Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma

07/03 2026

07/03 2026

500

500

Mid-Year Review: The Escalating Difficulty of the 2026 New Energy Vehicle Market

Another year of examination season has arrived, and June is once again filled with an atmosphere of anxiety and tension. The college entrance examination, high school entrance examination, and final exams dominate social attention. For college entrance examination candidates, choosing a major becomes a pivotal decision in their lives.

However, for most new energy vehicle (NEV) manufacturers, the high-stakes challenge of car manufacturing is an ongoing battle without a finish line.

As June draws to a close, automakers have reached their mid-year summary moment. Particularly, the new energy vehicle brands, seen as industry leaders, have become indicators of the automotive market's health. Perhaps buoyed by a favorable June market, all companies completed their sales announcements on the first day of July.

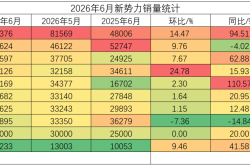

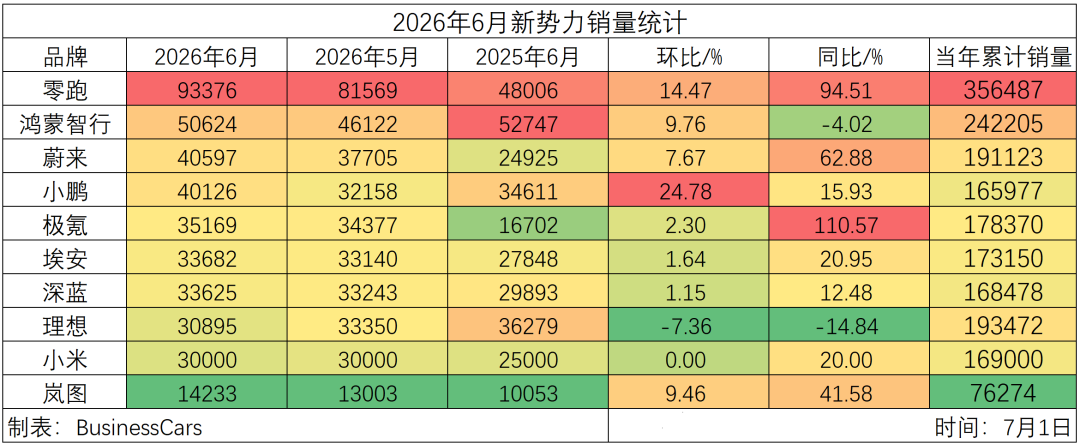

The 2026 market has proven to be quite challenging for many new energy vehicle brands. Amidst various cumulative challenges, selling cars has become increasingly difficult, with the benchmark for success rising significantly. Monthly sales of 30,000 units have become the threshold for success. From the results, less than half of the brands managed to surpass this mark.

The Academic Prodigy and the Top Performer

Unsurprisingly, Leapmotor once again claimed the top spot on the list, with 93,367 monthly sales, surpassing the half-year sales of the lowest-performing new energy vehicle brand. It maintained double-digit year-over-year and month-over-month growth.

Leapmotor's upward trajectory, which began in 2025, shows no signs of slowing down. For the market, the primary concern is when Leapmotor will achieve monthly sales of over 100,000 units. Based on its current performance, it appears poised to set a new sales milestone for new energy vehicle brands next month.

However, Leapmotor, despite its consecutive championships, is not without its worries. With cumulative half-year sales of 350,000 units, it still has a long way to go to reach its annual target of 1 million units. Although its average monthly sales are close to 60,000 units, nearly double the 30,000-unit threshold, achieving its own ambitious goals will require even greater efforts in the second half of the year.

The good news is that Leapmotor's current product lineup is nearly complete. The four major product lines, ABCD, saw additions in June. The once-mainstay C-series received a refresh, while the highly anticipated D-series welcomed its second model, the D99, filling the MPV gap in its portfolio.

For Leapmotor, channels and production capacity are now more critical than products. Channel expansion, in particular, is a bottleneck restricting further sales breakthroughs. Public data shows that by early 2026, Leapmotor had over 1,000 stores nationwide. According to its investment plan, the company aims to expand its channels by another 400 stores in 2026.

Even with 1,400 stores, the pressure on each outlet remains significant, proving that transitioning from a new energy vehicle startup to a large-scale automaker requires further accumulation and strategic planning.

As for the Harmony Intelligent Mobility Alliance, it continues to maintain a significant lead over other new energy vehicle brands. Its May sales rebounded to over 50,000 units, with cumulative half-year sales exceeding 240,000 units, inching closer to its second million-unit target.

A closer look reveals that AITO remains the primary contributor, with 30,199 units sold, forming the bedrock of its sales. However, its share within the Harmony Intelligent Mobility Alliance has declined slightly, from 73% in May to 60%, indicating the initial success of the alliance's multi-brand strategy.

Hidden within the Harmony Intelligent Mobility Alliance's sales poster is its second growth curve. The Shangjie Z7 series achieved over 10,000 monthly deliveries, becoming a new growth point and justifying Shangjie's inclusion in the alliance.

Beyond sales support, the Harmony Intelligent Mobility Alliance's determination to ascend is evident. Following the AITO M9 Ultimate Extended Edition, the Zunjie S800 also had its moment in the spotlight. At the June 25 press conference, the Zunjie S800 Grand Design Edition was priced at RMB 1.388 million, setting a new price benchmark for domestic new energy vehicles.

The press conference also unveiled the Harmony Intelligent Mobility Alliance's second MPV model, the Zunjie V800 and V680, with pre-sale prices starting at RMB 650,000, ensuring Zunjie's luxury positioning is not lonely in the market.

Of course, Seres and Arcfox require greater attention and support from the Harmony Intelligent Mobility Alliance. Despite product differentiation, without sales support, even the best strategies lack execution and harmony.

Besides the overwhelmingly dominant Leapmotor and Harmony Intelligent Mobility Alliance, NIO and Li Auto emerged as the last to cross the finish line in terms of sales performance.

Coincidentally, although Li Auto leads NIO in cumulative sales, NIO surpasses Li Auto in monthly sales by 10,000 units, making them both rivals and companions in the market. The only regret is that XPeng failed to break through the 180,000-unit admission line for significant market recognition.

Let's start with Li Auto. Its 2026 sales performance has been uneven, with hard-earned sales recovery slipping again in June, making it the only new energy vehicle brand to experience both year-over-year and month-over-month declines.

The primary issue remains sales fluctuations due to product transitions. Its battery electric vehicle lineup relies almost entirely on the i6, which, despite ranking among the top three in its category, struggles to single-handedly elevate the entire Li Auto brand.

This year's core focus for Li Auto lies in the L-series refresh. The new L8, launched on June 23, offers two versions starting at RMB 369,800. The most significant change is the shift from six to five seats, with other upgrades mirroring those of the L9, including in-house developed chips and intelligent chassis systems. These upgrades may also feature in future L7 and L6 refreshes.

During the press conference, Li Xiang presented a new perspective: the endpoint of extended-range technology is Li Auto's 5C extended-range system. Only time will tell if Li Auto's AI-embodied intelligence transformation can once again lead the new energy industry.

While AI remains a distant goal for Li Auto, internal reforms continue. Recently, Li Auto is rumored to be undergoing a new round of organizational restructuring centered around product decision-making processes. The product department will undergo mergers and splits to streamline internal decision-making and improve efficiency.

As for NIO, although it falls slightly short in cumulative sales, surpassing 40,000 monthly sales allows it to escape the embarrassment of being labeled 'NIO 30K.'

NIO's sales continue to rely on the ES8. Although the larger ES9 has been launched, the ES8 remains NIO's beacon of hope. NIO further expands the ES8's presence with the debut of a large five-seat version, continuing the success of the third-generation ES8.

Specifically, Ledo and Firefly need to step up their efforts and shoulder the sales burden sooner. Ledo, in particular, sold only 11,743 units in June, just 4,000 more than Firefly. Despite offering three models, Ledo's performance lags behind Firefly's single model, indicating a need for strategic adjustments.

Although NIO's brand sales are reaching new heights, true success hinges on Ledo's ability to step up and contribute significantly. NIO still has a long way to go before it can rest easy and claim market dominance.

While leading in sales, each brand faces its own unique challenges, and none can afford to rest on its laurels in this competitive market.

The Chase

Monthly sales figures reveal a tightly contested race among the remaining new energy vehicle brands, with differences of just a few thousand units, amounting to no more than 10,000 units cumulatively over six months. It remains difficult to determine the true rankings amidst such fierce competition.

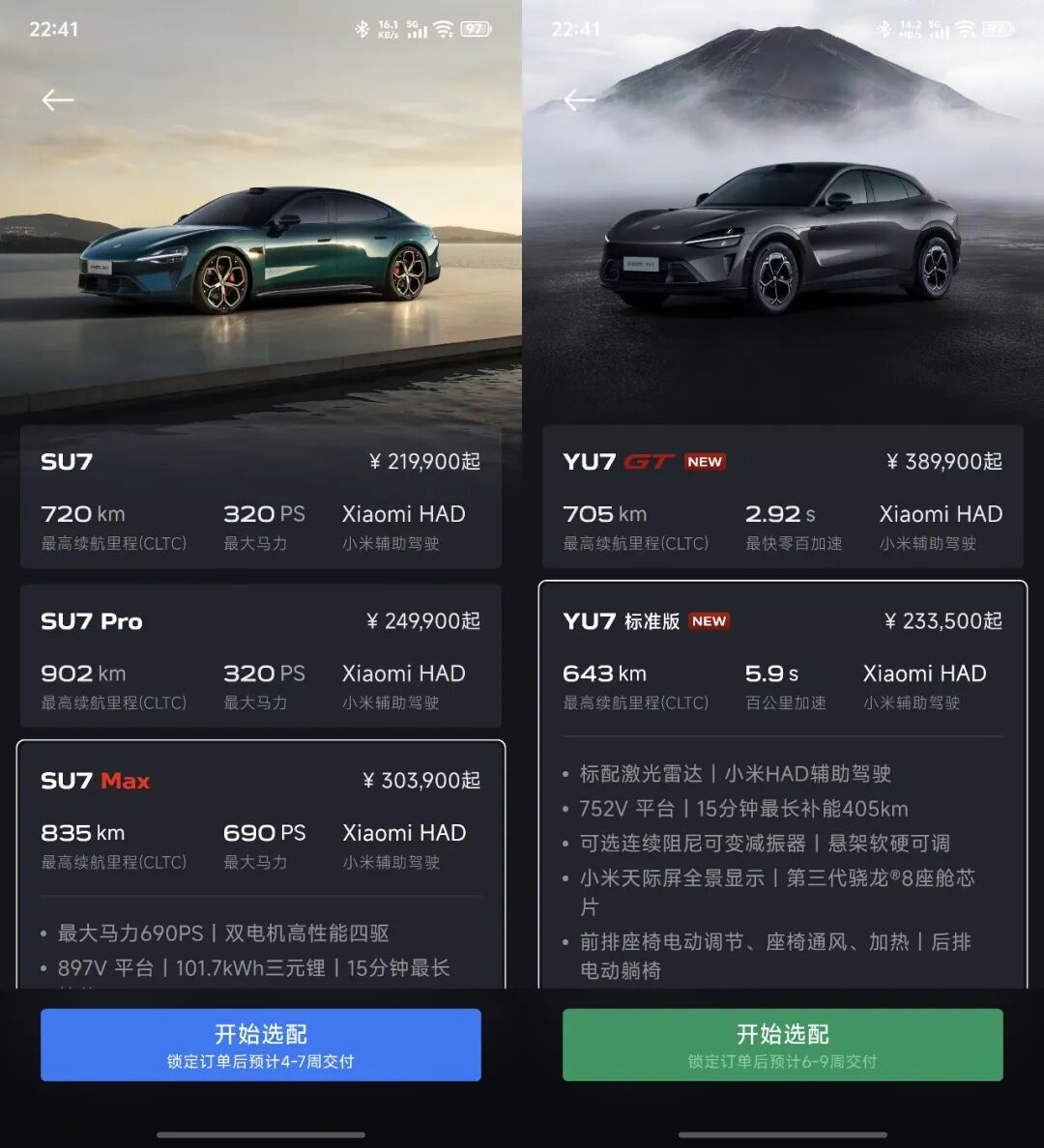

Let's start with the enigmatic Xiaomi. Its 30,000+ sales make it hard for the market to gauge its true standing, with cumulative sales of 169,000 units carrying significant uncertainty. Based on previous CPCA data, Xiaomi Auto may have surpassed 180,000 cumulative sales, crossing the admission line for significant market recognition.

What is certain is that Xiaomi's ranking slipped to fifth place or lower in June, as 30,000-plus sales still fall short of 40,000 units, which is seen as a benchmark for strong market performance.

Regarding Xiaomi Auto's sales, the only certainty is that production constraints have finally eased. According to its official website, delivery times for both the new SU7 and YU7 have been significantly shortened, with a maximum wait time of nine weeks. Additionally, a substantial number of in-stock vehicles are available, eliminating the once-frequent scenes of overwhelming demand and long waiting lists.

Meanwhile, some owners have noticed that the benefits for the standard version of the Xiaomi YU7 seem to disadvantage early adopters. Regarding this, one can only say that selling cars is tough this year—enjoy the early adoption benefits while they last, as market dynamics can change rapidly.

XPeng also broke through its bottleneck in June, achieving 40,000 monthly sales, largely thanks to the launch of the GX model. Priced starting at RMB 269,800, this large SUV, nearly 5.3 meters long, offers a significant advantage in the market, further bolstered by VLA 2.0 technology. Its sales justify its price and market positioning.

However, relying solely on the GX model is insufficient for XPeng to compete against numerous strong rivals. The company pins its hopes on the MONA L03, whose July 2 debut will significantly influence XPeng's trajectory in the second half of the year and determine its market standing.

In terms of cumulative sales, XPeng still lags behind most new energy vehicle brands. Its ability to overtake competitors hinges entirely on new models launched in the second half of the year and their market reception.

Next is Zeekr, whose cumulative sales fall just short of the threshold for significant market recognition, yet it remains hopeful of breaking through annually. Its 110% year-over-year growth surpasses all other new energy vehicle brands, even exceeding Leapmotor's 94% growth, indicating Zeekr has finally emerged from its sales slump and achieved a rebound in market performance.

However, its 2.3% month-over-month growth is negligible, signaling new sales bottlenecks in the current competitive environment. From a product lineup perspective, Zeekr has completed new model launches and facelifts. Its primary task in the second half of the year is to boost sales of existing models and capitalize on market opportunities.

Specifically, Zeekr has significant room for growth. Its June sales poster reveals over 10,000 deliveries of its shooting brake models, meaning the combined sales of the 001 and 007GT exceeded 10,000 units. While not a poor performance, it pales in comparison to the 001's past monthly sales of over 10,000 units. The growing market for shooting brakes and station wagons indicates potential for expansion, requiring Zeekr to leverage its strengths and cater to consumer preferences.

Regarding its SUV lineup, the 9X has performed well, successfully establishing itself in the RMB 500,000 market segment. Subsequent overseas expansion could further boost sales and brand recognition. The lack of sales discussion around the 8X makes it hard to speculate further, while the 7X's focus on total sales implies room for monthly sales growth and market penetration.

As a crucial part of Geely Group's new energy strategy, Zeekr, while not tasked with driving volume, must keep pace with the market to avoid falling behind and losing its competitive edge.

Aion and Deepal, both state-backed players, have performed decently, particularly with their strikingly similar monthly sales figures. This similarity underscores state-owned enterprises' current ability to match only the average performance of new energy vehicle brands in the sector. Breakthroughs require further efforts in institutional and product development to enhance market competitiveness.

Finally, Voyah, while falling short of other new energy vehicle brands in sales, deserves credit for consistently announcing monthly sales figures. Its month-over-month and year-over-year growth rates rank in the mid-to-upper echelon among new energy vehicle brands, keeping pace with the market and demonstrating resilience.

Most importantly, when compared horizontally with peer brands from the three central state-owned enterprises, Voyah stands out as the best performer, indicating sufficient accumulation over the past few years. Given time and strategic investments, Voyah may rise to the same heights as other leading new energy vehicle brands.

Reviewing the overall performance of new energy vehicle brands, they remain representatives of domestic new energy vehicles, outperforming the broader passenger vehicle market. CPCA data shows a 19.5% year-over-year decline in the passenger vehicle market over the first five months, with industry profits dropping to 3.4%. The market remains under significant pressure, highlighting the resilience and adaptability of new energy vehicle brands.

With 630 new models launched in the first half of the year, most new energy vehicle brands outperformed the market and achieved positive growth. Horizontally compared to traditional automakers, new energy vehicle brands' sales surpass those of single brands from most traditional automakers, affirming their market contributions and growing influence

-

![]()

Rokid's Ambition and Embarrassment: 300,000 Sales Can't Support Its Ecosystem Dream

-

Are Gaming Ventures No Longer in Vogue Among Tech Titans?

-

![]()

Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

-

![]()

Valued at $18 Billion with a Five-Year IPO Plan: Kuaishou’s Kling AI Takes a Bold Leap

-

![]()

NVIDIA Launches 'Computing Power Financing'

-

![]()

Following Up on the 'Safety Net' for Intelligent Driving: Is Huawei's Strategy Astute or Perilous?

-

![]()

ICML 2026 | One Model to Unify Humans, Objects, Sounds, and Actions: OmniShow Revolutionizes Multimodal Controllable Video Generation as a Systematic Engineering Feat!

-

![]()

Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma