Average Pricing Rivals Apple and Samsung: realme’s Pause in China Fuels OPPO’s Strategic Advance

07/17 2026

07/17 2026

547

547

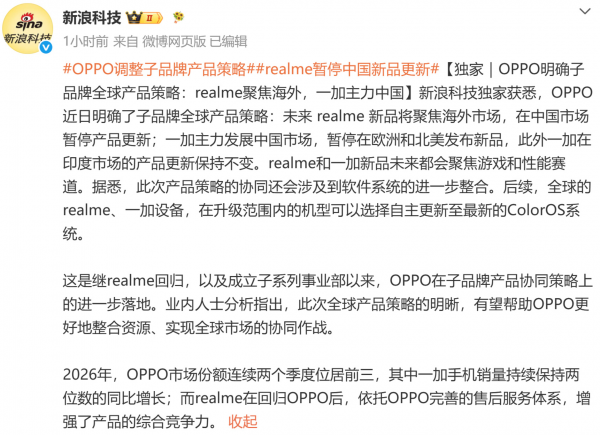

On July 16, OPPO unveiled a significant announcement regarding the adjustment of its global product strategy for sub-brands, an announcement that caused only a minor stir in the industry, contrary to what might have been expected.

This muted response might not stem from the insignificance of the matter—realme's temporary withdrawal from the Chinese market and OnePlus's decision to halt its European and U.S. launches to concentrate on China and India, both of which involve reshaping their global market presence—but rather because these strategic directions had already been hinted at and validated by data and prior adjustments over the past six months, leading to relatively rational expectations among stakeholders.

As early as January of this year, realme officially rejoined the OPPO ecosystem. At that time, the prevailing external assessment was that, with the smartphone market entering a phase of fierce competition for existing users, the return of sub-brands to their parent companies for collective strength represented a "strategic retreat."

However, when examining OPPO's subsequent market performance, this conclusion appears to be turned on its head.

OPPO's global ASP (average selling price) reached $284 in 2025, ranking third only behind Apple and Samsung. This figure underscores that OPPO is not relying on low prices to secure market share but is firmly establishing itself in the mid-to-high-end price segment.

During the same period, OnePlus experienced a 44% growth in sales in the Chinese market, with an additional 27.4% year-on-year increase entering 2026, ranking first in the industry for growth rate.

After realme's reintegration into OPPO, after-sales service, supply chain management, and distribution channels have all been shared, enhancing its product competitiveness in overseas markets rather than diminishing it.

The rationale behind this adjustment now seems straightforward.

realme has been consistently investing in the Chinese market for seven years. Xu Qi stated in his open letter this time that "learning to focus requires more courage than continuing with inertial advancement," a sentiment that is not purely emotional.

In the Chinese market, many online channel products have seen their profit margins dwindle to near zero amid soaring storage prices.

Meanwhile, realme's brand recognition and distribution efficiency in India, Southeast Asia, and Latin America far outweigh its prospects of continuing to compete with peer sub-brands domestically for a few percentage points of shipment volume. Redirecting realme's resources overseas and focusing more on gaming and performance segments is a highly rational move.

OnePlus's journey is more widely recognized; it has successfully carved out a niche as a "performance flagship" in China. As of early July this year, domestic activations of the OnePlus 15 exceeded 800,000 units, while the Ace 6 approached 1.1 million units. Therefore, halting releases in Europe and the U.S. to invest resources in the domestic market and maintain a foothold in India, while pursuing a performance-oriented track to differentiate from the main brand OPPO, is a sound decision based on ROI that also minimizes user confusion.

This adjustment in product collaboration strategy also mentions that subsequent realme and OnePlus devices globally within the upgrade scope can choose to update to ColorOS autonomously.

This signifies that the three Android custom systems previously maintained internally by OPPO—ColorOS, OxygenOS (overseas version, previously known as HydrogenOS in China), and realme UI—will move towards unification.

R&D manpower and budgets previously spread across three directions will now be concentrated on a single pivot, benefiting all product lines.

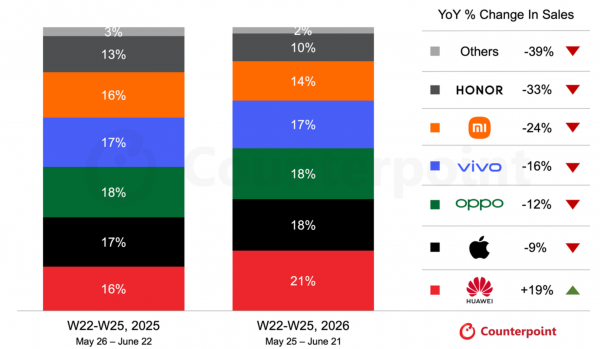

Data also supports market expectations. During the 2026 New Year period, OPPO's sales grew by 32.4%, compared to the overall market growth of 16.2%; in the ¥2,500-to-¥4,000 price segment, it surged by 60%, ranking first in market share. During the 618 shopping festival, OPPO ranked among the top three alongside Huawei and Apple with an 18% share.

Amid rising storage costs and widespread industry "downscaling to preserve profits," the Reno16 is a rare model that has bucked the trend by upgrading specifications. Making such an upgrade at this critical juncture when the entire industry is under pressure requires supply chain leverage, scale, and flexible R&D resources allocable across multiple product lines—benefits unlocked only through sub-brand collaboration.

Furthermore, OnePlus and realme previously overlapped in their domestic market niches. Now, with realme shifting its focus overseas and OnePlus continuing to deepen its domestic presence, user profiles, channel logistics, and pricing strategies across both brands have been streamlined.

OnePlus's 44% growth in 2025 and its industry-leading 27.4% growth rate in 2026 both occurred after it clarified its "performance flagship" strategic positioning. Resources are now invested more decisively, product definitions are more focused, and user perception is clearer.

Leveraging OPPO's global after-sales service network, realme users now enjoy significantly improved repair coverage—a practical advantage for a brand that already offers highly competitive products.

Thus, the main brand OPPO stabilizes the mid-to-high-end market, OnePlus caters to performance enthusiasts domestically, and realme leverages its "Dare to Leap" brand recognition overseas to capture incremental markets. Tasks that previously required three separate systems and channels to handle independently can now be optimally configured within a single ecosystem.

-

![]()

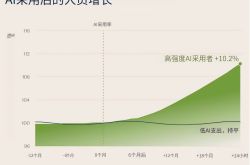

A16Z's Latest Insight: 80% of Tokens Are Idle; Managing AI Is the Next Trillion-Dollar Opportunity

-

![]()

Average Pricing Rivals Apple and Samsung: realme’s Pause in China Fuels OPPO’s Strategic Advance

-

![]()

Casarte Holds the Fort, COLMO Catches Up, Samsung Exits: Who Will Have the Last Laugh?

-

![]()

Striving to Lead in New Energy: Anhui's Challenge to Overcome the 'Hefei vs. Wuhu' Rivalry

-

![]()

Four Anhui Pioneers: Two Decades Shaping China’s Auto Industry

-

![]()

Important to Observe: BYD Surges 20% Against Market Trend in July, Will It Reclaim the 1 Trillion Yuan Mark or Soar Even Higher?

-

![]()

Autonomous Driving Enters the Second Half: ByteDance Enters the Field, NVIDIA Restructures, and the First IPO Emerges

-

![]()

Service Takes Center Stage: A 2026 Mid-Year Analysis of BBA Reputation Index