Who Would Be Most Panicked by Doubao's Subscription Fees?

05/08 2026

05/08 2026

651

651

Over the past two years, there has been an unspoken consensus in China's AI industry: grow the user base for free first, then talk about monetization.

This is not surprising. The successful playbook of China's internet industry over the past two decades has largely followed this formula: acquire traffic for free, then monetize through advertising, e-commerce, or value-added services. From search engines and short videos to mobile payments, this approach has been the norm.

However, in early May, Doubao updated its paid subscription service statement on the Apple App Store page, planning to introduce three tiers of paid versions: Standard at 68 RMB per month (688 RMB annually), Enhanced at 200 RMB per month (2,048 RMB annually), and Professional at 500 RMB per month (5,088 RMB annually), while retaining a free basic version.

Doubao, with 345 million monthly active users and ranking first among domestic AI applications, has started charging.

Behind this move lies mounting cost pressures. Doubao's daily token consumption has surged to over 120 trillion, a 1,000-fold increase in two years. ByteDance's annual capital expenditures, exceeding 100 billion RMB, are increasingly funneled into AI computing power.

The larger the user base, the stronger the model capabilities, yet costs continue to rise. The logic of the past internet era—where more users meant more profits—has flipped in the AI age to "more users, more burn."

I. A 1,000-Fold Cost Increase, With No One to Foot the Bill

To understand why Doubao is charging, let's look at some data. In March 2026, Doubao's large model processed over 120 trillion tokens daily, a 1,000-fold increase in less than two years since its launch. Three months ago, this figure was half its current level.

Tokens are the fuel for AI operations.

Every message sent, image or video generated by users requires server clusters to operate at high speed, consuming electricity and degrading hardware. A 1,000-fold increase in usage means ByteDance's costs are expanding at a non-linear rate.

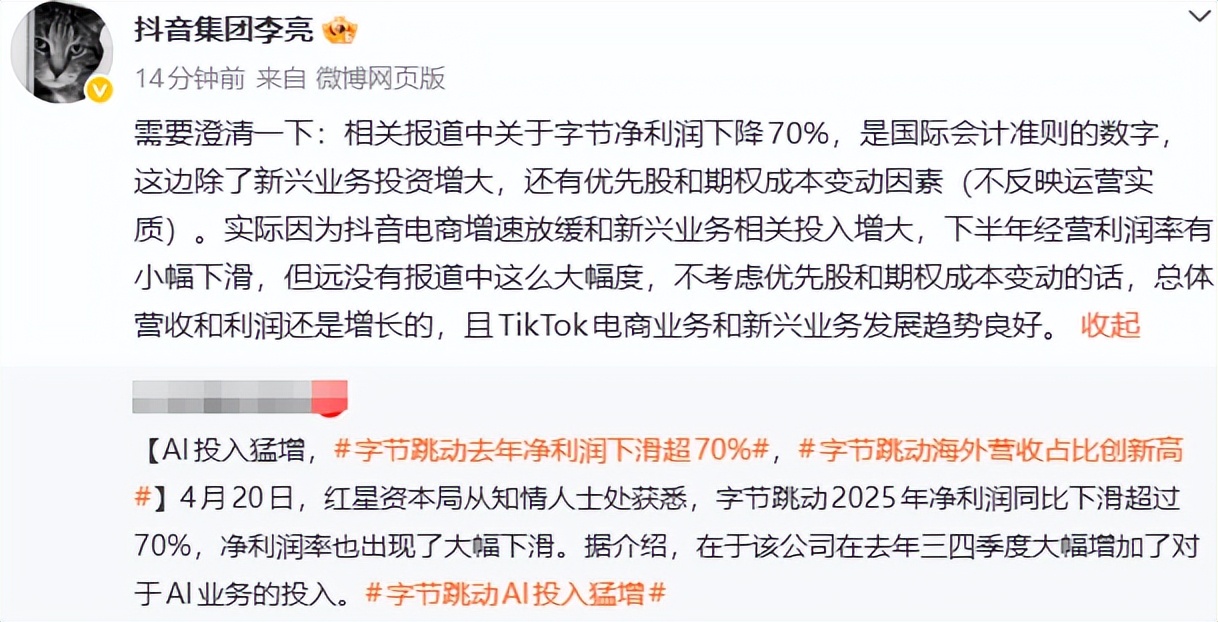

Rumors previously circulated that ByteDance's 2025 capital expenditures exceeded 150 billion RMB, with roughly 90 billion allocated to AI computing power procurement. In 2026, it planned to invest another 160 billion RMB, with 85 billion earmarked for AI chips. Reports at the time indicated a year-on-year net profit decline exceeding 70%.

Although Li Liang, Vice President of Douyin Group, clarified on Weibo that the decline was based on international accounting standards, including changes in preferred stock and option costs, and that actual operating profit margins only saw a "slight decline," the clarification itself acknowledged that "slower growth in Douyin E-commerce and increased investments in emerging businesses" had pressured operating profit margins in the second half of the year.

ByteDance is pouring more money into AI, but the more vexing issue is that AI's cost structure does not dilute with scale—quite the opposite.

Traditional internet monetization relies on a clear division of labor: platforms provide products, users contribute attention, and advertisers pay. Every second a user spends staring at a screen can be sliced, priced, and sold. This model has sustained nearly all major internet platforms for two decades.

But AI has altered the relationship between users and products. Users no longer browse; they assign tasks, such as generating reports, analyzing data, or organizing information. Tasks involve a complete processing chain with no gaps for attention—and thus no room for ads.

This means the most successful monetization formula of the past two decades has failed in the AI era.

Moreover, every new user performing a complex task represents an independent computing cost. The better the product, the more users it attracts, the higher the frequency of high-computing-demand scenarios, and the greater the total costs.

Video generation is one of the most computing-intensive AI applications today, consuming orders of magnitude more resources than text-based interactions. As such features roll out to more users, the growth trajectory of computing demand will remain steep with no short-term ceiling.

Three hundred million monthly active users are an asset under traffic logic but a liability under computing logic.

However, viewing Doubao's subscription fees solely as a sign of financial strain may underestimate another layer of intent behind the decision.

Doubao has long carried a market perception as a ByteDance-backed entertainment tool for casual chatting, not a serious productivity platform. This impression stems directly from its user acquisition strategy.

As we previously discussed in *Why Doubao: Late Start, Minimal Spending, Yet the Hottest AI*, while Tencent and Alibaba invested heavily in paid user acquisition, Doubao achieved explosive growth through "organic traffic" from Douyin creators. Many users discovered Doubao via Douyin recommendations, treating it as a free pastime rather than a productivity tool from day one.

A 68 RMB monthly fee represents a forced cognitive reset. After all, users willing to pay 68 RMB monthly are unlikely to be there just for casual chat. But this cognition (cognitive shift) can only succeed if users are willing to pay.

II. How Many Will Convert?

Doubao's 345 million monthly active users are frequently cited and form the basis for optimism about its subscription fees. The logic seems straightforward: with such a large user base, even a 1% conversion rate would yield 3 million paying users, generating over 2 billion RMB in annual revenue at 68 RMB per month.

Morgan Stanley estimates that assuming Doubao's paid conversion rate ranges from 0.3% to 3.0%, with monthly active users between 345 million and 525 million, and an average revenue per paying user (ARPPU) of approximately 98 USD, Doubao's annualized subscription revenue would range from 101 million to 1.5 billion USD.

This calculation is not wrong, but it overlooks a critical question: Who are these 300 million users?

Doubao's user growth path differs fundamentally from other domestic AI products.

Kimi's early users were acquired through intensive commercial advertising—splash screens, information feeds, Zhihu recommendations. Every user exposed to Kimi's ads underwent implicit value education: "This is a tool. It's useful. It might be worth paying for." This logic may not prompt immediate payment, but it plants a basic expectation in users' minds.

Doubao's users did not undergo this process. Its growth came from Douyin's organic traffic, pre-installations by phone manufacturers, and word-of-mouth referrals. The first thing users encountered about Doubao was never "how much this tool is worth" but "it's free, give it a try."

These two acquisition strategies represent entirely different starting points for Paid mindset (willingness to pay).

Stepping back, low paid conversion rates are not unique to Doubao; they remain an unsolved challenge for the entire AI industry.

OpenAI currently leads in consumer-facing AI monetization. Even so, as of early 2026, it had approximately 50 million paying users out of over 900 million weekly active users—a paid penetration rate of less than 10%.

What does this number signify? Even the world's most renowned, capable, and early-established AI application in terms of Paid mindset (willingness to pay) sees over 90% of its active users choosing not to pay.

Another unavoidable context is that domestic consumers have never naturally embraced paying for digital content.

Few domestic digital products have achieved genuine paid adoption, and even fewer have sustained it. Video streaming platforms took nearly a decade to scale membership subscriptions, yet many users' first instinct remains to carpool accounts or wait for free access.

Music streaming offers another example. Before stricter copyright enforcement, domestic users largely expected music to be free. To drive paid conversions, platforms resorted not to enhancing content value but to gradually restricting free access, creating inconveniences to force payment.

These precedents convey a consistent message: In the domestic market, transitioning from free to paid requires not just a good product but also time, habit reshaping, and, to some extent, design pressure that renders free options insufficient.

Doubao's current approach retains a free version while offering enhanced capabilities in paid tiers—a gentle design that does not force payment. However, the trade-off is limited conversion momentum; if the free version suffices, the paid version struggles to justify its necessity.

III. Who Faces the Greatest Discomfort After Doubao's Subscription Fees?

With Doubao, the largest AI player by user base, introducing subscription fees, what should other domestic AI companies do?

Kimi's situation is most emblematic. As the independent product furthest along in consumer-facing AI monetization, it has spent nearly two years building a paid user base—its most critical asset.

The competitive conditions are wildly uneven. Kimi is a pure AI company; every dollar of computing expenditure must be covered by subscription revenue. Doubao, backed by ByteDance, can monetize free users through advertising and e-commerce to subsidize computing costs while using subscriptions to target high-value users.

On one side stands Kimi, which must rely on subscriptions to survive. On the other stands Doubao, which can fall back on advertising and e-commerce. This is not a fair fight.

Yuanbao faces a different but equally passive predicament.

Yuanbao has 57.35 million monthly active users, less than one-third of Doubao's scale. During the 2026 Spring Festival, Tencent spent 1 billion RMB on an AI red envelope campaign. At the company's annual meeting, Pony Ma expressed direct beware (vigilance) toward Doubao's mobile assistant.

Yet Yuanbao's current awkward (awkwardness) lies in competing head-on with Doubao in the consumer AI space without Doubao's massive user base to support a tiered payment strategy. Charging too early could stifle scale growth. However, Tencent's advertising and gaming cash flows allow it to hold out.

Qianwen most closely resembles Doubao, trailing with 166 million monthly active users. QuestMobile data shows its Q1 2026 monthly active users approached half of Doubao's. Qianwen remains in a user-expansion phase, nearly doubling Doubao's scale gap. Charging prematurely at this stage would mean voluntarily slowing its pursuit.

Then there's DeepSeek.

DeepSeek is an open-source model and does not engage in consumer-facing subscriptions or direct competition in the paid market. On the surface, Doubao's subscription fees seem irrelevant to it. But precisely for this reason, DeepSeek represents the greatest potential threat to the entire Payment logic (payment logic).

The existence of open-source models fundamentally questions a premise: Why should users pay for AI? If open-source models continue closing the capability gap with closed-source alternatives, developers can build applications with nearly identical experiences on top of them, offering users free substitutes. What justifies the subscription fees of Doubao, Kimi, or ERNIE Bot?

Doubao's subscription fees truly signal a shift in industry logic.

Over the past two years, all AI products competed on who could offer more for free and grow faster. Henceforth, the competition will turn to who can better manage costs and establish a stable business closed loop (closed loop). Kimi, Yuanbao, and Qianwen each face pressures, while DeepSeek's open-source path continues compressing pricing space across the industry.

As "good enough" AI becomes increasingly free, what may truly become scarce is not model capability but the cash flow, ecosystem, and commercial systems to sustain models long-term.

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action