The Inseparable Dilemma of Gasoline and Electric Vehicles: A Challenge for New Car Sales

05/11 2026

05/11 2026

384

384

Introduction

You Can't Have the Best of Both Worlds

Have you ever noticed this issue? In China's new energy vehicle market, penetration rates, sales, and the introduction of new models continue to rise. However, the excitement is predominantly concentrated among a select few brands. Despite over 80% of automotive brands offering new energy products, why do their offerings struggle to make it onto the bestseller lists?

The crux of the problem lies in the dilemma of "gasoline and electric vehicles being inseparable." For instance, renowned new energy automakers and traditional automakers transitioning to new energy brands, such as Leapmotor, Li Auto, NIO, XPeng, Xiaomi, BYD, Geely Galaxy, Voyah, and Seres, are perceived as pure new energy brands.

Conversely, many more brands are traditional ones that have retained their gasoline vehicle product lines while loudly proclaiming their transition to electrification, such as MG, Haval, Hongqi, and Exeed. These brands are not considered pure new energy brands. Those that attempt to straddle both worlds often find themselves with low market and public attention when new energy vehicles are discussed.

This raises a pertinent question: In the new energy era, consumer perceptions have undergone a fundamental transformation. Young consumers are increasingly disenchanted with traditional brands that attempt to cater to all, preferring instead to opt for pure new energy brands that exclusively sell new energy vehicles to gain cutting-edge intelligent experiences.

In other words, consumers who purchase new energy products today naturally associate innovation, technology, and electrification with pure new energy brands that are unencumbered by legacy constraints. Electric vehicle models displayed alongside older gasoline models in traditional 4S stores lose the battle for consumer mindshare at the outset.

01 Natural Cognitive Disadvantages

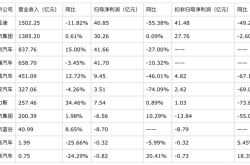

Based on this, this article has compiled a list of brand sales figures for brands that sell both gasoline and new energy vehicles. It becomes evident that these brands' gasoline vehicle products lack inherent popularity, and when they launch new energy products, consumers do not immediately associate these brands with innovation.

In fact, a previous report highlighted that when purchasing new energy vehicles, as high as 42% of young consumers prefer new brands that exclusively produce new energy vehicles; 29% choose traditional domestic brands; and a mere 5% opt for new energy vehicles from joint-venture brands. In other words, in the race toward electrification, pure "expert brands" wield overwhelming influence.

Why does attempting to cater to both gasoline and electric vehicles become a disadvantage? The core issue is the feeling of category blurriness in consumers' minds. When a new energy vehicle model is displayed in a showroom alongside a row of gasoline vehicles from the same brand, consumers experience significant cognitive confusion. Does this brand specialize in internal combustion engines or intelligent electric vehicles? Can it excel at both simultaneously?

This is why, in recent years, when people discuss joint-venture brand electric vehicles, they often think of generic electric vehicles. This difficulty in engagement applies equally to long-established domestic brands that have long operated in the gasoline vehicle market. Of course, today's joint-venture brand electric vehicles have also gained the strength to compete with Chinese brand electric vehicles.

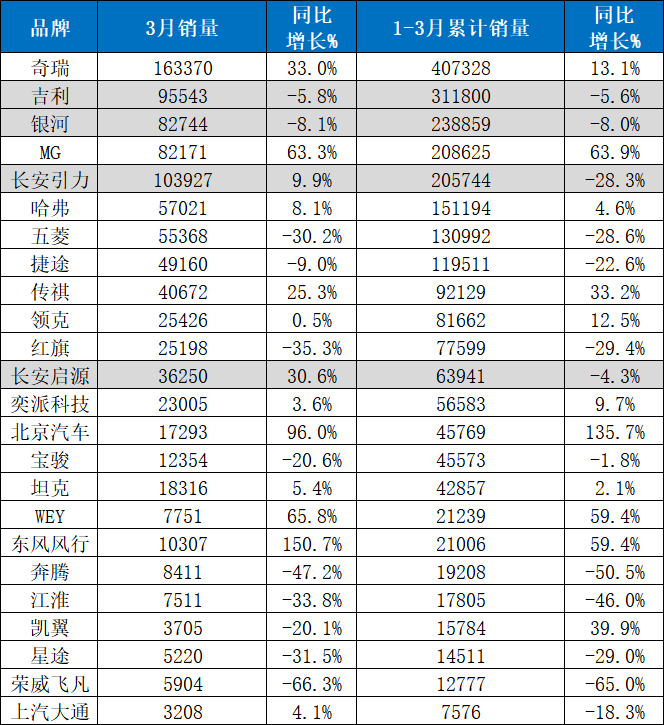

For example, the MG brand on the list has a best-selling model, the pure electric MG4, with average monthly sales exceeding 10,000 units over the past six months. However, MG actually sells three new energy models domestically, with the other two being the ES5 and Cyberster. The remaining three models are gasoline vehicles: the MG5, MG6, and MG7. So, do you remember these five models with lackluster sales?

Let's consider Wuling, a brand more familiar to many. The MINIEV and Bingguo series are its bestsellers. However, it's important to note that Wuling currently has 27 models on sale with sales statistics, covering pure electric, plug-in hybrid, and gasoline powertrains. So, how are models like the 560/730, Hongguang, and Xingguang faring?

In fact, there are quite a few brands in this predicament. If you've visited or paid attention to this year's Beijing Auto Show, you wouldn't find it difficult to notice that many brands' exhibition stands are filled with both gasoline and green-plated vehicles. Haval, Jetour, Trumpchi, Lynk & Co, Hongqi, Tank, and Wey all fall into this category.

Sales data also indicates that many brands attempting to cater to both gasoline and electric vehicles tend to experience a high start followed by a decline, becoming weaker over time. This is actually the fatigue of the mixed sales model during the market's winnowing phase. When intelligence and electrification become core factors in young people's car-buying decisions, mixed sales models simply cannot pass the screening process of the younger generation, who value both parameters and social circles.

This brings us to Geely Galaxy. Through the separation of gasoline and electric vehicles and the rapid launch of new products, Geely Galaxy has effectively cut ties with the gasoline-powered Geely Star series. This has created a clear cognitive distinction for consumers, resolving from the outset where to buy a car and whether to consider this brand.

At the critical juncture where new energy vehicles have shifted from early adopters to mass-market penetration, brands that mix gasoline and electric vehicle sales cannot gracefully exit the gasoline vehicle race nor regain recognition of their native identity in the new energy sector. They are being outperformed by pure electric new forces at every process node, and their sluggish sales are the most painful survival truth in the second half of the new energy era.

02 Greater Issues in Frontline Channels

Of course, many people will ask after seeing the data: Why has Geely Galaxy succeeded in this path while Changan Qiyuan and Chery Fengyun are still struggling? In fact, Geely Galaxy's ability to surge ahead, far surpassing Changan Qiyuan and Chery Fengyun, is not due to a single factor but rather a set of interlocking systems.

The essence of this system is to recreate a brand, and among its components, in addition to the automaker's strategic planning, frontline dealership channels are also a crucial factor. Because dealers are the key point of contact with consumers, their proactive engagement or enthusiasm determines whether consumers recognize the brand.

The dealership system relied upon by traditional automakers built a high moat during the golden age of gasoline vehicles. However, it is precisely this over-reliance on established paths that has trapped them in the game theory of co-locating gasoline and electric vehicles in the same store during the transition to new energy. Essentially, this comes down to two aspects: the capabilities of dealers and their profitability.

A survey shows that among automotive dealers, within the same 4S store, dealers are far less proactive in selling electric vehicles than traditional gasoline vehicles from the same brand. The reason is extremely simple: the profit margins differ vastly. A traditional brand dealer bluntly stated, "Especially if a brand's gasoline vehicles don't sell well, it can easily have a negative impact on the sales of electric vehicles."

For the vast majority of dealers, whose primary goal is profitability, selling a gasoline vehicle includes maintenance packages, high-priced parts, financial rebates, and long-term repair profits—all of which electric vehicle models simply cannot provide. Electric vehicles rarely require oil changes, spark plug replacements, or transmission fluid changes, and batteries are mostly warranted for eight to ten years, leaving dealers with almost no after-sales profit margins.

Under this business model, the traditional 4S store's strength in earning profits from after-sales and long-term services becomes ineffective. The more electric vehicles a dealer sells, the deeper losses they may incur due to the inability to generate sufficient income from new vehicle sales. In contrast, dealers for independent new energy brands achieve positive contributions from new vehicle sales, after-sales services, and financial insurance, with new vehicle profit contributions reaching 16.8%.

If the profit gap is the obvious issue, then dealers' mindset represents a deeper obstacle. The traditional dealer sales process is severely misaligned with the core demands of new energy vehicle users. Today's consumers are no longer passive recipients guided by salespeople; instead, they come with specific questions and seek scenario-based experiences to address pain points.

Sales consultants are accustomed to selling based on price and specifications, but consumers demand better car-viewing, purchasing, and ownership experiences. This is why many traditional dealers struggle when transitioning. If the mindset and thinking of frontline sales personnel do not change, they will find it difficult to meet consumers' new demands.

As a result, we can see that more and more dealers are joining cross-industry, higher-profile pure electric new brand dealership channels. Rather than continuing to endure hardship, they choose to start anew. This means that if traditional brands catering to both gasoline and electric vehicles do not undergo disruptive self-revolution in their channels, they will go from a sunk brand image to an exodus of their dealership network.

When dealers are skilled at selling gasoline vehicles and reap substantial profits, but find selling electric vehicles not only arduous but also less profitable than their peers in new force direct-sales channels by an order of magnitude, the internal resistance to transformation within traditional automakers naturally amplifies geometrically. If the dealership channel issues are not resolved, even the most advanced new platforms and ample R&D funding will remain castles in the air.

-

![]()

Samsung’s Home Appliance Business: A Seemingly Inevitable Decline

-

![]()

Zhipu’s GLM-5V-Turbo ‘Crosses the Rubicon’: The Dawn of a Domestic Multimodal Agent War

-

![]()

Doubao Introduces Charges: Fewer and Fewer Purely Free Large Models

-

![]()

Q1 Financial Reports Released: Cumulative Profits of Ten Automakers Lag Behind CATL

-

![]()

Can Doubao's Paid Subscription Model Succeed?

-

![]()

Understanding China Through DeepSeek's Triple Leap in Valuation

-

![]()

Samsung Home Appliances Exit China: A Strategic Withdrawal Rather Than a Forced Retreat

-

![]()

The Inseparable Dilemma of Gasoline and Electric Vehicles: A Challenge for New Car Sales