Are Gaming Ventures No Longer in Vogue Among Tech Titans?

07/03 2026

07/03 2026

376

376

Several media outlets, including Youxi Xinzhi and Sina Technology, recently reported that Alibaba is planning to divest its gaming division, Lingxi Interactive Entertainment, for an estimated RMB 7-9 billion. Alibaba has engaged in discussions with at least five potential buyers, including 37 Interactive Entertainment, China Ruyi, Shiji Huatong, Giant Network, and two private equity firms.

This move comes as no surprise. In 2023, Alibaba pivoted its strategy to concentrate on e-commerce, international digital commerce, and cloud computing (AI + cloud). Over the past two years, divesting non-core assets and refocusing on core operations have become central to Alibaba's business strategy. Earlier, Fan Luyuan, CEO of Alibaba Digital Media and Entertainment Group, criticized Lingxi Interactive Entertainment, stating that it "never truly embodied Alibaba's DNA," hinting at the impending divestiture.

Lingxi Interactive Entertainment, deemed an insignificant "pawn," has been callously discarded by Alibaba. This mirrors the choices of other tech giants who once had grand ambitions in the gaming sector. Strategic retrenchment is a key factor, but another consideration may be the gaming industry's diminishing appeal.

Tech Giants Withdraw from the Gaming Arena

A Decade-Long Gaming Aspiration Ends in Disappointment.

Over a decade ago, China's internet sector was in the midst of an "ecosystem expansion" golden age. Tech giants ventured into each other's domains, seeking to expand their horizons indefinitely. Alibaba was the most aggressive, aiming to construct a super ecosystem encompassing consumption, entertainment, finance, and services, with e-commerce at its core. Within this entertainment realm, gaming, with its strong profit potential, held a pivotal position. Alibaba thus spent RMB 1 billion to acquire Guangzhou Jianyue Games, later rebranded as Lingxi Interactive Entertainment.

The acquisition of Lingxi Interactive Entertainment marked a crucial step in Alibaba's gaming endeavors. In essence, it brought in a team of individuals who truly "understood gaming." The success of the blockbuster game "San Guo Zhi: Strategic Edition" serves as a prime example.

Launched in 2019, "San Guo Zhi: Strategic Edition" generated over USD 1 billion in total revenue on the global App Store and Google Play within two years, ranking as the fifth-highest-grossing mobile game worldwide at the time. This title consistently featured at the top of China's mobile game revenue charts and became Alibaba's most lucrative asset in the gaming business. Regrettably, Lingxi Interactive Entertainment has failed to produce another hit.

Fan Luyuan remarked that Lingxi Interactive Entertainment "never carried Alibaba's DNA," but the crux of the issue is that Alibaba never truly mastered the art of succeeding in gaming.

ByteDance, which also made a bold foray into gaming, awakened from its gaming dream even before Alibaba. In 2023, Nuverse, which had focused on the domestic market for five years, underwent significant business contraction. Moonton Technology, targeting overseas markets, was put up for sale. Since then, gaming has been marginalized within ByteDance.

Gaming was once envisioned by ByteDance as the next revenue growth pillar. Within a year, it acquired several gaming companies, including Nuverse, and swiftly established self-developed studios such as Beijing Oasis, Shanghai 101, and Hangzhou Jiangnan. It is reported that the Beijing gaming team alone had over 1,000 employees. ByteDance had ample financial resources and, through relentless acquisitions, quickly amassed sufficient "manpower" and a rich project pipeline. However, it ultimately failed to create successful games.

"Crystal Core" initially appeared promising for ByteDance's self-developed gaming efforts, but its promising start was followed by a swift decline within three months, leading the outside world to question ByteDance's capabilities in self-developed gaming.

Pop Mart, a trendy toy giant, has also been active in the gaming market for several years. In 2016, Pop Mart established Paqu Interactive Entertainment to handle game development and operations. To synergize with its main business of IP-based trendy toys, Paqu Interactive Entertainment chose to develop its own games and launched "Dream Homeland," a casual social mobile game that combines simulation management with party gameplay. However, the game's journey has been tumultuous: early testing began in 2018, it obtained a game license the following year, but the official public test did not occur until 2024, spanning a project duration of seven years.

Just a few days ago, "Dream Homeland" announced its shutdown, and investment in the gaming business was reduced, marking the failure of Pop Mart's cross-border gaming venture.

In the internet economy, gaming, as a vast gold mine, has continuously attracted tech giants to venture into the industry. They possess ample financial resources, talent, and technology, but despite investing all these resources, they still seem unable to create successful games. Ultimately, gaming is fundamentally different from other internet businesses. Most internet businesses belong to platform-based economies, where the key is to solve efficiency issues, such as information distribution, relationship matching, and rapid fulfillment. In contrast, the core of gaming lies in production—the external expression of unique creativity and experiences.

Approaching gaming with an efficiency-driven mindset can only make games visible to users, not retain them.

Profitability in Gaming Is No Longer Guaranteed

After experiencing a trough, recovery, and slow growth, the gaming industry has once again shown signs of vitality. In 2025, the actual sales revenue of China's domestic gaming market reached RMB 350.789 billion, up 7.68% year-on-year, with a user base of 683 million, up 1.35% year-on-year. Both figures reached historic highs.

Compared to previous years, these numbers appear promising, but they offer little optimism to industry insiders. Among the growth in the gaming industry, casual games have been the biggest contributors, not mid-core or hardcore games. According to the "2025 China Gaming Industry Report," the domestic casual gaming market revenue reached RMB 53.535 billion in 2025, up 34.39% year-on-year, far outpacing the industry average. Furthermore, while the actual sales revenue of self-developed games in the domestic market showed impressive growth, it almost entirely came from a few established top-tier games.

In recent years, the penetration rate of domestic gaming users has approached its ceiling, with the total number of players peaking and new user growth plummeting, effectively eliminating the user acquisition bonus. This is not the most dangerous part; the continuous diversion of users to short videos has left gaming companies feeling helpless.

According to a 2024 internet industry research report by CICC, total online user time in the second quarter increased by 4% year-on-year, with short videos growing by 9%, while live streaming and music plummeted by 33.1% and 15.5%, respectively. Gaming consumption time decreased by 2.2%. Specifically, total gameplay time for "Honor of Kings" and "Peacekeeper Elite" decreased by 9% and 21% year-on-year, respectively, while NetEase's party game "Eggy Party" saw a 56% drop in total gameplay time.

Short videos represent a global "invasion" of gaming, live streaming, and other forms of entertainment, not just in China but overseas as well.

Matthew Ball, a renowned gaming industry analyst, directly pointed out in his "2026 State of the Gaming Industry" report that young people prefer continuously scrolling through short videos on social platforms like TikTok and YouTube or engaging in online quizzes and adult content consumption over immersive 3A blockbuster games.

Young users are being drawn away by short videos partly because games are no longer as engaging. A few flagship products from major studios dominate the top positions, offering little freshness. New games fail to break free from the formulas and frameworks of older games, lacking innovation. Behind this is an extremely stagnant market structure. For cross-border tech giants, this means becoming a new "top player" is increasingly difficult.

Why? Because there are not enough players or time. Within this limited "capacity," players have already concentrated their time on one or two games, leaving them with no more energy or financial resources to invest in other games that are both time-consuming and expensive. Unless a new game is impressive enough to replace the current top-tier games.

"Crystal Core" is an example. Based on user feedback, many said that "Crystal Core" offers a combat experience comparable to earlier Korean PC games of the same genre. Unfortunately, "Genshin Impact" had already set a high standard for players.

In the past, the vast and highly profitable gaming market attracted tech giants, who believed that as long as they could make games, they could get a piece of the pie. However, as time passed, players increasingly flocked to top-tier games, leaving a shrinking market for latecomers. Forget about getting a piece of the pie; they might not even get any scraps.

The Real Disruption May Come from AI

On one hand, gaming assets are being put up for sale; on the other hand, heavy investments are being made in AI. The simultaneous moves by ByteDance and Alibaba are seen by the outside world as a sign that these major companies are selling their gaming businesses to invest in AI. While this interpretation is not entirely accurate, it does hold some merit. Within the narrative of AI, occupying the high ground of AI technology and seeking the next super entry point are far more important than a single gaming business segment.

Moreover, they may have realized that while the gaming industry appears to be recovering in growth, it is actually at a crossroads between the past and the future, potentially facing a baptism of a new era, which brings more uncertainty to participants.

This uncertainty is first evident in the memory crisis.

Since last year, the AI wave has swept across the globe, causing a global memory shortage. Electronic products have faced massive delays in release and price hikes, with the gaming industry being one of the hardest-hit sectors. Just a few days ago, Microsoft officially announced a global price increase for its Xbox Series X/S gaming consoles, with the Series X starting at USD 750. Hardware price hikes have increased the cost of gaming for players, significantly suppressing consumer demand. At the same time, user growth and activity across the entire ecosystem may be impacted.

Gene Park, a gaming critic at The Washington Post, stated that if consumers cannot afford or access high-end technologies like sufficient memory, industry innovation will slow down.

The memory shortage is relatively temporary; the more lasting and core issue lies in the application of AI tools in the gaming industry and the boundaries of such applications. Currently, major studios, especially overseas ones, are actively embracing AI, but we have yet to see AI technology bring about efficiency transformations in game development and production. The gaming industry is already deeply divided over whether to use AI.

This division is manifested as follows: Game developers believe that AI in gaming is an irreversible trend and are accelerating its adoption. Developers argue that AI cannot provide true "differentiation" and uniqueness and are reluctant to use it. Meanwhile, the vast majority of players refuse to pay for games labeled as AI-generated. On Reddit and Steam, we see strong resistance from players toward AI. A game labeled as "AI-generated" or even one whose art style merely hints at an "AI flavor" often faces boycotts.

What appears glamorous on the surface but is hollow inside is the intuitive feeling that many people have about the content produced by "generative AI" in 2025. This applies to text, images, videos, and games alike.

However, one thing is certain: Game developers will not abandon their exploration of AI applications due to resistance. This means that commercial interests, philosophical changes, and consumer behavior will intertwine and conflict for a long time to come. Whether this will push the gaming industry into a more freely innovative state or a state that "kills" innovation is worth pondering for industry insiders.

Of course, this seems irrelevant to the tech giants that have sold off their gaming assets. Facts have proven that the gaming industry still needs people who truly understand gaming.

-

![]()

Rokid's Ambition and Embarrassment: 300,000 Sales Can't Support Its Ecosystem Dream

-

Are Gaming Ventures No Longer in Vogue Among Tech Titans?

-

![]()

Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

-

![]()

Valued at $18 Billion with a Five-Year IPO Plan: Kuaishou’s Kling AI Takes a Bold Leap

-

![]()

NVIDIA Launches 'Computing Power Financing'

-

![]()

Following Up on the 'Safety Net' for Intelligent Driving: Is Huawei's Strategy Astute or Perilous?

-

![]()

ICML 2026 | One Model to Unify Humans, Objects, Sounds, and Actions: OmniShow Revolutionizes Multimodal Controllable Video Generation as a Systematic Engineering Feat!

-

![]()

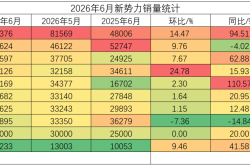

Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma