Will the Electric Vehicle Era Usher in Price Increases Alongside Extra Charges for 'Intelligent Driving'?

05/07 2026

05/07 2026

416

416

Lead

Introduction

When profitability remains elusive, price hikes may become an unavoidable trend in the post-electric vehicle era, no matter the circumstances.

As 2026 unfolds and China's new energy industry enters a phase of intense competition, the new car consumer market has become increasingly attuned to the demands of Chinese users. To gain recognition at this stage, achieving near-flawless product quality has become the standard pursued by the entire industry.

So, what qualities should a qualified new energy vehicle possess today?

Externally, it should feature comprehensive coverage of energy replenishment systems, a well-established after-sales service system, and the construction of an ecosystem for the entire vehicle lifecycle. Internally, it should ensure battery safety, steadily improve charging efficiency, rapidly iterate intelligent devices, and continuously lower official prices. Essentially, any conceivable aspect constitutes the most basic qualities of a best-selling product.

This has led to the current situation where everyone in the industry is acutely aware of the intense competition but seems unable to halt the trend.

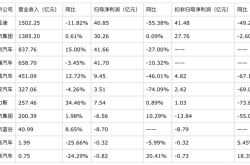

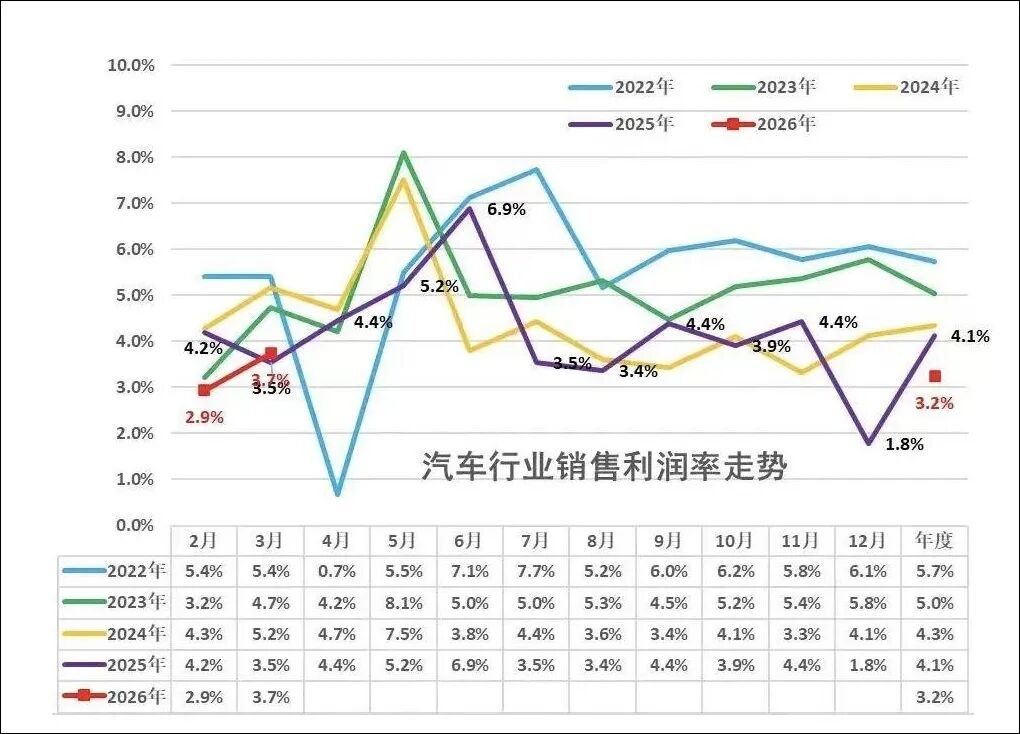

In the first quarter of this year, the difficulty of earning profits in the Chinese automotive industry became evident. According to data disclosed by Cui Dongshu, Secretary-General of the China Passenger Car Association, under the dual pressures of declining revenue and rising costs, the automotive industry's total profit from January to March was 78.4 billion yuan, a year-on-year decrease of 18%, with the sales profit margin dropping to 3.2%.

Given such meager industry profits, it is understandable that major Chinese automakers are seeking new breakthroughs out of necessity.

For consumers, the continuous decline in new car prices and the accelerating pace of technological updates are certainly positive developments. However, when most players in the industry have long been operating at a loss, chain reactions are inevitable.

In late April, companies including BYD and Changan announced with a single notice that the optional packages for high-level intelligent driving on some of their models would see price increases.

Perhaps this signals a new trend: Regardless of whether the policy is driven by the rising costs of intelligent driving hardware, Chinese automakers may become more cautious in equipping vehicles with intelligent technology. It will still take a considerable amount of time for the industry to achieve universal access to high-level intelligent driving.

Especially after consumers gradually accept the wonderful driving experience created by intelligent driving, this move is like a thunderclap in the end market, making people feel that with the end of the era for fuel-powered vehicles, the era of electric vehicle price hikes is about to arrive.

01 The Path to Universal 'Intelligent Driving' Is Long and Arduous

In the past, amid debates over the merits of fuel-powered versus electric vehicles, consumer focus on vehicle configurations centered on conventional concerns like range and energy replenishment. Until early last year, when BYD promoted the Popularize the Eye of the Gods (the popularization of the 'Divine Eye' intelligent driving system) as a catalyst, instilling in the public the notion that 'the future development benchmark for electric vehicles will hinge on intelligence,' Chinese consumers naturally began associating intelligent configurations with electric vehicles.

Although a few months later, new regulations were introduced to limit automakers' promotion of 'universal intelligent driving,' the trend of technological development remains evident. Halting the industry's disorderly development is necessary, but a blanket approach is clearly out of step with the times given the overall momentum of electric vehicle intelligence.

Regarding industry chaos, such as the sharp increase in vehicle recalls due to assisted driving system issues or the year-on-year surge in consumer complaints, we acknowledge that when the industry imposes rigid requirements on the promotion of information like the driving automation levels and system capabilities of intelligent connected vehicles—meaning that companies must not use language in the naming and marketing of combined driving assistance systems or functions that implies capabilities the systems do not actually possess, and must be truthful and comprehensive without making false or exaggerated claims—no company can break the rules.

On the other hand, as the market penetration rate of L2-level and above assisted driving systems in passenger vehicles sold in China continues to rise, Chinese consumers have become highly sensitive to whether new cars are equipped with similar functions.

Today, despite no policy relaxation on the promotion of intelligent driving, for companies, since the argument that AI defines automobiles has swept through the industry, incorporating high-level driving assistance systems into new car configurations has essentially further reinforced consumer perceptions.

Just in the past month, the number of new cars launched without similar assisted driving systems can probably be counted on one hand. In other words, in consumers' subconscious, if a new car lacks this function, it can basically be immediately excluded from purchase options.

More exaggeratedly, with LiDAR, an iconic hardware component of the system, appearing more frequently in products priced below 100,000 yuan, the number of people who would accept a 'simple' electric vehicle used solely for commuting is likely to differ greatly from previous years.

Against this backdrop, when automakers successively announce price increases for related optional configurations, the market impact is always evident. Indeed, among the brands officially announcing price hikes, the affected model versions are all high-end or already high-priced models. Additionally, since customers opting for this function are not the main force, there will not be much impact on sales at this stage.

However, looking ahead, if the costs of related hardware remain high, 'electric vehicle price hikes' seem to become an inevitable event. Even though many may argue that they can simply buy low-end models, the reality is that once 'new cars must come with high-level intelligent driving' becomes a consensus, it will inevitably lead companies to factor in the hardware costs of intelligent devices when setting prices.

In this era, automakers are engaged in fierce price wars to survive, with new car prices basically hovering around cost. Consumers have long been accustomed to the mindset of 'getting more for less' when buying cars. It remains to be seen whether, when the industry returns to rational competition, all research and development costs are reasonably allocated to each new model, and industry profits return to a healthy level from the current lows, consumers can maintain a balanced attitude toward this trend.

02 The Era of Price Hikes, Though Delayed, Is Inevitable

In the early stages of intelligent development, due to the high costs of related hardware, the price for consumers to access high-level driving assistance systems was substantial. Compared to standard model versions, optional package prices in the tens of thousands of yuan were common.

As technology advances and industry competition becomes increasingly fierce, even though the cost structure of new energy vehicle intelligent driving systems is complex, primarily covering hardware costs such as perception sensors, high-precision positioning, and intelligent driving domain controllers, as well as software costs, the costs of perception components like LiDAR and millimeter-wave radars continue to decline. This has ultimately enabled 100,000-yuan-level new energy vehicles to be fully equipped in this regard.

Under such momentum, it's no wonder Chinese users have developed strong self-judgment capabilities regarding the quality of driving assistance. However, the automotive industry has always been one that emphasizes supply-demand balance. Once this balance is disrupted, the strategy of expanding the market through low profits and high sales is unsustainable.

Entering 2026, centered around AI development, an unprecedented global competition has begun. GPUs from NVIDIA and AMD are in short supply, directly occupying the production capacity of automotive-grade high-computing-power chips. It is not uncommon for the delivery cycles of some chips to extend beyond six months, not to mention how exorbitant spot prices can be.

Outside of China, since high-level driving assistance systems are used to differentiate user groups, like users willing to pay high subscription fees for Tesla's FSD, a little extra cost may only lead to a few more complaints. In China, the mindset of those able to afford new cars priced at hundreds of thousands of yuan is likely similar.

However, in comparison, given the current market penetration rate of high-level driving assistance systems and the widespread adoption of this technology in low-priced models, users' attitudes toward 'optional intelligent driving price hikes' will undoubtedly differ significantly.

When TrendForce data shows that conventional DRAM contract prices rose by 90%-95% in the first quarter of this year, and NAND flash memory increased by 55%-60%, in the automotive industry, the cost surge resulting from the combined costs of similar hardware leaves automakers with little choice. The answer is clear.

With even cost-control experts like BYD being forced to consider 'optional high-level intelligent driving price hikes,' it seems to suggest that the era of universal access to intelligence may be drawing to a close.

Regarding cost control, it's not that no one in the industry has noticed. Li Bin, founder, chairman, and CEO of NIO, recently stated that current battery and chip costs already account for more than 50% of the total cost of intelligent electric vehicles. He hopes to further reduce costs and improve iteration efficiency by standardizing hardware specifications.

Similarly, Horizon Robotics launched China's first cockpit-driving fusion intelligent agent chip, Xingkong, with the aim of breaking the traditional architecture of separating cockpit and intelligent driving hardware through single-chip integrated design, ultimately reducing the hardware installation cost per vehicle by several thousand yuan.

Unfortunately, no amount of measures can obscure an objective fact: When automakers find it unprofitable to manufacture vehicles, and industry competition reaches a point where efforts yield little return, high-level assisted driving systems, which still hold the potential for premium pricing in the electric vehicle era, are transitioning from 'free lunches' to 'paid services,' with signs of becoming increasingly expensive. Making Chinese consumers, who have already become dependent on high-level intelligent driving, indifferent to price hikes will be extremely difficult.

In theory, once the production capacity of various hardware suppliers in the industry increases, returning to the previous phase of widespread new car price reductions is not impossible. However, with industry profits continuing to decline and old fuel-powered vehicles fading away, one must ask: Is the era of electric vehicle price hikes far off?

Editor-in-Chief: Cao Jiadong Editor: He Zengrong

THE END

-

![]()

Samsung’s Home Appliance Business: A Seemingly Inevitable Decline

-

![]()

Zhipu’s GLM-5V-Turbo ‘Crosses the Rubicon’: The Dawn of a Domestic Multimodal Agent War

-

![]()

Doubao Introduces Charges: Fewer and Fewer Purely Free Large Models

-

![]()

Q1 Financial Reports Released: Cumulative Profits of Ten Automakers Lag Behind CATL

-

![]()

Can Doubao's Paid Subscription Model Succeed?

-

![]()

Understanding China Through DeepSeek's Triple Leap in Valuation

-

![]()

Samsung Home Appliances Exit China: A Strategic Withdrawal Rather Than a Forced Retreat

-

![]()

The Inseparable Dilemma of Gasoline and Electric Vehicles: A Challenge for New Car Sales