Li Auto's Last Stand: MEGA Recall, L Series Stagnation, Can Billion-Dollar R&D Secure Its Future?

12/09 2025

12/09 2025

568

568

By Haishan

Source: Bowang Finance

Li Auto is facing its toughest challenge since its inception.

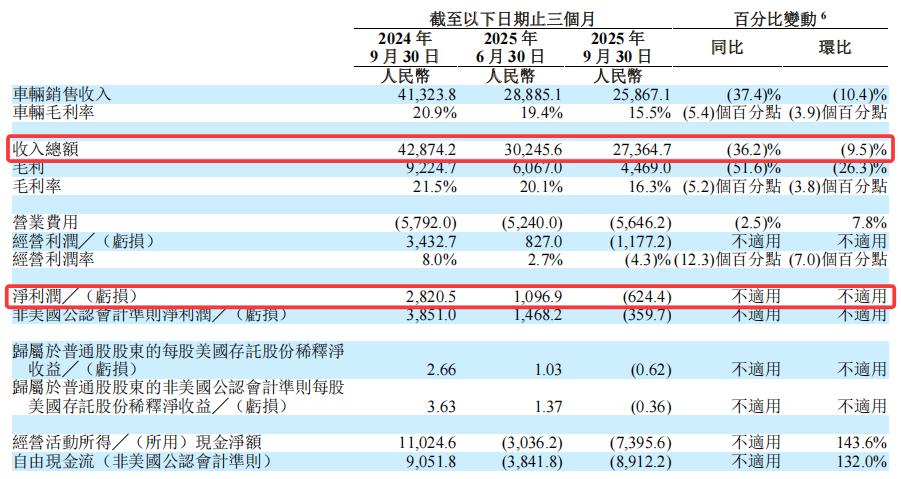

Recently, Li Auto (02015.hk) released its Q3 financial report, showing a revenue of RMB 27.365 billion, a 36% year-on-year decline; a net loss of RMB 624 million, ending 11 consecutive quarters of profitability. Worryingly, the company expects Q4 deliveries to continue declining, down 37% to 30.7% year-on-year.

During the earnings call, CEO Li Xiang stated, 'We have faced various challenges from product cycles, public relations, supply chain acceleration, and policy changes. These factors have also impacted our deliveries and operations.' He also announced a full return to a startup model.

As a 'top student' among China's new energy vehicle makers, what dilemmas has Li Auto encountered? What will its future development trajectory be? These are worth watching.

01

Double Decline in Sales and Revenue

On November 26, Li Auto announced its Q3 results, showing a loss after 11 consecutive quarters of profitability. The financial report revealed a Q3 revenue of RMB 27.365 billion, a 36.2% year-on-year decline; profitability was bleak, turning from a profit of RMB 2.821 billion last year to a net loss of RMB 624 million.

Source: Company's Q3 Report

This starkly contrasts with the company's 2024 performance of RMB 144.5 billion in annual revenue and RMB 8 billion in net profit, becoming the first domestic new energy vehicle maker to exceed RMB 100 billion in revenue for two consecutive years.

Moreover, NIO and XPeng reported Q3 revenues of RMB 21.79 billion and RMB 20.38 billion, up 16.7% and 101.8% year-on-year, respectively, making Li Auto the only one with declining revenue among the 'new energy vehicle makers.'

Li Auto's revenue primarily comes from car sales. In Q3 2025, the company's automotive sales revenue was RMB 25.9 billion, a 37.4% year-on-year and 10.4% quarter-on-quarter decline, due to reduced car deliveries.

Data shows that as the traditional peak season for car sales, Li Auto delivered a total of 93,200 vehicles in Q3, a 39.0% year-on-year decline. Meanwhile, NIO, XPeng, and Leapmotor delivered 87,000, 116,000, and 173,900 vehicles, up 40.8%, 149.3%, and 101.77% year-on-year, respectively.

Source: Company's Q3 Report

Previously, Li Auto had lowered its 2025 sales target from 700,000 to 640,000 vehicles. As of October, it had delivered 328,900 vehicles, with the annual target completion rate less than 60%.

Source: Yiche

Besides declining sales, the large-scale recall of the MEGA model was also a significant factor in Li Auto's quarterly loss. In late October, it proactively recalled some 2024 Li MEGA models, incurring related costs, and provisioned about RMB 1.1 billion in warranty costs in Q3, directly dragging down the gross margin.

The financial report showed that in Q3 2025, the company's gross profit was RMB 4.469 billion, with an overall gross margin of 16.3% and a vehicle sales gross margin of 15.5%; excluding recall expenses, the gross margin was 20.4%, slightly higher than the same period in 2024.

In terms of expenses, in Q3 2025, Li Auto's total operating expenses were RMB 5.6 billion, a slight 2.5% year-on-year decrease and a 7.8% quarter-on-quarter increase. Among them, R&D expenses were RMB 3 billion, with continued investment in pure electric technology and intelligent driving; sales, general, and administrative expenses were RMB 2.8 billion, a 17.6% year-on-year decrease.

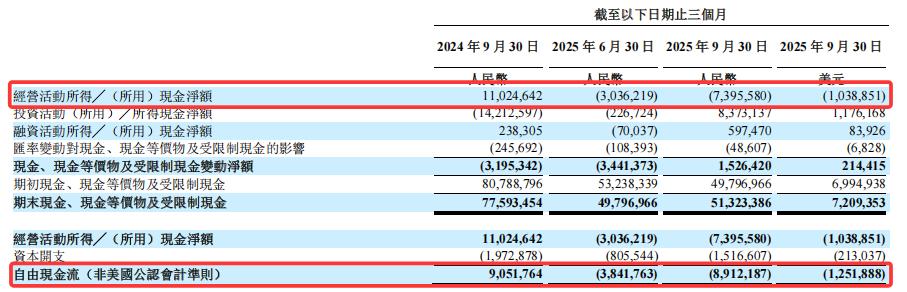

Li Auto also faces financial pressure. In Q3 2025, the company's operating cash flow deteriorated, with a net cash outflow of RMB 7.4 billion from operating activities, turning from a net inflow of RMB 11 billion in the same period in 2024, and further widening from the RMB 3 billion net outflow in Q2. The free cash flow gap widened to -RMB 8.9 billion, turning from a net inflow of RMB 9.1 billion in the same period in 2024, and widening by 134% from the -RMB 3.8 billion gap in Q2.

Source: Company's Q3 Report

As of September 30, 2025, Li Auto's cash reserves reached RMB 98.9 billion. Although short-term liquidity is not a concern, if the continuous net cash consumption is not improved, it may affect subsequent R&D investment and market expansion.

In the short term, Li Auto's performance will continue to be under pressure. The company expects Q4 deliveries to be between 100,000 and 110,000 vehicles, a 37.0% to 30.7% year-on-year decline; total revenue is expected to be between RMB 26.5 billion and RMB 29.2 billion, a 40.1% to 34.2% year-on-year decline, with deliveries and revenue still falling.

02

Reasons for the Growth Dilemma

What has caused Li Auto to fall into a temporary growth dilemma?

Extended-range technology was once key to Li Auto's market position, acting as its 'logistics provider' for long-term development, but now its 'moat' effect is weakening.

Early this year, Li Auto vaguely touched the 'ceiling' of its extended-range business. After several years of development, the extended-range vehicle market has become highly mature and severely homogenized, with narrowing gaps in technology and configuration, making 'price competition' inevitable. In May, the entire L series was refreshed and upgraded, described as the 'strongest ever' in terms of upgrade dimensions, core technology breakthroughs, and configuration downgrades, but the price remained unchanged, yet it still failed to halt the downward trend. In Q3, Li Auto delivered 93,200 vehicles, a 39.0% year-on-year decline, with both extended-range and pure electric lines struggling.

The shrinking extended-range market is a major reason for Li Auto's extended-range business setback. With the popularity of 800V high-voltage fast-charging technology and improved charging networks, the refueling experience of pure electric models has improved, rapidly diminishing the advantage of extended-range vehicles as a transitional solution. Meanwhile, competitors like Seres have diverted users with similar extended-range technology, leading to a continuous decline in extended-range vehicle sales. Since June this year, the extended-range market has shrunk for five consecutive months, with October sales down 7.7% year-on-year, and retail sales accounting for only 7.5%. Li Auto's main L series relies on extended-range technology, and the deteriorating market environment has caused a slump across the board, with cumulative sales of the L9 down more than 40% year-on-year in the first ten months, and L6 sales also significantly declining.

Li Auto's first pure electric flagship model, MEGA, sparked huge controversy in the market due to its futuristic 'high-speed train-style' design, failing to replicate its success in the extended-range market. The i8 and i6 were delayed until the second half of this year. By then, the pure electric market was highly competitive, with multiple competitors launching around the i8's release, and the i6 facing direct competition from Xiaomi's YU7 upon launch.

According to Autohome's sales statistics for October 2025, the i8 averaged only about 5,700 deliveries per month in September and October, performing poorly. More What's serious is (What's more critical is), the i6 sold well quickly after launch, securing nearly 50,000 reservations in 48 hours, but it 'internally squeezed' the higher-priced i8 and the original extended-range L series, causing internal cannibalization within the product matrix and making it difficult to form synergy.

Insufficient product technology iteration is also a problem for Li Auto. The L series has seen few major system-level upgrades in three years, relying on supplier solutions for intelligent driving, with self-developed chips and OS plans not forming closed-loop capabilities, gradually widening the gap with Tesla, NIO, and XPeng in algorithms and energy ecosystems.

On the secondary market, Li Auto's stock performance has also been unsatisfactory. Compared to the high of HKD 105.3 in late September, the stock closed at HKD 69.9 on December 5, with a more than 33% decline in over two months and a market capitalization shrinking to HKD 141.1 billion.

Source: Baidu Stock Market

03

Returning to the 'Startup' Model

Facing reality, Li Auto founder Li Xiang has conducted a 'comprehensive reflection' on the company's organization, products, and technology.

At the earnings call, Li Xiang stated, 'Over the past three years, the company has mistakenly chosen a professional manager governance model. We tried to transform into a professional manager governance system, but it made us worse.'

In terms of organizational structure, Li Auto will abandon the professional manager governance model and return to a 'startup' model. At the product and technology level, Li Auto plans to Break out of homogeneous competition (break out of homogeneous competition) by self-developing AI and hardware, transforming cars into mobile 'embodied intelligent robots.' To this end, Li Auto will launch self-developed M100 chips, shift to 3D vision, and increase investment in perception, models, computing power, and hardware.

With the extended-range business squeezed by hybrid and pure electric models and the pure electric product line troubled by production bottlenecks and quality control controversies, Li Auto sees intelligent driving as the core to breaking the dilemma. In Q3 2025, Li Auto's R&D expenses increased by 15% year-on-year, mainly for new models, product configuration adjustments, and intelligent driving technology iterations (such as the VLA Driver large model). In the long term, Li Auto plans to invest about RMB 2 billion annually in intelligent driving R&D, with cumulative investment over the next decade possibly exceeding RMB 50 billion. After entering the L4 autonomous driving stage, the annual investment threshold will be at least USD 1 billion.

However, Li Auto's bet on intelligent driving still faces challenges. XPeng's XNGP city NOA coverage has taken the lead, and Huawei's Seres ADS 3.0 has gained a reputation advantage with its lidar fusion solution. For Li Auto to catch up in the intelligent driving race, it needs to maintain high-intensity investment, posing a challenge to its cash flow.

In fact, for Li Auto, betting on intelligent driving is an inevitable choice. The extended-range business needs intelligent driving to reinforce its moat, the pure electric business needs intelligent driving to attract users, and reshaping the brand image requires intelligent driving safety endorsements.

At the call, Li Xiang stated that our technological reserves for a complete embodied intelligent system over the past three years give us confidence in our next-generation products. The era of embodied intelligent robots officially begins with automotive robots, and RMB 100 billion in revenue is just the starting point.

Source: Media Reports

Li Auto is also trying to tell a new story. On the evening of December 3, Li Auto's AI glasses, Livis, were unveiled. According to Li Auto's official introduction, Livis can naturally connect with Li Auto vehicles, enabling glasses-controlled car functions, such as opening the trunk by waking up 'Li Xiang Tongxue.' It is clear that this product is hardware for building a 'human-vehicle-home' panoramic intelligent ecosystem and a preliminary exploration towards 'wearable robots' and 'embodied intelligence.'

If automotive ecosystems are not considered, Livis focuses on image recording and voice interaction, similar to other photo-taking AI glasses on the market, integrating first-person perspective shooting and other functions, emphasizing 'hands-free' and 'constant recording.' However, Baidu's AI Glasses Pro and Kuake AI Glasses also have similar functions.

Meanwhile, internet giants generally have user ecosystems of tens of millions or even over a billion users, while automakers have a relatively limited user base. How many potential consumers Livis can reach and how many of Li Auto's approximately 1 million car owners will pay for 'human-vehicle collaboration' remains unknown.

In the recently concluded November, Li Auto's overall sales still showed no improvement. According to the latest sales data, Li Auto delivered 33,200 new vehicles in November, a 31.92% year-on-year decline, marking the sixth consecutive month of year-on-year decline since June this year.

Relying on a 'startup model' and embodied intelligence to bet on the future, its success still needs time to verify. How will Li Auto's future story unfold? We will continue to watch.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving