Can Kuaishou Sustain AI-Driven Growth Momentum with Kling’s Rise and Legacy Business Stabilization?

03/26 2026

03/26 2026

439

439

Kuaishou released its fourth-quarter results after the Hong Kong market closed on March 25 (Beijing Time). The results slightly surpassed expectations, highlighted by steady revenue growth and internal efficiency improvements that fueled profit expansion. However, among its various business segments, Kling—a key driver of valuation upside—fell short of the optimistic forecasts set by analysts at the beginning of the year. Coupled with intensifying industry competition, this has contributed to the stock price correction since February.

Nevertheless, insights from the company’s earnings call suggest that Kling’s performance was not as weak as it appeared, and the outlook remains promising. Conversely, traditional businesses are expected to face significant pressure due to policy shifts, competitive pressures, and the recognition of AI investment costs.

The current market valuation already reflects some of these negative factors. While our analysis indicates that Kling’s implied valuation is still not fully reflected in the stock price (especially amid the ongoing boom in large language models), some investors remain cautious due to the drag from legacy operations. Whether Kuaishou can achieve further revaluation in the near term hinges on Kling’s ability to deliver more surprises.

Let’s examine the key points in detail:

1. Can operational efficiency improvements continue this year?

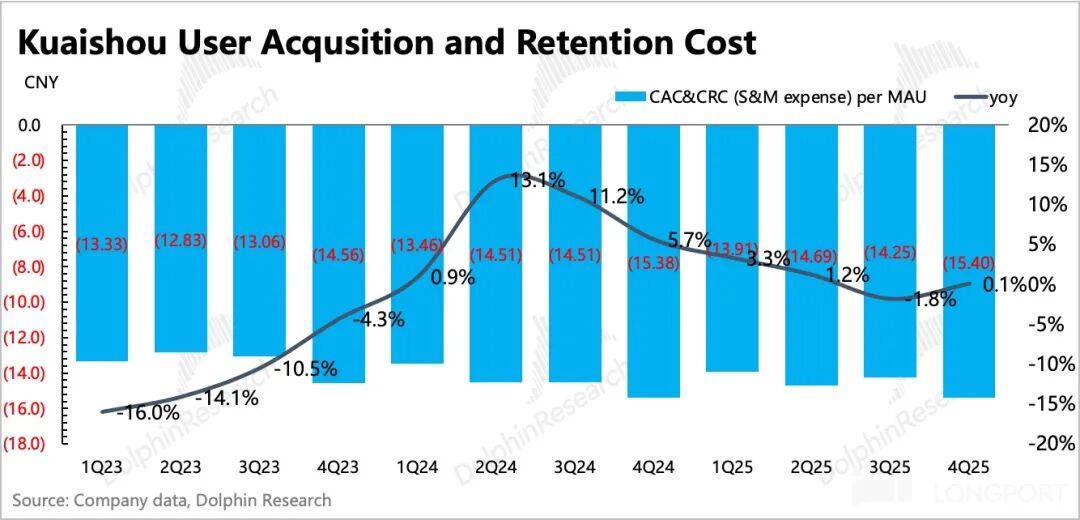

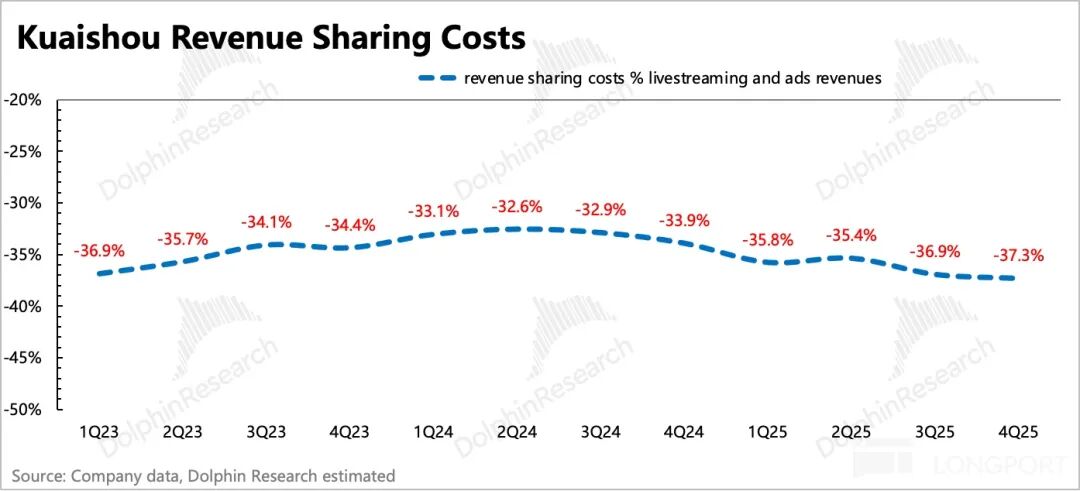

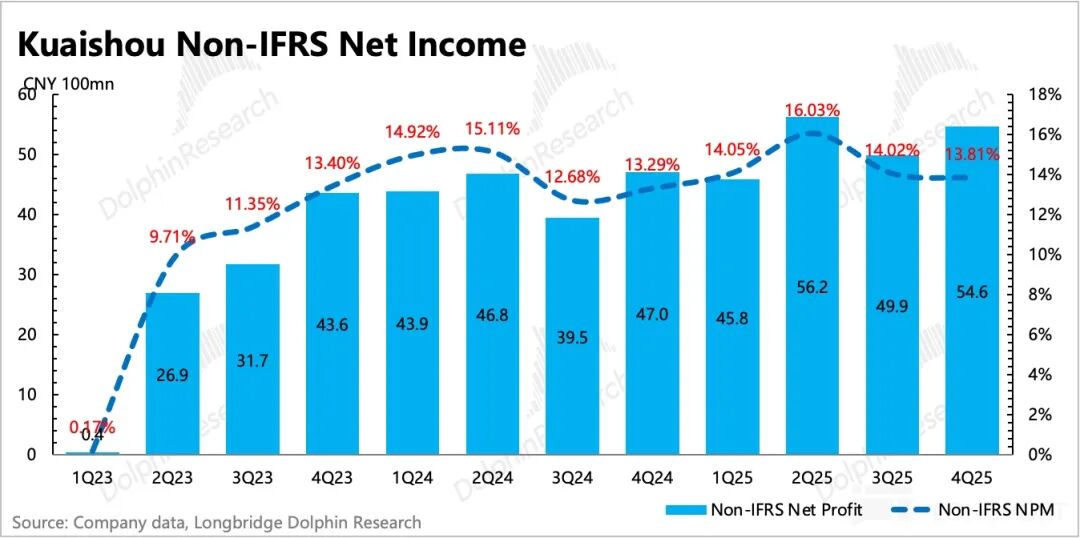

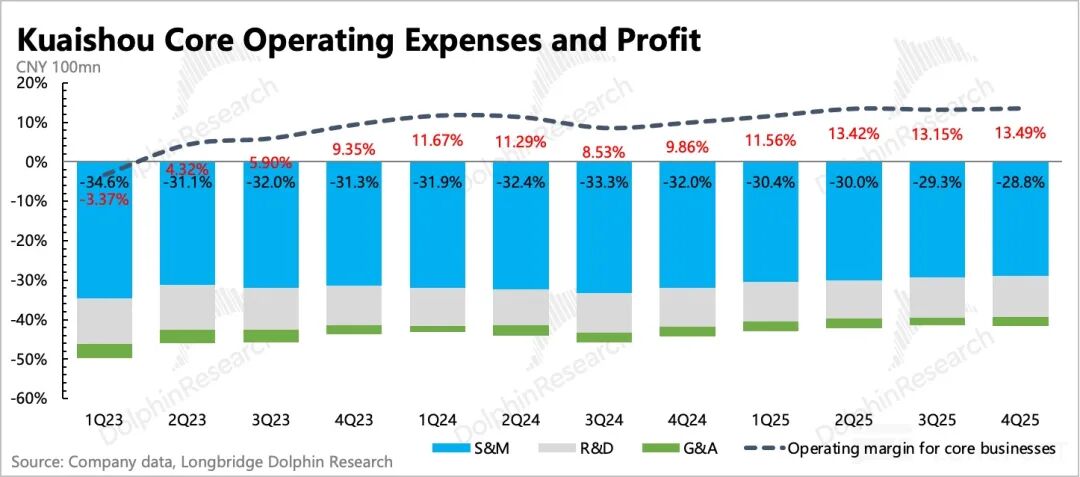

Despite rising AI investment costs (equipment depreciation increased by 10% year-over-year, and R&D expenses surged by 34% year-over-year), Kuaishou has managed to control core operational expenses. For instance, overall employee expenses rose by just 4%, while marketing expenses remained flat year-over-year. As a result, the core operating profit margin reached 13.5%, up 3.5 percentage points year-over-year and slightly higher by 0.4 percentage points quarter-over-quarter.

Looking ahead, as more AI-driven revenue is recognized, the impact of AI investments on profits is expected to intensify (the company warned that this would erode profit margins this year). Whether investors will tolerate this weakening of operating leverage (i.e., maintain valuation multiples) depends on whether it translates into higher business growth or growth potential. Can traditional businesses reverse their natural slowdown and rebound? Or can Kling withstand competition and industry shifts to sustain high quarterly growth?

2. Kling fell short of expectations this time, but guidance remains optimistic

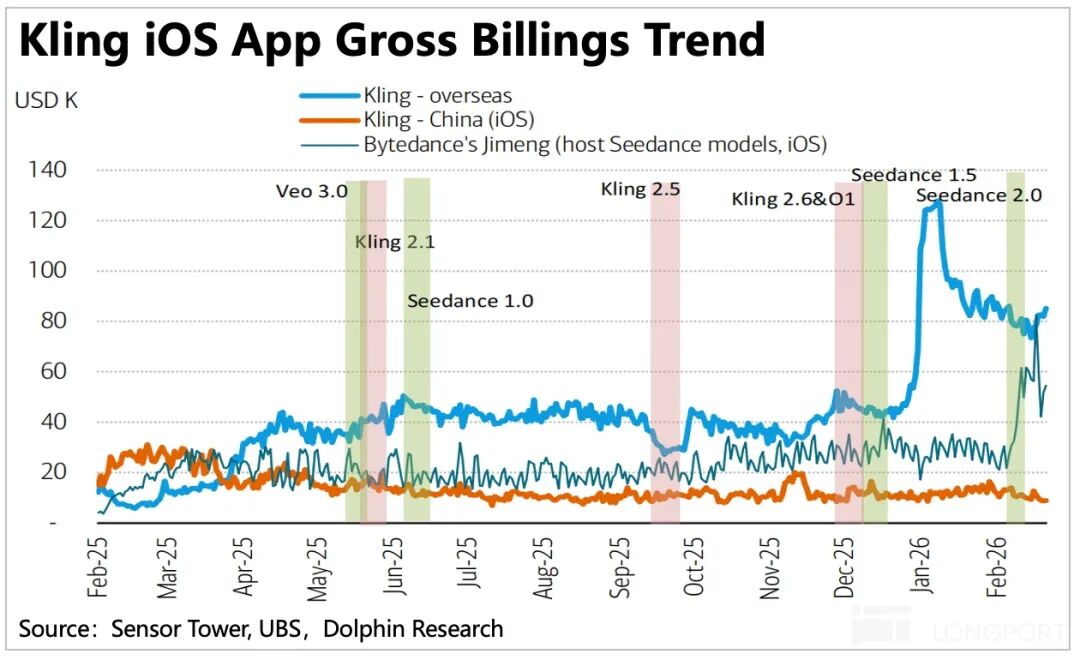

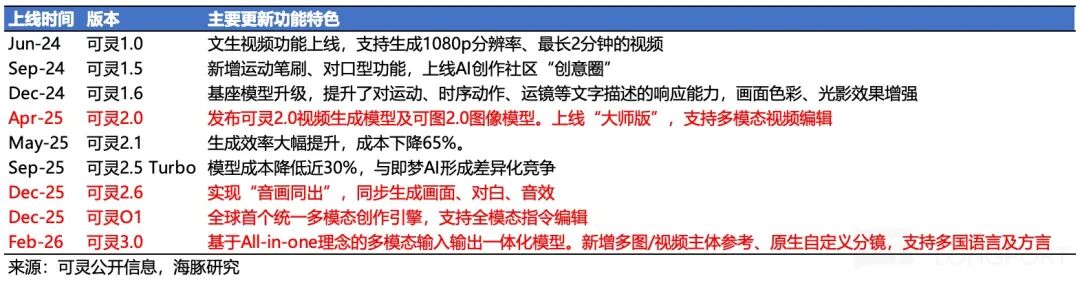

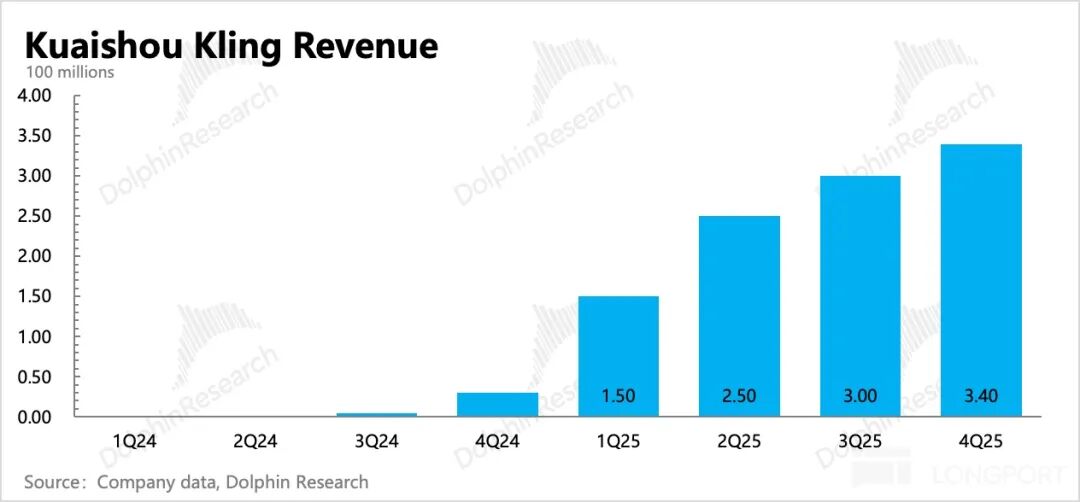

The December launch of Kling version 2.6 received positive user feedback, thanks to new features like motion control and synchronized audio-visual output, driving monthly revenue to a record high of $20 million. As a result, analysts raised their Q4 revenue expectations from the initial guidance range of RMB 300 million to RMB 350–400 million, with full-year 2026 projections nearing RMB 2 billion—representing nearly double growth.

Actual Q4 revenue came in at RMB 340 million, at the lower end of guidance and market expectations. Typically, companies communicate with analysts during previews, and after a spike in December followed by a sharp decline in January (on the iOS side), February saw the release of Kling 3.0. However, the popularity of Seedance 2.0 also impacted Kling’s revenue rebound, likely prompting analysts to lower their expectations and suppressing Kuaishou’s stock price performance since February.

During the earnings call, the company revealed that the January 2024 ARR update (exceeding $300 million, up 25% month-over-month from December 2023) indicates that Kling’s revenue is stronger than external data suggests.

Dolphin Research believes this discrepancy may stem from third-party data tracking only the iOS app side. In reality, as a productivity-focused platform, Kling’s more impressive B-side revenue (accounting for an increasing share quarter-over-quarter, reaching 40% in Q3) is likely generated primarily on the PC side—a segment missing from third-party data.

3. Stable e-commerce growth

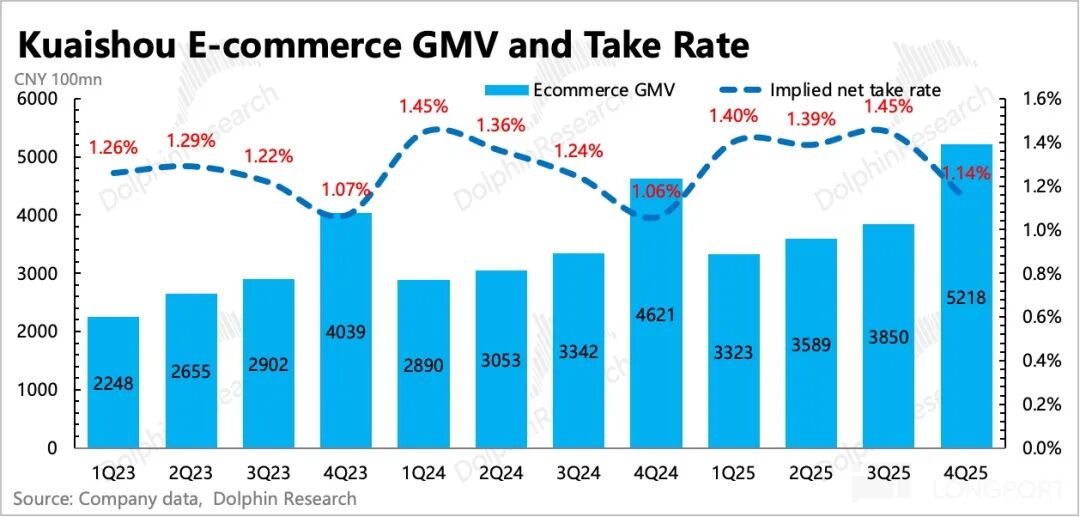

Q4 e-commerce GMV grew by 13%, slightly slower than the previous quarter, with annual transaction volume nearing RMB 1.6 trillion. Under initiatives like Expert Product Selection and Distribution (influencer-driven product curation), full-hosting (full-service management), and Hyperlink services (super link services), the overall e-commerce commission monetization rate improved by 8 basis points year-over-year (though it declined quarter-over-quarter due to increased peak-season commission rebates). Consequently, e-commerce revenue grew nearly 22% year-over-year, slightly exceeding top-tier analyst expectations (18% YoY).

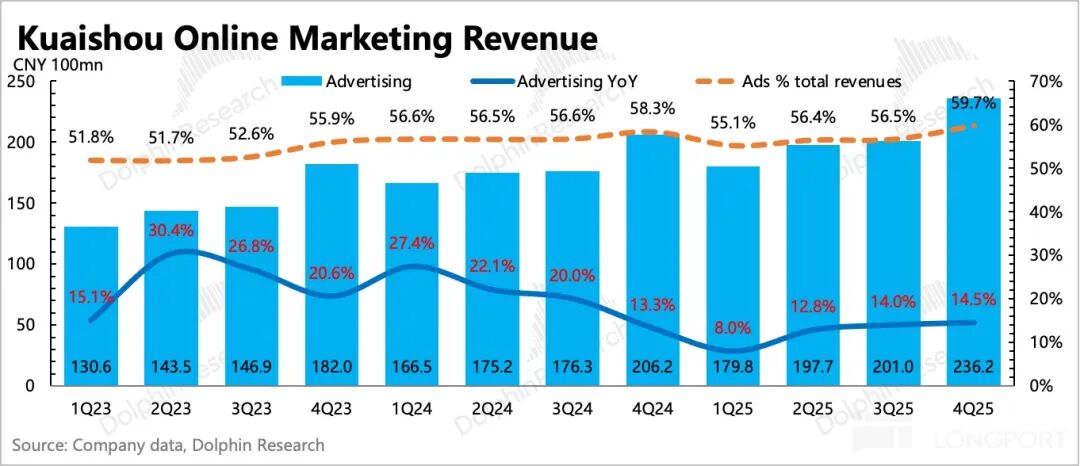

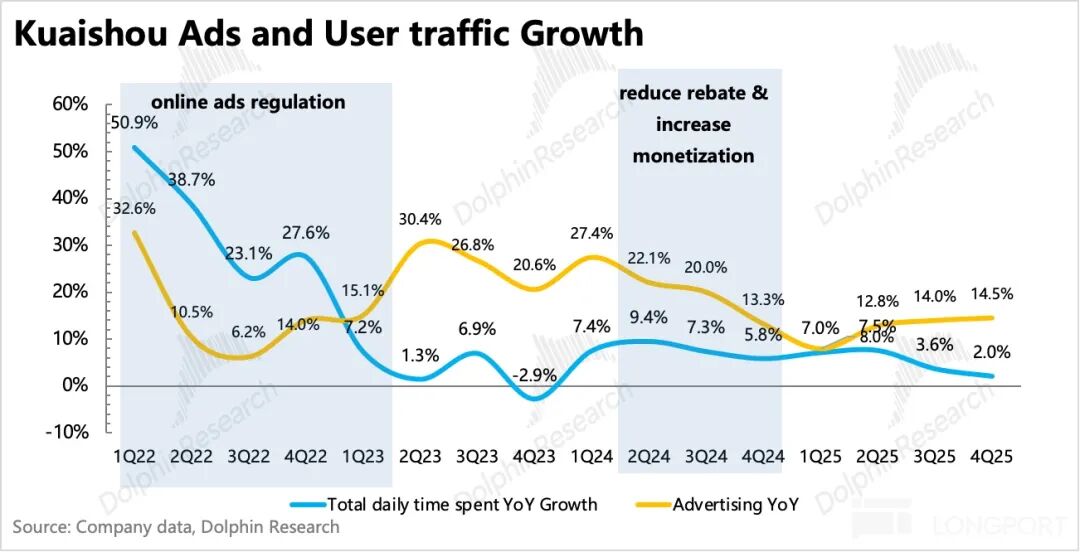

4. Advertising slightly outperformed expectations, with attention on the ‘investment tax’ impact

Q4 marketing ad revenue grew by 15%, continuing its recovery from Q3 and slightly surpassing market expectations. Concerns about the broader consumption environment, peer competition, and the ‘investment tax’ may have led to relatively low expectations for ad growth. However, whether the ‘investment tax’ will further expand its impact in 2026 remains uncertain, and we recommend monitoring management’s comments during the earnings call.

Growth was primarily driven by a low base last year, stable e-commerce expansion, sustained popularity of short dramas (including AI-generated comics) and casual games, and incremental contributions from the recommendation large model OneRec, UAX fully automated ad placement (reaching 80% penetration in external ad spend, up 10 percentage points quarter-over-quarter), and AIGC ad marketing tools.

5. Live streaming faced expected pressure

Q4 live streaming payers declined by 2%, remaining relatively weak due to industry contraction trends and the company’s own adjustments for a healthier ecosystem. We expect this pressure to persist.

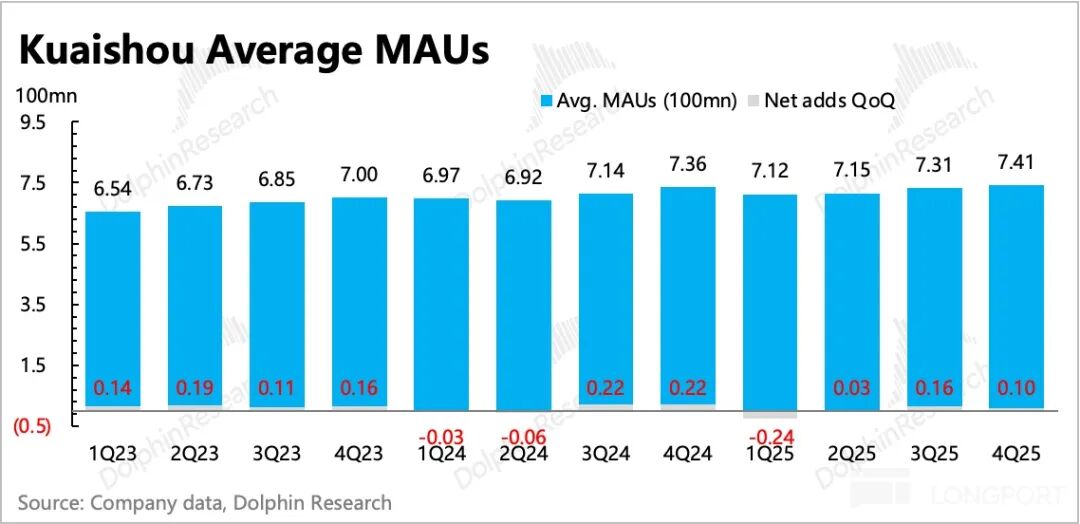

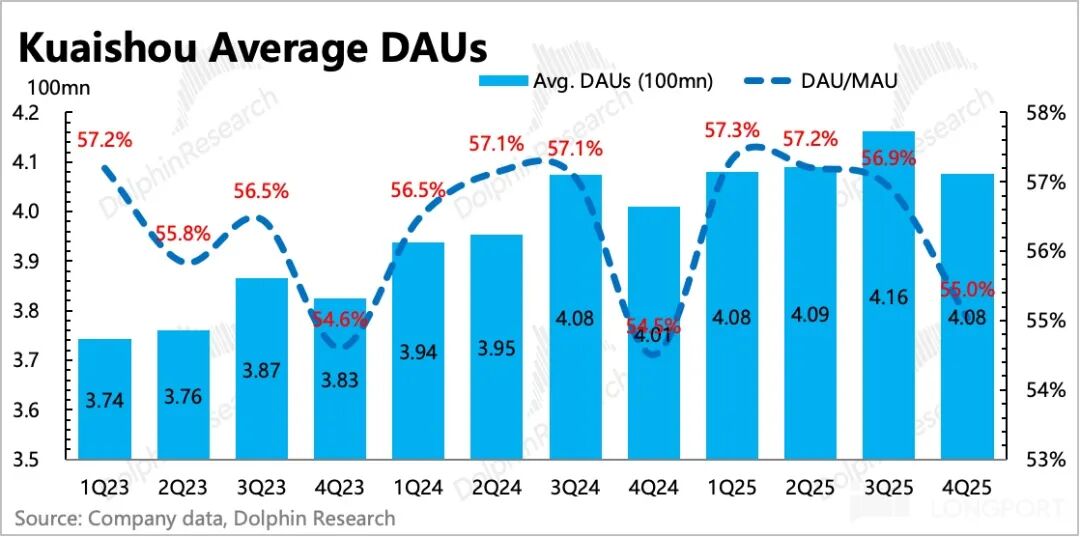

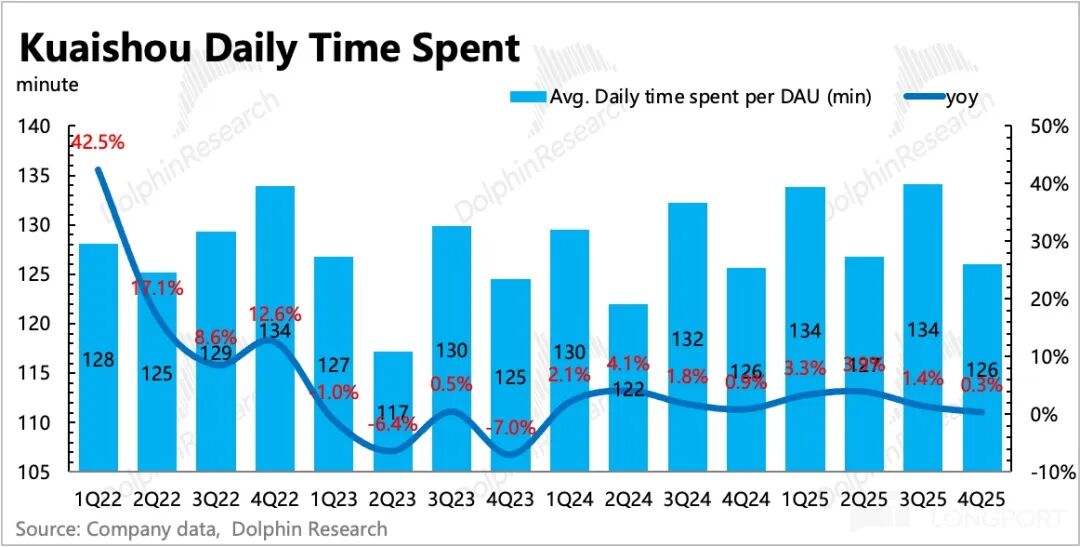

6. Stable user ecosystem

The platform is now mature, with user metrics largely stable. Monthly active users (MAUs) reached 740 million, while daily active users (DAUs) stood at 410 million, representing low single-digit year-over-year growth. Engagement remained at 55%, and user time spent was flat year-over-year.

7. Potential improvements in shareholder returns

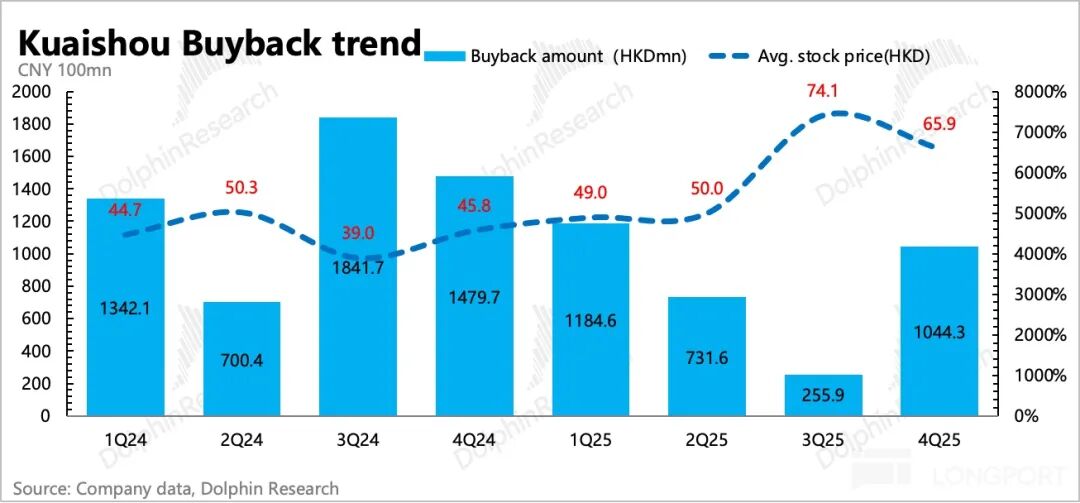

Following the Q4 stock price correction, the company increased its share buybacks, repurchasing HKD 3.2 billion worth of shares for the full year while announcing HKD 3 billion in dividends—totaling a 2.7% shareholder return. With ample cash on hand and recent stock price pressure, Dolphin Research speculates that the company may continue aggressive buybacks after the blackout period, depending on management’s comments during the earnings call.

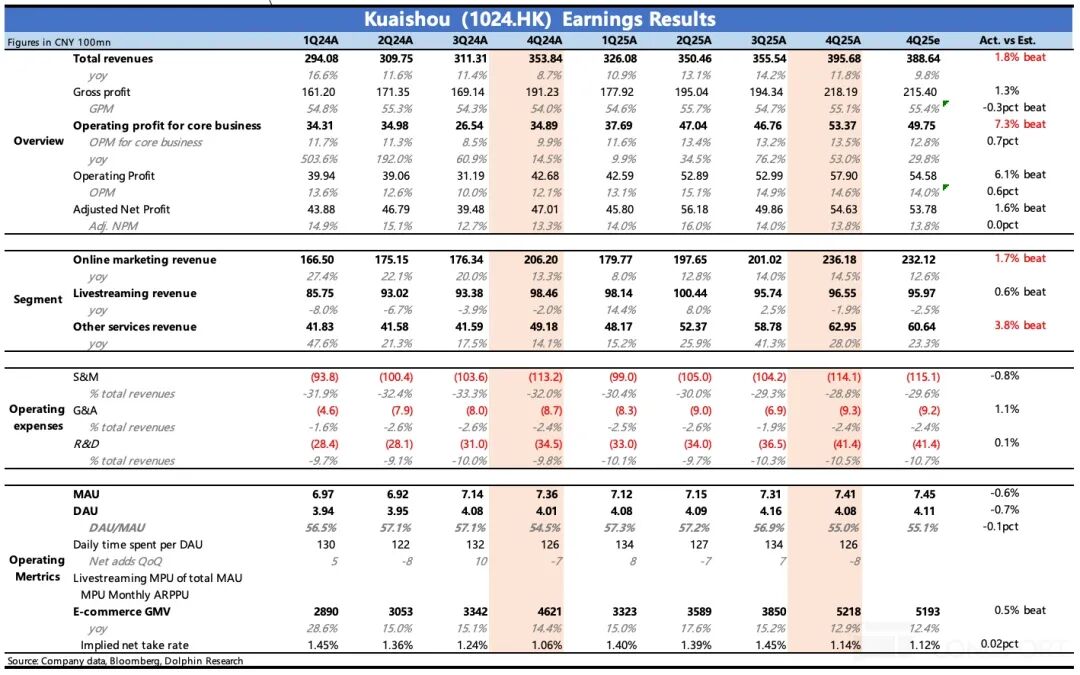

8. Detailed financial data overview

Dolphin Research’s View

Q4 results were solid, especially given the current valuation level of approximately 9x P/E, implying that market expectations have already adjusted downward and become more conservative.

However, market concerns are not entirely unfounded—user growth is nearing stagnation, and traditional businesses lack ‘extra’ support amid policy challenges (investment tax & weak physical consumption) and peer competition. Thus, Kuaishou’s growth hopes largely rest on AI, including advertising, ToC AI-generated comics, ToB AI digital marketing, AIGC solutions, and the key business ‘Kling.’

AI’s role in advertising is primarily to slow the deceleration of revenue growth, while Kling represents entirely new business growth and is the true catalyst that has caught investors’ attention. Since Kling’s revenue surge in Q2 last year, investors quickly revalued Kuaishou—mostly assigning a 35x P/S valuation based on high-growth expectations.

Kling’s high valuation expectations also mean that short-term revenue fluctuations have a significant impact on Kuaishou’s overall valuation. For example, ARR revenue of $150 million versus $300 million can cause nearly HKD 35 billion in valuation fluctuations (equivalent to 15% of the current market cap). Given that investors’ optimistic expectations for Kling’s future revenue were even higher last year, the impact on valuation fluctuations is even greater.

Currently, market expectations for 2026 performance are generally more optimistic than the company’s internal guidance. Despite management’s tendency to be ‘conservative,’ the significant gap still requires downward adjustments:

1) Traditional business growth is expected to slow to just 5%, compared to 11.7% growth this year. We believe this accounts for continued pressure on live streaming rewards and the impact of the investment tax and competition on advertising and e-commerce.

2) Benefiting from the launch of standout features in the December 2.6 version and February 3.0 version, the company disclosed during the earnings call that Kling’s January 2024 ARR exceeded $300 million and guided for at least double-digit growth in 2026 (i.e., over RMB 2.1 billion), higher than market expectations (+85% YoY). Market references to iOS revenue trends overlook the increasingly significant but hard-to-track B-side PC performance.

On the profit side, we make further adjustments considering the impact of AI investments on profit margins: We assume AI investments will reduce gross margins by 2 percentage points (RMB 26 billion in capital expenditures, depreciated over 5 years, impacting 3–4 percentage points, offsetting the trend-based optimization of 1–2 percentage points), while R&D expenses increase by 1 percentage point due to AI expansion. At the current market cap of $30 billion, the traditional business is expected to trade at an adjusted PE of 11x, within the valuation range of traditional e-commerce and social platforms among Chinese assets.

In other words, the current market cap has hardly fully priced in Kling’s valuation. A more detailed valuation analysis has been published in the Longbridge App under the 「Dynamic - Depth (Investment Research)」 section in an article with the same title.

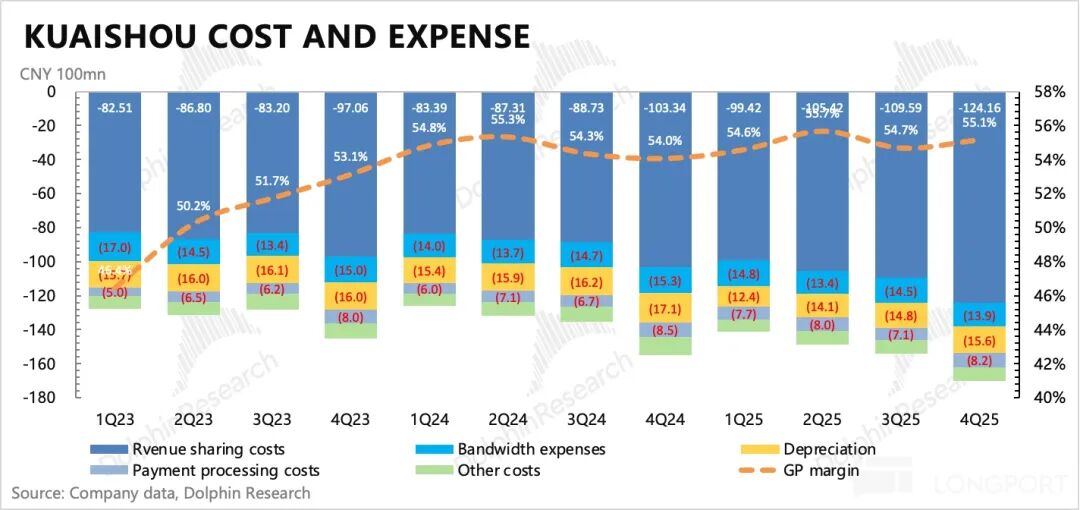

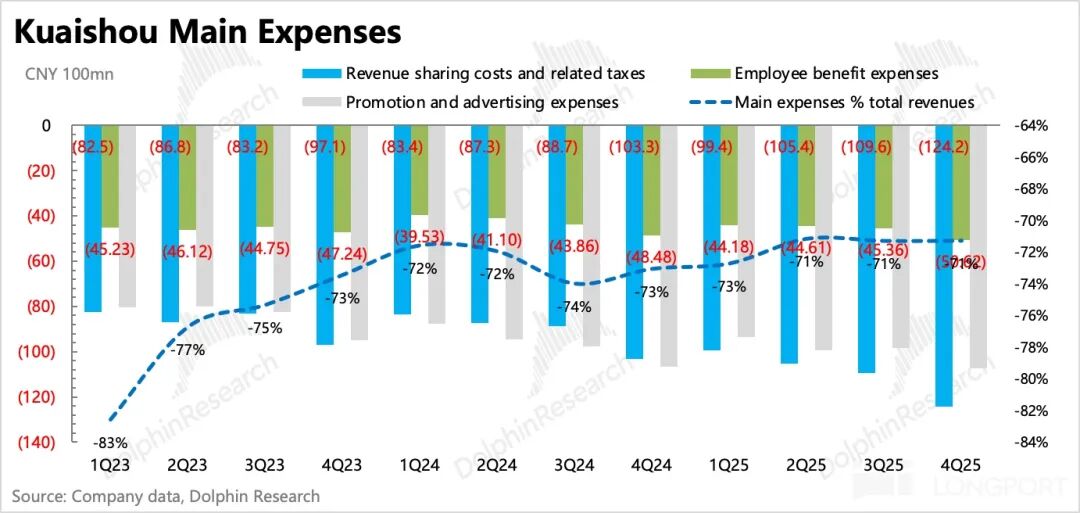

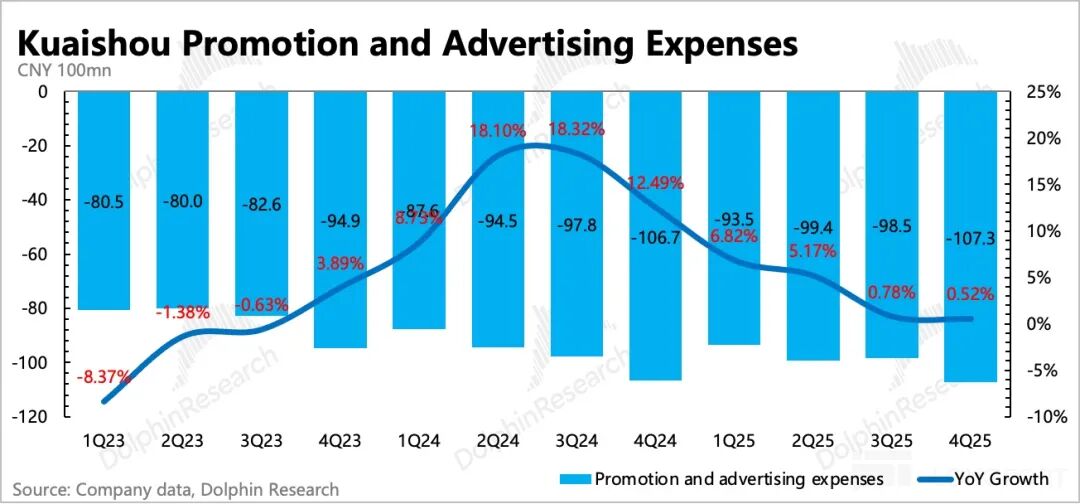

Below are detailed charts:

produce, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner whatsoever, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized individuals. Dolphin Research reserves all related rights.</p></div>

<!-- <p><span style=)

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?