Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

07/03 2026

07/03 2026

490

490

Kuaishou has propelled Keling AI onto a far grander stage.

On the evening of July 2, Kuaishou Technology officially announced through the Hong Kong Stock Exchange that the spin-off financing for Keling AI—previously a topic of speculation in May—had now been finalized into a legally binding agreement. This development marks the most significant milestone in Keling AI’s journey toward capitalization since Kuaishou first confirmed on May 12 that its board was considering restructuring options. It also represents the largest financing round in the global video generation large model sector to date.

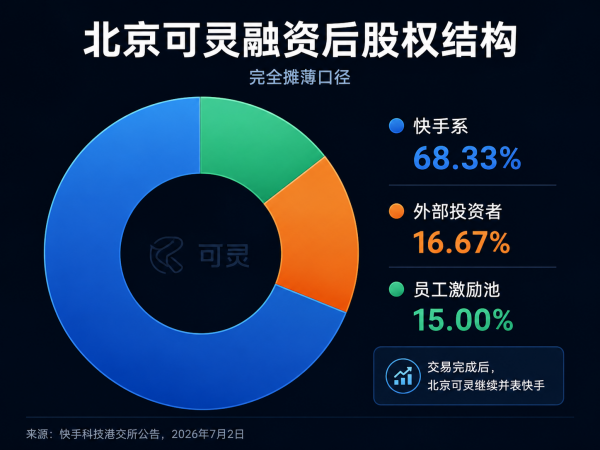

According to the disclosed subscription limits and equity ratios in the announcement, Beijing Keling’s pre-investment valuation stands at approximately $15 billion, with a post-investment valuation of around $18 billion.

With this infusion of capital, Keling AI’s path forward becomes less carefree. It must now demonstrate how a listed company can revalue its rapidly expanding AI assets, retain core technical talent through independent financing, and forge a unique identity amid competition from ByteDance’s Seedance and Alibaba’s HappyHorse.

1 · Revaluing Keling

Following the financing, if subscription limits and employee incentive plans are fully utilized, Kuaishou’s indirect stake in Beijing Keling will decrease from 100% to approximately 68.33%. Beijing Keling will continue to be consolidated into Kuaishou’s financial statements, and Kuaishou will maintain control.

Thus, the essence of this transaction lies not in a “divestiture” but in a “revaluation.”

Over the past year, Keling has emerged as Kuaishou’s most critical asset in the AI video domain. Within the group, its contributions primarily manifested as R&D investment, computational costs, and losses from innovative ventures. Post-restructuring, Keling gains an independent equity structure, external investors, and management incentives, enabling capital markets to evaluate its growth potential separately.

This is pivotal for Kuaishou. While short videos, livestreaming, e-commerce, and advertising remain its core businesses, Keling represents new avenues for valuation. Financing Keling independently opens external funding channels for its AI operations without relinquishing control, providing the market with a clear valuation benchmark.

The announcement also revealed Kuaishou’s intention to initiate Keling AI’s Hong Kong IPO process within the next 12 months, aiming to submit filing materials by early 2027. The raised funds will primarily support computational and data center construction, recruitment of core technical talent, and team incentives.

Kuaishou has designed a performance-based incentive structure for the Keling AI team. If the future IPO valuation reaches $40 billion, the team will receive substantial rewards. Within the parent company, team compensation was constrained by Kuaishou’s stock price system. Independence allows compensation to align with the value they create.

This is not mere foresight. After Keling AI’s former technical lead, Zhang Di, departed for Alibaba in August last year, he spearheaded the development of HappyHorse-1.0 in just five months. Reportedly, it temporarily outperformed both Seedance and Keling 3.0 on authoritative benchmarks, becoming a persistent concern for Kuaishou.

2 · The ‘Spillover Value’ Backed by Industry Giants

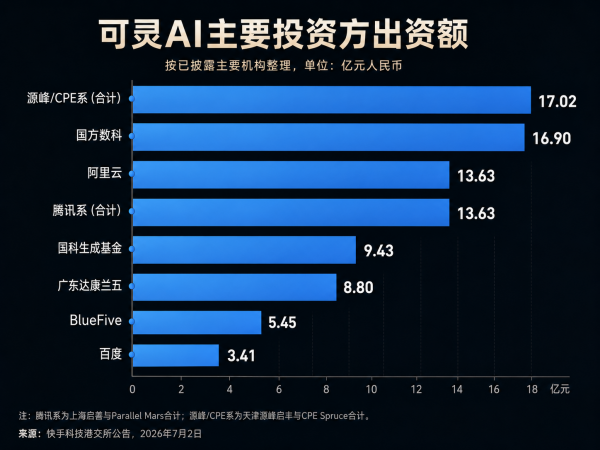

More critical information lies in the shareholder list. Tencent, Alibaba Cloud, and Baidu appear together—a rare sight. Tencent and Alibaba Cloud each invested RMB 1.363 billion, while Baidu invested RMB 341 million. Other investors include Shanghai Guofang Shuke, Yuanfeng Capital, CPE, Beijing Guoke Generation Fund, Shenzhen Hongtu, Suzhou Gongrong Jinzhi, China Internet Investment Fund, and the Beijing AI Industry Investment Fund.

This marks a coordinated entry by “industrial capital + state-owned platforms + top-tier financial investors.”

In the gateway sector of video generation large models, leading internet companies refuse to let ByteDance dominate the ecosystem alone.

ByteDance boasts Seedance, Doubao, Jianying, Jimeng, Volcano Engine, and the Douyin ecosystem. It naturally controls creator distribution, content feedback, and commercialization closures. If AI video becomes the foundational production tool for short videos, advertising, e-commerce materials, short dramas, and gaming assets, ByteDance’s advantages will amplify further.

By bringing in Tencent, Alibaba Cloud, Baidu, and a cohort of industrial capital, Kuaishou is essentially weaving a broader industrial network for Keling. It needs more than capital—more clients, more scenarios, more computational synergy, and more leverage against ByteDance’s ecosystem.

However, resource-based investments do not guarantee business orders. Keling must prove whether these shareholders can translate into actual business channels rather than mere endorsements on an investment list.

3 · The Real Pressure Lies in Repurchase Clauses

The toughest part of this announcement is not the financing scale but the repurchase rights.

According to the agreement, if Beijing Keling fails to complete an IPO by the latest listing deadline or before October 30, 2031, investors have the right to demand a repurchase of all or part of their equity. The repurchase amount includes the original investment plus an 8% annual simple interest return, minus any dividends or distributions received.

Additionally, if Beijing Keling fails to complete relevant restructuring items within the agreed timeline, repurchase arrangements may be triggered. These items include acquiring 100% of overseas operating entities, obtaining value-added telecom business licenses, and completing AI large model and algorithm filings.

This indicates that investors are not buying an AI story unconditionally. Behind the high valuation, exit paths, IPO timelines, and restructuring progress are all contractually stipulated.

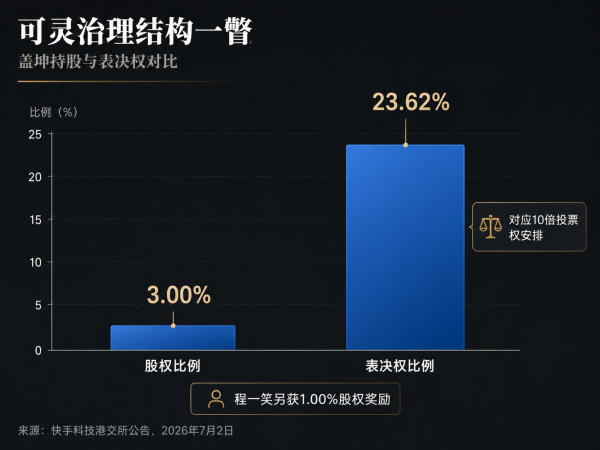

In the same announcement, Keling also established a governance structure closer to that of a pre-IPO company. Beijing Keling adopted share incentive, shareholding, and option plans, with a combined authorized limit of 15% of the expanded registered capital. Cheng Yixiao received approximately 1% in equity awards, while Gai Kun received about 3%. Notably, Gai Kun’s 3% equity carries tenfold voting rights, corresponding to a 23.62% voting power.

This setup reflects Kuaishou’s intent to govern Keling as an independent AI company: the group retains control, the core team is bound to long-term value, and investors receive exit protections.

4 · Unavoidable Rivals

While financing and spin-offs address capital and talent issues, Keling AI’s true test lies across the table.

The domestic video large model market now features a “Big Three” pattern (triopoly): ByteDance’s Seedance, Alibaba’s HappyHorse, and Kuaishou’s Keling.

ByteDance is the most resource-rich player in this race. Its Seedance 2.0, released in February, garnered global attention with its unified multimodal audio-video joint generation architecture. Its computational demands once strained even ByteDance’s own resources. ByteDance’s response was direct: a 25% increase in capital expenditures for 2026, reaching approximately RMB 200 billion—nearly eight times Kuaishou’s budget. On June 23, ByteDance unveiled its next-gen model, Seedance 2.5, at the Volcano Engine FORCE Conference, supporting 30-second single-shot native output and joint referencing of up to 50 materials, with a formal launch expected in early July—almost concurrent with Keling’s financing announcement.

Yet Keling is not defenseless. According to Orient Securities research, based on API pricing for generating one-minute videos, HappyHorse-1.0 costs approximately $14.4, Seedance 2.0 about $22.4, and Keling 3.0 around $13.4—the lowest among the three.

Goldman Sachs’ February research also noted that while Seedance 2.0 may excel in physical motion and complex action rendering, Keling AI remains competitive in visual consistency, commercial scenario adaptability, and professional creation capabilities, particularly carving out differentiated advantages in enterprise and professional user markets.

Currently, approximately 70% of Keling’s revenue comes from overseas subscriptions and enterprise API calls, pursuing a B-end-oriented route that emphasizes “deliverability” over mere technological showmanship.

Goldman Sachs also offered a relatively optimistic industry outlook. AI video generation will not evolve into a single-platform monopoly. The global market size is expected to grow roughly tenfold over the next five years, reaching approximately $29 billion by 2030.

The table is large enough for non-zero-sum competition. This may explain why Tencent is willing to bet on both in-house R&D and external investments without rushing to pick sides.

-

![]()

Rokid's Ambition and Embarrassment: 300,000 Sales Can't Support Its Ecosystem Dream

-

Are Gaming Ventures No Longer in Vogue Among Tech Titans?

-

![]()

Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

-

![]()

Valued at $18 Billion with a Five-Year IPO Plan: Kuaishou’s Kling AI Takes a Bold Leap

-

![]()

NVIDIA Launches 'Computing Power Financing'

-

![]()

Following Up on the 'Safety Net' for Intelligent Driving: Is Huawei's Strategy Astute or Perilous?

-

![]()

ICML 2026 | One Model to Unify Humans, Objects, Sounds, and Actions: OmniShow Revolutionizes Multimodal Controllable Video Generation as a Systematic Engineering Feat!

-

![]()

Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma