CPU Surges, Helios Approaches: Is AMD Finally Breaking Through?

05/08 2026

05/08 2026

685

685

AMD (AMD.O) released its Q1 2026 earnings report (as of March 2026) after the U.S. market closed on the morning of May 6, 2026 (Beijing Time). Key highlights are as follows:

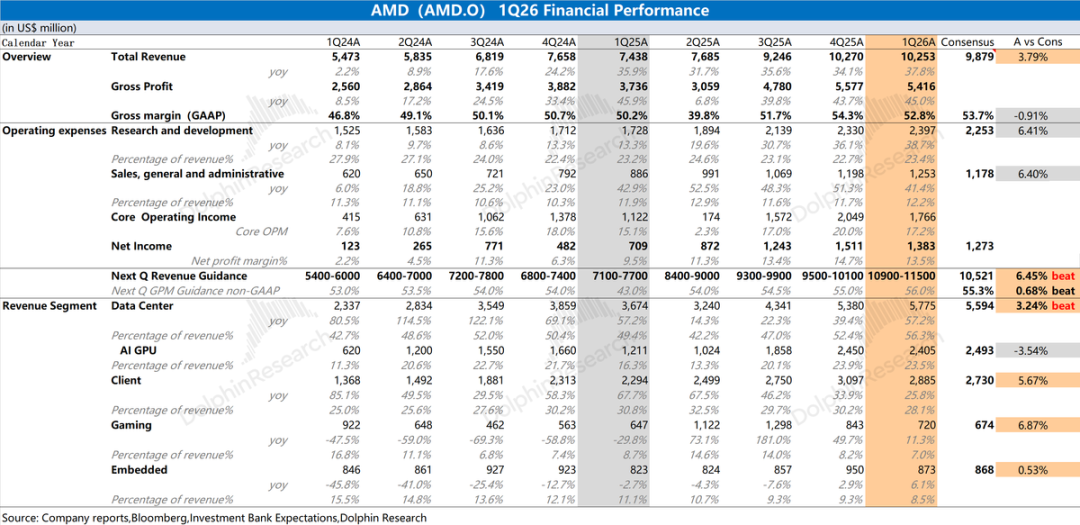

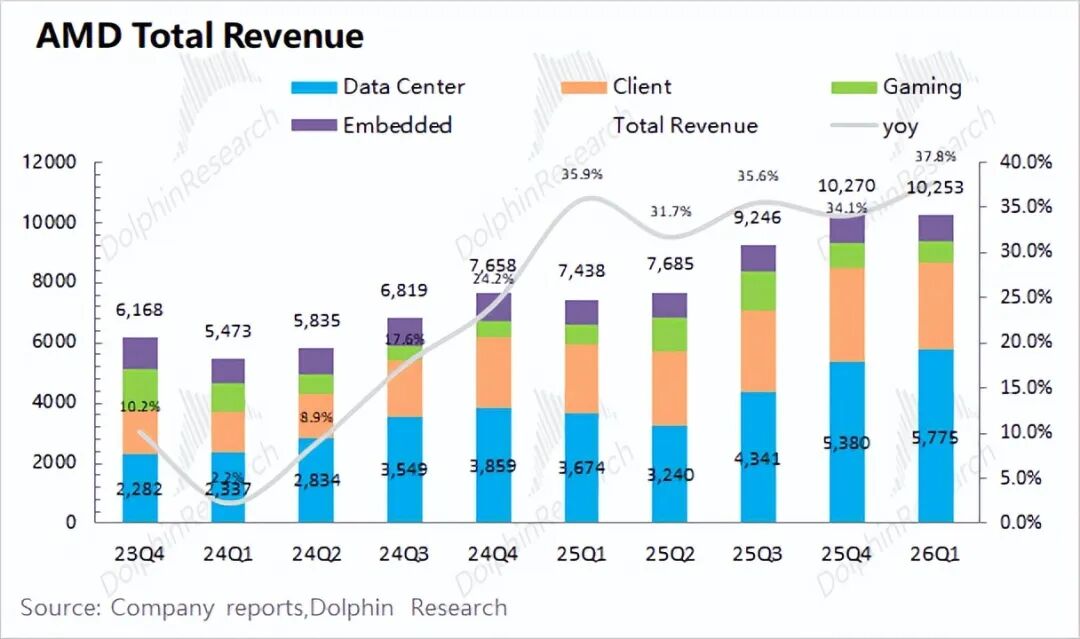

1. Overall Performance: AMD achieved Q1 2026 revenue of $10.25 billion, up 37.8% YoY, surpassing market expectations ($9.9 billion). The revenue growth was primarily driven by expansion in the data center and client businesses.

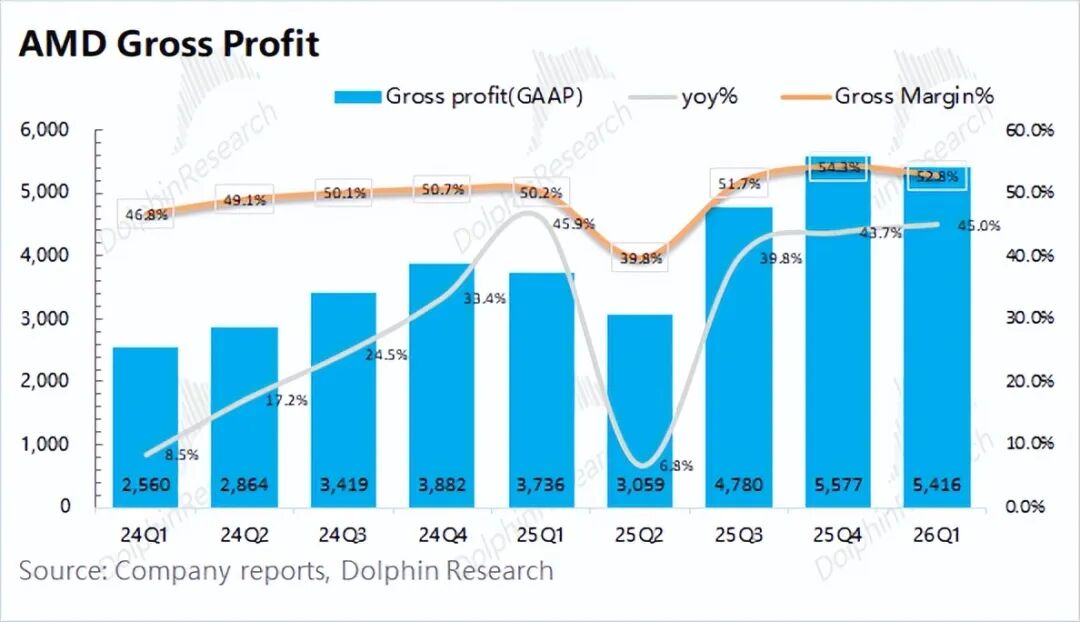

The company's Q1 gross margin (GAAP) was 52.8%, up 2.6 percentage points YoY, mainly due to an increased proportion of higher-margin data center business.

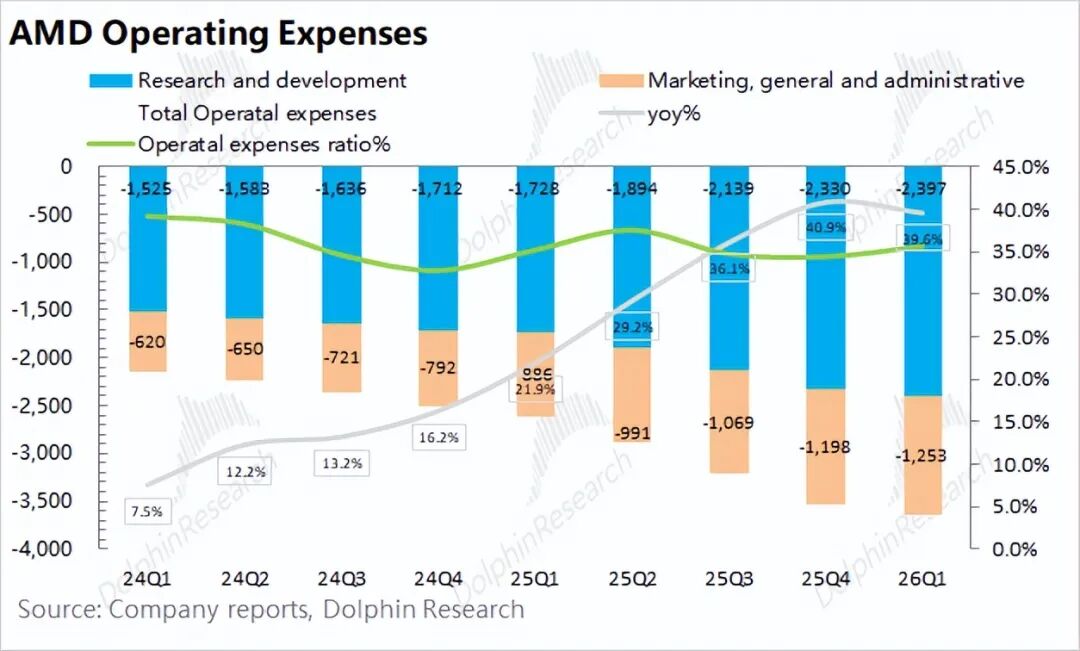

2. Operating Expenses: R&D expenses reached $2.4 billion, up 38.7% YoY; selling, general, and administrative expenses were $1.25 billion, up 41% YoY. The growth in core operating expenses aligned closely with revenue growth, maintaining the core operating expense ratio near 35%.

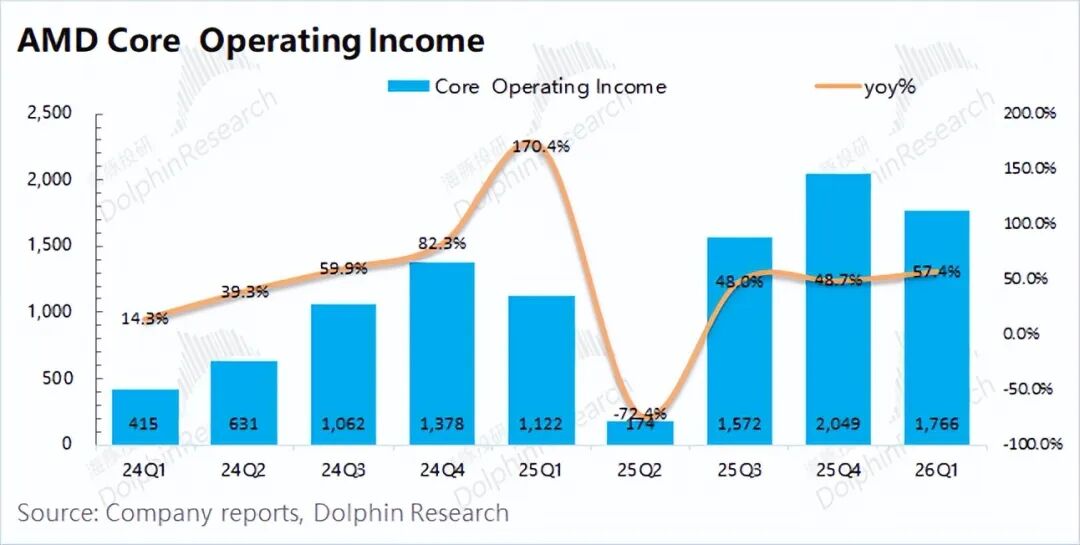

AMD reported Q1 net income of $1.38 billion, primarily influenced by non-recurring items. From an operational perspective, core operating profit was $1.77 billion, up 57% YoY, with a core operating margin of 17%.

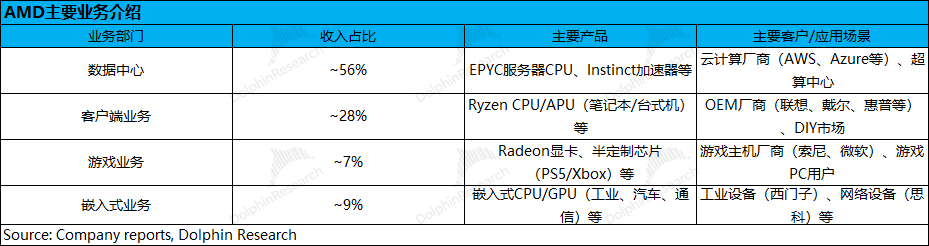

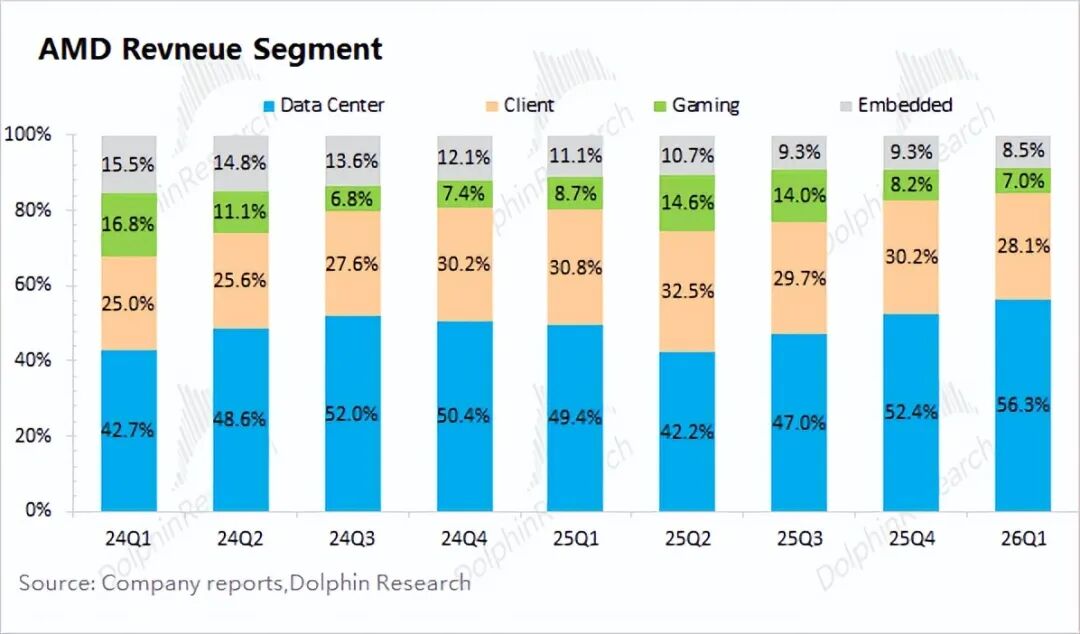

3. Business Segment Breakdown: Driven by growth in data center and client businesses, these two segments accounted for over 80% of total revenue.

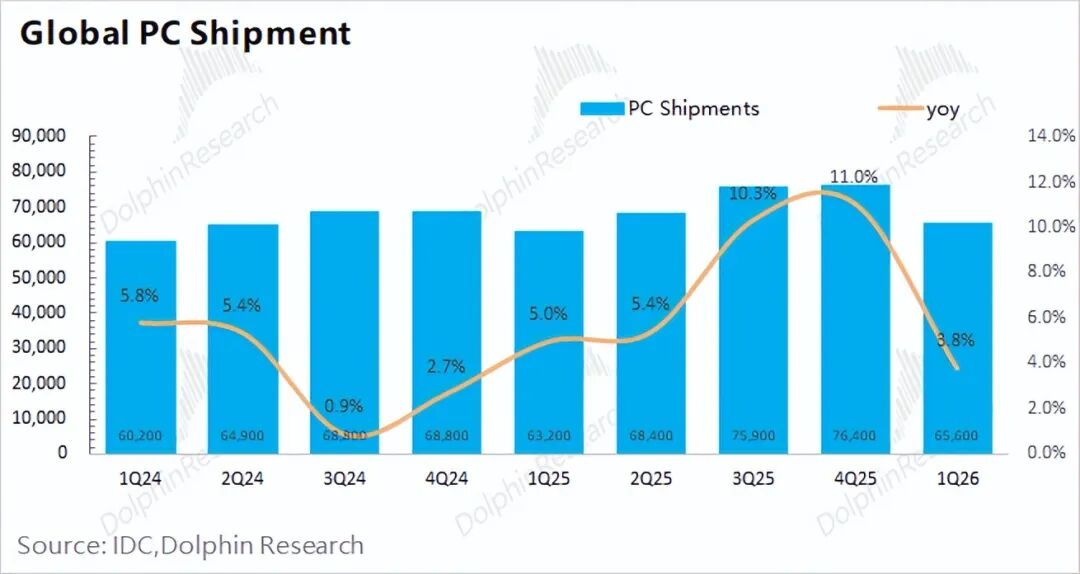

1) Client Business Gains Market Share: Revenue reached $2.89 billion, up 26% YoY. Global PC shipments grew 3.8% YoY, while AMD's client business continued to surge, primarily due to increased market share in the PC segment.

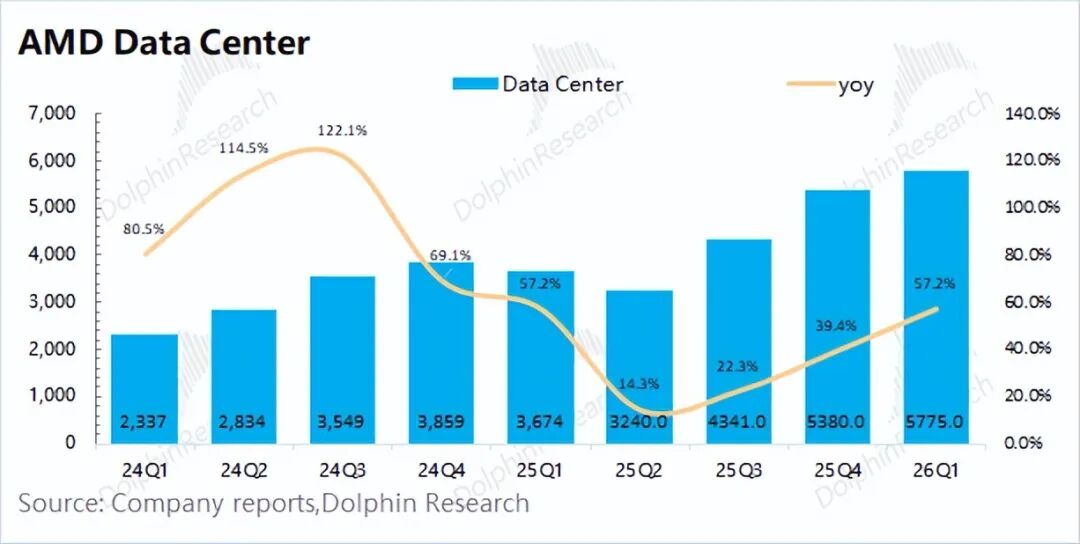

2) Data Center: Server CPUs Enter Positive Cycle, Anticipation for MI450 Series. Revenue hit $5.78 billion, up 7% QoQ. Growth was driven by tight supply-demand dynamics in server CPUs.

① Server GPUs: AI GPU revenue declined slightly QoQ due to revenue adjustments in China, with approximately $390 million from MI308 sales to China last quarter.

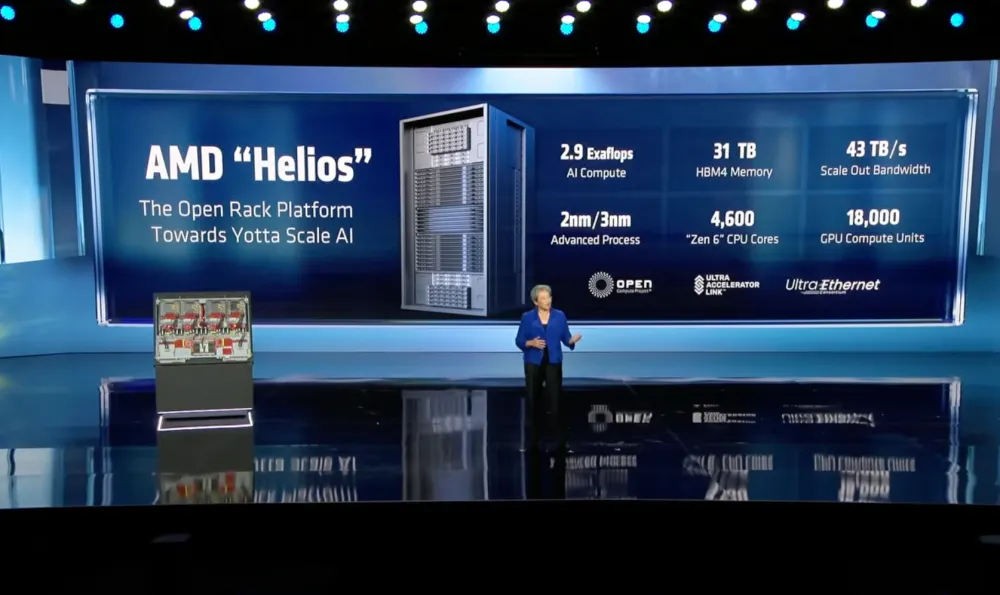

The market is more focused on the MI450 series, slated for mass production in H2 2026. This will mark AMD's first transition from 'single-chip' to 'rack-level cluster' delivery. The company has established partnerships with clients like OpenAI and Meta, with MI450's mass production performance directly impacting final deliveries.

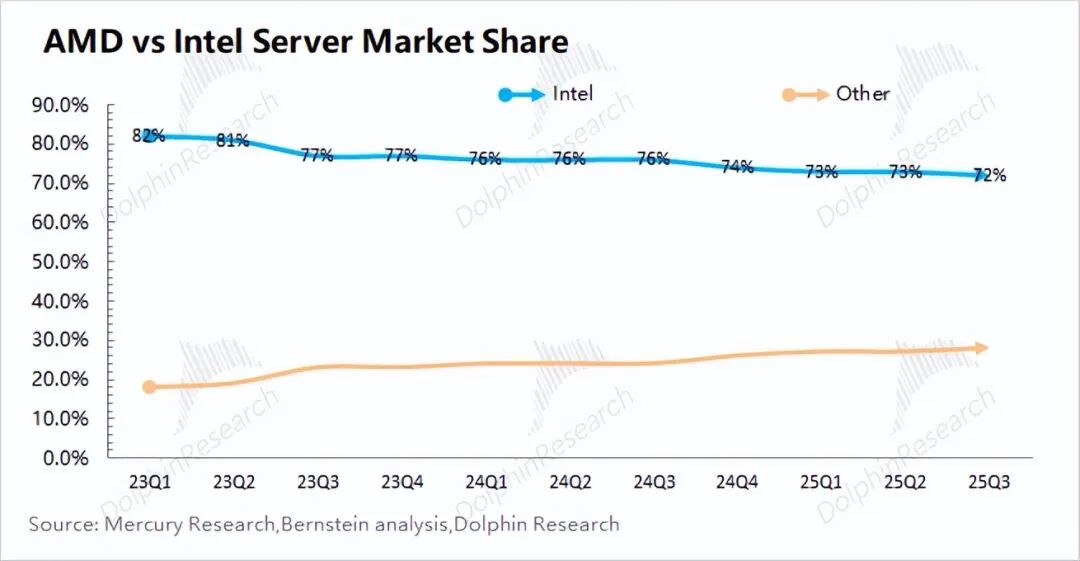

② Server CPUs: Driven by increased demand for server-side CPUs, this segment was the primary growth contributor in Q1. Dolphin Research estimates AMD's server CPU revenue reached approximately $3.3 billion, up 15% QoQ. According to third-party data, AMD's server CPU market share has surpassed 20%.

4. AMD's Guidance: Q2 2026 revenue is expected to be $10.9-11.5 billion (surpassing market expectations of ~$10.5 billion), with a midpoint ($11.2 billion) up 9% QoQ. Non-GAAP gross margin is expected to be around 56% (surpassing market expectations of 55.3%).

Dolphin Research's Overall View: CPU Enters Upcycle, Awaiting MI450 to Unlock 'Dual-Wheel Drive'

AMD's Q1 earnings were strong, with revenue exceeding expectations primarily due to growth in server CPUs.

Current AI GPU (MI355) performance is weak, with a slight QoQ decline influenced by revenue adjustments in China. The market is more focused on the upcoming MI450 series. AMD has secured partnerships with clients like OpenAI and Meta for the MI450, which will transition from 'single-chip' to 'rack-level cluster' delivery.

Beyond Q1 results, the company provided strong guidance. Next quarter's revenue is expected to be $10.9-11.5 billion, up 6-12% QoQ, significantly surpassing market expectations ($10.5 billion). Non-GAAP gross margin is expected to be around 56% (surpassing market expectations of 55.3%).

The strong next-quarter outlook is primarily driven by server CPUs. Dolphin Research projects AMD's server CPU-related revenue could reach $3.8 billion, up 15% QoQ.

Beyond Q1 earnings, the market is focused on the following aspects of AMD:

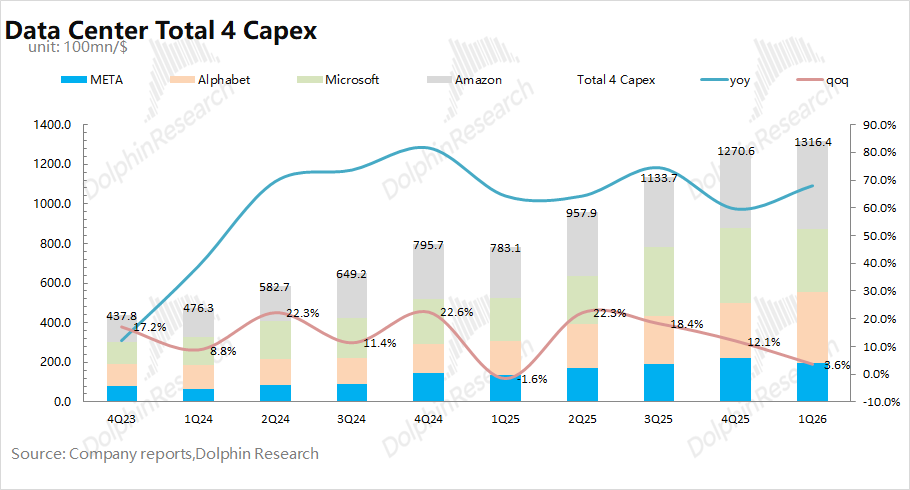

a) Capital Expenditures by Major Players: In this 'hot' AI cycle, cloud service giants are the primary chip buyers.

Recently, four major players released their latest earnings, with Meta and Microsoft explicitly raising their capital expenditures.

For 2026, Dolphin Research expects the combined capital expenditures of the four core cloud providers (Meta, Google, Microsoft, and Amazon) to exceed $700 billion, with YoY growth exceeding 70%.

Capital expenditures in 2026 will follow a 'low in H1, high in H2' trend, as NVIDIA's Rubin and AMD's MI450 series will both begin mass production in H2.

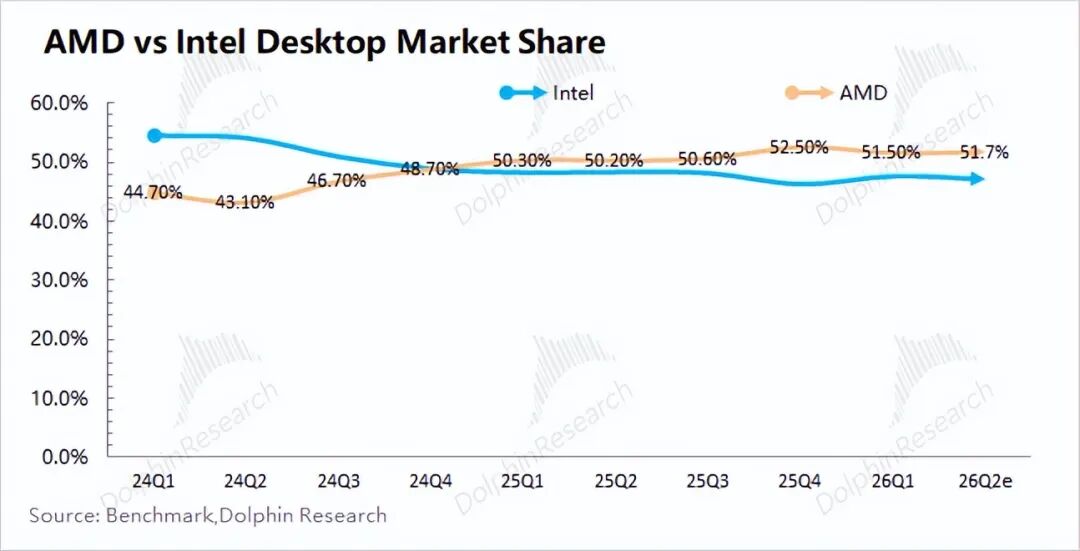

b) CPUs Enter the AI Mainstage: While PC industry shipments grew 3.8% YoY in Q1, Intel's client business grew only 1.3% YoY. AMD, however, achieved 26% growth, reflecting its continuously improve (sustained improvement) in CPU competitiveness.

In the overall CPU market (including PC and server CPUs), AMD's market share has been increasing in recent years, particularly surpassing Intel in the desktop market.

Previously, AI training focused on 'computing power,' making CPUs less critical. However, as the focus shifts to AI inference, 'latency' becomes more important. CPUs handle resource scheduling and data preprocessing, directly impacting throughput, latency, and efficiency in the inference stage. Increased demand for CPUs in AI servers has driven up server CPU prices.

On the other hand, AMD is gradually 'eroding' Intel's market share through its competitiveness. According to third-party data, AMD's server CPU market share has surpassed 20%.

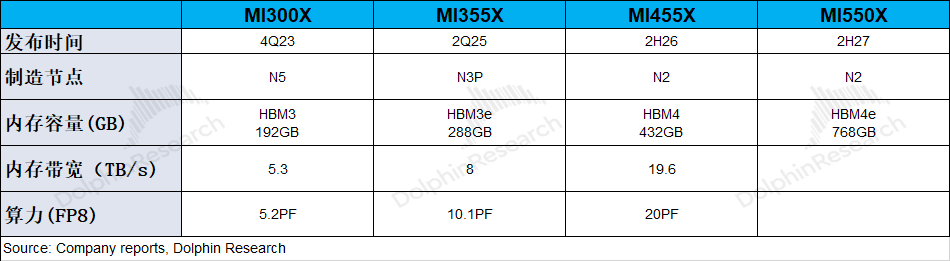

c) AI GPU Progress: Currently, AMD's primary shipments are MI355, with market attention focused on the MI455 launching in H2.

The MI355 to MI455 upgrade primarily involves computing power, memory, and clustering. Computing power is expected to double (adopting 2nm process), while memory upgrades enhance bandwidth and capacity (from HBM3E to HBM4).

Beyond computing power and memory upgrades, the market is more focused on AMD's breakthrough in rack-level solutions. As the focus of large models shifts from training to inference, the importance of computing power diminishes. For example, AMD's MI355 series is in the same tier as NVIDIA's B200 in terms of computing power, but AMD's market competitiveness hinges on its inability to deliver rack-level clusters.

For the MI450 series, AMD plans to deeply integrate it with the Helios rack-mounted platform, enabling a transition from 'single-chip' to 'rack-level cluster' delivery, directly competing with NVIDIA's Rubin architecture.

For large cloud service providers, 'clustered' deployments at scale are more critical than 'simply buying cards.' The MI450 series' 'rack-level cluster' delivery method is exactly what large CSPs need. Since the MI450 series will only begin mass production in H2, AMD's AI GPU revenue in 2026 will follow a 'low in H1, high in H2' trend.

AMD has secured multi-GW partnership agreements with companies like OpenAI, Meta, and Oracle. The mass production ramp-up of the MI450 series will directly impact deliveries to these clients.

Given AMD's current market cap ($579.2 billion), it corresponds to approximately 33x PE on 2027's after-tax core profit (assuming a two-year CAGR of 44% in revenue, a gross margin of 56.7%, and a tax rate of 13%).

Since the MI450 series will mainly ramp up in H2, 2027's performance is used as a reference. Compared to AI peers, AMD's current PE is significantly higher than NVIDIA's and TSMC's, reflecting expectations for the CPU upcycle and AMD's potential to gain greater market share in AI.

Overall, AMD's short-term performance is primarily influenced by its CPU business and MI355 shipments, especially as tight server CPU supply-demand dynamics drive a CPU upcycle. In the medium to long term, while server CPU demand surges, the market is also focused on the progress of the next-gen MI450 series, including new clients, new orders, and mass production delivery of rack-level clusters.

Driven by the broad CPU recovery cycle, AMD's earnings base is set to improve relatively. Notably, management raised the total addressable market for CPUs to $120 billion (from $60 billion) and increased the CPU/GPU ratio to 1:1, implying that CPUs will play a role in AI no less significant than GPUs, significantly boosting expectations for server CPUs.

In AI GPUs, AMD still lags behind NVIDIA in computing power but can still secure inference-related orders, having already won clients like OpenAI, Meta, and Oracle.

Attention will now focus on the mass production delivery of the MI450 series' 'rack-level cluster' solutions in H2. If deliveries to current major clients proceed smoothly, AMD could secure more external client orders, enjoying the dual-wheel-driven benefits of CPUs and GPUs in the AI track (AI sector).

Below is a detailed analysis:

I. Overall Performance: Revenue Exceeds Expectations, Guidance Even Stronger

1.1 Revenue

AMD achieved Q1 2026 revenue of $10.25 billion, up 38% YoY, surpassing market expectations (~$9.9 billion). The YoY revenue growth was primarily driven by expansion in the data center and client businesses.

Although AI GPU revenue declined slightly QoQ, server CPUs entered a positive cycle, driving continued growth in the data center segment. Dolphin Research estimates AMD's server CPU-related revenue reached $3.3 billion, up 15% QoQ.

1.2 Gross Margin

AMD achieved Q1 2026 gross profit of $5.42 billion, up 45% YoY. The gross margin was 52.8%, up 2.6 percentage points YoY, primarily due to an increased proportion of higher-margin data center business.

The company guided for Q2 non-GAAP gross margin of 56%, up 0.6 percentage points QoQ, driven by growth in server CPUs. While MI450 mass production in H2 will dilute margins slightly, the long-term gross margin guidance remains at 55-58%.

1.3 Operating Expenses

AMD's Q1 2026 operating expenses were $3.65 billion, up 40% YoY. Both R&D and selling, general, and administrative expenses increased significantly.

Breaking down the expenses: ① R&D expenses were $2.4 billion, up 39% YoY, as the company continued to increase investments in AI-related directions; ② Selling, general, and administrative expenses were $1.25 billion, up 41% YoY, reflecting higher revenue growth and increased employee incentive spending.

1.4 Profitability

Due to significant deferred expenses from AMD's acquisition of Xilinx, profitability will be eroded for some time to come. Regarding the actual operating conditions for this quarter, Dolphin Research believes that 'core operating profit' is a more accurate reflection.

Core Operating Profit = Gross Profit - R&D Expenses - Sales and Administrative Expenses

After excluding the impact of acquisition expenses, Dolphin Research estimates AMD's core operating profit for this quarter to be $1.77 billion, a 57% year-over-year increase, primarily driven by the recovery in server CPU demand.

II. Business Segment Breakdown: Server CPU Major Cycle, Focus on MI450 Mass Production Progress

From a business segment perspective, data center and client businesses are AMD's current primary operations, accounting for over 80% of total revenue. Benefiting from the mass production and shipment of AI GPUs (MI series) and the recovery in server CPU demand, the proportion of data center business continues to rise.

2.1 Data Center Business

AMD's data center business achieved revenue of $5.78 billion in the first quarter of 2026, a 57% year-over-year increase, outperforming market expectations (around $5.6 billion). The growth was primarily driven by the positive cycle of server CPUs.

Combining company and market expectations, a detailed breakdown shows: Dolphin Research anticipates AI GPU revenue of approximately $2.4 billion for the quarter, a slight sequential decline; server CPU and related revenues of about $3.3 billion, a 15% sequential increase. With the MI450 series set for mass production in the second half of the year, AMD's AI GPU revenue is expected to follow a 'low first half, high second half' trend.

Details:

a) Data Center CPUs: Leveraging the competitive combination of 'CPU+GPU,' AMD continues to increase its market share in the data center CPU segment, now exceeding 20%. Although Intel has recently established partnerships with NVIDIA and Google for x86 CPUs, this is primarily to provide customers with x86 solution options.

Amid the current major CPU cycle and with iterative upgrades to the Zen series, AMD's data center CPU performance is expected to sustain growth. Company management has provided guidance for a 70% year-over-year increase in server CPU revenue next quarter, with this growth rate expected to continue into the second half of the year, laying the foundation for strong annual growth.

b) AI GPUs: Current revenue primarily comes from the MI350, which entered mass production in the second half of last year. Since the MI350 series is still delivered at the 'chip level' and does not align with mainstream market demand, AI GPU performance has been relatively weak.

Given the increased capital expenditures from the four major cloud providers (Meta, Google, Microsoft, and Amazon), Dolphin Research expects their combined capital expenditures in 2026 to exceed $700 billion, a year-over-year increase of over 70%, setting the stage for high growth in the AI chip market in 2026.

In this rapidly growing market, AMD's ability to secure more orders hinges on its product capabilities. Beyond capitalizing on the current server CPU cycle, AMD's primary focus in the AI GPU segment is on the mass production progress of the MI450 series in the second half of the year.

In its outlook for the MI450 series, AMD plans to deeply integrate it with the Helios rack-mounted platform, enabling delivery from 'single chips' to 'rack-level clusters.' This directly competes with NVIDIA's Rubin architecture and aligns with the current mainstream demands of large-scale CSPs.

AMD has already secured customers such as OpenAI, Meta, and Oracle. The mass production progress of the MI450 will directly impact delivery performance for these customers.

2.2 Client Business

AMD's client business achieved revenue of $2.89 billion in the first quarter of 2026, a 26% year-over-year increase, outperforming market expectations ($2.7 billion). The growth was primarily driven by AMD's increasing market share in the PC segment at the expense of Intel.

Combining industry data, global PC shipments in the first quarter of 2026 reached 65.6 million units, a 4% year-over-year increase. Meanwhile, AMD's client business achieved a 26% year-over-year increase. In comparison, Intel's client business grew by only 1.3% year-over-year.

Comparing the growth rates of the three, Dolphin Research believes that even amid a sluggish PC market, AMD is poised to outperform the market through its product competitiveness.

2.3 Other Businesses

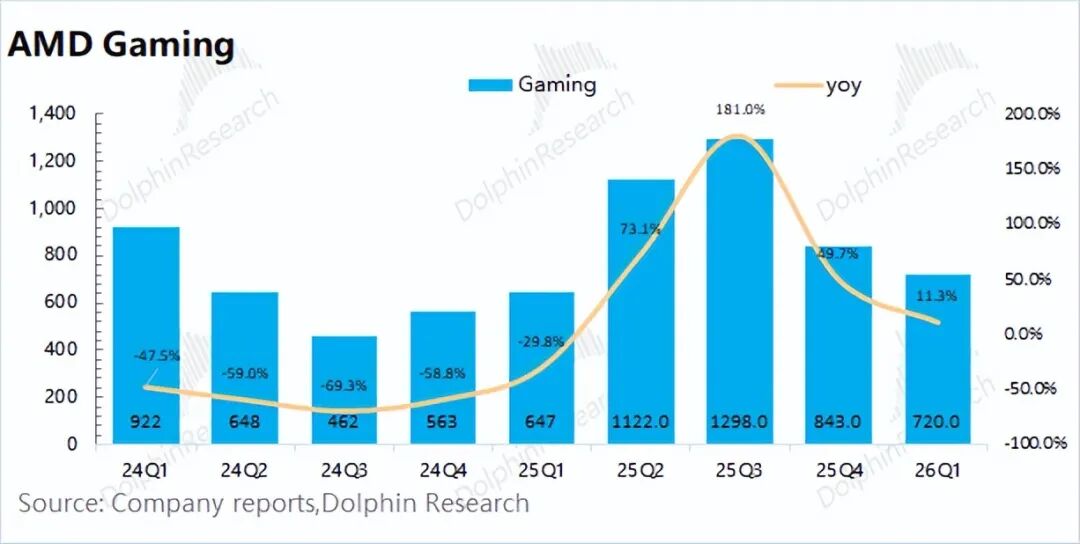

1) Gaming Business: AMD's gaming business achieved revenue of $720 million in the first quarter of 2026, an 11% year-over-year increase.

Details: ① Gaming GPUs: The Radeon RX9000 series saw year-over-year growth; ② Semi-Custom Business: Expected to decline year-over-year due to the console cycle, now in its seventh year in 2026, a transitional period for product upgrades. Coupled with rising component costs such as storage, a more pronounced decline in the gaming business is expected in the second half of the year.

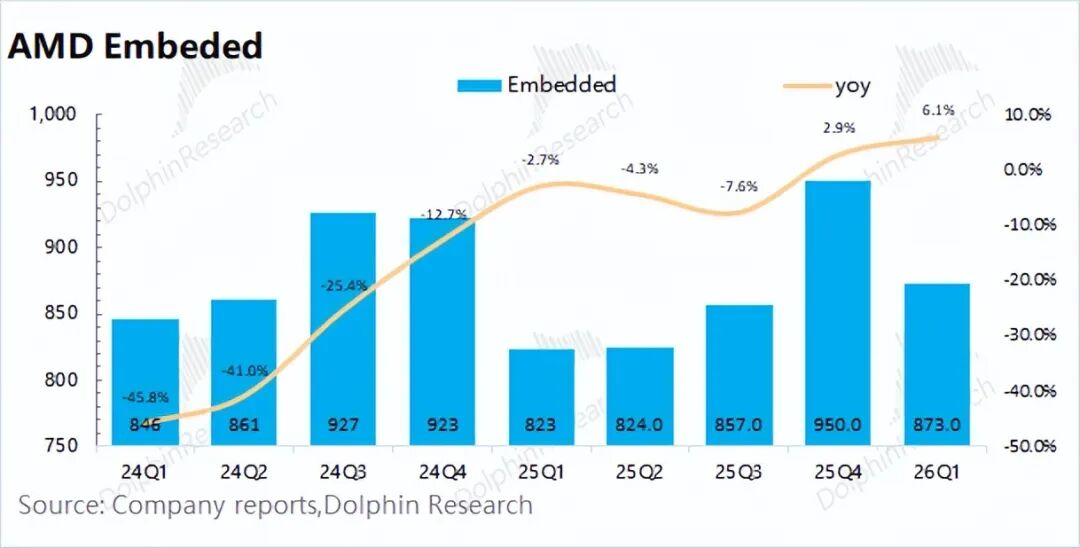

2) Embedded Business: AMD's embedded business achieved revenue of $870 million in the first quarter of 2026, a 6% year-over-year increase, driven by test and measurement, simulation, aerospace and defense, communications, and x86 embedded products.

AMD's semi-custom business continues to expand in data centers and communications, evolving from an FPGA-focused portfolio to adaptive embedded x86 and semi-custom solutions, significantly broadening AMD's total addressable market.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Authorization is required for reprinting.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general viewing and data reference by users of Dolphin Research and its affiliated entities. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or particular needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referencing the content or information in this report are undertaken at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, solicitations, or endorsements of relevant securities or related financial instruments. The information, tools, and data contained in this report are not intended for or intended to be distributed to jurisdictions where distribution, publication, provision, or use of such information, tools, and data conflicts with applicable laws or regulations, or where Dolphin Research and/or its subsidiaries or affiliates would be required to comply with any registration or licensing requirements in such jurisdictions, nor to citizens or residents of such jurisdictions.

This report merely reflects the personal viewpoints, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated entities.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or distribute in any form any copies or reproductions, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!