Nowadays, iPhone Buyers Might Feel the Most Embarrassed

04/23 2026

04/23 2026

485

485

Source | YuanSight

As of now, domestic smartphone makers have mostly rolled out their flagship offerings for the first half of 2026.

Generally, the pricing trend for this batch of domestic flagships is on the rise, with some high-end and foldable models firmly positioning themselves in the RMB 10,000 price bracket, significantly narrowing the price gap with Apple smartphones.

Beyond flagship models, most brands have also raised prices for some mid-range and budget offerings due to less flexible cost structures.

Several factors are driving this trend, including surging memory chip prices, increased costs for advanced manufacturing processes, escalating AI hardware expenses due to greater component usage, and manufacturers' strategies to position their products as premium. This is exacerbated by product homogenization and prolonged replacement cycles.

It is clear that after more than a decade of efforts to position their products as premium, the domestic smartphone industry seems to have finally broken free from the low-price competition trap. However, the current scenario may not be what major brands truly desire, especially given their limited bargaining power at the upstream supply chain level.

Nonetheless, a new competitive landscape has emerged. Apple and Huawei, two brands with relatively stable positions in the premium segment, are further mitigating upstream price hikes by relying on local suppliers, premium product portfolios, and supply chain management capabilities. Meanwhile, other brands still need to strike a more stable balance between costs and pricing.

01

Price Hikes Driven by Upstream Costs

Following this wave of smartphone price increases, it can be said that there will be no more top-tier flagships priced below RMB 5,000, and even the RMB 4,500-5,000 range will be considered secondary flagship territory.

However, this is not entirely by choice for manufacturers. Not long ago, Wei Siqi, General Manager of Xiaomi's China Marketing Department, stated on her personal Weibo account that the company had already taken various measures to offset the terminal pricing pressure caused by rising memory prices. However, the magnitude and persistence of this round of memory price increases far exceeded the company's initial projections and are now beyond controllable limits.

Source: Wei Siqi's personal Weibo

In response, Lu Weibing, President of Xiaomi Group, also acknowledged that the intensity of this round of memory price increases indeed far exceeded expectations, with prices for the same memory version surging nearly fourfold compared to Q1 of the previous year... necessitating minor price increases or a return to original pricing for some models.

Clearly, this round of price pressures primarily stems from the upstream.

Third-party agency Counterpoint Research predicts that in the second quarter of 2026, the prices of mobile-grade LPDDR4/5 will reach nearly three times the levels seen in the third quarter of 2025, reflecting unprecedented supply constraints. Additionally, memory chip shortages, rapid inflation in component prices, and structural vulnerabilities among low-end OEM manufacturers will not only impact 2026 data but also prolong the downturn into 2027. Recovery is not expected until late 2027, when new memory production capacity comes online.

Furthermore, Counterpoint Research also analyzes that the market will experience a significant downturn in 2026, with shipments expected to decline by 12.4% year-on-year, marking the most severe annual contraction on record.

In addition to increased BOM costs due to rising memory and chip prices, amidst ongoing product homogenization, brands continue to enhance features such as imaging and battery life, further driving up product prices.

"Recently, for some of our new products, to improve effects in areas like lens zoom, the BOM costs are even higher than those of our competitors," revealed a source from a leading domestic smartphone brand to YuanSight. They also stated that despite the current industry-wide price increases, smartphone manufacturers still have to absorb upstream cost pressures, thereby sacrificing gross margins.

Counterpoint Research points out that in response to market trends, rising component costs have driven up retail prices, affecting both old models and the initial pricing of new models. This trend is expected to keep the Chinese smartphone market under significant pressure in the second quarter. However, high-end smartphones are showing resilience, with brands driving replacement demand through breakthrough imaging hardware, foldable screens, and AI agents.

02

Some Opt for Counter-Strategies

From multiple perspectives, the upcoming prolonged period of upstream cost increases will inevitably impact smartphone manufacturers' pricing, sales volumes, and even profitability.

According to Counterpoint Research data, in the first quarter of 2026, Chinese smartphone shipments declined by 4% year-on-year. This decline was primarily attributed to the high base effect from last year's government subsidy policies and this year's cost increases.

Of course, some have adopted counter-strategies amidst this wave of price hikes. After all, brands with stronger supply chain management capabilities and larger shipment volumes have more room for adjustment amid rising memory prices and a saturated market.

In the second half of last year, Huawei announced price reductions for its Mate 80 series, with the standard version's starting price lowered by RMB 800 and the Pro version by RMB 500. Early this year, Huawei again officially reduced prices for older models, with the foldable Mate X6 seeing a direct price cut of RMB 2,000, and the Mate 70 series and Pura 80 series experiencing maximum price reductions of RMB 1,800 and RMB 1,500, respectively.

Additionally, at the recent Pura series and full-scenario product launch event, Huawei released the Pura 90 series, with the standard version's pricing remaining unchanged from the previous generation. The 12GB+256GB and 12GB+512GB versions of the Pro model were both reduced by RMB 1,000 compared to the previous generation.

Source: Huawei Official Online Store

Apple has also taken similar actions. In the second half of last year, amid sales pressure, the entire iPhone Air series saw direct price reductions of RMB 2,000. The iPhone 17 standard version, despite increased storage, did not see a price increase. Even before that, some of its specifications were eligible for government subsidies.

The effects of these adjustments are evident.

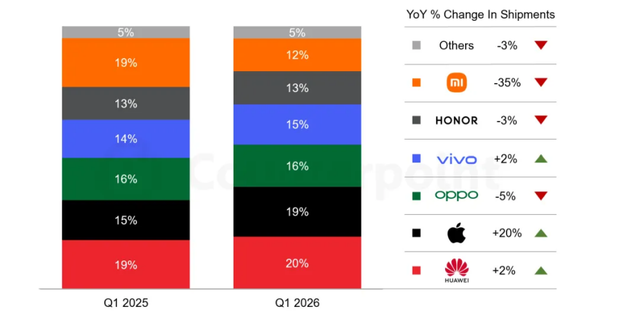

Counterpoint Research data shows that Huawei led the Chinese smartphone market in the first quarter of 2026 with a 20% market share, reaching its highest level since the fourth quarter of 2020. Against the backdrop of soaring global memory prices, Huawei's strategy of relying on local suppliers provided a good cost buffer.

Source: Counterpoint Market Monitor Report

Additionally, leveraging the continued strong performance of the iPhone 17 series, promotional price reductions, and government subsidies, Apple ranked second in the Chinese market in the first quarter, with shipments increasing by 20% year-on-year, the highest growth rate among the top six brands.

Counterpoint Research believes that Apple, with its premium product portfolio and strong supply chain management capabilities, is widely considered the manufacturer best positioned to cope with the current global memory price hikes. In the short to medium term, Apple is more likely to absorb cost pressures internally and further expand its market share.

Previous media reports have indicated that amid the global memory chip supply shortage and soaring prices, Apple has adopted an extremely proactive supply chain strategy, acquiring available mobile memory chips in the global market at high prices.

In January this year, Tianfeng International analyst Ming-Chi Kuo analyzed that amid the volatile memory chip market, Apple has the ability to maintain stable terminal product prices by absorbing memory cost increases and sacrificing some profit margins, thereby expanding its market share. It can later compensate for hardware profit losses through its high-margin services business.

03

True Head-to-Head Competition

Over the past decade, domestic smartphone brands have been committed to positioning their products as premium, with their flagship products rising from the RMB 3,000 price range to the current RMB 7,000-8,000 segment, and even reaching the RMB 10,000 range, reshaping their premium image.

Additionally, as domestic brands have caught up with or even surpassed Apple in software experience, signal strength, imaging, battery life, charging, and localized features, their high-price strategies have been supported, and consumer acceptance has increased.

This is also an inevitable choice for brands to improve profit margins, repair gross margins, and cover R&D expenses amidst long-term fierce competition.

Even so, for a long time previously, except for Huawei, the domestic camp had a certain price gap with Apple. In other words, even as domestic flagship smartphones became increasingly expensive, there was still a certain price and user segmentation between the two camps.

Under such circumstances, Apple, Huawei, as well as Xiaomi, OPPO, vivo, and Honor, all achieved relatively stable growth in the Chinese market amidst continuously growing market demand.

By 2026, the premiumization journey of domestic brands has entered another watershed, with their product pricing further venturing out of their comfort zones and directly competing with Apple. However, they still face numerous challenges against opponents wielding upstream bargaining power and brand premium advantages.

On one hand, after more than a decade, Apple's established premium perception in the smartphone sector remains firm, and its system fluidity holds a significant advantage. Meanwhile, compared to same-generation products, iPhones generally have higher resale values than domestic brands. Against the backdrop of prolonged consumer replacement cycles, users will place greater importance on this long-term value.

According to data released by Counterpoint Research in March this year, consumer replacement cycles have extended to over four years.

On the other hand, a current pain point for some domestic brands' pricing systems is the frequent price reductions of their high-end terminal products. In recent years, it has often been observed that some flagship smartphones see direct or indirect price reductions by channel partners just two to three months after launch.

Amidst prolonged replacement cycles, consumers' wait-and-see mentality may become even stronger.

In fact, over the past many years, to reduce upstream costs and enhance product premiumization and competitiveness, domestic smartphone manufacturers have been making efforts, including developing in-house chips, memory, and imaging sensors to reduce reliance on external procurement, while strengthening differentiated experiences in fast charging, signal strength, imaging, and localized features, forming advantages that Apple cannot replicate in the short term.

A decade ago, amidst memory and other configuration competitions initiated by smartphone manufacturers, upstream product price increases for memory chips and other components also triggered a wave of BOM cost adjustments.

The difference is that during the previous industrial chain adjustment, in addition to Apple, brands like Huawei, Xiaomi, OPPO, and vivo gradually absorbed market share from brands like Gionee, ZTE, and LeEco. The former continued to enhance their scale effects through increasing shipments and gradually entered the ranks of first-tier brands, while the latter either began to decline or completely exited the market.

Nowadays, the growth of the smartphone industry has hit a ceiling, entering an era of stock competition. The current domestic smartphone market has already formed a landscape of a few giants facing off. After losing the buffer zone formed by small and medium-sized brands, leading brands have reached a point where they must truly face direct competition.

Some images are sourced from the internet. Please notify us for removal if there is any infringement.

-

![]()

"3D Vision Pioneer" Grapples with Internal Strife: $120 Million in Share Reductions Offset by $147 Million Private Placement

-

![]()

The domestic auto sales have declined so much that dealers who can't hold on have started closing stores en masse

-

![]()

Five Brands Team Up with Huawei: Will Dongfeng Still Pursue Independent R&D?

-

![]()

The Large Six-Seater SUV Market: Overhyped and Overrated

-

![]()

The Smart Driving Blue Light: Urgent Need for Rectification

-

![]()

Would OpenAI Be Fascinated by Anthropic’s Concepts?

-

![]()

Tencent: Few Great Queries, Yet Possessing the Ultimate One

-

Does DingTalk Need Revolutionaries or Reformers?