The Sweet Trap and Growth Ceiling of Seres

04/13 2026

04/13 2026

462

462

Author|Lightning Editor|Duke Source|Taicaijing

The new energy vehicle market is undergoing fierce reshuffling, with the landscape changing rapidly.

In this war without smoke, Seres was once one of the brightest stars. Leveraging its deep integration with Huawei, the AITO series made a splash, quickly rising to the top tier of the high-end new energy vehicle market and creating an industry miracle. However, the release of the 2025 financial report has placed Seres at a delicate turning point.

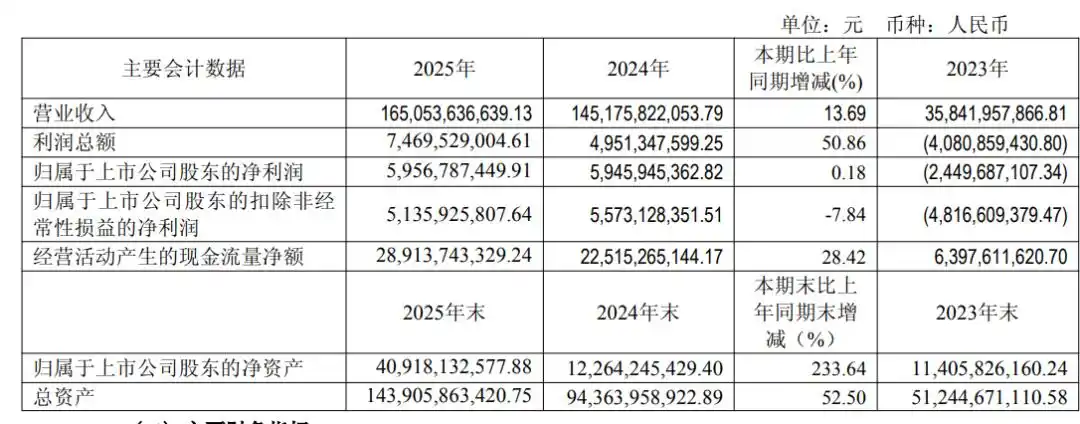

According to the financial report data, Seres' full-year revenue in 2025 was 165.05 billion yuan, a year-on-year increase of 13.7%, which appears robust (robust) at first glance but actually represents a significant slowdown—in 2024, this figure was 305.04%. Meanwhile, net profit was 5.957 billion yuan, a year-on-year increase of just 0.18%, nearly stagnant. Net profit excluding non-recurring items even declined by 7.84% to 5.136 billion yuan.

The growth momentum has clearly slowed, the hidden dangers of over-reliance on Huawei have emerged, and the unique differentiated advantages have been diluted by the "Five Brands"... Seres, once regarded as the "strongest benchmark enabled by Huawei," now finds itself in a somewhat awkward position. Facing a new landscape battle, it may no longer be able to rely on the "Huawei halo" to win effortlessly.

「 01 」Slowing Momentum: Hitting the Growth Ceiling

Ultimately, the numbers in the financial report require a deeper look beyond the surface.

The 2025 Seres financial report still appears glossy at first glance. However, a deeper dive into the data reveals hidden concerns behind this "prosperity."

First is the near-stagnation of profit growth. Seres' net profit in 2025 increased by only 0.18% year-on-year, while net profit excluding non-recurring items declined by 7.84%, which is highly inconsistent with the double-digit revenue growth. This indicates that Seres' profitability is weakening, and economies of scale have not effectively translated into profit growth.

If we extend the timeline, Seres' performance in Q4 2025 is even more concerning: As the traditional peak sales season, the fourth quarter saw revenue of 54.519 billion yuan, but net profit was only 644 million yuan—far below the 2.193 billion yuan and 2.371 billion yuan in Q2 and Q3, respectively. The phenomenon of increasing revenue without increasing profit has become more pronounced. It's like a person running—although the speed hasn't decreased, each step requires more effort than before, with energy consumption far exceeding expectations.

Second is the sluggish sales growth. In 2025, the AITO brand delivered 426,000 vehicles, a year-on-year increase of only 10.1%, far below the industry average and major competitors. It's worth noting that in 2025, the total sales volume of the high-end new energy market with transaction prices above 250,000 yuan was 2.49 million units, a year-on-year increase of about 26%. This indicates that Seres' product appeal is declining, and the traffic dividend brought by the "Huawei halo" is fading.

Finally, the asset-liability ratio remains high. At the end of 2025, Seres' asset-liability ratio reached 70.9%, although down from 2024, it is still at a high level. Meanwhile, Seres' 600,000-unit production capacity is underutilized, with depreciation expenses continuously eroding profits. This reflects the financial pressure and operational efficiency issues Seres faces during its expansion.

Seres' growth slowdown is not accidental but the result of multiple overlapping factors. On the one hand, the new energy vehicle market has shifted from high-speed growth to high-quality development, with narrowing incremental space. On the other hand, Seres' own product matrix has been slow to update, leading to insufficient product competitiveness. At the same time, Seres' over-reliance on Huawei's technology and channels has resulted in weak independent innovation capabilities. When Huawei began supporting other partners, Seres' growth ceiling became clearly visible.

「 02 」Huawei Dependence: Risk Accumulation Under Deep Integration

It must be acknowledged that the cooperation between Seres and Huawei can be described as a "perfect match" in the new energy vehicle industry.

The relationship between Seres and Huawei resembles an idol drama—a "humble" small automaker meets a dominant tech giant, and together they stage a "comeback" story. Since 2021, the two sides have upgraded from technical cooperation to a dual binding of capital + ecosystem. However, as the cooperation deepens, Seres' "Huawei dependence" has become increasingly severe, posing a hidden threat to its long-term development.

From a technical perspective, Seres relies almost entirely on Huawei for core intelligent technologies. The HarmonyOS cockpit, ADS high-level intelligent driving system, and other technologies equipped in the AITO series are all Huawei's, with Seres only responsible for vehicle manufacturing and supply chain management.

This division of labor model may cause Seres to lose its independent research and development capabilities amid the wave of intelligence. A more vivid metaphor is that Seres is like a dancer wearing Huawei's "intelligent outerwear"—although the dance is graceful, once the outerwear is removed, the core competitiveness is lost.

From a cost structure perspective, the fees Seres pays to Huawei have become a heavy burden. In 2025, Seres' procurement of core components and technologies from Huawei-affiliated companies reached 22.335 billion yuan, equivalent to approximately 52,400 yuan in "technology usage fees" per vehicle sold.

Coupled with Huawei's channel service fee of about 8% of the vehicle's selling price, each vehicle pays approximately 83,700 yuan to the Huawei ecosystem, accounting for about 21.4% of the transaction price. This means that for every 390,000-yuan AITO vehicle sold, Seres pays over 80,000 yuan to Huawei. This business model has left Seres in the awkward (awkward) position of "gaining attention but little profit."

From a channel perspective, AITO vehicles are primarily sold through Huawei's offline stores. Although this has achieved rapid expansion, it has also caused Seres to lose control over its sales channels. Huawei stores simultaneously sell multiple other brands, and when these brands launch more competitive products, AITO may be marginalized.

What Seres should be even more vigilant about is that Huawei is accelerating its expansion of automotive partnerships, establishing cooperative relationship (cooperative relationships) with multiple automakers such as Chery and BAIC, and launching new brands like Luxeed and Qijing. This has transformed Seres from the "only one" to "one of many," with its once-exclusive halo now gone.

From a brand perception perspective, consumers who purchase AITO vehicles are more drawn to Huawei than the Seres brand itself. This has resulted in a severe lack of brand value for Seres. Once Huawei launches more competitive products in cooperation with other automakers, AITO's user base may quickly erode. This means that Seres still has a long way to go to achieve true independence.

Seres is clearly aware of this. In 2024, Seres acquired the ownership of the AITO trademark for 2.5 billion yuan and invested 11.5 billion yuan to acquire a 10% stake in Huawei's Aito Automobile Technologies Co., Ltd., attempting to upgrade from a "client" to a "shareholder" in exchange for technology priority and a more stable symbiotic relationship. However, this series of moves is less about moving toward independence and more about deeper entanglement.

Seres' "Huawei dependence" is clearly accumulating risks. As Huawei's partners multiply, technological and channel resources become dispersed, and the support Seres receives may decrease. If Huawei makes strategic adjustments to its automotive business in the future or if cracks appear in the cooperation between Seres and Huawei, Seres will face significant operational risks.

「 03 」Diminishing Differentiated Advantages: Facing a Breakout Dilemma

There was a time when the AITO brand, powered by Huawei's technology, stood out in the high-end new energy vehicle market, forming a distinct differentiated advantage.

The smooth experience of the HarmonyOS cockpit, the leading performance of ADS high-level intelligent driving, and the extensive coverage of Huawei's channels quickly made AITO a benchmark product in the 300,000-500,000 yuan price range. However, with Huawei's "Five Brands" strategy and its expanding partnerships with more companies, Seres' differentiated advantages are rapidly fading, facing a situation of "wolves in front and tigers behind."

It must be seen that internal competition within the "Huawei ecosystem" is intensifying. Previously, Huawei's technological, channel, and marketing resources were tilt (tilted) toward Seres, allowing AITO to form strong brand momentum and consumer awareness. However, Huawei later became dissatisfied with a single partner and began building a more complete ecosystem matrix by cooperating with multiple automakers.

For example, brands like Chery's Luxeed and BAIC's Qijing have been launched, creating competitive relationships with Seres' AITO. These brands also equip Huawei's core technologies, share Huawei's sales channels, and even highly overlap with AITO in product positioning. It's like Huawei sending multiple teams to race on the same track, transforming Seres from an "exclusive competitor" to a "team member."

From another perspective, external competitors are rising strongly. For instance, Li Auto, with its precise positioning for family users and a dual-line layout of extended-range + pure electric, delivered over 800,000 vehicles in 2025. Brands like XPENG, Leapmotor, and Xiaomi are also squeezing AITO's market space through technological innovation or price advantages.

In addition, changing consumer demands pose challenges to Seres' differentiated advantages. As the new energy vehicle market matures, consumers are shifting from purely pursuing intelligence to a comprehensive experience, including space, comfort, range, and charging convenience. Obviously, Seres cannot lead in all aspects, which may easily divert consumer choices.

To be frank, Seres faces a breakout dilemma. It must both get rid of (break free from) over-reliance on Huawei and strengthen independent technological research and development, which requires significant capital investment and time accumulation. At the same time, Seres must cope with the dual pressures of internal and external competitors within the "Huawei ecosystem" to enhance product differentiation and market competitiveness.

More importantly, Seres needs to reshape its brand image and establish its own brand recognition. This requires Seres to form unique advantages in product design, technological research and development, and service systems, allowing consumers to recognize the Seres brand itself rather than just being a carrier of Huawei's technology. However, given Huawei's strong brand influence, the difficulty for Seres to achieve this goal is evident.

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’