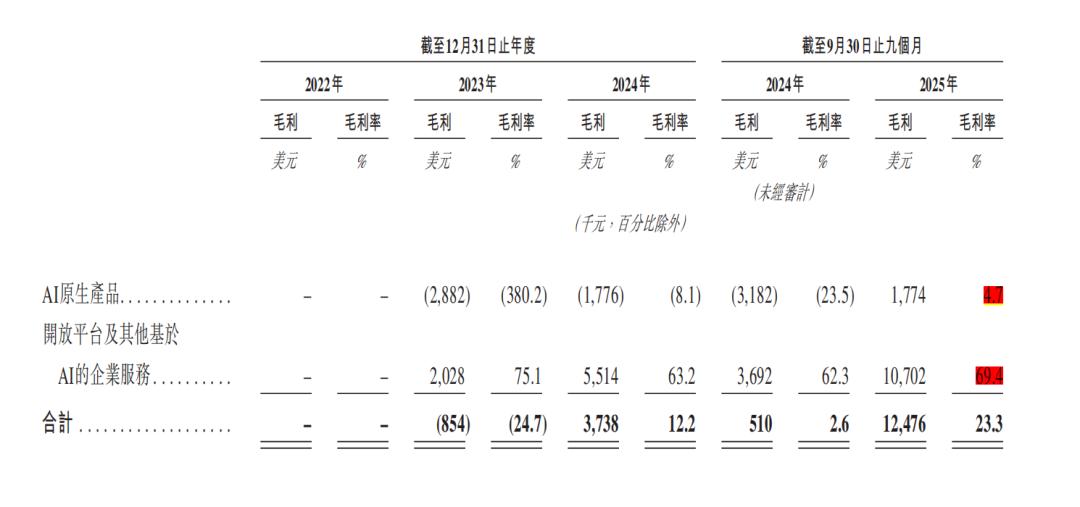

MiniMax is one of the few Chinese large model companies that has achieved success in both C-side and B-side markets, with the B-side business showing strengthening momentum. In the fourth quarter of 2025, 2B revenue (i.e., API income) surged from $4.83 million to $31.86 million, a 6.6-fold increase, with its share of total revenue rising from 15.8% to 40.3%. Given the current release status of M2.5 and M2.7, this revenue is expected to continue climbing in the first half of 2026.

The expansion of 2B operations also drove the overall gross margin up from 12.2% in the first three quarters to 25.4% for the full year. However, compared to the API's gross margin of 69.4%, the overall margin is still significantly dragged down by the C-side—the prospectus shows that 2C gross margin was -380.2% in 2023 and only turned positive to 4.7% in the same period of 2025.

Now, let's look at the expense structure.

Research and development expenses were $253 million, up 33.8% year-on-year, obvious (This Chinese character seems out of place; assuming it's a typo and removing it) lower than the revenue growth rate; marketing expenses fell 40.3% year-on-year to $51.9 million, with the sales expense-to-revenue ratio dropping from 285% to 65.7%. This indicates that MiniMax has shifted from a "burn money for scale" approach to a model emphasizing efficiency and quality.

However, the optimization of gross margin and expense structure has not translated into profitability.

Data shows that MiniMax reported a net loss of $1.872 billion for the full year of 2025, including a $1.6 billion paper loss from the conversion of convertible debt into equity. Excluding this factor, the adjusted net loss was $251 million, up slightly by 2.7% year-on-year, but at least the losses did not spiral out of control with scale expansion.

2B Leads the Profitability Charge

Many might think that since the 2C side is so costly, focusing on 2B would suffice. However, MiniMax's platform-style operation determines the true nature of its business model: The C-side serves as a data collection tool, and using this data to optimize the 2B business forms the profit point.

This is not surprising, as data is currently one of the main moats for large models. Yan Junjie also explicitly mentioned at the earnings call that the iteration of the dialogue model M2-her benefited from the massive interactions on Xingye and Talkie, while the refinement of the video model relied on the 600 million videos generated by Hailuo AI.

The question is, can this logic of collecting data on the C-side and monetizing optimized capabilities on the B-side form a long-term closed loop?

In the view of Node AI, its validity hinges on two premises: First, C-side interactions can truly be continuously converted into model and product advantages; second, B-side clients are willing to pay for these advantages long-term. If either link loosens, the closed loop becomes fragile.

However, MiniMax's C-side business is not without risks.

In September 2025, Disney and other Hollywood studios sued MiniMax in California, alleging infringement issues during model training, content generation, and promotion stages by its Hailuo AI. Although the company rebutted the compensation scale and legal applicability in its prospectus, the case itself highlights that copyright and data compliance are becoming crucial variables in overseas business expansion.

Thus, the improvement in MiniMax's fundamentals represents a structural repair.

Agent Capabilities Improve, Hallucinations Finally Decrease

After discussing the 2C side, let's turn to the 2B side, which is the main factor supporting MiniMax's high market capitalization today.

The lobster economy trend has enriched a wave of Chinese model factories. Less than a month after the release of Kimi's K2.5 model, its cumulative revenue exceeded the total revenue for all of 2025; MiniMax's M2 series model saw its average daily token consumption in February this year grow more than sixfold compared to December last year, with token consumption from the coding plan surging over tenfold. ARR reached $150 million in February, up 46% from the Q4 2025 average based on the latest monthly revenue.

Product quality is paramount. Let's start with M2.5. While it doesn't hold an absolute technological lead, its most competitive aspect is its lower cost.

According to public information, at an output speed of 100 tokens per second, the cost of continuous operation for one hour is about $1; at 50 tokens per second, it's only around $0.3. Notion's co-founder, Akshay Kothari, announced that Notion Custom Agents has introduced the open-source weighted model MiniMax M2.5 and made it available to users as an experimental feature. This precisely demonstrates that MiniMax is entering the market with high cost-effectiveness for a large number of low-to-medium complexity tasks.

We're not interested in the one-sided hype from marketing accounts. Looking at third-party evaluations from Artificial Analysis, M2.5's agent capabilities have indeed significantly improved compared to M2.1, but this seems more like a trade-off—M2.5's hallucination rate worsened from 67% to 88%.

On the bright side, after a month of iteration, the newly released M2.7 has a hallucination rate of only 34%, down by 54%.

However, M2.7 still exhibits some instability in complex reasoning and long-process stability, issues that may not be apparent in a single conversation but can be amplified when placed in an Agent framework that runs for extended periods.

For enterprise clients, a model being "cheap enough" is one thing, but being "stable enough" is another. Especially when Agents enter scenarios like office work, processes, and knowledge handling, instability can lead to process errors.

MiniMax's current reality is clear: Its strengths are evident—improved fundamentals, the B-side starting to shoulder profits, the model making rapid progress in the Agent direction, and strong cost advantages.

But the challenges are also significant.

The Agent track is highly crowded: Competitors include domestic players like Zhipu, Kimi, DeepSeek, Alibaba, and ByteDance, as well as overseas giants like OpenAI, Anthropic, and Google.

Keep in mind that in March this year, overseas media reported that Anthropic achieved an annualized revenue of $19 billion thanks to its strong programming capabilities. The programming scenario offers high willingness to pay but also low tolerance for errors, ensuring that head (Assuming " head " means "top players" and translating accordingly) players dominate while others scramble for scraps.

We're not saying that model factories following the lobster trend should be denied; rather, we're raising a very real question: How long can this lobster-driven wealth last? It's a question worth pondering.

While API services can generate cash flow, the underlying infrastructure expenses are a fixed burden. To attract more consumers, major model and cloud providers are likely to engage in price wars, which is not a positive signal for profit margins, especially since model providers are not yet profitable.

MiniMax's next major test is how to enhance its comprehensive engineering capabilities amid slowing marginal improvements in model performance, competing with powerful model providers and tech giants at the table.

Of course, this isn't just MiniMax's dilemma but a question every model provider must consider.

Thus, the $330 billion market capitalization isn't about how much MiniMax is earning now but a bet on whether it can become one of the few platform-type companies remaining at the center of the table in the future.

This valuation clearly factors in significant expectations in advance.

If the answers to these questions gradually become "yes," today's valuation may not be exaggerated; however, if any key link fails, this round of revaluation could merely be an amplification of phased (translating " phased " as " phased " (phased/stage-based) emotion.

Today, what MiniMax deserves credit for is that it's still riding the wave. But the high valuations in the capital market are a bet on "being the last one standing." Looking ahead, the war in the Agent era has only just begun.

*The featured image was generated by AI.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?