Anthropic Comes to the Rescue: Is It Amazon's Turn to Shine Among the MAG7?

05/07 2026

05/07 2026

453

453

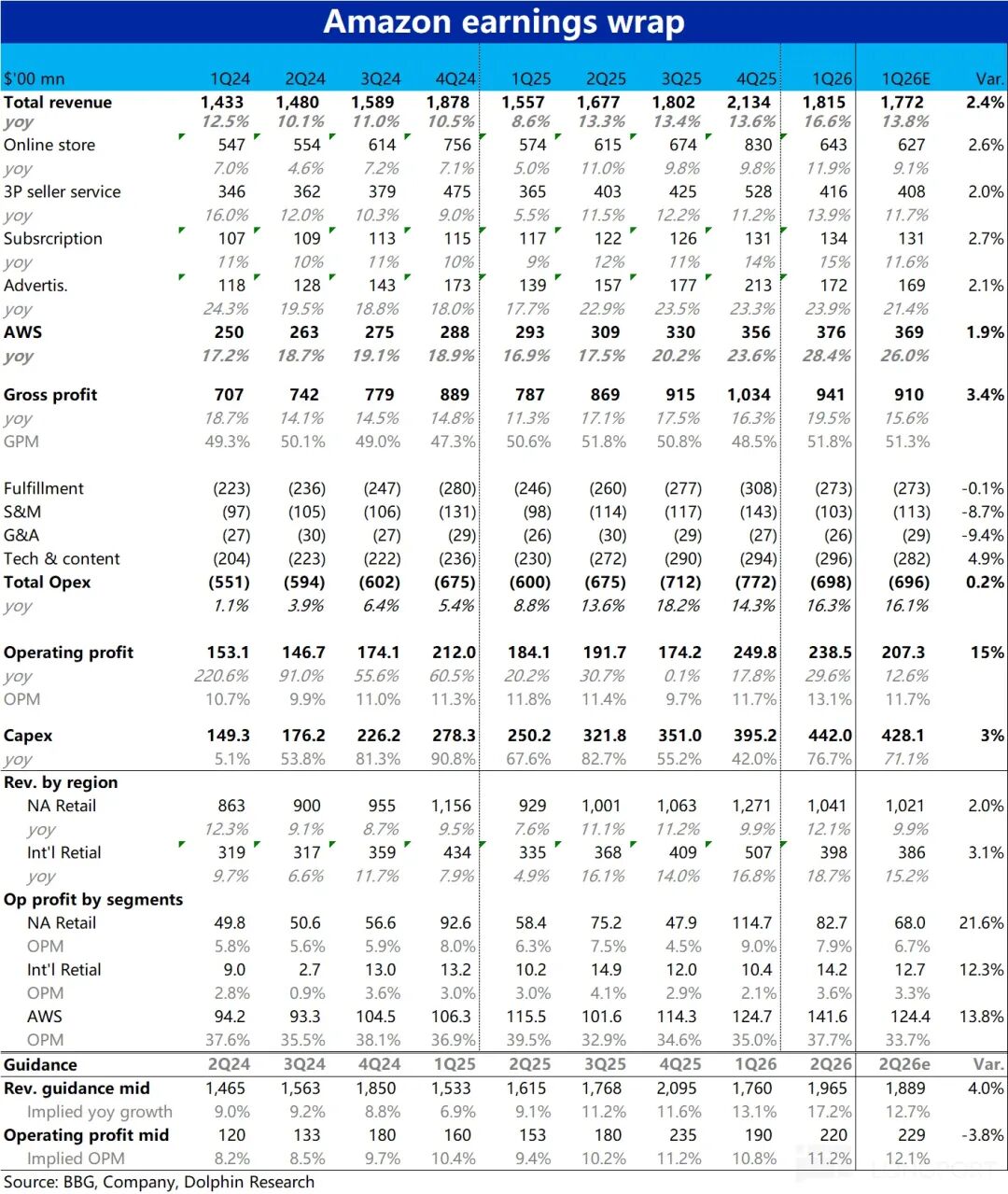

Amazon released its financial results for the first quarter of 2026 after the U.S. stock market closed on April 30 (Beijing Time). Overall, AWS experienced significant accelerated growth, and the pan-retail sector also showed steady improvement, with both revenue and profit for the quarter outperforming Bloomberg's expectations.

However, since the company's stock price had rebounded by over 30% from its low in recent weeks, market expectations had already risen sharply. From the perspective of expectation gaps, there were no real surprises. Specific observations include:

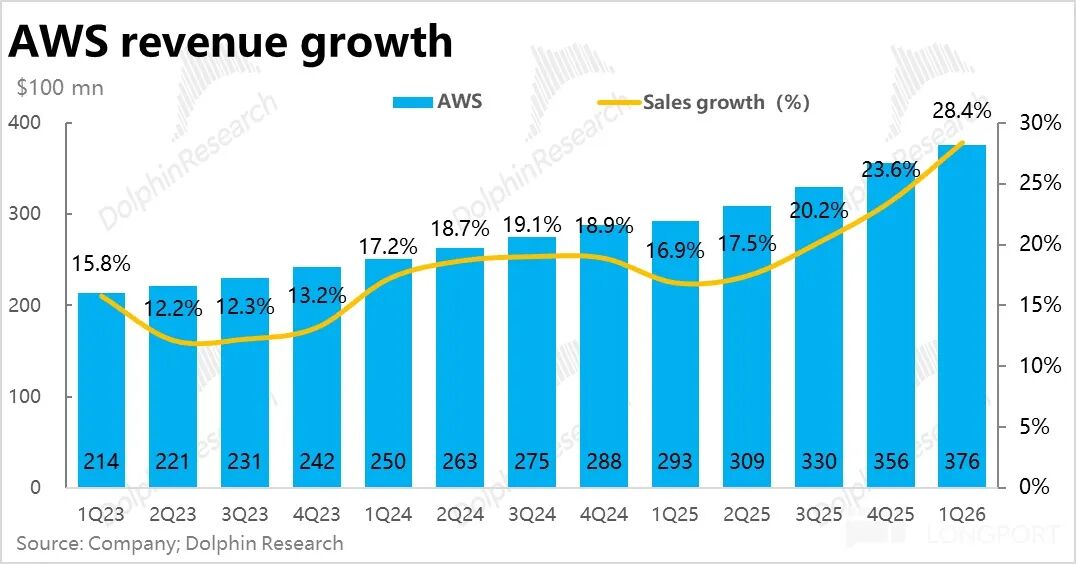

1. AWS Accelerates as Expected, Enhancing Competitive Position: The core metric of focus—AWS revenue—increased by 28% year-over-year to $37.6 billion, accelerating significantly by over 4 percentage points from the previous quarter.

However, before the results, due to the outstanding performance of Anthropic, a spin-off from AWS, and frequent shortages in computing power, many investment banks had already raised their growth expectations for AWS to over 30%. Therefore, the actual growth rate of AWS this quarter fell short of the more optimistic buyer expectations.

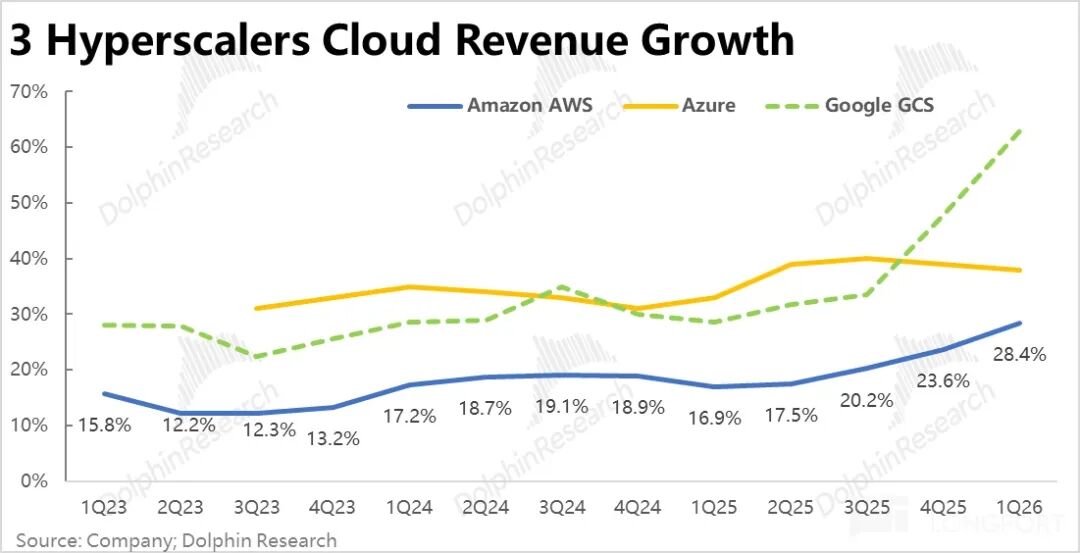

In terms of trends, AWS has accelerated for three consecutive quarters and recently signed major contracts with OpenAI and Anthropic, two of the strongest AI labs, clearly indicating a significant improvement in Amazon's competitive position in this wave of AI.

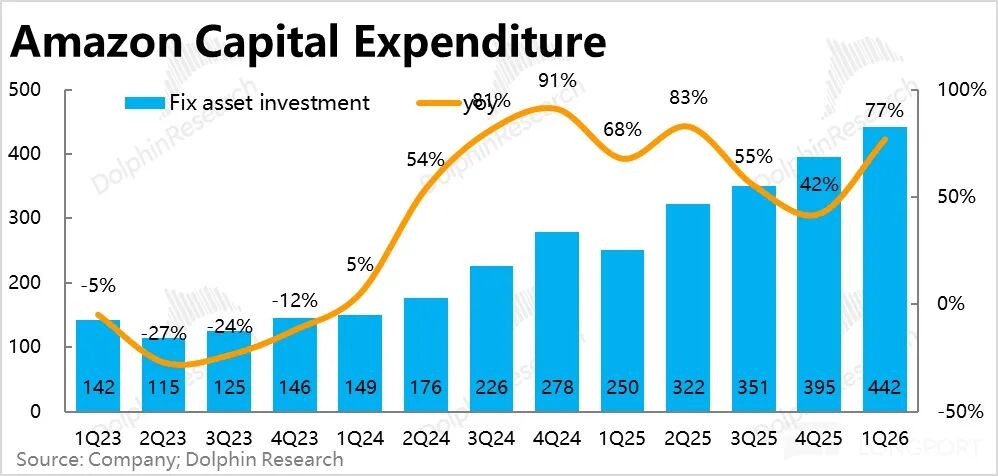

2. Capex Spending Reaches New Heights: Capex spending in this quarter reached $44.2 billion, increasing by $4.7 billion from the previous quarter's high base, exceeding market expectations (which were $42.8 billion). Compared to the other two major CSP giants, Amazon is currently the most aggressive in Capex investment.

On one hand, this is why AWS revenue has been able to accelerate significantly in recent quarters (with more computing power supply coming online). On the other hand, considering the company has just signed large contracts worth hundreds of billions of dollars with OAI and Anthropic, subsequent Capex investments and the pace of computing power center construction are likely to further accelerate.

3. Continued Bond Issuance to Support Cash Flow: This quarter, Amazon's operating cash inflow was $26.6 billion, but after deducting Capex, the free cash outflow was as high as over $17 billion. This marked the first time since the previous Capex cycle from 2021 to early 2023 that free cash flow turned negative again. After raising nearly $15 billion through bond issuance last quarter, the company raised over $53 billion this quarter.

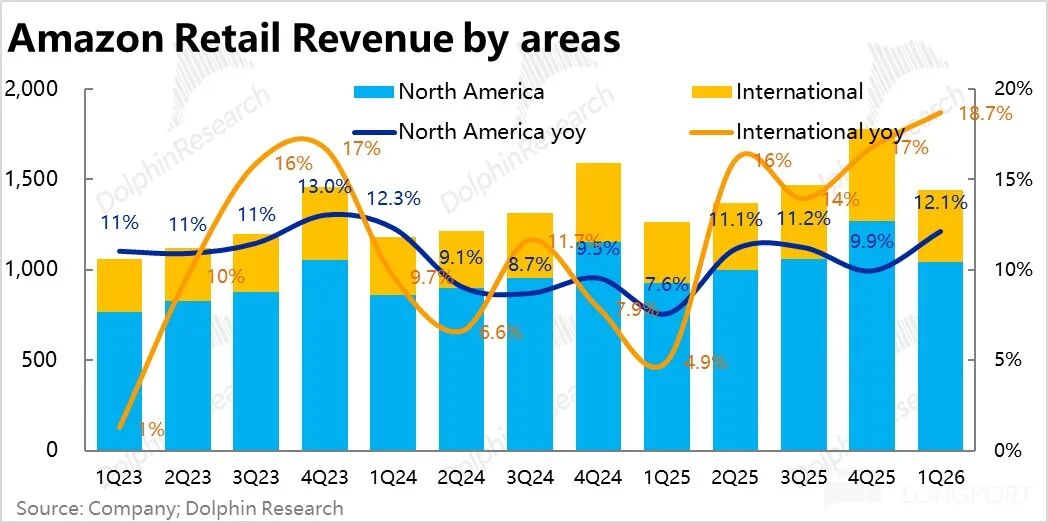

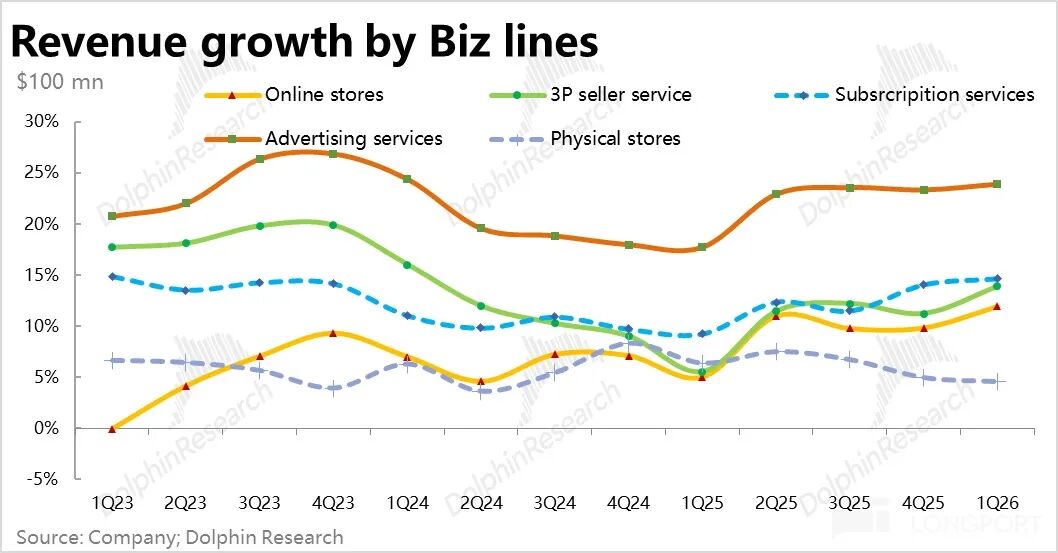

4. Steady Progress in the Retail Sector: The total revenue of the pan-retail sector this quarter was $143.9 billion, up 13.9% year-over-year, accelerating by nearly 2 percentage points from the previous quarter. Before the results, due to the impact of the U.S.-Iran conflict and rising oil prices, market expectations for the retail business were not optimistic. Therefore, it can be said that the performance of the retail sector this quarter exceeded expectations.

Among them, North American retail revenue growth was 12%, accelerating by over 2 percentage points from the previous quarter, and was not overly affected by the U.S.-Iran conflict. On one hand, overall U.S. non-store retail growth in January-February (7.7%-8.6%) was indeed higher than last quarter's growth rate.

On the other hand, Amazon's own investments in logistics and near-field grocery retail should have also contributed to the acceleration of retail business growth (the 15% increase in order volume this quarter was a historical high after the pandemic).

As for international retail revenue, it grew by 18.7%, but almost all of it was driven by favorable exchange rates. On a constant currency basis, revenue growth in recent quarters has been around 10%-11%, without any real acceleration.

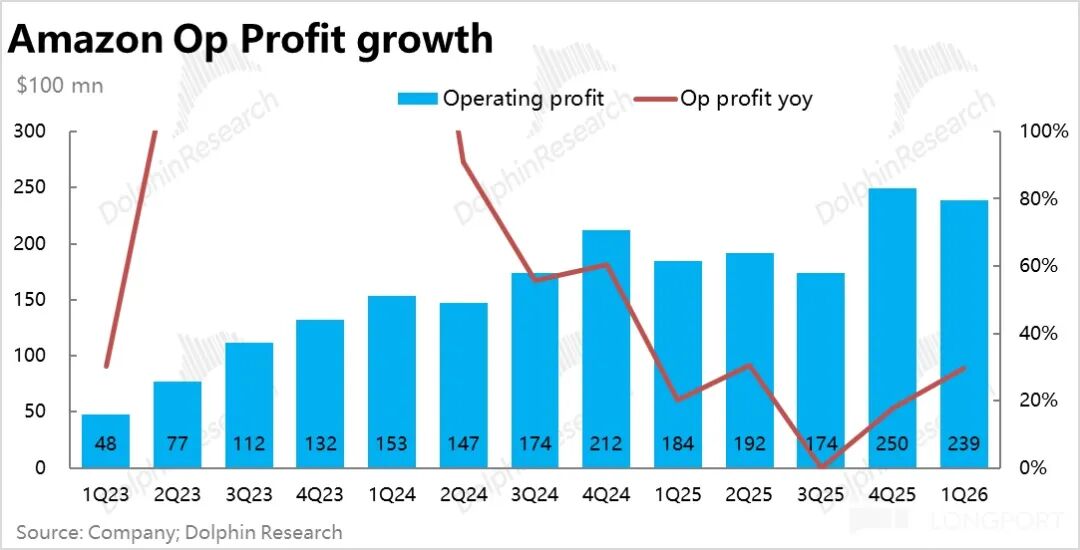

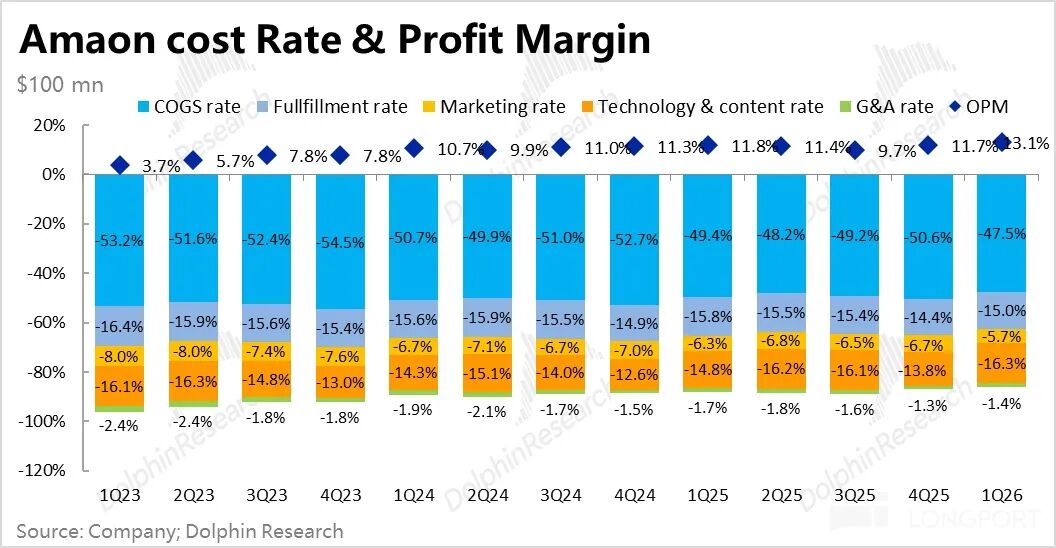

5. Strong Profits in AWS and North American Retail: Overall operating profit this quarter was $23.9 billion, better than the expected $20.7 billion. Profit increased by nearly 29% year-over-year, significantly outpacing revenue growth. Market concerns about the impact of the U.S.-Iran conflict and AI investments on profit margins were not as severe as feared, with profit margins actually still on an upward trend.

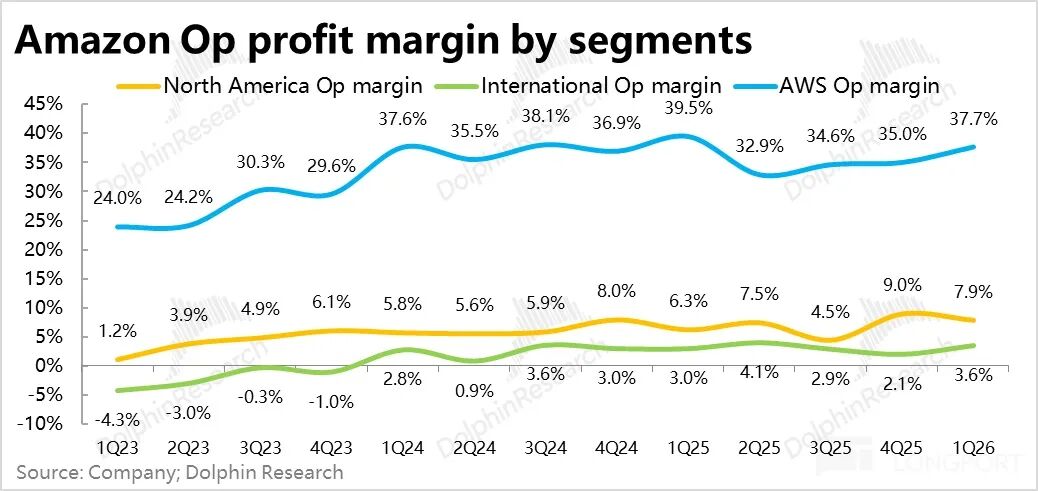

By segment, the operating profit margin for North American retail reached 7.9%, significantly higher than the expected 6.7% and the 6.3% from the same period last year. Although international retail profits also exceeded market expectations this quarter, about $350 million of that profit was due to favorable exchange rates. Excluding this impact, the actual profit margin for the international segment should have declined year-over-year.

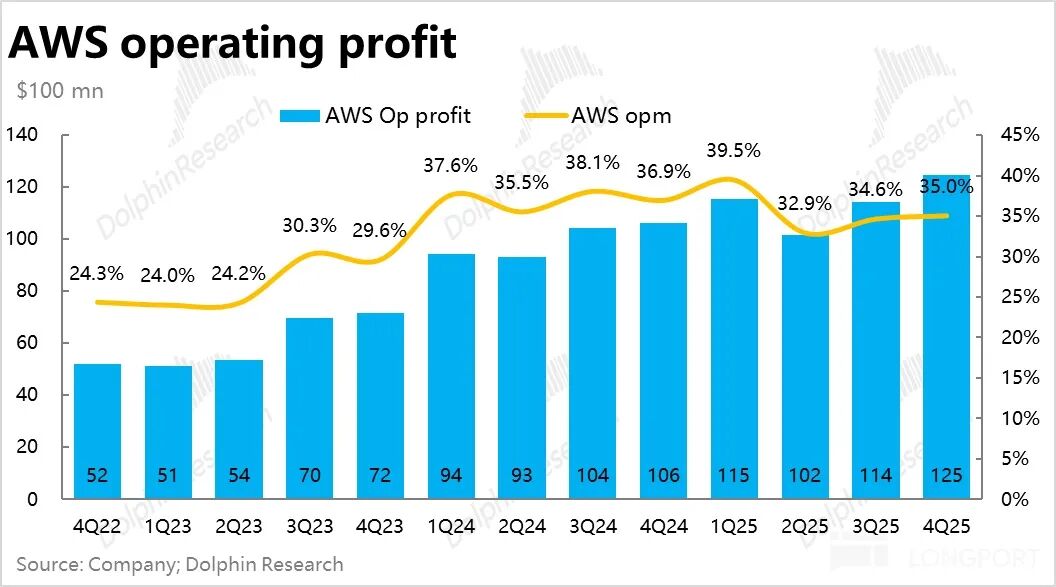

Meanwhile, although the operating profit margin for the AWS segment did decline due to AI investments, from 39.5% to 37.7%, the actual drop was far less severe than market concerns. Therefore, AWS's actual operating profit was about $14.2 billion, also significantly better than the expected $12.4 billion.

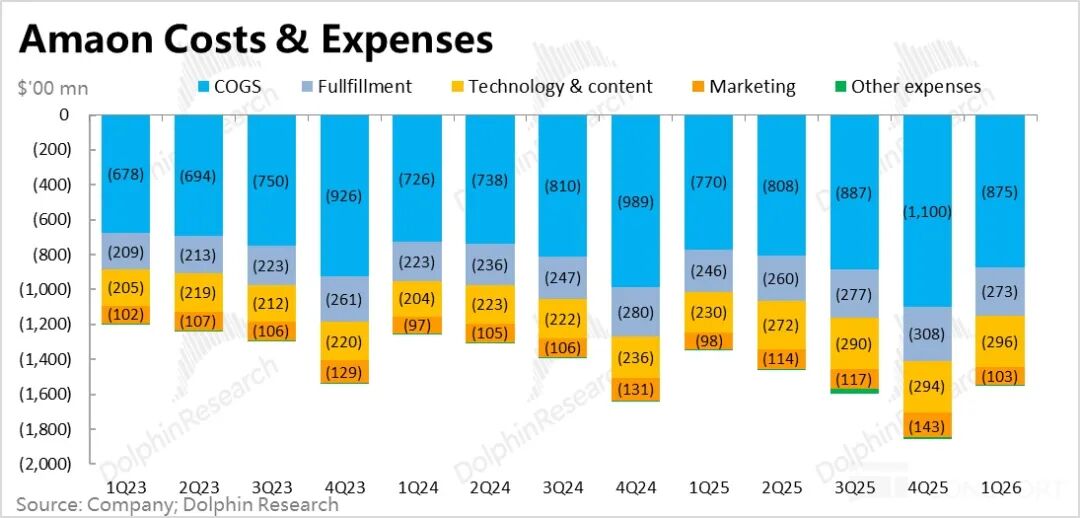

6. Profit Beat Expectations Mainly Due to Gross Margin Improvement: From a cost and expense perspective, the profit beat this quarter was mainly due to an improvement in gross margins rather than cost control. The overall gross margin was 51.8%, up 1.2 percentage points year-over-year, similar to the increase in the previous quarter.

Total operating expenses were $69.8 billion, slightly higher than expected, and increased by 16.3% year-over-year, roughly in line with revenue growth, meaning expense ratios remained largely unchanged.

The main reason for the significant year-over-year increase in R&D expenses (up 29%) should be the higher investment in R&D for AWS business and AI-related features.

Dolphin Research View:

1. Strong Quarterly Performance: Overall, Amazon's performance this quarter was undoubtedly strong:

a. The AWS segment saw accelerated revenue growth, and profit margins did not decline significantly as the market had feared;

b. The pan-retail sector, especially North American retail, demonstrated resilient revenue growth and improved profit margins despite the U.S.-Iran conflict;

c. Although Capex spending continued to rise, leading to negative free cash flow and frequent bond issuance, the market is unlikely to be overly critical given AWS's accelerated growth and the ability to secure major contracts, proving the value of the investments.

2. Guidance Suggests Continued Revenue Acceleration but Greater Profit Pressure: For next quarter's guidance, the company expects revenue to grow by 16%-19% year-over-year, continuing to accelerate from this quarter.

One reason for this is that this year's Prime Day promotion has been moved from July to June, which will benefit retail revenue in the second quarter (Wells Fargo estimates the benefit at around $7 billion, equivalent to a 4% contribution to growth).

On the other hand, assuming the upper limit of the guidance for revenue and that retail revenue grows by 15%-16% overall next quarter, it implies AWS revenue growth of around 30%-35% next quarter, continuing to accelerate.

However, the expected median operating profit for next quarter is $22 billion, somewhat below market expectations. The implied profit margin for next quarter is 11.2%, lower than the market's expected 12.1% and the same as last year's level.

This suggests that the impact of the conflict and Capex investments on profit margins may become more pronounced next quarter. However, the actual delivery will be key—if the upper limit of the guidance ($24 billion) is achieved, the implied profit margin would be in line with market expectations.

3. Continued Improvement in AI Competitive Position: Combining this quarter's financial performance with a series of recent developments related to the company, the most significant change in Amazon's recent logic is the significant improvement in its overall AI competitiveness in the current AI wave. Accumulated positive signs over the past few quarters have finally "quantitatively transformed into qualitative change" this quarter. Specific observations include:

a. Deeper Cooperation with OpenAI: Following OAI's announcement last quarter of signing a $38 billion seven-year contract with AWS, cooperation between Amazon and OAI deepened further this quarter.

First, OAI committed to expanding its order size with AWS to $138 billion over seven years, equivalent to about $20 billion in annual AWS revenue;

With the cancellation of Microsoft's exclusive sales agreement for OAI APIs, Amazon can now also distribute various models and tools developed by OpenAI on AWS and embed some features into AWS's own services/products;

OAI committed that about 2GW of its new hundred-billion-dollar computing power contract will be based on Trainium chips.

b. Deeper Cooperation with Anthropic: Similarly, Amazon and Anthropic recently signed a new series of cooperation terms. This includes Amazon committing to invest an additional $5 billion in Anthropic, with the option for up to $20 billion in additional investment.

In "return," Anthropic committed to expanding its computing power contract with AWS to $100 billion over ten years and also committed to using a total of 5GW of Trainium chips (including existing models and subsequent new releases).

Through cooperation with the two strongest AI labs, Amazon has "killed multiple birds with one stone" by securing more computing power contracts, enhancing its products' AI capabilities, and building a cornerstone user base and ecosystem for its ASIC chips.

This is reflected in the financial results, with significant acceleration in AWS revenue growth and RPO contract balances increasing from $244 billion last quarter to $364 billion (reflecting OAI's orders but not Anthropic's hundred-billion-dollar contract yet).

c. Self-Developed Chips: It is worth emphasizing separately that the annualized revenue from chip sales has reached $20 billion, and if including internal use, the annual revenue scale has reached $50 billion, with committed order amounts for Trainium chips reaching $225 billion.

From this perspective, Amazon's ASIC chip business (including GPUs and CPUs) is already close to one-fifth of NVIDIA's scale (including self-use), Expected to contribute separately to the valuation of the group .

From the perspective of the group's overall competitiveness, Trainium is expected to save the company tens of billions in Capex spending annually (reducing reliance on external chips) and provide a few percentage points of advantage in operating profit margins due to higher energy efficiency.

In other words, in the three core competitiveness areas of the AI era—large models, cloud, and chips—Amazon already holds an industry-leading position in the latter two.

From an investment perspective, Amazon is clearly at an important inflection point where its investment narrative is changing. Subsequently, its AWS and chip businesses should enter a stage of gradual release and realization of benefits. A more detailed value analysis has been published by Dolphin Research in an article with the same title in the "Insights-Depth" section of the Changqiao App.

In the medium to short term, Dolphin Research believes that an important indicator to assist in judging Amazon's investment opportunities is the growth rate of Anthropic's annualized revenue, or the speed of adoption and usage of its models/products.

We believe that the significant acceleration in AWS revenue growth in the first quarter and Anthropic's success in the AI wave from Chatbot to Agent and Vibe Coding during the same period, driven by its Opus model and Claude Code, are closely related. According to reports, Anthropic's annualized revenue surged from about $9 billion at the end of 2025 to $19 billion in March this year.

As Anthropic's primary computing power supplier, and Anthropic being AWS's current most significant AI client (OpenAI just signed a contract with AWS, with limited substantial revenue contribution in the short term), AWS's AI revenue likely grew by a similar magnitude in the first quarter when Anthropic's annualized revenue doubled.

Therefore, close attention should be paid to subsequent major product/model updates released by Anthropic, such as the model "Claude Mythos"—rumored to have major breakthroughs in logical reasoning and cybersecurity—and whether it can achieve similar or greater success than Claude Code, driving another significant increase in Anthropic's token consumption. If so, it could likely prompt AWS's revenue growth to exceed expectations again.

Detailed analysis is as follows:

I. AWS: Accelerated Growth, Strong Profits, but Expectations Are High

The most closely watched core business metric—AWS revenue—increased by 28% year-over-year to $37.6 billion (similar growth rate on a constant currency basis), accelerating significantly by over 4 percentage points from the previous quarter and nearly 11 percentage points from the same period last year.

However, although AWS continues to accelerate, its actual performance did not exceed expectations. Before the results, several major banks had already raised their growth expectations for AWS this quarter to over 30%, and for the full year of 2026 to over 35%. Therefore, optimistic investors may be somewhat disappointed.

Combined with the already highest Capex spending among CSPs, which continues to rise this quarter, and the recent signing of over hundred-billion-dollar contracts with both OAI and Anthropic, subsequent AWS growth is basically certain to continue accelerating. The question is whether it can meet the significantly raised market expectations.

In addition to accelerated growth, AWS's operating profit this quarter also significantly exceeded expectations, with an actual operating profit margin of 37.3%, far surpassing the market's expected 33.7%. Actual operating profit was nearly $14.2 billion, up 23% year-over-year, without a significant "revenue growth without profit growth" issue.

Although profit margins did decline year-over-year due to the impact of AI business, the drop was only 1.8 percentage points. The pressure was not as severe as generally expected by sellers, but with Capex and AI-related revenue accounting for a further increase, the downward trend in profit margins is likely to continue.

II. Continued Rise in Capex

In terms of Capex, expenditures reached $44.2 billion this quarter, up approximately $4.7 billion from the previous quarter and higher than the already not-low market expectation of $42.8 billion. In a horizontal comparison, Amazon is also the only one among the three major cloud providers to have Capex exceed expectations and to have seen a quarter-over-quarter increase from 1Q to 4Q. However, from a full-year perspective, the company still maintains a Capex budget of $200 billion.

Such aggressive Capex investments explain why AWS revenue has continued to accelerate significantly. Dolphin Research believes that this is also likely because the company recently signed major deals with OAI and Anthropic, which may necessitate accelerating the pace of computing power center construction to meet the computing needs of these two major clients on time.

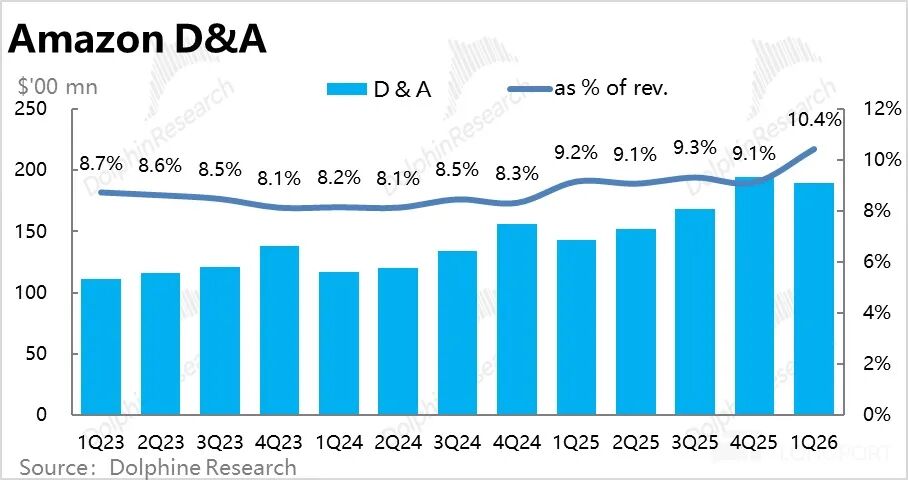

Correspondingly, the proportion of D&A to revenue also broke through the level of just over 9% last year, reaching 10.4% this quarter. Dolphin Research believes that this may be one of the reasons why AWS's profit margin was still decent this quarter, aligning with our previous judgment that the proportion of depreciation to revenue is likely to increase by another 2-3 percentage points by 2026. Therefore, the pressure on AWS's profit margins is expected to inevitably increase in the coming quarters and will require attention.

III. Steady Growth in Pan-Retail: Genuine Improvement in North America, International Growth Driven by Exchange Rates

The pan-retail sector also showed steady growth this quarter, with total revenue reaching $143.9 billion, a year-over-year increase of 13.9%, accelerating by nearly 2 percentage points from the previous quarter. Due to the significant rise in U.S.-Iran conflicts and oil prices, unlike the optimistic outlook for AWS, market expectations for the retail business before the results were not overly optimistic. Therefore, it can be said that the retail business's performance this quarter exceeded expectations.

Regionally, retail revenue growth in North America was 12%, accelerating by more than 2 percentage points from the previous quarter. According to U.S. Census Bureau data on non-store retail growth, the year-over-year increase from October to December was 5%-7%, while the growth from January to February was 7.7%-8.6%. This indicates an overall acceleration in the U.S. retail industry.

However, we believe that Amazon's recent investments in logistics efficiency (such as same-day delivery) and near-field fresh and grocery retail have also contributed to the acceleration of retail business growth.

Additionally, retail business revenue in international regions grew by 18.7%, but this was almost entirely driven by favorable exchange rates. In constant currency terms, revenue growth in recent quarters has been around 10%-11%, without any real acceleration.

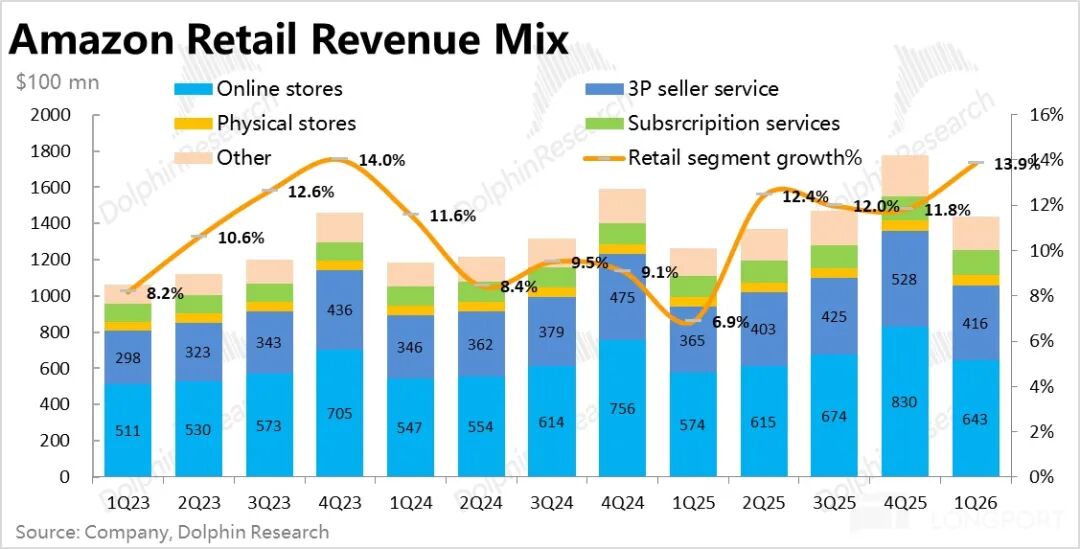

Growth across various business lines has also been generally steady, with specifics as follows:

a. Revenue growth from self-operated retail and third-party merchant services showed a slight improvement of 1-2 percentage points quarter-over-quarter, while sales growth in offline physical stores slowed somewhat.

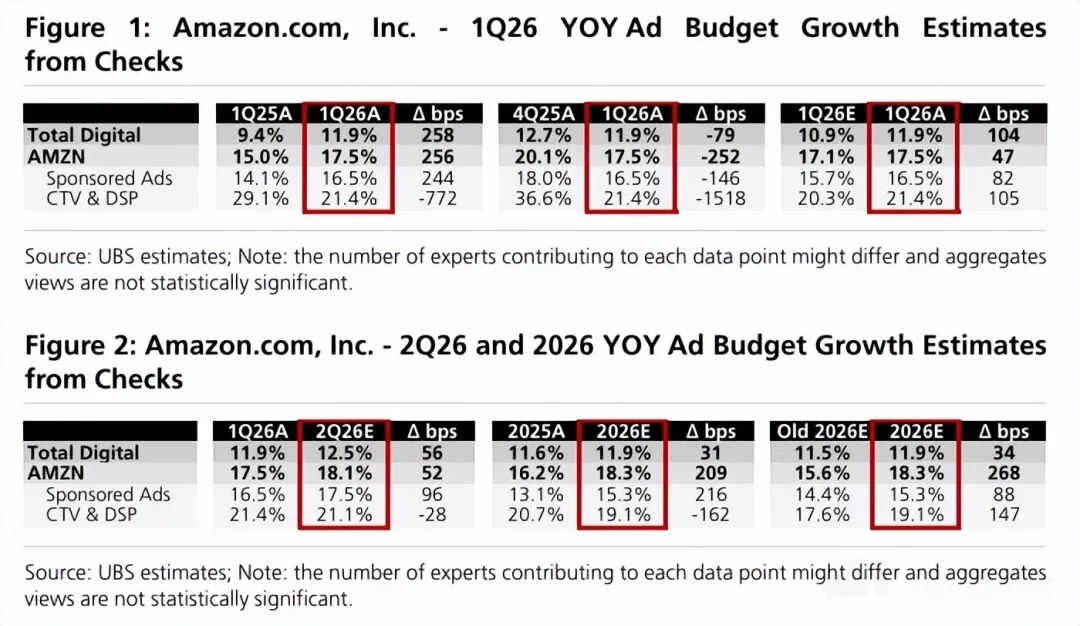

b. Advertising revenue growth remained strong, increasing by 22% in constant currency terms, the same as the previous quarter's growth rate. According to previous reports, advertising for other Amazon multimedia content, such as Prime Video, should be the main driver.

Additionally, according to recent research on advertising budgets, Amazon's advertising revenue growth is expected to significantly outpace overall market growth in 2026, at approximately 18% vs. 12%.

IV. Profit Exceeds Expectations, with North America and AWS Being the Main Contributors

Across all businesses, Amazon's total revenue for the quarter was $181.5 billion, a year-over-year increase of 16.6%, better than the market expectation of $177.2 billion. Excluding the impact of favorable exchange rates, actual revenue growth was approximately 15%, accelerating by 3 percentage points from the previous quarter, primarily driven by AWS, with contributions from the retail sector in North America.

Meanwhile, Amazon's profit for the quarter was also strong, with overall operating profit reaching $23.9 billion, better than the expected $20.7 billion.

Profit increased by nearly 29% year-over-year, significantly outpacing revenue growth. Concerns about the impact of U.S.-Iran conflicts and AI investments on the company's profit margins are, at least for now, not evident, as the company's profit margins are still on an upward trend.

By segment:

a. As mentioned earlier, while AWS's profit margin did decline year-over-year, the drop was only 1.8 percentage points, not as severe as market concerns suggested.

b. Within the pan-retail sector, the operating profit margin in North America reached 7.9% this quarter, significantly higher than the expected 6.7% and the 6.3% from the same period last year, indicating that profit margins are still improving.

c. The operating profit for the international retail segment was $1.42 billion this quarter, higher than market expectations. However, it should be noted that approximately $350 million of this profit was due to favorable exchange rates. Excluding the impact of exchange rates, the actual profit margin for the international segment declined slightly compared to the same period last year.

Overall, the better-than-expected profit this quarter was mainly due to contributions from the North American retail segment and AWS business.

V. Gross Margin Exceeds Expectations, R&D Expenses Surge

From a cost and expense perspective, the better-than-expected profit this quarter was mainly due to an improvement in gross margin rather than cost control. Specifically, Amazon's overall gross margin for the quarter was 51.8%, expanding by 1.2 percentage points year-over-year, with an improvement rate similar to that of the previous quarter.

This shows that despite the gradual increase in Capex and depreciation dragging down AWS's gross margin, the impact of revenue structure improvements and efficiency gains in the pan-retail sector was more significant.

In terms of expenses, total operating expenses for the quarter were $69.8 billion, slightly higher than expected and up 16.3% year-over-year, roughly in line with revenue growth. In other words, the contribution of expense control to profit margin improvement was very limited this quarter.

Specifically, the main driver was a significant year-over-year increase of 29% in R&D expenses, while other expenses remained relatively restrained. Since R&D expenses include AWS employee salaries, R&D costs, some equipment costs, and streaming content production costs, it can be inferred that the increase was mainly due to higher investments in AWS business and AI-related R&D.

- END -

// Reproduction Authorization

This article is an original piece by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any person receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or opinions expressed in this report shall not, under any jurisdiction, be construed as or deemed to be an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for or proposed for distribution to jurisdictions where distribution, publication, provision, or use of such information, tools, and materials would conflict with applicable laws or regulations, or result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in such jurisdictions, nor are they intended for citizens or residents of such jurisdictions.

This report only reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any way, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!